Overcoming Barriers in IoMT: Addressing Industrial Fragmentation, Unclear Business Models, and Key Technological Gaps

In the previous special report on the Internet of Medical Things (IoMT)《Among the 14 application scenarios of the Medical Internet of Things (IoMT), which five are most favored by hospitals?》In China, VCBeat has outlined 14 application scenarios for the current implementation of IoT in hospitals.

This time, we will analyze the development obstacles of the Internet of Things in terms of technology, industrial collaboration, standard system, and business model.

Infrastructure, Standards, and Business Models Urgently Need Breakthroughs

In 2017, the Ministry of Industry and Information Technology (MIIT) formulated the "13th Five-Year Plan for the Internet of Things" based on relevant documents such as the "Outline of the 13th Five-Year Plan for National Economic and Social Development" and the "Guiding Opinions of the State Council on Promoting the Orderly and Healthy Development of the Internet of Things." The Plan serves as a guiding document for the development of the IoT industry over the next five years.

The Plan states that, at the current stage, there are five major areas in the Internet of Things (IoT) industry that urgently require breakthroughs:

1. The industrial ecosystem lacks strong competitiveness; core foundational capabilities in chips, sensors, and operating systems remain weak, R&D capacity for high-end products is insufficient, and there is a significant gap in original innovation capability compared to developed countries;

2. Weak synergy across the industrial chain, with a lack of leading enterprises capable of integrating upstream and downstream resources and driving coordinated industry development;

3. The standard system remains imperfect; the development of certain critical standards is progressing slowly, and formulating cross-industry application standards poses significant challenges;

4. The integration of the Internet of Things (IoT) with various industries needs to be further deepened; mature business models are still lacking. Some sectors suffer from fragmented management and insufficient promotion efforts, while the development of new technologies and business formats faces cross-industry institutional and mechanistic barriers.

5. The situation regarding network and information security remains severe, with urgent issues to be addressed in facility security, data security, and personal information security.

Building on the issues raised, the “Guidelines” also offer several strategies for breaking through industry bottlenecks:

1. Improve the top-level design of standardization. Establish and improve the Internet of Things (IoT) standard system, and release guidelines for IoT standardization development. Further promote the coordinated development of national, industry, and group standards for IoT, encourage enterprises to take the lead in formulating standards, actively incorporate innovative achievements into international standards, accelerate the construction of technical standard testing and verification environments, and enhance standardized information services.

2. Strengthen the development of standards for key generic technologies. Accelerate the formulation of standards for sensing technologies and devices, including sensors, instruments and meters, radio frequency identification (RFID), multimedia acquisition, and geographic coordinate positioning. Organize the development of network technology standards for wireless sensor networks, low-power wide-area networks (LPWAN), network virtualization, and heterogeneous network convergence.

3. Establish information processing standards for operating systems, middleware, data management and exchange, data analysis and mining, and service support. Develop fundamental common standards for IoT identification and resolution, network and information security, reference models, and evaluation testing.

In the healthcare industry, much like the broader Internet of Things (IoT) sector, the development of the Healthcare IoT is similarly constrained by factors such as standards and policies. Before addressing these issues individually, it is essential to first understand the evolution of industry standards and policies, as well as the current state of development.

Policy Evolution and the Current State of Industrial Development

The National IoT Basic Standards Working Group was jointly established by the Standardization Administration of China and the National Development and Reform Commission in November 2010. The main responsibilities of the working group include studying proposals for IoT technical architectures and standard systems that align with China’s national conditions, putting forward recommendations for projects to develop or revise standards for key IoT technologies and foundational general-purpose technical standards, and carrying out standard development work.

