Over $3 Billion Raised! Decoding the Investment Logic Behind the Tumor Testing Boom

In recent months, the field of clinical oncology testing has seen frequent financing activities. Feishuo Biology secured nearly RMB 40 million in its latest funding round, Youxun Medicine raised RMB 170 million in its Series A round, Geneseeq obtained hundreds of millions of RMB in its new financing round, and Annoroad Gene Technology raised nearly RMB 700 million. Additionally, according to VCBeat, two other companies have announced successful fundraising, with amounts reaching hundreds of millions of RMB.

Tens of millions at a minimum, often exceeding hundreds of millions: What does the frenzy of corporate fundraising signify, and how will the industry evolve?

From a regulatory perspective, with the precedent set by NIPT, the approval and management procedures for clinical oncology testing now appear to have a reference point. Following large-scale financing rounds, will the industry enter a phase of orderly development akin to that of NIPT? Are these companies securing funding in anticipation of an imminent market boom, or is this strategic positioning before the storm?

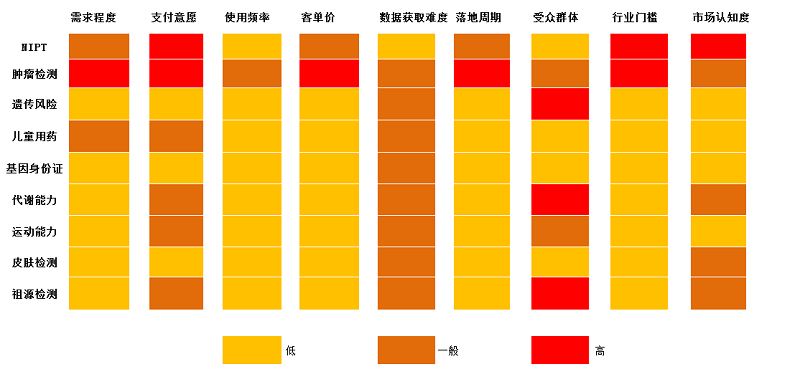

If the entire genetic testing landscape is divided into three segments, clinical testing—represented by NIPT and tumor liquid biopsy—occupies the inner circle, while health management and pan-entertainment testing reside in the second and third circles, respectively. Compared to the other two categories, clinical testing is far more rigorous and has higher entry barriers. The majority of large-scale financing activities also take place within this segment.

The industry has high barriers and strict regulation. If the goal is a faster return on investment, mass-market products would seem to offer quicker results. So why are investors pouring substantial capital into this sector? Let’s examine this model.

This model uses the industry average as the benchmark.

A product’s ability to gain a foothold in the market is closely tied to the level of market demand. Is there genuine demand? Are there substitute products available? Are customers willing to pay? Only by answering these questions can a talented product (“Qianlima”) find its discerning investor or partner (“Bole”). Meanwhile, the size of the product’s market is correlated with the size of the target audience, the frequency of product use, and users’ willingness to pay at given average transaction values.

Compared to NIPT, cancer testing represents a larger market

This model indicates that non-invasive prenatal testing (NIPT) and oncology (including early cancer screening and clinical cancer diagnostics) are relatively ideal sectors. NIPT has a shorter implementation cycle and lower technical barriers, allowing this field to mature prior to clinical cancer diagnostics. However, compared with NIPT, liquid biopsy for oncology targets a broader population and addresses more urgent clinical needs.

Among alternative products, clinical techniques similar to NIPT include traditional Down syndrome screening and amniocentesis. Traditional Down syndrome screening has lower accuracy, while amniocentesis carries higher risks; in comparison, NIPT technology offers superior advantages.

However, NIPT targets only individuals who are preparing for pregnancy or are currently pregnant, resulting in a relatively small target audience and low usage frequency; thus, the overall market size is not particularly large. Furthermore, as NIPT testing does not involve subsequent therapeutic interventions, it is difficult to establish a closed-loop industry ecosystem.

In contrast, for tumor detection, other clinical methods include radiology, biochemical testing, pathology, histology, and mass spectrometry. However, apart from tissue biopsy, no technology is capable of performing molecular- and genetic-level detection or analysis of tumors. Yet, tissue biopsy is highly invasive; therefore, it is not a practical approach for monitoring drug response and tumor recurrence during or after treatment.

