Global Healthcare Investment and Financing Report Q3 2017: Soaring Funding Volumes Amid Increasing Capital Rationality

According to statistics from the VCBeat database, global healthcare financing reached a new high in Q3 2017. The total financing amount for Q1–Q3 2017 has already surpassed the full-year total of 2016.

Key Points of the Report

In Q3, the total financing amount for healthcare companies both domestically and internationally increased, while the number of investment deals declined significantly.

The capital market is becoming more rational, as evidenced by greater diversification in investment areas and the concentration of capital in high-quality projects.

The average size of individual financing rounds, both domestically and internationally, has seen a substantial increase, which is also a result of capital concentration.

The healthcare and medical sub-sectors, both domestically and internationally, are gradually maturing, with financing rounds shifting significantly toward later stages.

From the perspective of financing rounds, overseas healthcare and medical sectors are at later stages compared to those in China.

The technology-driven digital health sector attracts more investment than the consumer-driven services sector.

In China’s digital health sector, the amount of investment capital has significantly decreased.

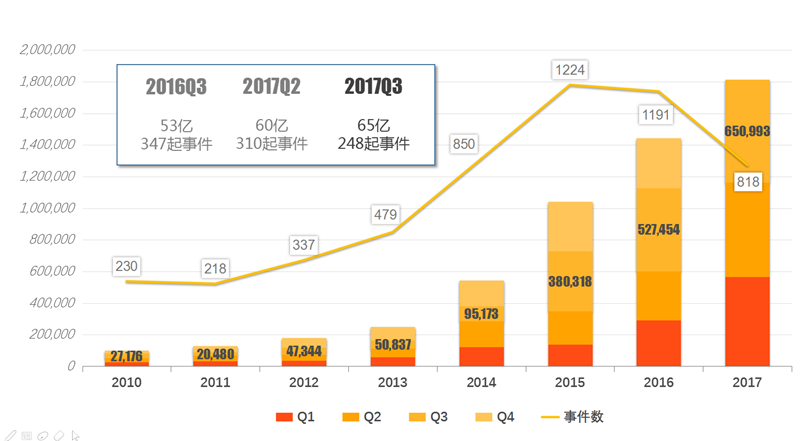

In Q3 2017, global healthcare industry financing totaled $6.5 billion.

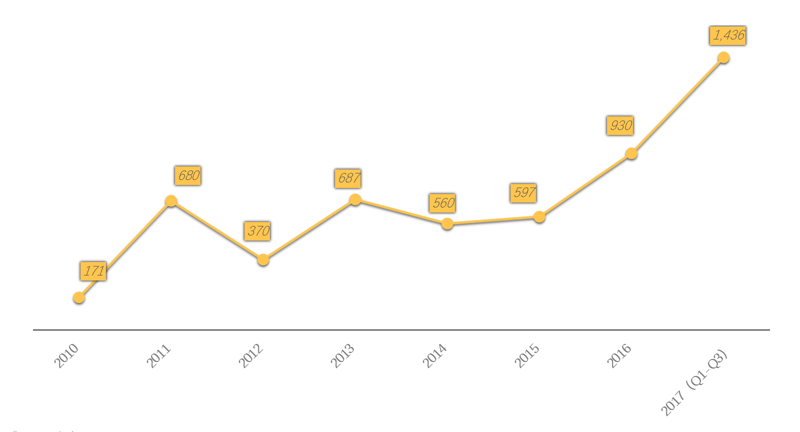

Since 2012, global healthcare market financing has experienced explosive growth, with a compound annual growth rate (CAGR) as high as 69%. Today, the healthcare sector has become the second most significant investment domain after TMT (Technology, Media, and Telecom).

In October 2017, VCBeat (WeChat ID: vcbeat) released a report on venture capital and financing in the global healthcare industry for Q3 2017. The report showed that there were a total of 248 transactions globally in Q3, with total funding reaching $6.5 billion, marking the highest quarterly financing amount on record. As of September 30, 2017, the total scale of financing in the global healthcare sector had already surpassed the full-year total of 2016.

