Medical Informatics in 2017: Navigating Market Stagnation and Seeking New Growth Engines

The entire healthcare IT industry in 2017 was more akin to a year of collective exploration. Sluggish revenue growth among publicly listed companies drove them to urgently seek new sources of industry expansion. Unlike the clear investment trends observed the previous year, financing activities for IT enterprises in 2017 revealed no such distinct trajectory; instead, investment directions became scattered and fragmented. The emergence of artificial intelligence captured nearly all capital attention. For traditional healthcare IT companies, this raised a series of unavoidable questions: Is it a challenge or an opportunity? And how should they transform?

I. Health and Medical Big Data Enters the National Team Era

There was no shortage of policies and major events related to healthcare informatization in 2017, including industry plans issued by the State Council. In this regard, VCBeat has selected some of the most core policies and events:

In January 2017, the State Council issued the “13th Five-Year Plan for Health and Wellness.” The Plan states that it is necessary to promote the interoperability and sharing of population health information. Relying on regional population health information platforms, it aims to achieve continuous recording of electronic health records (EHRs) and electronic medical records (EMRs), as well as information sharing among medical institutions of different levels and categories. It calls for the comprehensive implementation of “Internet+” health and medical services benefiting the public, developing telemedicine and smart healthcare combining online and offline services targeted at central and western regions and grassroots levels, and promoting the deep integration of information technologies—such as cloud computing, big data, the Internet of Things, mobile internet, and virtual reality—with health services, thereby enhancing the capacity of health information services.

In January 2017, to accelerate the implementation of the national big data strategy and promote the healthy and rapid development of the big data industry, the Ministry of Industry and Information Technology (MIIT) formulated the "Big Data Industry Development Plan (2016–2020)." The Plan emphasized promoting cross-industry integration and innovation in big data. It called for breaking down institutional and mechanistic barriers, eliminating data silos, innovating cooperation models, and fostering new forms of business characterized by cross-sectoral integration. Support was to be given to sectors with strong informatization foundations—such as telecommunications, internet, industry, finance, healthcare, and transportation—to take the lead in launching cross-domain and cross-industry big data applications, thereby cultivating new models of big data application.

In February 2017, the National Health and Family Planning Commission issued the "Notice on Issuing the Administrative Specifications for the Application of Electronic Medical Records (Trial)," simultaneously repealing the previous versions of the "Basic Specifications for Electronic Medical Records (Trial)" and the "Basic Specifications for Traditional Chinese Medicine Electronic Medical Records (Trial)."

On April 27, 2017, China Health and Medical Big Data Co., Ltd., with state-owned capital as the main body and involving thirteen industry-leading enterprises and investment and financing platforms including Digital China Holdings Limited, Industrial and Commercial Bank of China Limited, Bank of China Limited, Chinese Academy of Sciences Holdings Co., Ltd., Neusoft Corporation, Inspur Group, Wonders Information Co., Ltd., E-Linkwell Information Technology Co., Ltd., and Rongke Technology Co., Ltd., held its preparatory meeting in Beijing.

In May 2017, the website of the National Health and Family Planning Commission (NHFPC) released the “Notice on Effectively Implementing Family Doctor Contracted Services in 2017,” jointly issued by the NHFPC and the State Council’s Office for Healthcare Reform. The Notice stated that all localities should strengthen the development of regional health information platforms and information management systems for primary healthcare institutions to promote interoperability and sharing of health data. A service interaction platform between family doctors and contracted residents should be established, leveraging channels such as websites, mobile applications, WeChat, Weibo, and video visits to facilitate online appointment scheduling, online consultations, health management, access to laboratory and diagnostic test results, and online payments, thereby enhancing doctor-patient interaction and strengthening doctor-patient relationships.

In July 2017, the State Council issued the Development Plan for New-Generation Artificial Intelligence: In the field of intelligent healthcare, promote and apply new AI-driven models and methods for treatment, and establish a rapid and precise intelligent healthcare system. Explore the development of smart hospitals, develop human-machine collaborative surgical robots and intelligent diagnostic and therapeutic assistants, research and develop flexible, wearable, and biocompatible physiological monitoring systems, and formulate human-machine collaborative clinical intelligent diagnosis and treatment solutions to achieve intelligent medical image recognition, pathological classification, and intelligent multidisciplinary consultations.