Furthermore, as cancer is a complex disease, clinical diagnosis and treatment often require the combined assistance of multi-omics approaches, including radiology, pathology, and histology. In other words, tumor genetic testing does not stand in complete competition with other diagnostic modalities, which is fundamentally different from the relationship between NIPT and traditional Down syndrome screening.

More importantly, liquid biopsy for tumors involves subsequent treatment and monitoring after detection, with downstream applications, resulting in a significantly higher frequency of use and a larger target population compared to NIPT.

As for other pan-entertainment and health monitoring sectors, although building robust industry barriers would require significant effort in certain areas, the current entry thresholds remain low. With numerous market participants, consumers struggle to differentiate between products, making price wars highly likely.

The Logic Behind the Frenzy of Capital Accumulation

For technology-driven companies, both product commercialization and scaling require substantial capital. The 2015 lung cancer diagnosis guidelines have already included liquid biopsy as an indicator, meaning it is a product that has been recognized and accepted by the clinical community. A casual visit to the website of any liquid biopsy company reveals that nearly all of them promote and introduce clinical-grade products (with the exception of early screening tests).

But have these companies’ products truly been commercialized? In fact, not yet.

Currently, all enterprises adopt a service-oriented model, engaging in scientific research collaboration and services with hospitals either through joint establishment or as third-party service providers. Enterprises are prohibited from entering into commercial partnerships with hospitals or supplying substantive products.

In the 2014 “Suspension Notice,” in addition to targeting NIPT, clinical-grade oncology testing products were also suspended. Subsequent pilot program documents included pilots for oncology as well. During this period, regulatory oversight for oncology testing and non-invasive prenatal testing remained synchronized. However, while NIPT test kits subsequently received successive approvals and the NIPT pilot programs were discontinued, there were no new developments in the regulation of oncology testing.

Commercialized clinical testing must meet two requirements: the testing institution must hold qualifications as a third-party medical laboratory, and the instruments, reagents, and consumables used in the testing process must be approved by the China Food and Drug Administration (CFDA). Currently, most companies engaged in tumor testing have obtained third-party medical laboratory qualifications, and some instruments have received market approval. However, the CFDA has not yet approved any diagnostic kit products from enterprises, and the pilot program has not been discontinued.

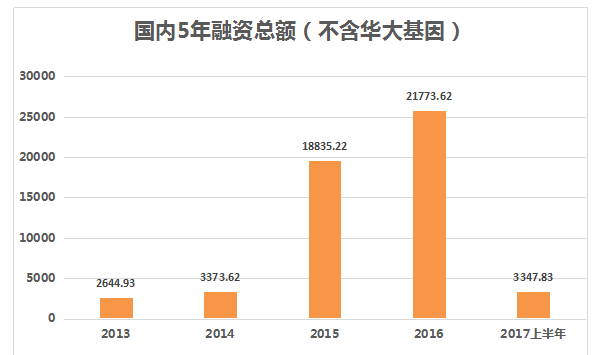

Certainly, this was not due to the CFDA’s rejection of the technology, but rather stemmed from the inherent complexity of tumors. The fact that regulatory classification had already begun indicated that final approval would ultimately be granted. Consequently, capital inclined toward early-stage projects began to position itself during this period. As a result, total financing in this field saw a sharp surge in 2015 and 2016.

Image sourced from VCBeat's investment and financing report, June 2017

On the other hand, with no product yet commercialized, the timeline for CFDA approval remains uncertain. Consequently, some investors are adopting a wait-and-see approach.

CFDA Releases Positive Signals, Second Wave of Financing Boom Arrives

Currently, no company’s NGS-based tumor detection kit has received approval from the China Food and Drug Administration (CFDA). Similar to the market landscape of non-invasive prenatal testing (NIPT) at that time, the first company to secure regulatory approval will undoubtedly gain a first-mover advantage.

As early as 2015, several industry-leading companies, including Burning Rock Biotech and Novogene, had already submitted applications for their test kit products to the China Food and Drug Administration (CFDA). However, it was not until the end of 2016 that the CFDA began to send positive signals.

In September 2016, Burning Rock Biotech’s kit products were the first to be approved by the Center for Medical Device Evaluation of the China Food and Drug Administration (CFDA) to enter the “Special Approval Procedure for Innovative Medical Devices.” This news was not only exciting for Burning Rock Biotech but also a tremendous boon for the entire industry: regulatory authorities had finally accepted the application!

