Whither the $70 Billion API Industry? Monopoly Allegations, Price Surges, and Environmental Constraints Reshape China's Pharmaceutical Raw Materials Sector

5-Minute Conspiracy: API Prices Surge Fivefold Nationwide

Active Pharmaceutical Ingredient (API) Prices Rise Again, with Some Increasing by 500%

API Prices Surge, Yet Manufacturers Remain Troubled...

The above are all headlines from reports on the active pharmaceutical ingredient (API) industry in recent months. The API sector, the most fundamental yet opaque link in the pharmaceutical supply chain, has emerged into the public eye with an image of “quietly reaping huge profits.” Accused of colluding to raise prices and dividing illicit gains, API manufacturers featured in these reports have been portrayed as the hidden manipulators behind the pharmaceutical market.

In fact, absent administrative monopolies or absolute barriers to entry, such scenarios cannot exist in any fully competitive industry. Beyond the media’s excessive sensationalism, the audience’s lack of understanding of the active pharmaceutical ingredient (API) industry has further reinforced this perception.

Here, VCBeat (WeChat ID: vcbeat) provides a brief overview of the active pharmaceutical ingredient (API) industry, aiming to clarify its landscape from perspectives such as product categories, market size, key players, and development trends.

China’s Annual API Exports Reach RMB 150 Billion, Ranking First Globally

Active pharmaceutical ingredient (API), as the name suggests, is the “raw material” for drug production. Its full English name is API (Active Pharmaceutical Ingredient,Active Pharmaceutical Ingredient), refers to the active ingredient in a drug, which is a compound that can be safely used for the treatment of human diseases after thorough pharmaceutical research."Although it is the active ingredient of a drug, it can only become a pharmaceutical product for clinical use after undergoing specific preparation processes."

Active pharmaceutical ingredients (APIs) are generally produced by chemical synthesis, recombinant DNA technology, fermentation, enzymatic reactions, or extraction from natural substances.For instance, the renowned artemisinin was initially extracted from *Artemisia annua* (sweet wormwood), while cephalosporins and penicillin were derived from corn fermentation broths. Steroidal hormone active pharmaceutical ingredients (APIs) are produced using yellow ginger (*Dioscorea zingiberensis*) as the starting material, whereby diosgenin is extracted and then synthesized into the final products.

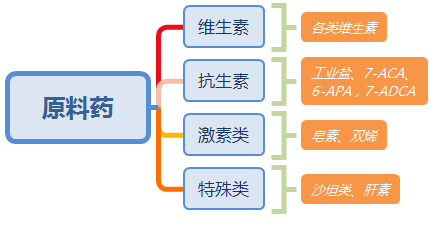

By category, active pharmaceutical ingredients (APIs) can be broadly classified into four major groups: vitamins, antibiotics, hormones, and specialty APIs.

Vitamins include Vitamin A, Vitamin B1, Vitamin B2, Vitamin C, Vitamin D3, Vitamin E, and Vitamin K3; antibiotics include penicillin industrial salt, 6-APA, 7-ACA, 7-ADCA, and amoxicillin; hormones include diosgenin and dienes; special active pharmaceutical ingredients (APIs) are represented by sartans and heparin.

In China,Active Pharmaceutical Ingredients (APIs) are subject to drug regulatory oversight.The Drug Administration Law (2015 Amendment) explicitly stipulates that chemical active pharmaceutical ingredients (APIs) are classified as drugs, and their production requires an approval number. Drugs manufactured using APIs without an approved number shall be treated as counterfeit drugs. Furthermore, the raw materials and excipients used in the production of APIs must also comply with pharmaceutical requirements.

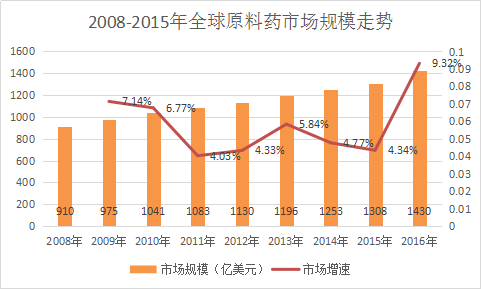

The global active pharmaceutical ingredient (API) market is valued at approximately USD 130 billion, having grown by USD 50 billion over the past decade, with a compound annual growth rate (CAGR) of 5%., which is lower than the average growth rate of 8% in the pharmaceutical market during the same period. The slower growth of the active pharmaceutical ingredient (API) market size is attributed to its status as a highly mature industry with intense competition, primarily benefiting from the natural growth of the pharmaceutical market.