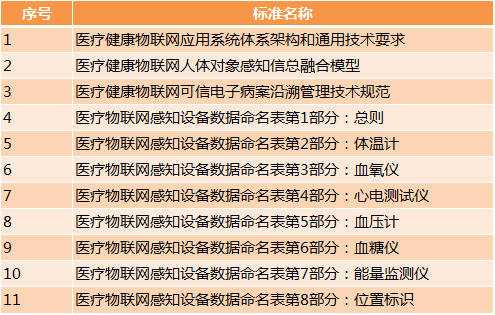

Following the establishment of the National Working Group on Basic Standards for the Internet of Things (IoT), 47 items were approved for the first batch of national IoT standards, including 11 healthcare-related items, as detailed in the table below:

Thus, it can be seen that the Internet of Medical Things (IoMT) has already established some industry-recognized standards at this stage.

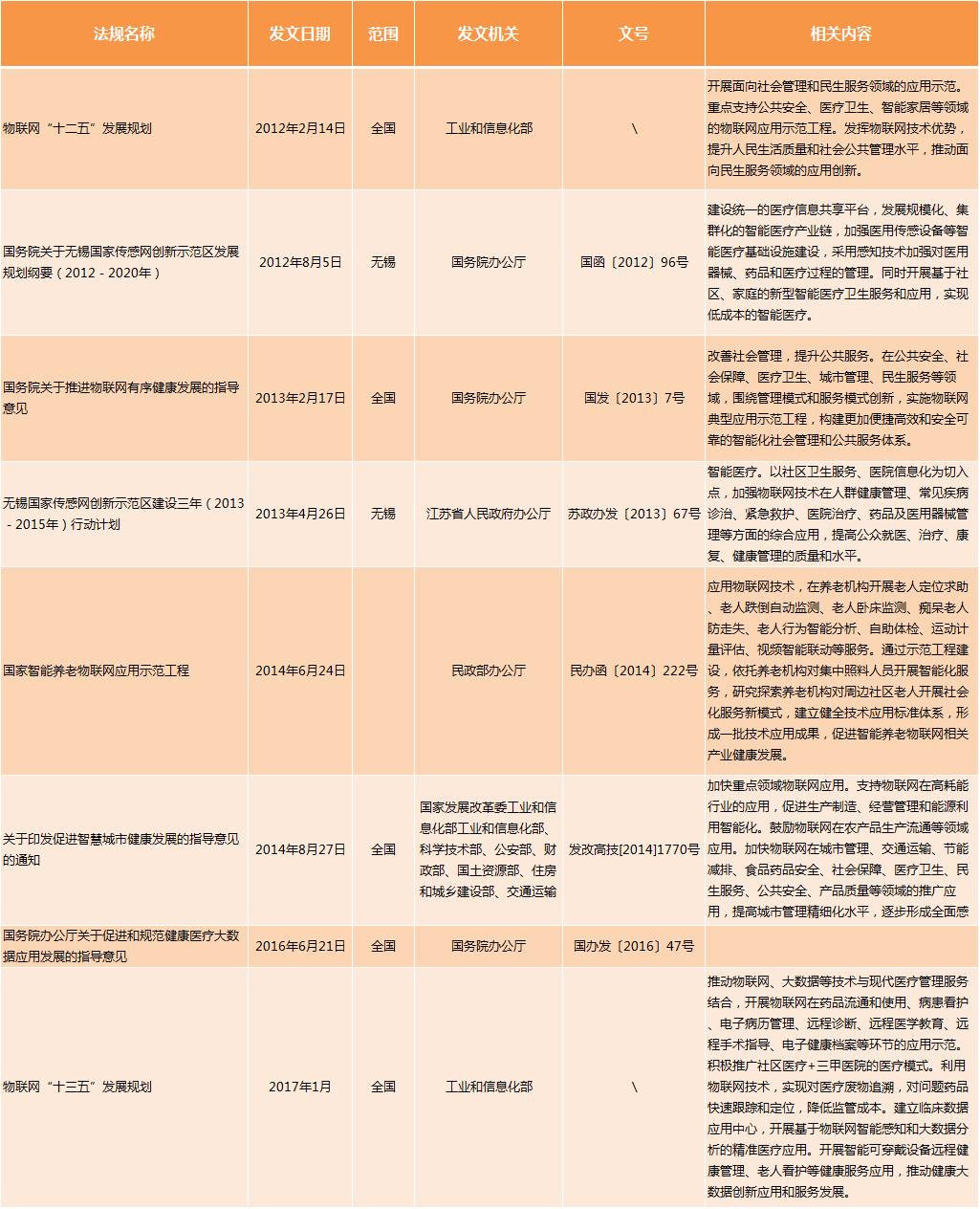

Furthermore, by examining the series of policies directly related to the Internet of Things (IoT) in health and healthcare issued by the state during the “12th Five-Year Plan” period and focusing on their key priorities, we can broadly outline the following evolutionary path:

Application Demonstration and Scenario-Based Exploration Phase (2012–2014) — Establishment of a Large-Scale, Clustered Smart Healthcare Industry Chain (2014–2016) — Precision Medicine Application Phase Featuring IoT Intelligent Sensing and Big Data Analytics (Post-2016).

National IoT Policies Related to Healthcare Issued from 2012 to 2017

Thus, we can conclude:Scenario-based implementation is the foundation of industrial development, while scaling and clustering are the inevitable paths for industrial deepening. Only by achieving a certain level of scale and industrial depth is it possible to accumulate big data, which is ultimately why the Internet of Things (IoT) will inevitably converge with big data.。

Based on the industrial achievements released in the 13th Five-Year Plan for the Internet of Things (IoT), during the 12th Five-Year Plan period, China’s healthcare IoT sector had established a relatively complete IoT industry chain encompassing chips, components, devices, software, system integration, operations, and application services.

A development pattern characterized by regional clustering has taken shape across four major areas: the Bohai Rim, the Yangtze River Delta, the Pan-Pearl River Delta, and the Central and Western regions, giving rise to a large number of leading enterprises in the Internet of Things (IoT). In the medical IoT industry, a batch of public service platforms has been initially established, covering common technology research and development, testing and inspection, investment and financing, identifier resolution, achievement transformation, talent training, and information services.

