Startup Health Q3 2017 Digital Health Funding Report: Annual Investment on Track to Reach $10 Billion, Chinese Healthcare Companies Show Strong Momentum

Startup Health is one of the most influential digital health startup accelerators globally, with a current portfolio comprising 200 companies across five continents, 18 countries, and more than 60 cities. The various reports and rankings it regularly publishes have consistently garnered widespread attention from all sectors of the industry.

As soon as the third quarter of 2017 concluded, Startup Health released its Q3 2017 Financing and Investment Report (with data current as of September 30, 2017). VCBeat (WeChat ID: vcbeat) brings you the full translation of the report without delay; see below for details.

One of the most exciting trends in recent years has been a cohort of entrepreneurs, leaders, and investors focusing on various bold “Health Moonshots.” StartUp Health is organizing and supporting its portfolio companies in achieving the following 10 “Health Moonshots,” dedicated to improving global human health from every angle.

These 10 “Health Moonshot Initiatives” are:

1. Universal Care Access Program. Provide high-quality care to everyone, regardless of location or income;

2. Healthcare Cost Reduction Plan. Fundamentally reduce healthcare costs;

3. Disease Cure Plan. Achieving disease cures through big data, new technologies, and personalized medicine;

4. Cancer Plan. The fight against cancer will continue;

5. Women's Health Initiative. Focus on women's health, including preventive care and new research;

6. Child Health Program. Ensure that every child has access to high-quality care, particularly in underdeveloped regions;

7. Nutrition and Fitness Plan. Provide a healthy environment to support an active lifestyle;

8. Brain Health Program. Explore the mysteries of the brain and improve brain health;

9. Mental Health Plan. Acknowledge the importance of mental health, and reconnect mind, body, and spirit;

10. Longevity Plan. Extend everyone's lifespan by 50 years.

Digital Health Funding Shatters All Previous Records in Q3: Year-to-Date 2017 Funding Surpasses $9 Billion

If this momentum continues into the fourth quarter, total annual funding is expected to reach $10 billion.For entrepreneurs dedicated to achieving the “Health Moonshot,” this is undoubtedly an encouraging signal.

Despite the constant stream of headlines on healthcare reform in recent times, which has heightened uncertainty within the industry, investment in digital health companies continues to accelerate.

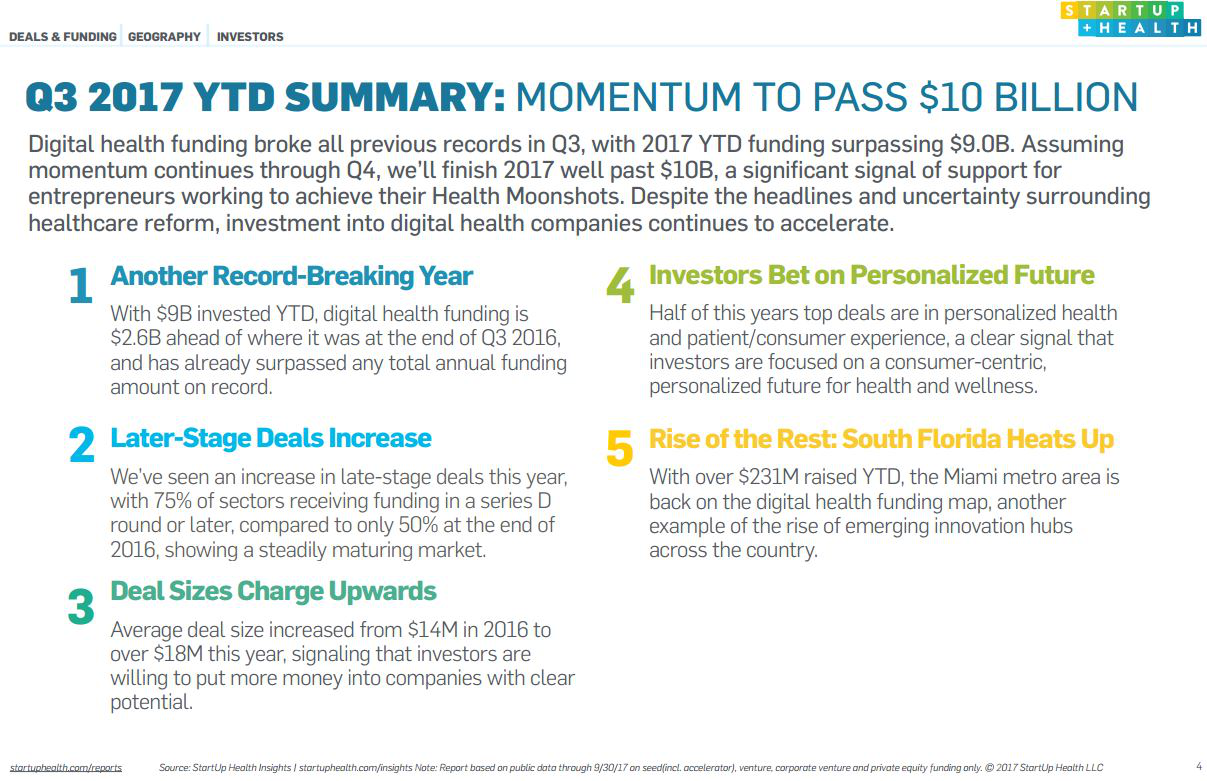

1. Total Investment and Financing Amount Hits New Record High

From the beginning of 2017 through Q3, digital health financing and investment reached $9 billion, $2.6 billion higher than at the end of Q3 2016, breaking the previous record for total annual funding during the same period.

2. Increased transactions in the mid-to-late stages

By the end of 2016, only 50% of transactions occurred at Series D or later; this year, the proportion of late-stage deals has risen to 75%, indicating that the market is gradually maturing.