Behind the Surge in Financing: A Rational Choice by Capital

2010–Q3 2017: Global Healthcare Industry Financing Trends (USD 10,000)

Although the financing scale this quarter reached a historic high, this does not imply that capital decisions were impulsive. In fact, the number of investment deals in Q3 saw a significant decline both year-over-year and quarter-over-quarter.

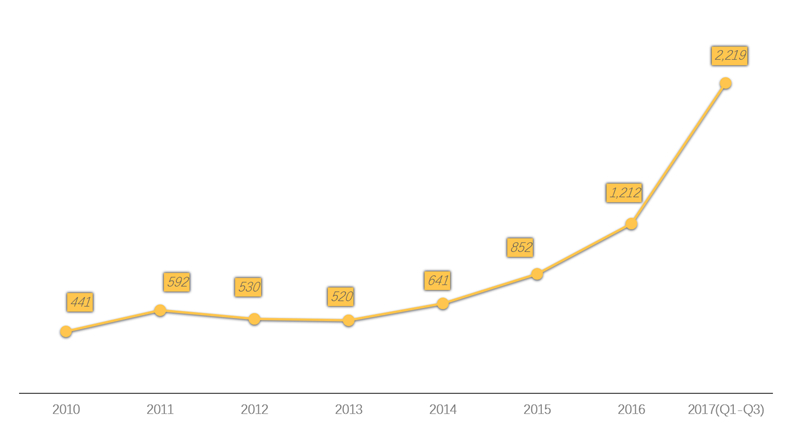

The increase in average deal size resulted in a higher total funding amount this quarter, despite fewer investment transactions.

2010–Q3 2017: Trend in the Average Amount per Investment Deal in the Global Healthcare Industry (USD 10,000)

According to the VCBeat database, the average financing scale reached $22.19 million in Q1–Q3 2017, significantly higher than the $12.12 million recorded in 2016.

A comparison with the full-year financing data for the healthcare industry in 2014, which saw 850 investment deals totaling $5.4 billion, reveals that Q3 2017 achieved a larger financing volume than the entire year of 2014, despite accounting for only 30% of the number of investment deals.This signifies a shift from the previous "scattergun" investment approach, with capital now strategically converging on high-quality, mature projects, as the capital market demonstrates a willingness to provide robust financial backing for high-value ventures.

A-round financing dominates, while angel and seed rounds decline

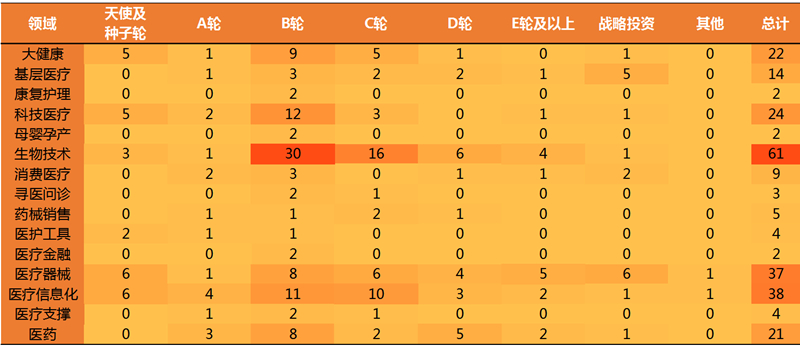

Q3 2017: Investment Hotspots in the Global Healthcare Industry

In Q3 2017, there were 96 Series A transactions in the global healthcare sector.It was the investment round with the highest number of transactions this quarter.. Its proportion reached as high as 39%, basically flat compared to the previous quarter.Angel and seed rounds decreased by nearly 20 deals compared to the previous quarter, marking a significant decline.