Fiber-optic and infrared sensor technologies have reached an internationally advanced level. The technological capabilities of ultra-high-frequency smart cards, passive microwave radio frequency identification (RFID), and BeiDou navigation satellite system chips have improved significantly. Micro-electromechanical systems (MEMS) sensors have achieved mass production, and breakthroughs have been made in the development of Internet of Things (IoT) middleware platforms and multifunctional portable smart terminals.

We take Wuxi, China’s leading city in the Internet of Things (IoT), as our blueprint:

On July 11, 2017, the General Office of the Wuxi Municipal Committee of the Communist Party of China and the General Office of the Wuxi Municipal People’s Government issued the “2017 Implementation Plan for the Three-Year (2017–2019) Action Plan on Accelerating the Development of the New Generation Information Technology Industry with IoT as the Leader in Wuxi City.”

The Plan clarifies development goals, emphasizing the accelerated construction of specialized industrial parks. Xinwu District will prioritize the development of the Smart Health Industrial Park and advance the construction of carrier platforms. It will also accelerate the establishment of a batch of national-level IoT industry platforms, with a focus on entities such as the National Medical and Health IoT Product Evaluation Center and the Smart Sports (Wuxi) Innovation Center.

It is evident that platformization and park-based development have become the next-stage goals for the Internet of Medical Things (IoMT). However, achieving these objectives necessitates overcoming the five major obstacles mentioned earlier. Only by enhancing industrial ecosystem competitiveness and synergy, improving standard-setting, and expanding business models can the IoMT achieve its next leap forward.

In this regard, VCBeat has conducted an analysis on three of these items respectively.

# How to Understand Industrial Chain Synergy?Literally, it refers to achieving a win-win scenario among upstream and downstream players in the industrial chain—characterized by improved efficiency and reduced costs—through the optimized allocation and enhancement of the value chain, enterprise chain, supply-demand chain, and spatial chain.