The API market can be divided into the captive-use segment and the merchant market. The captive-use segment refers to APIs produced in-house by pharmaceutical companies for their own needs, while the merchant market refers to APIs procured by pharmaceutical companies from specialized API manufacturers. In 2015, out of a total market worth nearly $130 billion, the captive API segment accounted for $80 billion, and the merchant API market was valued at $50 billion. In recent years, the merchant API market has been expanding steadily, with a growth rate higher than that of the captive-use segment, which to some extent reflectsOutsourcing of Active Pharmaceutical Ingredients (APIs)trend.

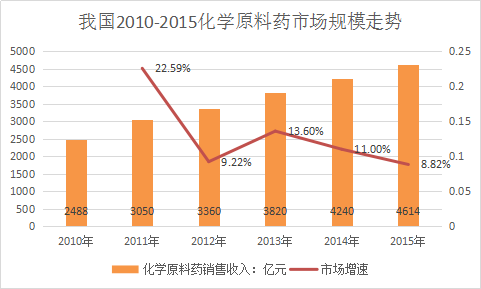

Compared with the global market growth rate, China's API market is growing relatively faster, with a compound annual growth rate of around 13%, exceeding that of the pharmaceutical market.In 2015, China's active pharmaceutical ingredient (API) industry achieved sales revenue of RMB 461.4 billion.

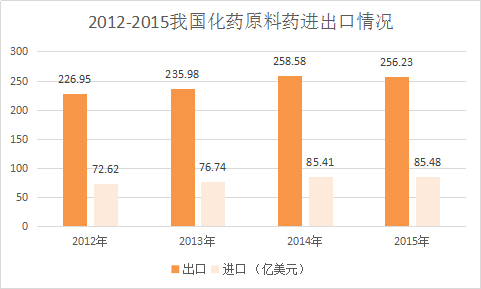

China is also the world's largest exporter of active pharmaceutical ingredients (APIs)., according to China Customs data, China's exports of chemical drug active pharmaceutical ingredients (APIs) reached US$25.623 billion in 2015.Exports account for approximately one-fifth of the global market., with the primary export destinations being Asian countries, including Japan, South Korea, and India.

China's exports of active pharmaceutical ingredients (APIs) are dominated by bulk chemical APIs. Antibiotics account for 30% of the international market, and China ranks among the global leaders in most vitamin categories, with only a few exceptions. Hormones and specialized APIs also hold significant market shares.

In recent years, China's exports of active pharmaceutical ingredients (APIs) have faced a situation of "rising volume but falling prices." According to data from CPhI, China's API export volume reached 8.274 million metric tons in 2016, a year-on-year increase of 13.04%, while prices decreased by 11.59%.

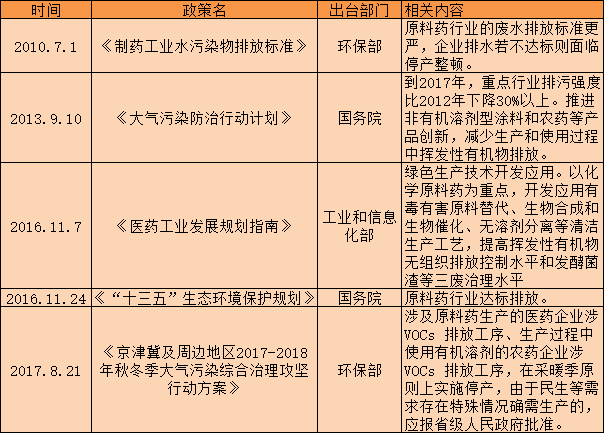

Soaring API Prices? Environmental Pressure Is the Primary Cause

Major domestic production hubs for active pharmaceutical ingredients (APIs) are concentrated in provinces such as Zhejiang, Hebei, and Shandong. Since 2016, these regions have undergone multiple rounds of environmental inspections, leading to the shutdown or production curtailment of numerous pharmaceutical companies due to non-compliance with environmental standards, thereby disrupting the API supply.