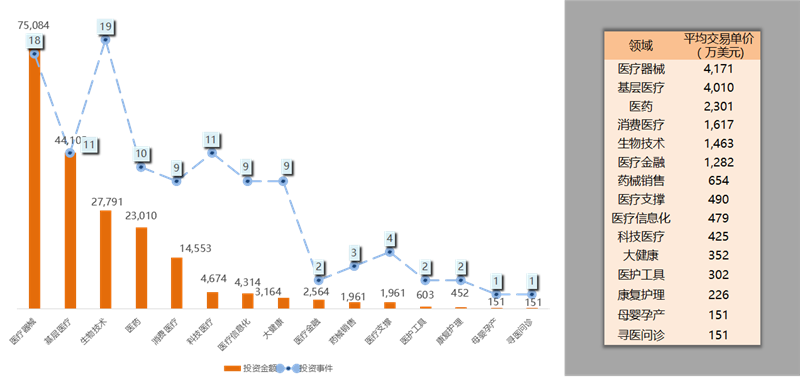

In the biotechnology sector, there were 61 financing events, accounting for 25% of the total, making it the most active area for investment and financing in the healthcare industry. Compared to the previous quarter, investment activities decreased in most sectors this quarter, with medical informatics experiencing the largest decline of 14 cases. As the hottest investment field last quarter, biotechnology continued to rank first this quarter, with seven more investment events than the previous quarter, marking the highest growth rate.

Q3 2017: Global Healthcare Sub-sector Financing Overview

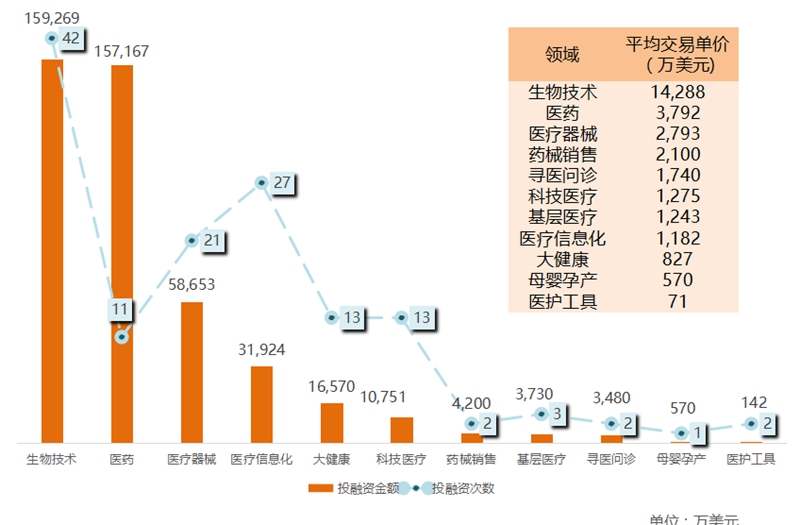

In terms of transaction value, the pharmaceutical sector recorded the largest financing scale, with a total transaction amount of $1.80177 billion in the third quarter. This sector also had the highest average transaction price, reaching $85.8 million per deal.

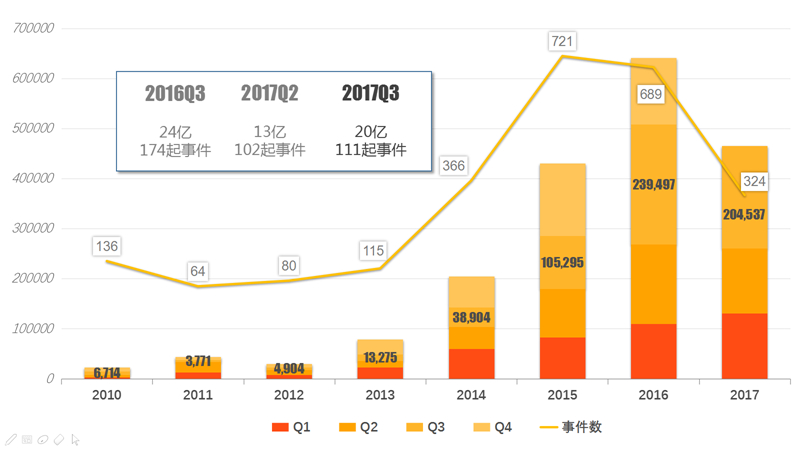

Focusing on the domestic market, there were a total of 111 financing events this quarter, amounting to $2 billion.

Financing Amount: Month-on-Month Increase, Year-on-Year Decrease

2010–Q3 2017: Financing Trends in China’s Healthcare Industry (USD 10,000)

In Q3 2017, total financing in the healthcare sector amounted to approximately $2 billion, representing a 9% year-on-year decrease and a 58% quarter-on-quarter increase. The growth in financing scale was primarily driven by capital markets’ heightened preference for traditional medical services and medical devices.