A lack of systemic cohesion in the industrial chain indicates weak synergy among enterprises at various stages, failing to achieve a synergistic effect where the whole exceeds the sum of its parts (i.e., 1+1+1>3), with players largely operating in silos. This not only results in inefficient market expansion but also creates conditions prone to Gresham’s law, where inferior products drive out superior ones.

The core objective of industrial chain collaboration is to integrate all segments across the upstream and downstream, thereby enhancing corporate competitiveness.

Take YiHui Technology as an example. Unlike other IoT companies that focus solely on product development and marketing, YiHui Technology operates more like an open medical IoT platform. Depending on the specific implementation scenarios, every company has the opportunity to join this platform. This approach creates a comprehensive IoT solution that integrates the entire industry chain. Compared to a single company working in isolation, this model offers greater potential for growth.

Zhang Lizhong, General Manager of Yihui Technology, once told VCBeat: “The application scenarios for the Internet of Things (IoT) in healthcare are too complex for any single company to handle everything. Moreover, given the high degree of specialization in niche sectors, many companies are developing dedicated IoT products that can all be utilized on Yihui Technology’s IoT infrastructure platform.”

In response, YiHui Technology has launched an IoT infrastructure platform that integrates four networks. This platform addresses communication and data fusion applications across wired networks, the Internet of Things (IoT), and wireless networks. If the IoT infrastructure platform is regarded as the skeleton of the medical IoT, then adding flesh, tendons, and veins to this skeleton through collaborations with other enterprises embodies the true significance of industrial synergy.

Although the IoT infrastructure platform is open, it is not without barriers. The integration of all hardware and software products must be closely aligned with medical workflows and comply with established standards and protocols, which demands a high level of professional expertise from enterprises.

Infusion management, infant anti-theft, medical waste management, sterile supply chain management, sterilization management, and linen and uniform management are the primary IoT application scenarios implemented by Yihui Technology within hospitals.

At the communication layer, YiHui Technology collaborates with H3C, a leading domestic IT solutions provider. Every IoT access point (AP) from H3C integrates YiHui Technology’s RADER technology, ensuring seamless technological convergence across all IoT APs.

At the application layer, Yihui Technology, building on its in-house development capabilities, has partnered with companies such as Lvyang Technology and Yingwang Technology to collaborate in areas including intelligent infusion monitoring and smart beds.

At the network layer, consumable TEDs such as temperature patches are predominantly researched, developed, and manufactured by SinoMeditech, the parent company of YiHui Technology. Currently, SinoMeditech’s production capacity ranks among the top three globally.

Yihui Technology’s industrial synergy model can be regarded as a practical exploration of the future industrial paradigm for IoT enterprises. Clearly, under this model, companies across different segments of the industry chain can identify their respective positions and leverage their strengths, thereby avoiding resource waste.

It is foreseeable that as more industry leaders emerge, this type of platform-based industrial integration will become increasingly prevalent. Competition among platforms will inevitably arise, leading to a corresponding increase in industry concentration.

Currently, the primary payment model for medical IoT enterprises to enter hospitals is through bidding processes. Additionally, they can gain access to hospitals via established distributor channels and platform-based companies (such as YiHui Technology).

In addition to the one-time fees generated through bidding, many IoT companies offer consumable products, such as temperature patches, which are single-use medical devices. This undoubtedly expands the market opportunity for enterprises to generate recurring revenue through consumables.

The major trend in the Internet of Things (IoT) is its integration into medical devices, components, accessories, and consumables routinely used in hospitals. Once successfully integrated, IoT companies can undergo a significant transformation in their operational models.

At present, IoT companies primarily collaborate with tertiary hospitals (Grade III Class A), while partnerships with lower-tier hospitals, community health centers, and township health centers remain relatively limited, consisting only of scattered pilot projects.