Looking back at the major informatics developments of 2017, we can broadly identify two key trends: first, the vigorous promotion of big data and interoperability; second, the formal inclusion of big data–based artificial intelligence into national development planning.

Regarding big data, VCBeat has previously analyzed the current policies on health and medical big data. We have found that although national macro-level policies encourage and support the development of health and medical big data, there are still numerous practical difficulties and obstacles to be overcome in terms of policy implementation and specific operations. These mainly include the following five points:

① The legal framework in the field of big data for health and medical care urgently needs improvement, with insufficient safeguards for security and privacy;

② Proliferation of digital silos within hospitals creates barriers to data sharing and interoperability;

③ Data Standardization Issues;

④ Shortage of talent in health and medical big data;

⑤ It is difficult for enterprises to establish a viable business model.

In particular, big data has faced significant obstacles in terms of data openness and business models.

Currently, there are six main payers in the big data market for healthcare: consumers, enterprises, insurance companies, governments, hospitals, and pharmaceutical companies (including medical device manufacturers). In the short term, insurance companies and pharmaceutical companies have the strongest willingness to pay, with representative companies beginning to explore applications of big data. The demand from hospitals, governments, and enterprises remains evident, but they are still relatively conservative at this stage.

The conservatism of hospitals and other institutions stems primarily from concerns over data value, privacy, and security. Large hospitals lack the incentive to share their data with smaller ones, and the prevalence of cyberattacks has made them extremely wary of connecting to external networks. Under these circumstances, data interoperability is largely confined within individual hospitals.

Whether it is the “Big Data Industry Development Plan (2016–2020)” compiled by the Ministry of Industry and Information Technology, the new version of electronic medical records that places significant emphasis on data sharing, or the establishment of China Health and Medical Big Data Co., Ltd., which has a “national team” background, all these can be seen as the state’s step-by-step promotion of health and medical big data. In light of the increasing emphasis on information security by the national team, VCBeat believes that big data companies with state-owned capital backgrounds are poised to usher in a new wave of development peaks. Meanwhile, the adoption of enterprises with foreign investment backgrounds in institutions such as hospitals is expected to face certain restrictions.

The development foundation and long-term optimization of artificial intelligence require high-quality, continuous data. Due to historical factors, data within traditional Hospital Information Systems (HIS) often suffer from insufficient quality and limited dimensions, making AI models trained on such data difficult to deploy in clinical practice with adequate accuracy and generalizability. Therefore, only by ensuring the professional quality, structured integration, and multidimensional diversity of raw data can we enable the future development of artificial intelligence that is both authentic and accurate.

In this domain, several companies in China have made significant strategic investments. Taking Boshi Medical Cloud as an example, the company can meet the rapidly accelerating iterative demands of hospital clinical data under the premise of standardized structures and unified terminology. Meanwhile, it enables physicians to retrieve desired information for each case based on different input fields. According to different disease categories, Boshi Medical Cloud also helps hospitals achieve personalized and standardized data integration, ultimately bridging the gap between patient health data and clinical diagnosis and treatment data, thereby forming true healthcare big data.

II. Healthcare IT Investment and Financing Showed a Fragmented Trend in 2017

As of November 2017, the total financing amount in the healthcare informatics industry was approximately $119 million, with 17 companies securing funding. In the same period of 2016, a total of 22 companies obtained financing, with the total amount reaching approximately $384 million. Clearly, not only were fewer companies funded in 2017, but the total financing amount also decreased by more than half compared to 2016.

An analysis of 2016 financing data reveals that seven companies secured funding rounds beyond Series A, whereas only four did so in 2017. By sector, healthcare IT financing in 2017 was characterized by a fragmented distribution across various fields.

Data source: VCBeat, Eggshell Research Institute database

After analyzing the overall development trends, VCBeat believes that the general decline in investment and financing activity in the medical informatics industry in 2017 was largely due to the concentrated focus on artificial intelligence (AI) that year, which became a favored target for investors. Meanwhile, certain niche sectors that did secure funding—such as indoor hospital positioning, smart elderly care, infection prevention and control management, hospital patient follow-up, and clinical research—were primarily centered around in-hospital operations, while out-of-hospital informatics solutions attracted relatively less financing. Alongside the rising prominence of AI, medical informatics companies have gradually begun transitioning toward AI-driven models this year (a dedicated section below will provide a detailed analysis).