3. Large-value transactions are on the rise

In 2016, the average deal size was $14 million, whereas this year, that figure has risen to $18 million, indicating that investors are more willing to channel capital into companies with more pronounced growth potential.

4. Personalized Medicine Is More Favored

More than half of this year’s mega-deals were concentrated in subsectors such as “personalized medicine” and “patient/consumer experience,” indicating that investors are focusing on patient-centric companies in the healthcare and health sectors that advocate for personalized medicine.

5. Emergence of New Investment Hotspots

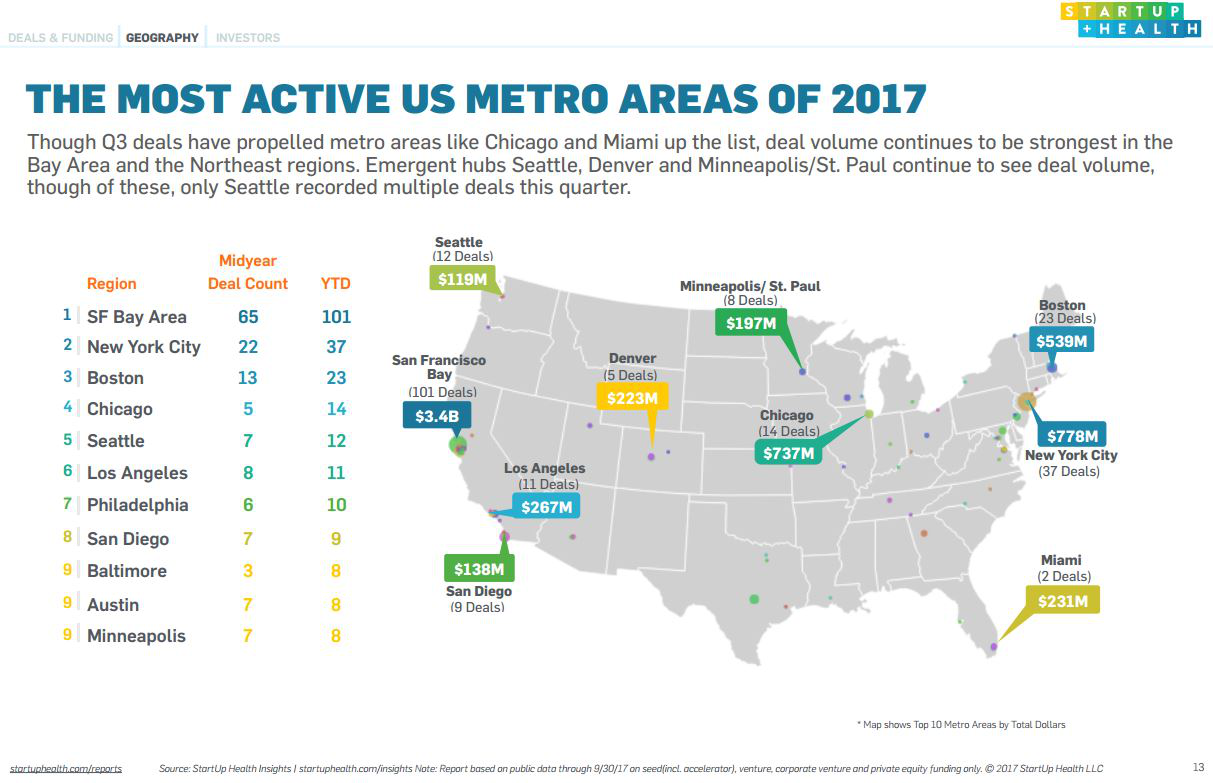

Since 2017, the Miami metropolitan area has attracted $231 million in financing and investment, positioning it as a leader among emerging digital health innovation hubs across the United States and firmly re-establishing its status as a key hotspot for investment.