This signal has also reignited a wave of fundraising enthusiasm in the industry. Some institutions that had previously been on the sidelines have begun to accelerate their strategic investments.

As of September 2017, there had been more than 15 financing events in this sector, with a total funding amount exceeding RMB 1.3 billion. Including Annoroad Gene Technology’s latest round of financing, the total funding for this sector this year has reached approximately RMB 2 billion, with several large-scale financing deals yet to be disclosed.

A review of financing news for liquid biopsy companies this year reveals that most have mentioned the regulatory submission of “diagnostic kit” products. VCBeat considers this a signal of a shift in business models among large-scale enterprises; currently, all known companies are engaged in the submission or preparation for submission of diagnostic kit products. Among them, Burning Rock Biotech, Novogene, Geneseeq Technology, Amoy Diagnostics, and Fushuo Biology have had their diagnostic kit products enter the CFDA’s Special Approval Procedure for Innovative Medical Devices.

Data source: Center for Medical Device Evaluation, China National Medical Products Administration

Previously, nearly all enterprises adopted a service-oriented model, either by establishing laboratories in collaboration with hospitals or through partnership arrangements wherein hospitals provided samples for corporate testing.

What if the kit is offered as a product? The single-service model would evolve into a “service + product” model. In addition to providing testing services to hospitals, companies can also distribute products. Hospitals with the necessary capabilities and qualifications may purchase instruments and reagents independently and establish their own laboratories. This is akin to the IVD model adopted by Berry Genomics following the formal regulation of non-invasive prenatal testing.

The approval of kit products not only enables midstream companies to unlock commercialized testing but also, to some extent, brings a wave of benefits to the upstream instrument market.

Future Potential

The market landscape and regulatory frameworks for oncology products share notable similarities. Companies that are first to launch their test kits will gain a certain first-mover advantage. However, as more companies secure approvals, the market dynamics will shift. Enterprises may enter clinical practice through government tendering or direct collaborations with hospitals. If a company holds an absolute advantage in distribution channels, it is highly possible for it to catch up from behind and emerge as a market leader in the future.

What sets tumor detection apart is its greater complexity compared to the detection of chromosomal abnormality disorders. Chromosomal abnormalities can be identified at the chromosomal level, whereas tumors are complex diseases regulated by multiple genes, and our current understanding of these gene expressions is less mature than that of chromosomal disorders. This field represents a “high-altitude” technological domain within genetic testing, where technical capabilities and product-market fit will become key competitive factors.

Moreover, the target audience for clinical oncology testing is broader and the frequency of use is higher, resulting in a larger market.

In the NIPT industry, BGI Genomics, Berry Genomics, Daan Gene, CapitalBio, and Annoroad have captured nearly the entire market, making it difficult for other companies to establish strong competitiveness against them. The oncology sector, however, presents a different landscape. In addition to listed companies and unicorns such as BGI, Berry Genomics, AmoyDx, and Novogene, three major players—Burning Rock Biotech, Geneseeq, and 3DMed—have emerged. Furthermore, highly influential leading enterprises include Panacea Genomics, Yuanma Gene, HalioDx, Genetron Health, and Kinnear Genomics.

Beyond the strategic moves of industry giants, the oncology testing sector faces numerous formidable challengers, suggesting that its future market landscape will be far more complex than that of the NIPT market.

Furthermore, it is unlikely that most companies will enter the instrument market at present. In the NIPT industry, since no instruments had previously received approval from the China Food and Drug Administration (CFDA), there was significant room for growth in the upstream sector, leading these companies to pursue a dual strategy of developing both reagent kits and instruments. However, sequencing instruments from BGI Genomics, Berry Genomics, CapitalBio Technology, Daan Gene, and Annoroad have now sequentially obtained regulatory approval. Moreover, companies represented by BGI Genomics are developing more sequencing instrument products with broader clinical applicability.

With increasingly clear industry specialization and the high technical barriers in tumor detection, it is unlikely that companies will devote significant resources to entering the instrument market.

Conclusion

In addition to policy and market drivers, this round of financing boom is also inseparable from technological advancements. It is precisely the continuous development and maturation of technology that has gradually earned the industry recognition from regulatory authorities and the market, paving the way for the public listings of leading enterprises. Such recognition, in turn, will further propel industry development, thereby providing support for technological innovation.