III. Development in the Field of Innovation

In 2017, the informatization of medical consortiums became a major hotspot. On September 1, 2017, at the National On-Site Promotion Conference on Medical Consortium Construction held in Shenzhen, Li Bin, Deputy Head of the State Council’s Leading Group for Healthcare Reform and Director of the National Health and Family Planning Commission, announced that by the end of June 2017, 1,764 tertiary hospitals across China had engaged in the construction of medical consortiums in various forms, accounting for 80% of all tertiary hospitals nationwide; in eight provinces and municipalities, including Jiangsu, Chongqing, Sichuan, and Shaanxi, over 90% of tertiary hospitals participated in forming medical consortiums.

The development of specialized medical consortia is currently a top priority for tertiary Grade A hospitals in China. Conventional medical consortia are typically initiated by government bodies or hospital leadership, with the primary aim of enhancing institutional branding rather than adopting a patient- or discipline-centered approach. Consequently, such consortia often experience significant expert attrition once initial momentum wanes.

In contrast, specialized medical consortia adopt a patient-centered approach, leveraging standardized disease treatment protocols and talent development as key mechanisms to ensure homogeneous care for patients. Previously, it was extremely difficult for patients at primary care hospitals to consult specialists in key departments at tertiary Grade A hospitals. Now, through specialized medical consortia, patients with complex and refractory conditions at the primary care level can receive timely guidance from experts.

Taking the Jianggan District Fundus Disease Consultation Center as an example. Under the leadership of the Jianggan District Health and Family Planning Bureau, led by the Fundus Disease Center of Zhejiang Eye Hospital, and with technical support from Zhuojian Technology, the Jianggan District Fundus Disease Consultation Center is a regional fundus disease diagnosis and treatment platform aimed at improving the regional diagnosis and treatment level of fundus diseases in Jianggan District. It is the first regional fundus disease consultation platform in Hangzhou City and even Zhejiang Province.

Through the “Jianggan District Fundus Disease Consultation Center” platform, community physicians can upload patients’ test results in real time. Specialists from Zhejiang Eye Hospital can promptly conduct remote consultations on patients’ fundus conditions and feed back their recommendations to the community hospitals. Based on the consultation outcomes, community physicians can determine whether further referral is necessary and arrange referral appointments via the platform for patients who require them. This approach ensures timely and efficient patient care while conserving medical resources and expanding access to healthcare services for those in need.

Regarding family doctor enrollment, Shequ 580, a benchmark family doctor service provider in China, exclusively disclosed to VCBeat the latest operational data for its resident-facing app. The data shows that from March to June 2017, while continuing to expand its market horizontally, Shequ 580 launched a revenue conversion initiative. Within just three months, the conversion rate from free-tier to paid-tier hospitals exceeded 7%, with month-over-month revenue growth surpassing 100% for three consecutive months, achieving nearly one million yuan in monthly profit.

In its conversation with Liu Bo, CEO of the company, VCBeat identified three current realities in the digitalization of family doctor contract services:

Status 1: Rapidly establishing a family doctor service system is an urgent need for community hospitals. As long as high-quality platforms and tools are provided, community hospitals demonstrate a strong willingness to pay.

Current Situation 2: Patients with chronic diseases, pregnant and postpartum women, and children are currently the core populations for family doctor contract services. Providing effective, personalized care to these key groups is critical to the success of family doctor practices.

Current Situation 3: The management of subsidies for family doctor contracts, performance management, and health management by family doctors will generate substantial demand for informatization.

VCBeat believes that the development of medical consortiums and family doctor contract services are the two “wings” driving the implementation of the tiered diagnosis and treatment system. The establishment of medical consortiums will restructure and reorganize China’s healthcare service system. By forming specialized medical consortiums across different regions, the public will enjoy greater convenience through family doctor contracts and comprehensive, full-cycle medical services within these consortiums.

Among these, the digitalization of specialized medical consortia and family doctor contract services will serve as a key driver for the development of tiered diagnosis and treatment. Through digitalization, various barriers hindering inter-institutional collaboration and resource integration can be removed, thereby building tightly-knit medical consortia, promoting family doctor contract services, channeling high-quality medical resources to the grassroots level, and achieving sustainable development.