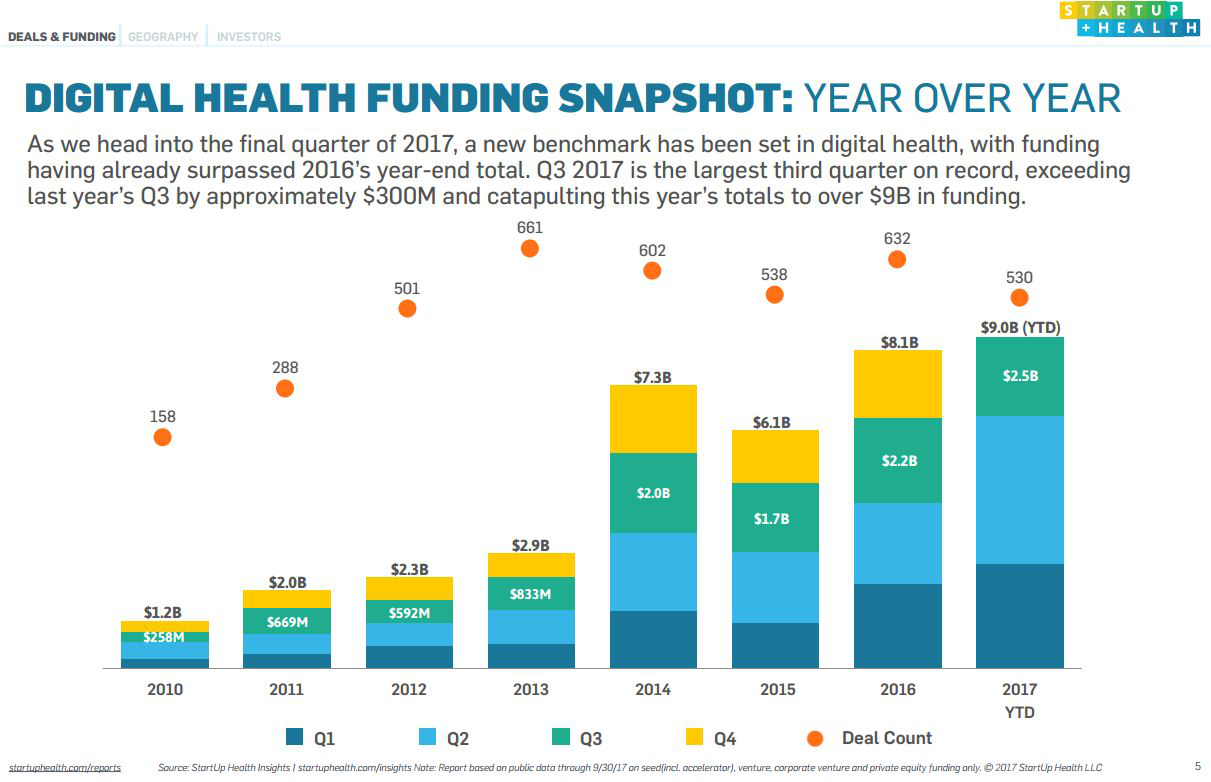

Annual Data Analysis:As we enter the final quarter of 2017, year-to-date investment and financing in the digital health industry has already surpassed the full-year total of $8.1 billion in 2016, marking a new benchmark for the sector.

Q3 2017 was the highest-funded third quarter on record, with $2.5 billion in financing, significantly surpassing the $2.2 billion raised in Q3 of the previous year and bringing the total for the first three quarters of the year to $9 billion.