In November 2016, Shijiazhuang issued the "Shijiazhuang Air Pollution Prevention and Control Dispatch Order," requiring all pharmaceutical companies in the city to suspend production, with resumption prohibited without approval from the municipal government. The production capacities of CSPC Pharmaceutical Group and North China Pharmaceutical Group, which together account for more than 30% of global vitamin C (VC) active pharmaceutical ingredient (API) output, were affected, leading to a rise in VC prices. Other API manufacturers were also partially impacted.

In early 2017, Zhejiang Province issued the Emission Standard of Air Pollutants for Chemical Synthetic Pharmaceutical Industry to strictly control VOCs (volatile organic compounds) emissions from API manufacturers. Active pharmaceutical ingredients (APIs) account for approximately half of Zhejiang’s entire pharmaceutical industry, with their VOCs emissions representing 4.6% of the province’s total industrial sources.

In February 2017, the Ministry of Environmental Protection launched special inspections in Beijing, Tianjin, Hebei, Henan, Shandong, and other regions, proposing rectification or shutdown plans for a batch of local high-energy-consuming and high-pollution enterprises, with some active pharmaceutical ingredient (API) manufacturers included on the rectification list.

API manufacturers bear the brunt of environmental inspections, which is not unrelated to their high pollution levels.Industry insiders note that the production process for active pharmaceutical ingredients (APIs) involves lengthy technological routes and a wide variety of raw and auxiliary materials, some of which are classified as hazardous chemicals. Meanwhile,Low conversion rate of input materials into finished products, and it exhibits biological toxicity; furthermore, due to the small quantity of single-category materials input, the economic recovery rate for individual waste streams in the waste is low,Difficult to Achieve Waste Resource Recovery,Generally, it can only be disposed of as waste.Taking vitamin C as an example, with a yield rate of 14%, based on the national annual output of 200,000 tons in China in 2012, a total of 1.43 million tons of raw and auxiliary materials were required. Excluding the 200,000 tons converted into finished products, the remaining 1.23 million tons of materials became waste, imposing a significant burden on environmental governance.

In the campaign to rectify the “three highs”—high pollution, high energy consumption, and high emissions—industries such as active pharmaceutical ingredients (APIs), non-ferrous metal smelting, and pulp and paper manufacturing have been subject to production cuts or shutdowns.

Control measures at the production level have transmitted to the market level, manifesting as rising prices for active pharmaceutical ingredients (APIs). In fact, since the first round of environmental inspections began last year, some API manufacturers have ceased providing external quotations. Currently, real-time price monitoring is lacking for major vitamin categories, erythromycin thiocyanate, diosgenin, dienes, and sartan-class APIs.However, overall, API prices have remained stable, with no sharp spikes observed.

Recent Regulatory Policies on Active Pharmaceutical Ingredients (APIs)

At present, policy-driven production suspensions and restrictions in the active pharmaceutical ingredient (API) industry are expected to continue, with intensified monitoring and regulatory enforcement.

The latest policy is that on August 21, the Ministry of Environmental Protection, in conjunction with 15 other departments including the National Development and Reform Commission, the Ministry of Industry and Information Technology, and the Ministry of Public Security, jointly issued the “Action Plan for the Campaign to Comprehensively Control Air Pollution in the Beijing-Tianjin-Hebei Region and Its Surrounding Areas During the Autumn and Winter Seasons of 2017–2018.”

The plan specifies that most areas of Beijing, Tianjin, Hebei, Shanxi, Shandong, and Henan must implement optimized production controls for the non-ferrous chemical industry during the autumn and winter seasons. Pharmaceutical enterprises involved in active pharmaceutical ingredient (API) production with processes emitting volatile organic compounds (VOCs) are, in principle, required to suspend operations during the heating season. If production is indeed necessary due to special circumstances such as public livelihood needs, approval must be obtained from the provincial people's government.