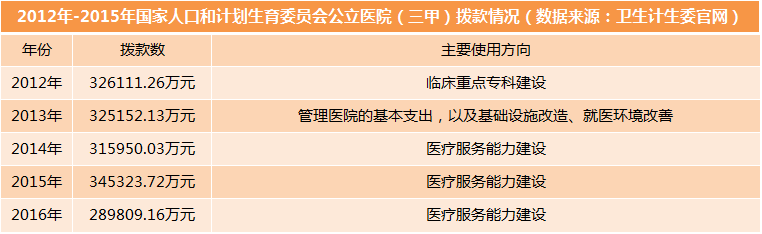

According to the fiscal expenditure data for public hospitals released by the National Health and Family Planning Commission in recent years, Grade 3A hospitals had largely completed their infrastructure and healthcare environment upgrades by around 2013. Since 2014, fiscal appropriations have been directed toward enhancing medical service capabilities, creating opportunities for the entry of medical informatics and Internet of Things (IoT) industries.

According to industry insiders, a significant proportion of secondary hospitals in central and western China have annual operating revenues of less than RMB 100 million, with annual IT investments amounting to only several hundred thousand yuan.

Particularly in western China, including some Grade 3A hospitals, annual IT investment ranges from RMB 1 million to RMB 2 million, primarily allocated to maintenance fees and the replacement of computer equipment. In fact, these hospitals generate substantial annual revenues. For instance, a certain Grade 3A hospital in Shaanxi Province reports an annual revenue of approximately RMB 1.5 billion, with annual IT spending between RMB 1 million and RMB 2 million—accounting for only one-thousandth of its total revenue.

Certainly, in addition to a hospital's revenue-generating capacity, its mindset is equally important.

Unlike medical equipment, where a CT scanner begins generating revenue from the moment it becomes operational in a hospital, the direct benefits of information technology upgrades are not immediately apparent. This is why many hospital directors are hesitant to adopt the Medical Internet of Things (MIoT).

In eastern regions such as Wuxi, the situation is entirely different. The Wuxi Municipal Health and Family Planning Commission requires hospitals to allocate a proportional share of their budgets to health information technology (HIT). For a hospital with an annual revenue of approximately RMB 1.5 billion, this translates to an annual HIT investment of over RMB 20 million in Wuxi.

At present, it is not yet the optimal time for hospitals below the secondary level to implement comprehensive IoT infrastructure. Although the mindset of directors at tertiary Grade A hospitals still requires cultivation, these institutions should be the primary target market for enterprises.

The measurement precision of consumer-grade medical wearables is constrained by multiple factors. Taking consumer-level wearable medical applications as an example, the sensors employed still exhibit a certain gap in reliability and accuracy compared to professional medical diagnostic equipment. This discrepancy arises not only from the inherent limitations of the sensor components themselves but also because slight variations in how the wearable device is worn can significantly affect the data obtained from biophysiological monitoring. Furthermore, differences in sensing points for data acquisition, measurement environments, and sensor usage methods all impact the actual test results.

Measurement devices designed for clinical-grade applications impose stringent operational requirements, including the device placement environment, the wearing method and mounting position of sensors for data acquisition, and even the physiological state of the subject. However, individual consumers often struggle to precisely meet these critical measurement criteria, which frequently results in an inability to effectively improve the accuracy of the collected data.

In the 13th Five-Year Development Plan for the Internet of Things, clear judgments were also made regarding the key technological breakthroughs for the IoT in the coming years:

1. Core Sensing Elements of Sensor Technology

Test sensitive materials such as biomaterials, graphene, and special functional ceramics to secure a first-mover advantage in the field of advanced sensitive materials; strengthen research on the sensing mechanisms, structures, and packaging processes of silicon-based sensors, and accelerate the R&D and industrialization of various sensitive components.

Integration, Miniaturization, and Low Power Consumption of Sensors: Conduct research on technologies and processes for integrating similar and dissimilar sensors, supporting circuits, and sensitive elements. Support the development of diverse types of sensitive chips based on MEMS and thin-film technologies, and pursue innovations in various structural forms of packaging and packaging processes. Support the R&D of modular devices featuring energy storage and power control capabilities, such as external energy harvesting and automatic restart from power-off sleep mode.