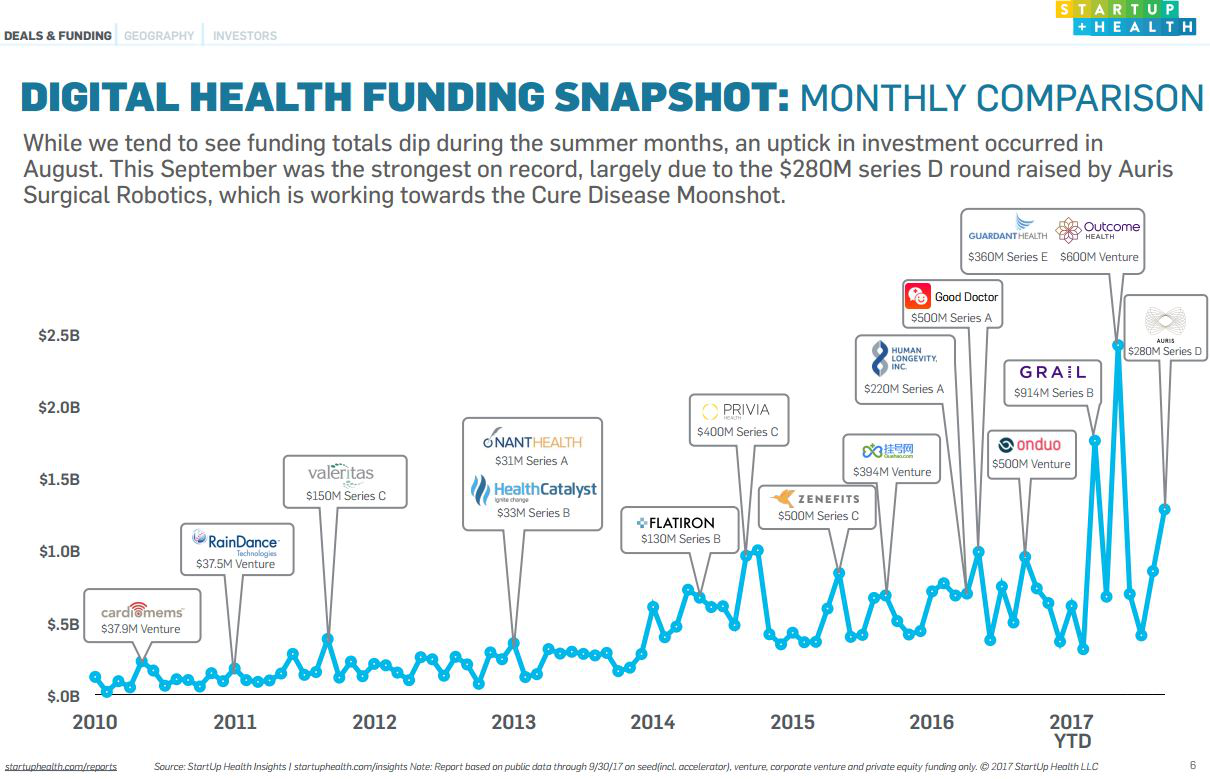

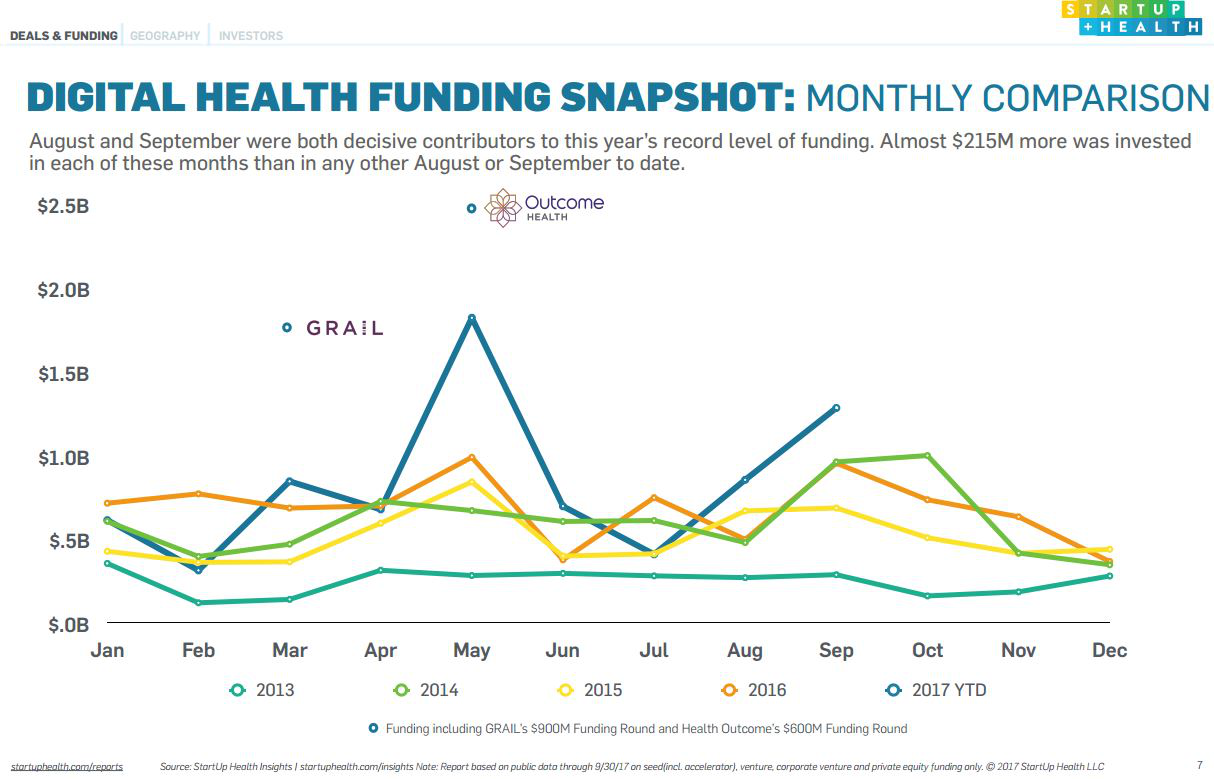

Monthly Data Analysis:In July 2017, total investment funding in the digital health sector declined compared to the previous period, but rebounded in August.

August and September were the decisive factors in achieving record-breaking investment and financing volumes this year. Compared with the same months in other years, the investment amounts secured in August and September 2017 were each approximately $215 million higher.

This September set the strongest investment and financing record in history, with Auris Surgical being the main contributor. The company’s Series D funding round alone reached $280 million. Auris Surgical is dedicated to researching surgical robots, which is also part of the “Cancer Moonshot” initiative.

The deal sizes for digital health startups worldwide are growing larger. Compared with the first-half report, companies that completed large-scale financing in Q3 include Auris (ranked 5th, medical devices subsector, $280 million), 23andMe (ranked 6th, personalized medicine subsector, $250 million), Haodf Online (ranked 8th, $200 million), and WuXi NextCODE (ranked 9th, a new entity established after WuXi AppTec acquired NextCODE Health, personalized medicine subsector, $165 million).

Compared with the first-half report, the digital medical equipment subsector has made a strong entry into the rankings, securing the top three positions.

In Q3 2017 alone, the “Digital Medical Devices” subsector secured over $585 million in investment, bringing its year-to-date total to $1 billion. This figure ranks third, trailing only “Big Data/Analytics” at $1.3 billion and “Personalized Medicine” at $1.2 billion. Furthermore, it remains one of the most active subsectors in terms of deal volume.

Although“Big Data/Analytics” sub-sector remains firmly in first place, with its position still high, but it recorded only 13 deals this quarter, with a total financing and investment amount of $138 million.