2010–Q3 2017: Change in Average Financing Amount in China’s Healthcare Industry (USD 10,000)

In terms of the amount per single transaction, the average financing amount in China is lower than the global average. Part of the reason lies in the differences in the main sub-sectors of investment and financing between domestic and international markets, as different sectors have varying requirements for financing scale.

What remains consistent is that the average size of individual financing rounds has increased significantly compared to the past. Both domestic and international capital markets are increasingly favoring mature projects in the healthcare sector.

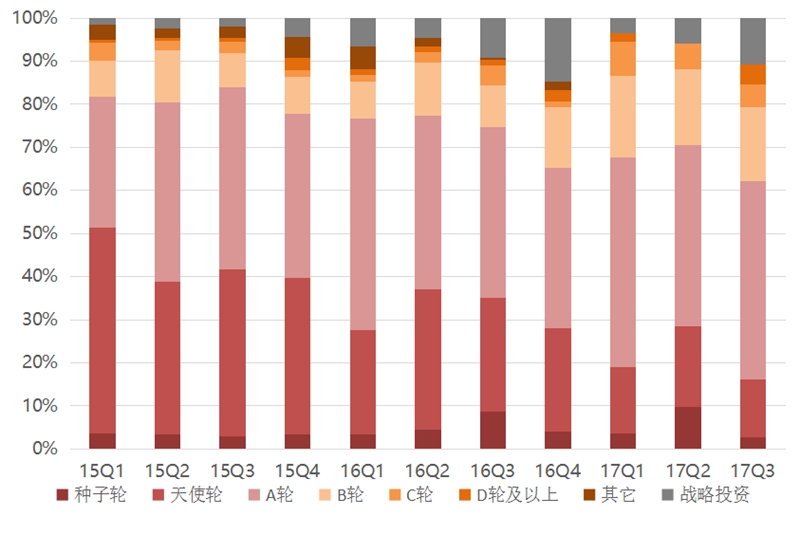

Seed and Angel Investment Deal Counts Decline Significantly

Q3 2015–2017: Changes in Financing Structure by Round

An analysis of funding rounds reveals that the proportion of seed and angel investments in the healthcare sector has decreased by more than twofold compared to Q1 2015. Currently, these early-stage transactions account for less than 17% of the total. This shift is primarily attributable to the maturation of many enterprises across various healthcare segments following two and a half years of development, which has led to diminished interest from capital markets in early-stage projects.

Digital Health: Cooling Investment Enthusiasm

Q1–Q3 2017: Changes in Investment Heat in China’s Digital Health Sector

We categorize the healthcare industry intoFour key sectors: digital health, traditional medical services, biological and pharmaceutical R&D, and medical devices. Among these, digital health refers to a novel, modernized approach to healthcare delivery that integrates modern computer and information technologies into the entire medical process; companies operating in this space span nearly all its sub-segments.