Research on Clinical Decision Support Systems (CDSS) began in the late 1950s. The earliest research direction involved medical experts organizing professional knowledge and clinical experience into a knowledge base via reasoning engines, utilizing logical reasoning and pattern matching to assist users in diagnostic inference.

It was not until the mid-1970s that the world’s first Clinical Decision Support System (CDSS), MYCIN, was developed at Stanford University in the United States. This system could automatically identify 51 types of pathogens and appropriately select from 23 antimicrobial agents based on inputted laboratory data. It assisted physicians in diagnosing and treating bacterial infections, thereby providing patients with optimal prescription regimens.

Subsequently, various CDSS with distinct features emerged, such as Internist-I and QMR from the University of Pittsburgh, ILIAD and HELP from the University of Utah, DXPLAIN from Harvard University, UpToDate from Wolters Kluwer, and MD Consult from Elsevier.

From physicians’ perspective, leveraging Clinical Decision Support Systems (CDSS) to enhance their diagnostic and therapeutic capabilities is a highly effective approach. Moreover, for large hospitals aiming to achieve certification under the HIMSS EMRAM evaluation framework, CDSS is an indispensable component.

Over the past two years, numerous health IT companies have successively launched their own CDSS-related products:

In 2016, Huimei Technology launched the Huimei Clinical Decision Support System, an AI-powered platform that provides general practitioners with a comprehensive knowledge-based solution. The system offers functionalities including triage, differential diagnosis, rational medication management for chronic diseases, and disease-related knowledge resources.

In November 2016, the “Bore” Intelligent Expert Diagnostic System under Ruoshui Doctor was officially launched;

In February 2017, the Kangfuzi Clinical Intelligent Decision Support System was officially launched;

In April 2017, LinkDoc Technology’s HUBBLE Medical Big Data-Assisted Decision-Making System was officially launched.

CDSS, a term that was hardly novel in the information technology industry, has seemingly become a major hotspot this year.

VCBeat once conducted a survey on 24 companies in China (including foreign products distributed by domestic agents) that develop CDSS products. According to the survey, nine products were capable of exchanging data with electronic medical record (EMR) systems; seven CDSS products explicitly featured deep learning capabilities, while the others were primarily knowledge-base-driven products. From a technical perspective, CDSS solutions equipped with deep learning can process physicians’ feedback more promptly and rapidly, thereby enabling smarter clinical decision-making. This represents the future direction of CDSS development.

In 2017, a year marked by the explosive growth of artificial intelligence, numerous companies—including Jiahe Meikang, Ruoshui Doctor, Mulao Renkang, LinkDoc Technology, and Kangfuzi—integrated deep learning capabilities into their clinical decision support systems.

In this regard, VCBeat believes that big data, as the foundation of artificial intelligence (AI), holds a natural advantage in AI adoption due to the deep integration between medical big data companies and clinical data within hospitals. Since the existing business models and products of big data companies have been well implemented, integrating AI as an ancillary service into these products does not impose additional costs on either enterprises or hospitals, thereby minimizing barriers to adoption. Consequently, VCBeat is optimistic about the expansion and exploration in Clinical Decision Support Systems (CDSS) and AI by health informatics and big data companies such as LinkDoc Technology and Jiahe Meikang.

In addition, VCBeat has also conducted an analysis of the market potential for CDSS.

In late April 2017, the Statistical Information Center of the National Health and Family Planning Commission released the latest data on healthcare institutions nationwide. The data showed that there were 987,000 healthcare institutions across China at that stage, including 2,267 tertiary hospitals and 930,000 primary healthcare institutions (comprising 35,000 community health service centers/stations, 37,000 township health centers, 638,000 village clinics, and 205,000 clinics/medical rooms).

In China“Grading Evaluation Standards for the Application Level of Electronic Medical Record Systems” andHIMSS certification pass rates and ceiling levels are both relatively low, and the CDSS market is gradually shifting from public hospitals to primary healthcare institutions.