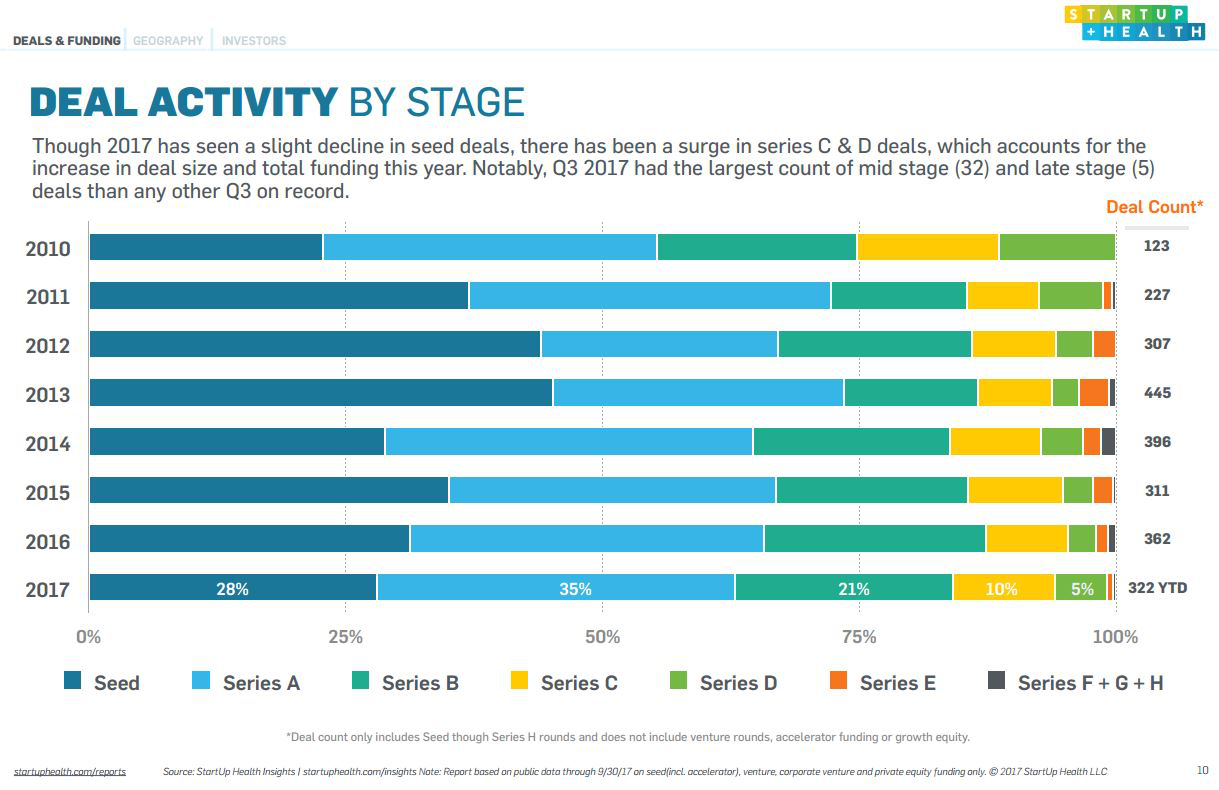

There have been 322 transactions from 2017 to date. Although the volume of seed-stage deals declined slightly in 2017, the number of Series C and D financing rounds increased, indicating that both the deal size and total funding amount rose this year. Notably, the third quarter of 2017, compared with the third quarters of other years,Mid-term (32 transactions) and late-stage (5 transactions) deal volumes were significantly higher.。

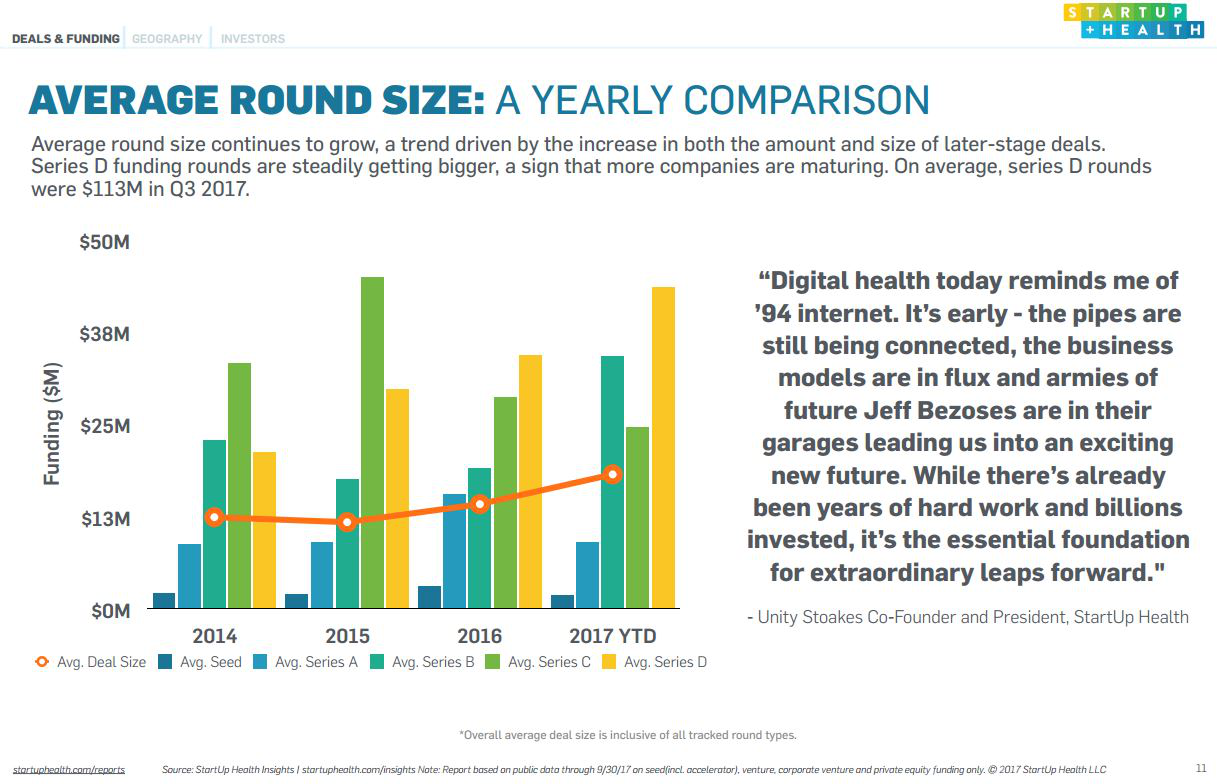

As shown in the figure, the average financing size in the digital health sector has been on a continuous upward trend in recent years; when broken down by financing rounds, both the number of transactions and the amounts in later-stage rounds have been increasing.

Specifically, Series D financing rounds are gaining momentum, with $113 million raised in Q3 2017, indicating that digital health companies are becoming increasingly mature.