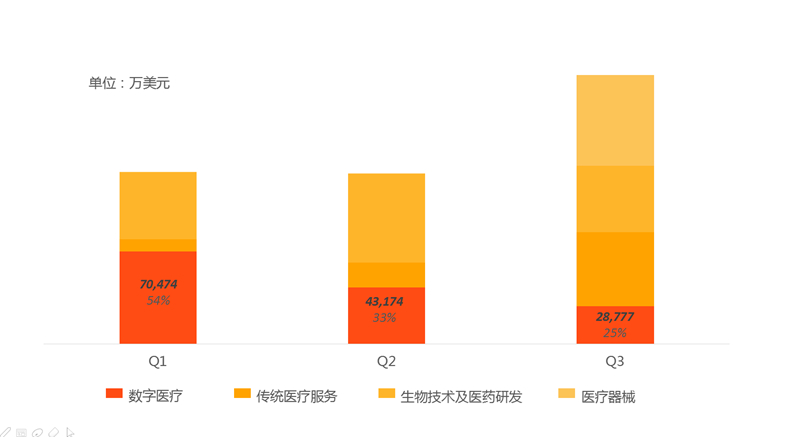

In fact, the rapid growth of the healthcare industry in the third quarter was primarily driven by increased investment interest in traditional medical services and medical devices. Taking medical devices as an example, in Q3 2017, United Imaging Healthcare received RMB 3.333 billion, the largest investment in China’s healthcare industry to date. (Although United Imaging Healthcare is involved in informatization, its core business focuses on medical devices; therefore, it is temporarily categorized under the medical devices sector rather than digital health.) This single investment accounted for more than 95% of the total investment in the medical devices sector for the quarter, significantly impacting the overall financing volume in this field. Meanwhile, the rapid growth in the traditional medical services sector was mainly attributed to heightened investment interest in primary care, which is partly related to the recent relaxation of national policies regarding clinics.

The digital health sector witnessed a notable decline, with its share of total funding dropping from 33% in Q2 2017 to 25% in Q3 2017. A significant contributing factor was the cooling investment sentiment in the healthcare informatization sector.

Technology-Driven Sectors Are More Popular Than Consumer-Driven Sectors

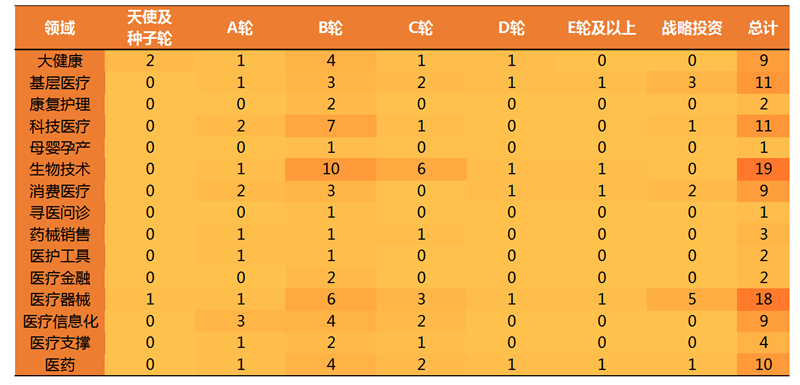

Q3 2017: Financing Status in Sub-sectors of China's Healthcare Industry

In terms of the distribution of investment enthusiasm across niche sectors,Certain extentTechnologyBarriersSubsectors, with relatively high investment enthusiasm in areas such as medical devices and biotechnology;andInnovative Service ModelsField, investment enthusiasm in sectors such as maternal and infant care and online medical consultation is declining. Taking online medical consultation as an example, there were 47 financing events in 2016, whereas only seven investment deals occurred in the first three quarters of this year, with just one deal in the third quarter.The only companies in the “Maternal and Infant Care” and “Online Medical Consultation” sectors to secure funding this quarter were Wen'er Diagnostics and Dajia TCM, respectively.

Service InnovationField,Compared to the technical field'sIndustryHigh MaturityProduct homogenization among enterprises is severe, with low entry barriers and strong replicability. Fueled by capital injections, these companies can grow rapidly; once industry giants emerge, the resulting homogenized products and services make it difficult for smaller players to survive. After two years of frenzied fundraising, certain consumer-driven service sectors may have already established a degree of monopoly. If new entrants in these fields fail to differentiate themselves from homogeneous market offerings, the cooling trend in the capital markets is likely to persist.

Biotechnology and medical devices lead in transaction volume

2017Q3: Investment Hotspots in China's Healthcare Sector

Among the 15 investment subsectors, the biotechnology and medical device sectors recorded the highest number of transactions, accounting for 33% of total financing events. AndPrimary healthcare and pharmaceuticals are the most sought-after sectors with the fastest growth; investment enthusiasm in the medical informatics sector has declined the most rapidly.

Compared with the previous quarter,Although the total number of investment deals decreased this quarter, the majority of sectors saw an increase in transactions. This indicates thatInvestment sectors this quarter were more diversified, reflecting a gradual rationalization of capital.

In terms of investment rounds, Series A transactions were the most frequent, with 51 deals accounting for 46% of the total number of events, a proportion that remained basically flat compared to the previous quarter.