Taking the HIMSS evaluation as an example, the pass rate for HIMSS EMRAM Stage 6 in the Asia-Pacific region is approximately 5.6%. Using the number of tertiary hospitals in China (2,267) as the upper limit, and assuming an average project construction cost of RMB 3 million (derived from consultations with multiple health IT companies), the market size for CDSS in the context of HIMSS evaluations (Stages 6–7) in China is estimated to be approximately RMB 380 million.

Even excluding the 638,000 village clinics, there are still 277,000 primary healthcare institutions in China. Assuming an average project price of RMB 50,000, the market size for Clinical Decision Support Systems (CDSS) in China’s primary healthcare sector is approximately RMB 13.85 billion, far exceeding the market potential solely driven by hospital accreditation reviews. If secondary hospitals, primary hospitals, and public health institutions are also included, the market opportunity would be even larger.

IV. Listed Information Technology Companies Collectively Expand into Artificial Intelligence

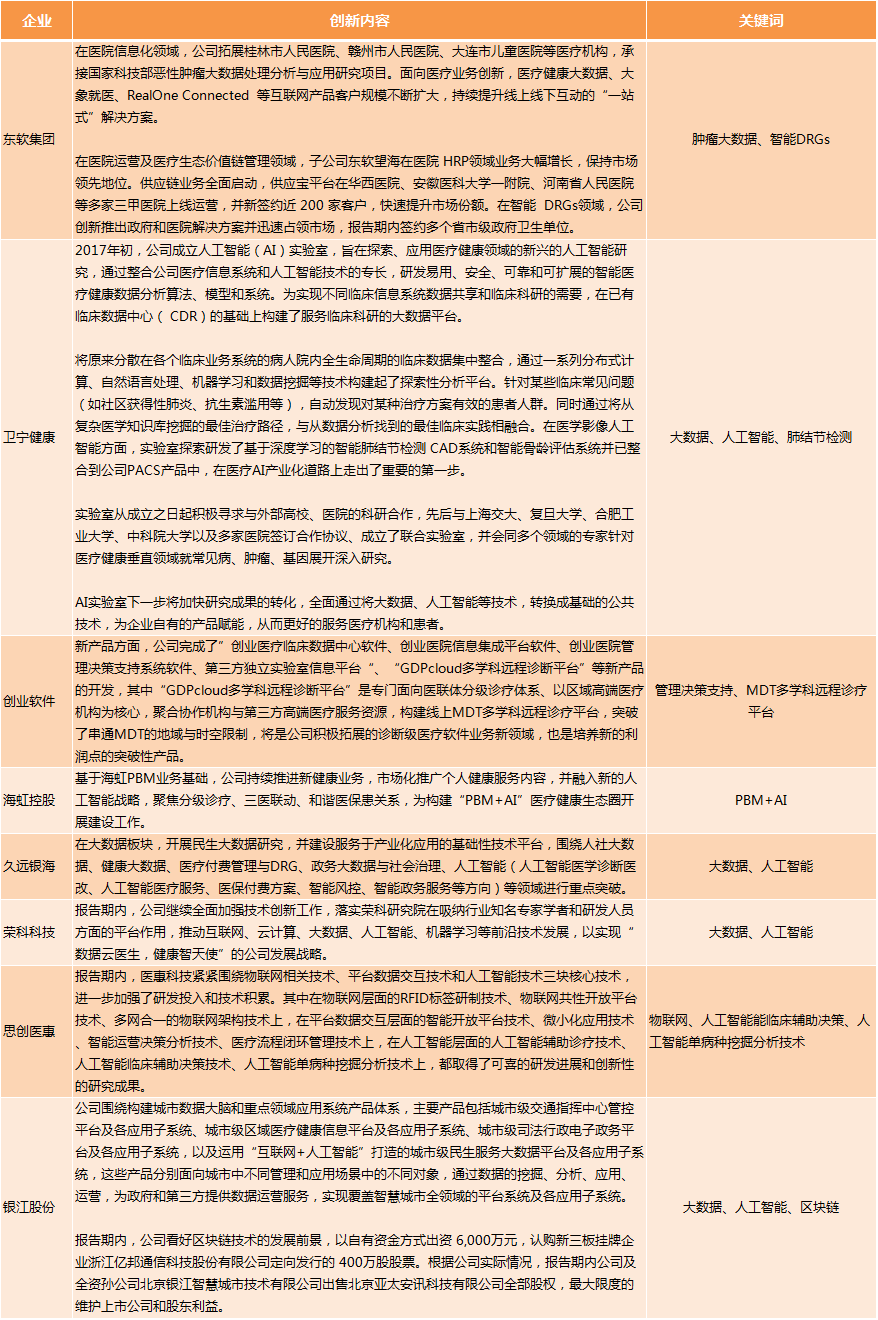

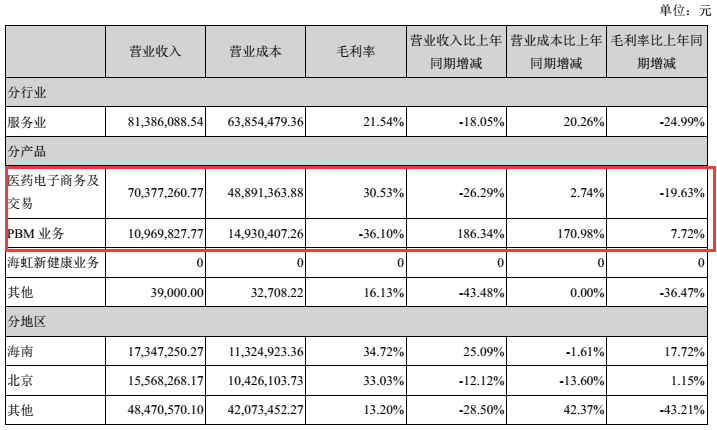

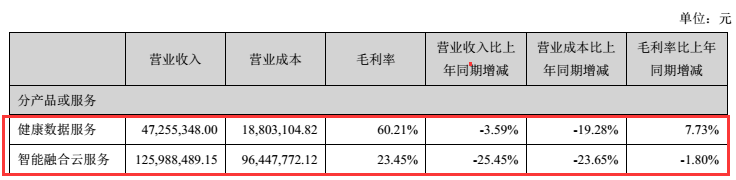

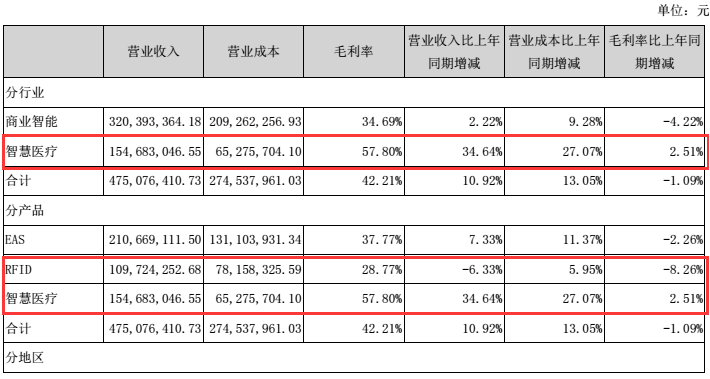

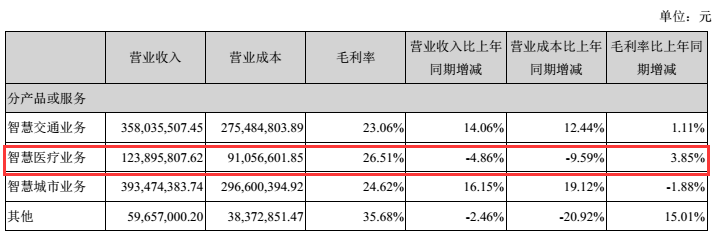

The moves of publicly listed healthcare IT companies serve as a barometer, directly reflecting the development trends of the entire industry. After reviewing the 2017 semi-annual reports of eight major domestic healthcare IT companies, VCBeat extracted the sections related to technological innovation:

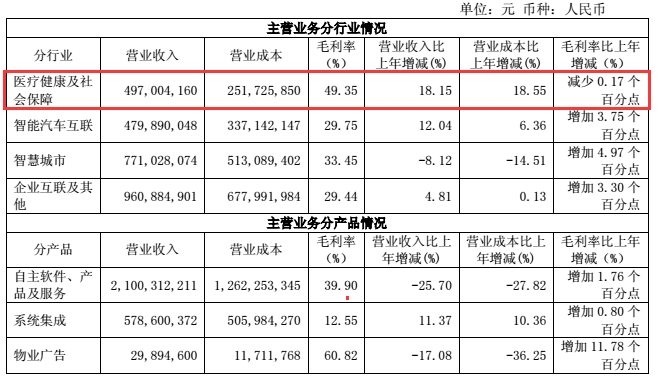

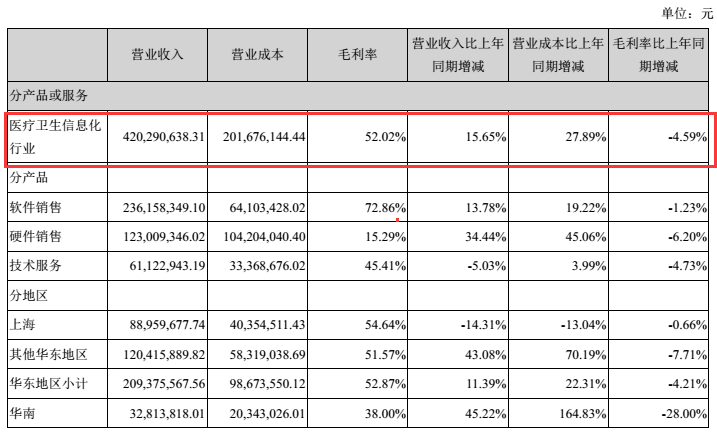

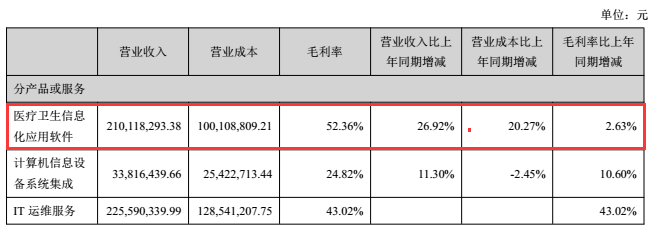

It is evident that the most frequently cited keywords in the realm of technological innovation by healthcare IT companies this year are big data and artificial intelligence. Before analyzing the underlying reasons, we first reviewed the operational performance of various companies with core healthcare-related businesses (all data sourced from the semi-annual reports of listed companies):

Based on the operational performance of various companies, not only are gross profit margins for healthcare-related businesses generally low (with no company achieving growth exceeding 10%), but many have also experienced negative growth. We can broadly infer that the healthcare informatics industry as a whole has reached a development bottleneck. In this broader context, expanding into new technologies and markets to identify new sources of business growth has become critical for corporate development.

In 2017, AI-related companies successively secured substantial financing:

In May, Yitu Technology completed its Series C financing round of RMB 380 million;

In July, Yasen Technology secured tens of millions in Series A+ financing;

In August, Diannei Biology secured an angel round of financing nearing RMB 10 million;

In September, Infervision secured RMB 120 million in Series B financing;

……

Given the close integration of deep learning with healthcare informatization and big data, the practical implementation of artificial intelligence is expected to significantly stimulate the healthcare informatization industry, making it inevitable for listed companies to follow suit. As more industry giants explore and enter this space, this wave of AI innovation is likely to sustain its momentum for an extended period.

V. Big Data and Artificial Intelligence

Looking back at the entire healthcare informatics industry in 2017, big data and artificial intelligence (AI), as the two core focal points, have become strategic priorities for startups and publicly listed companies alike. If 2016 was the inaugural year of big data, then 2017 can more aptly be described as the inaugural year of AI. Traditional informatics companies are gradually transitioning from big data-driven models toward AI-enabled solutions. Initiatives such as hospital interoperability, medical consortiums, and digital infrastructure for family doctor contracting services are facilitating the migration of big data toward population health information. The generation of larger-scale datasets has also laid a solid foundation for the development of artificial intelligence.

“Big Data + AI + Healthcare” not only brings new intelligent solutions and new industry growth points to traditional informatization enterprises. At the same time, it will also create more value for patients, doctors, and hospitals, thereby better promoting the implementation of the national policy of tiered medical care at the grassroots level, better serving the vast number of grassroots patients, and ultimately solving the problem of “difficulty in seeing a doctor” for the general public.