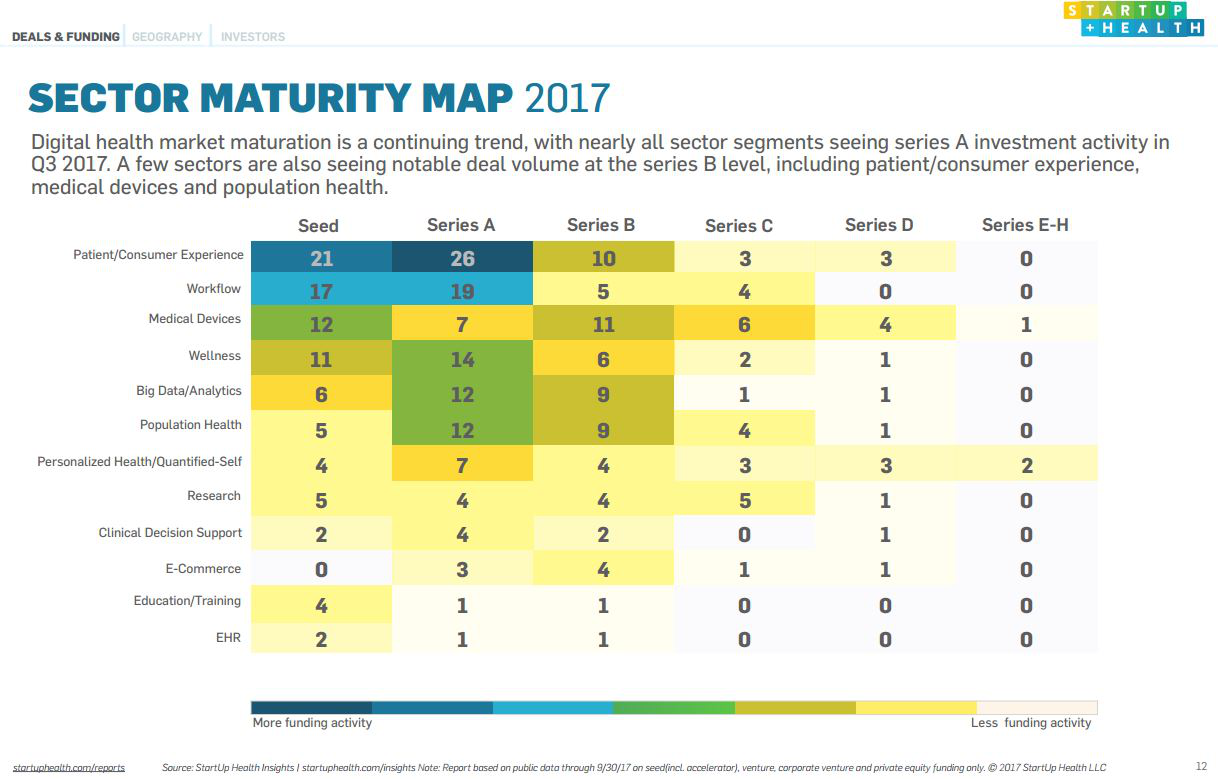

The maturation of the digital health market is an ongoing trend. As shown in the figure, all subsectors listed experienced Series A and Series B financing activities in the third quarter of 2017.

Among the top-ranked categories are “Patient/Consumer Experience” (26 and 10 deals in Series A and B financing, respectively), “Workflow” (19 and 5 deals), “Medical Devices” (7 and 11 deals), “Health” (14 and 6 deals), “Big Data/Analytics” (12 and 9 deals), and “Population Health” (12 and 9 deals).

As the rankings show, although metropolitan areas such as Chicago (9 deals, $737 million) and Miami (2 deals, $231 million) have demonstrated a strong presence in the digital health sector since 2017, they have yet to displace the traditionally dominant San Francisco Bay Area and Northeast regions.

In emerging digital health innovation hubs such as Seattle, Denver, Minneapolis, and St. Paul, transaction volumes continued to rise; however, this quarter saw no more than one deal in any of these markets except Seattle, which recorded five deals in Q3.

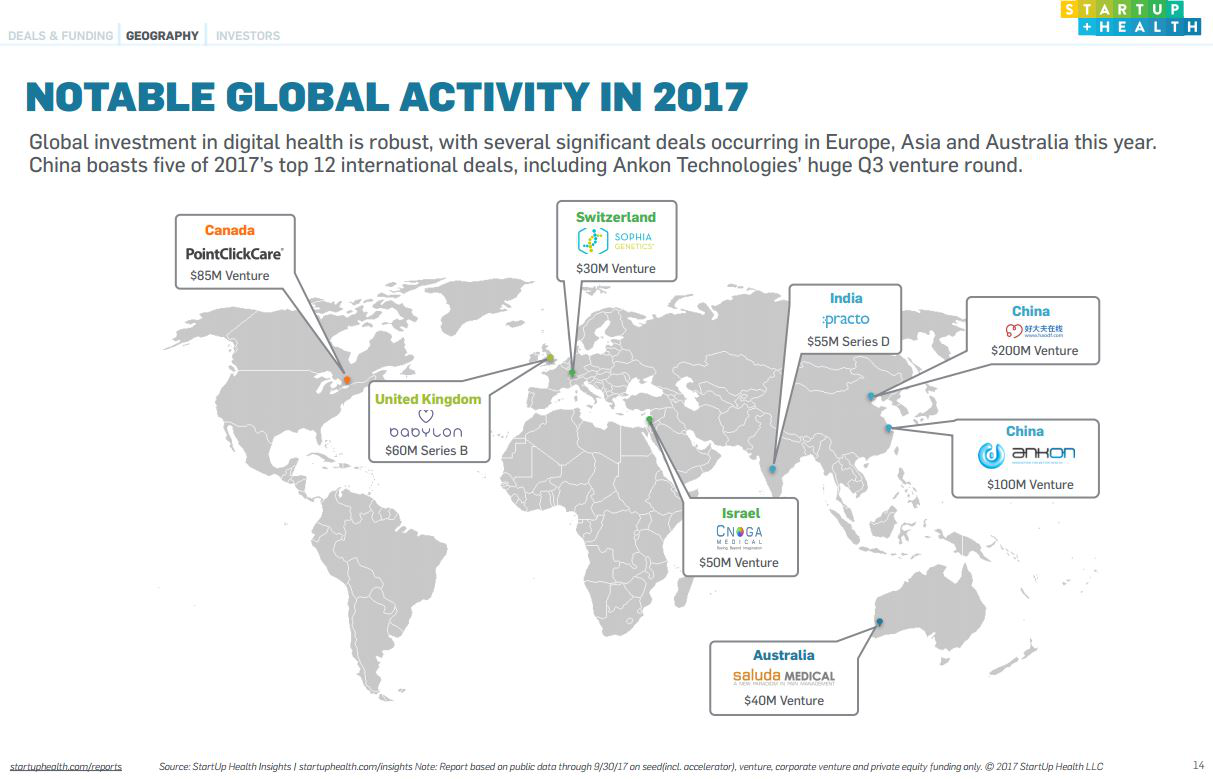

In 2017, global investment in digital health remained robust, with several major deals closed across Europe, Asia, and Australia. Notable examples include Haodf Online in China (Series D, $200 million), PointClickCare in Canada (venture capital, $85 million), Babylon in the UK (Series B, $60 million), Practo in India (Series D, $55 million), Cnoga Medical in Israel (venture capital, $50 million), and Saluda Medical in Australia (venture capital, $40 million). These transactions underscore the comprehensive global expansion of digital health financing and investment.