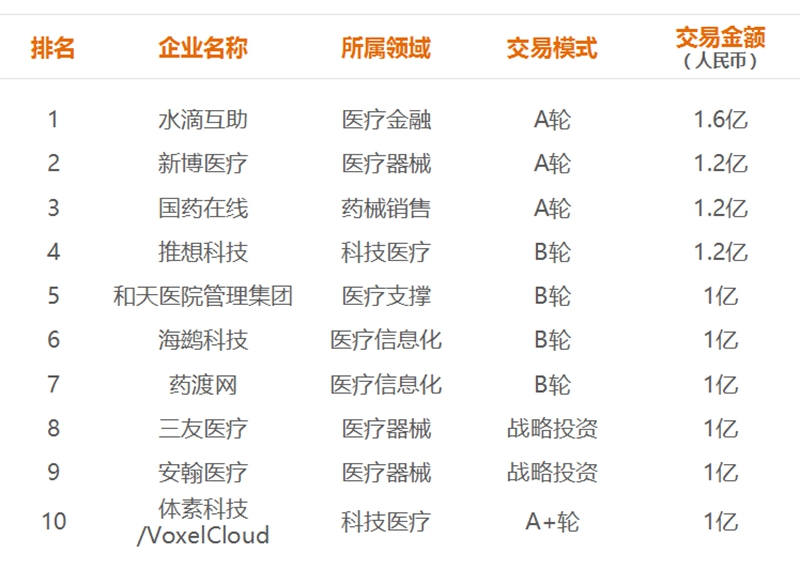

Financing Projects Become More Concentrated, with an Increase in High-Value Deals

Q3 2017: Top 10 Most-Funded Companies in China’s Healthcare Industry

United Imaging Healthcare Secures RMB 3.333 Billion in Series A Financing, Marking the Largest Primary Market Fundraising Deal in China’s Healthcare Sector to Date

The pharmaceutical sector and primary healthcare topped the list, with the former concentrated in post-Series D rounds and the latter more focused on earlier investment stages.

Compared with Q2 2017, the concentration of financing and investment in the Top 10 list increased this quarter.

In Q3 2017, the most active healthcare investment firm was Qiming Venture Partners, with seven investment deals.Other active institutional investors include CITIC Securities, Shenzhen Capital Group, and others.

Digital healthcare sector leans toward early- to mid-stage Series A and B financing rounds.

Q3 2017: Top 10 Most-Funded Digital Health Companies in China

Compared to the top rankings in the broader healthcare industry, the top rankings in the digital health sector are dominated by companies at early to mid-stages securing Series A and B funding, reflecting lower levels of corporate and industry maturity.AlthoughInvestment in this sector declined this quarter, but the industry’s relative immaturity suggests that significant opportunities will continue to emerge in the future.

This quarter, there were 137 overseas investment deals, with total financing amounting to $4.5 billion. Compared to the previous quarter, the number of financing deals decreased by more than 33%, and the total financing amount also saw a slight decline.

Overseas capital markets favor technology-driven sectors

Q3 2017: Financing Status in Overseas Healthcare Subsectors

In terms of fundraising momentum, biotechnology is the most sought-after sector, with a higher number of investment and financing events than any other field.

The pharmaceutical and healthcare sector recorded the highest total financing amount as well as the highest average financing per deal.

Overseas investment events are more inclined toward technology-driven niche sectors.

Biotechnology and Pharmaceuticals Demonstrate Stronger Capital Attraction

Q3 2017: Top 10 Overseas Healthcare Investments

Roivant in the pharmaceutical sector secured $1.1 billion in angel funding, marking the largest overseas financing round this quarter.

The biotechnology and pharmaceutical sectors demonstrate the strongest capital absorption capacity, accounting for 70% of the top rankings.

The overall investment and financing levels of the top overseas healthcare companies are higher than those of their domestic counterparts, while the distribution of key sectors among the top-ranked companies is largely similar to that seen in China’s financing rankings.

Overseas Digital Health Sector Is More Mature

Q3 2017: Top 10 Most Funded Companies in the Overseas Digital Health Sector

Unlike China’s top digital health rankings, which are dominated by Series A and B financing rounds, all companies on the overseas top digital health list have secured Series B or later funding. This indicates that the overseas digital health sector is more mature, suggesting significant growth potential for China’s digital health industry in the future.