Key Application Areas: Support the R&D of high-performance sensor products and application technologies for inertia, pressure, magnetism, acceleration, light, imaging, temperature and humidity, distance, etc., and actively tackle key challenges in developing new types of sensor products.

2. Common Technologies for System Architecture

Continuously track and study the evolution trends of IoT system architectures, actively promote interoperability and standardization among existing heterogeneous IoT network architectures, and prioritize support for research on trusted architectures and architectural interoperability in areas such as network communications and data sharing. Strengthen research on component technologies related to resource abstraction, resource access, semantic technologies, as well as key IoT entities, interface protocols, and common capabilities.

3. Operating System: User-Interactive Operating System

Promote the porting of mobile terminal operating systems to IoT terminals, with a focus on supporting the research and development of IoT operating systems for key areas such as smart homes and wearable devices.

Real-Time Operating Systems: Prioritize support for the research and development of IoT operating systems tailored to key sectors such as industrial control and aerospace. Conduct R&D on peripheral modules, including file systems and network protocol stacks adapted to IoT characteristics, as well as various development interfaces and tools. Support enterprises in launching open-source operating systems and releasing kernel development documentation, thereby encouraging users to engage in secondary development of the operating systems.

4. Key Technologies for the Integration of IoT, Mobile Internet, and Big Data Oriented Toward Mobile Terminals

Priority support will be given to research on technologies such as human-computer interaction for mobile terminals, micro smart sensors, MEMS sensor integration, ultra-high frequency or microwave RFID, and converged communication modules.

For IoT convergence applications, priority support will be given to technical research on operating systems and data sharing service platforms. Key technologies for data acquisition and exchange will be breakthroughs achieved, as well as those for compression, indexing, storage, and multi-dimensional querying of massive high-frequency data. Distributed foundational software platforms, such as big data stream computing and real-time in-memory computing, will be developed. By integrating typical application scenarios including industrial operations, intelligent transportation, and smart cities, key technologies for IoT data analysis, mining, and visualization will be advanced, resulting in specialized application software products and services.

Taking RFID technology as an example. According to statistical data from the Qianzhan Industry Research Institute, since China’s Internet of Things (IoT) development was formally incorporated into the national development strategy in 2010, China’s RFID and IoT industries have ushered in a rare opportunity for growth. In 2014, the market size of China’s RFID industry reached RMB 31.1 billion, representing a 30% year-on-year increase from 2013, and the market size amounted to approximately RMB 37.3 billion in 2015.

Although the RFID market is currently expanding at a rapid pace, technological breakthroughs are still required in the following four areas:

① High frequency remains the mainstream, while ultra-high frequency represents the future development trend.

Currently, ultra-high frequency (UHF) RFID accounts for only about 10% of the overall market share, but it is projected to become the mainstream technology in the RFID market within five years.

② The market potential for software and system integration is immense.

China’s information technology infrastructure remains relatively underdeveloped, and applications that truly leverage the advantages of RFID are still limited. In simple RFID implementations, software costs remain low, with some solutions even provided to users as complimentary add-ons, and integration fees are likewise modest. However, with the expansion of large-scale logistics applications and open-loop systems, software will constitute a significant portion of RFID project expenditures, in some cases even surpassing hardware costs.

③ Chinese companies’ chip manufacturing capabilities will gradually strengthen.

At present, Chinese enterprises’ mastery of RFID technology still needs to be strengthened. Domestic chips are limited to high-frequency products and a small number of ultra-high-frequency products. In the future, the Chinese government and enterprises will certainly increase R&D efforts to safeguard their interests, with chip manufacturing capability being a particularly important focus.

④ Unifying standards will be a key focus for China’s RFID industry in the future.

Each RFID tag contains a unique paired identification code. If its data formats are diverse and mutually incompatible, RFID products adhering to different standards will be unable to interoperate. However, the specific standards in China have not yet been fully implemented. Therefore, coding management, core technologies, and databases will be the key focus areas for future RFID development.