Notably,Of the first 12 international transactions from 2017 to date, China accounted for five., including Ankon Technologies’ $100 million Series C financing round in Q3.

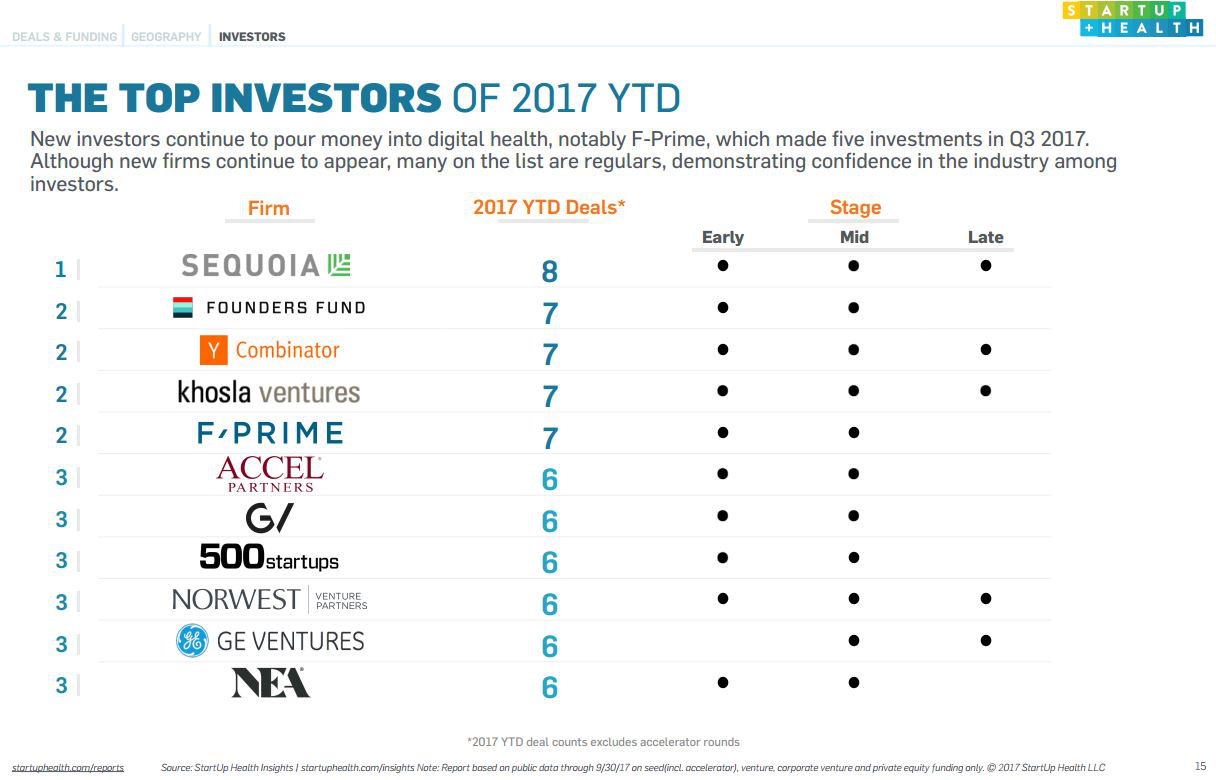

In terms of overall transaction volume, similar to the first-half report, new investors continue to emerge and inject capital into the digital health sector. Of particular note is F-Prime Capital, headquartered in Cambridge, Massachusetts, which made five investments in the third quarter of 2017 alone, ranking second on the leaderboard with seven year-to-date transactions.

Although new entrants continue to emerge, most companies on the list remain familiar names, indirectly reflecting investors’ confidence in the industry.

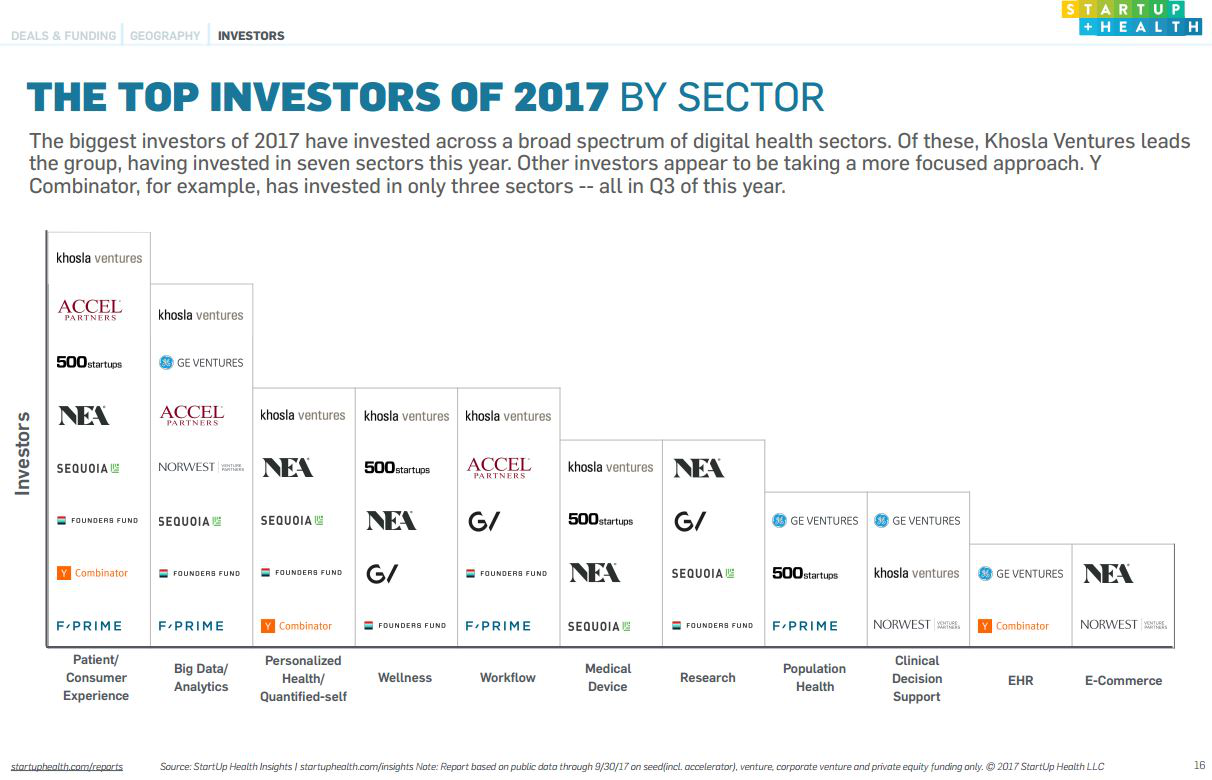

In terms of investment across various sub-sectors, in 2017, some investors distributed their investments broadly across the digital health industry. Khosla Ventures took the lead, investing in seven sub-sectors this year, including “Patient/Consumer Experience,” “Big Data/Analytics,” “Personalized Medicine/Self-Quantified Health,” “Wellness,” “Workflow,” and “Medical Devices.”

In contrast, some other investors appear to be embracing the strategy of concentrated investment. For instance, Y Combinator invested in only three subsectors—“Patient/Consumer Experience,” “Personalized Medicine/Self-Health Quantification,” and “EHR”—with all investments completed in the third quarter of this year.

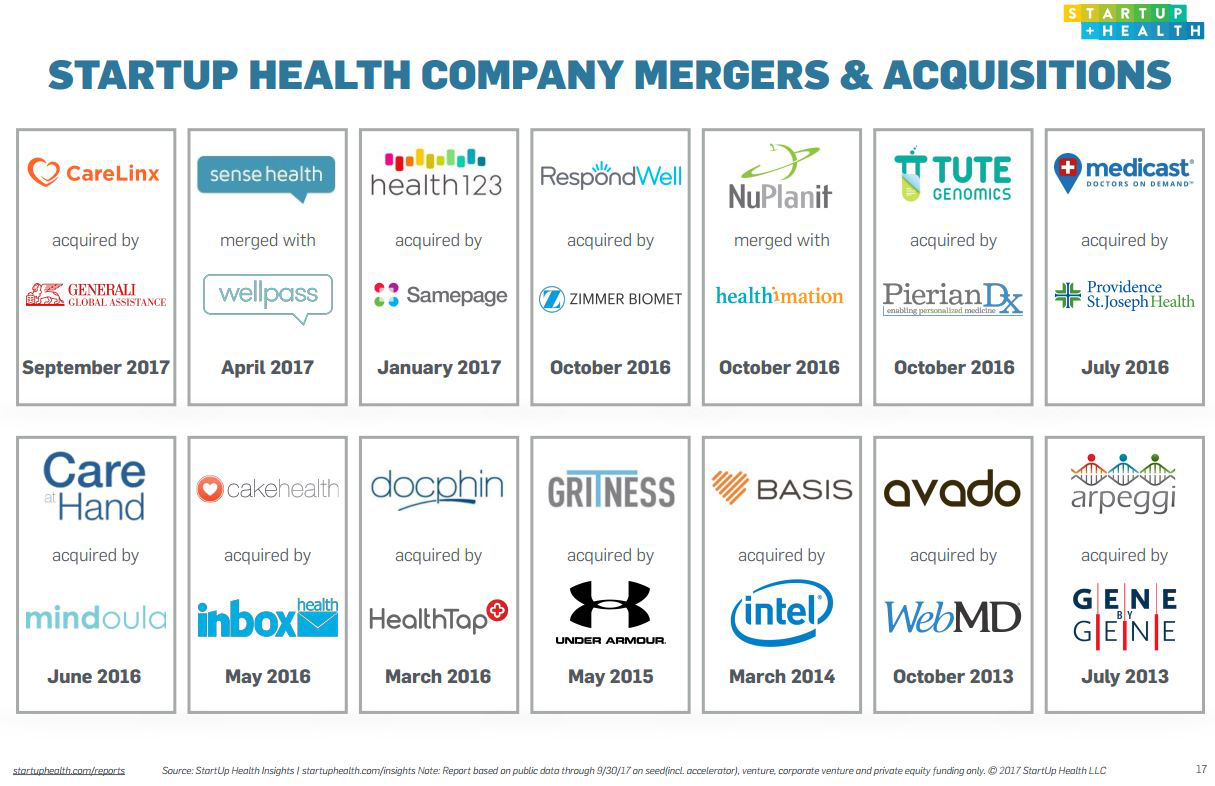

As shown in the figure, Startup Health portfolio companies completed three M&A transactions in 2017: Same Page acquired Health 123 in January; Wellpass merged with Sense Health in April; and Generali Global Assistance acquired Care Links in September (Q3).