The heating season in northern China runs from November 15 of the previous year to March 15 of the following year, which meansOver the course of a full quarter, production of active pharmaceutical ingredients (APIs) will be constrained, which will also impact future API prices.

Overview of the Domestic API Market and Key Enterprises

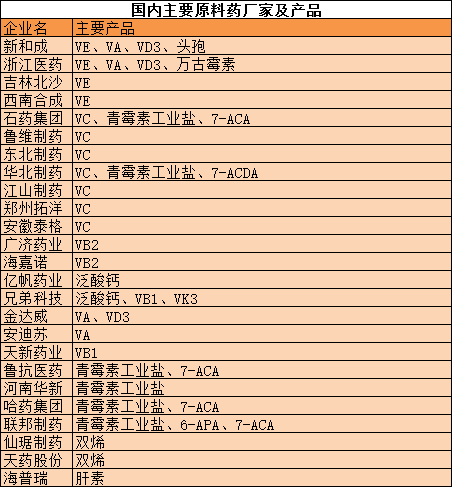

Major domestic API manufacturers include NHU, Zhejiang Medicine, CSPC Pharmaceutical Group, North China Pharmaceutical Group, Henan Huaxing, Harbin Pharmaceutical Group, and The United Laboratories. From the industry level to the corporate level, the impact on company performance varies due to differences in their main products. The following analysis will focus on products, incorporating the situations of major API manufacturers.

Vitamins

Taking vitamin E as an example. The current global total production capacity of vitamin E is approximately 100,000 metric tons, with average annual output growing at a rate of 2–5%. Its downstream applications are primarily in animal feed, which accounts for about 80% of demand, while demand from the pharmaceutical and food sectors is relatively small.

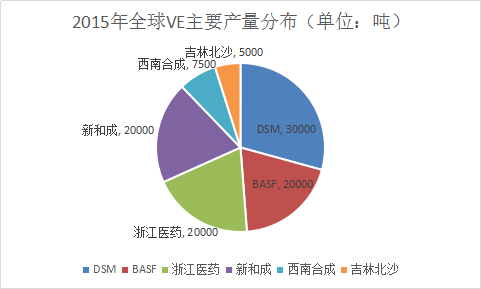

From the manufacturer's perspective,Currently, four major international manufacturers control approximately 90% of the global vitamin E supply, collectively known as the “Big Four”: DSM, BASF, NHU, and Zhejiang Medicine.Production capacity is primarily distributed as follows: DSM, 30,000 tons; BASF, 20,000 tons; Zhejiang Medicine, 20,000 tons; NHU, 20,000 tons; Jilin Beisha, 5,000 tons; and Southwest Synthetic Pharmaceutical, 7,500 tons. In addition, Guanfu Shares is constructing a vitamin E production line with an annual capacity of 20,000 tons, which may break the oligopolistic dominance of the four major suppliers in the vitamin E market.

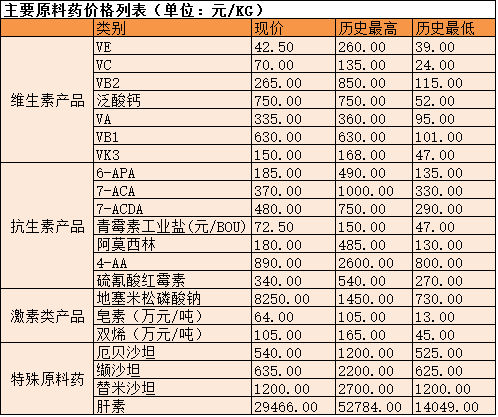

The price trend of vitamin E (VE) has undergone several phases. Before 2003, DSM and BASF expanded production capacity, leading to market oversupply and low prices. Starting in 2007, VE market demand approached equilibrium. In 2008, Chinese manufacturer Adisseo announced its withdrawal from the market, causing prices to surge temporarily. After 2009, an oligopoly dominated by four major players emerged, resulting in narrowed price fluctuations. In the second half of 2014, VE prices briefly rose to RMB 90/kg. This price level began to decline in 2015, with foreign manufacturers temporarily suspending quotations, and prices eventually settling at RMB 45–50/kg.

According to customs data, China's vitamin E (VE) export volume last year was 61,300 metric tons, a year-on-year decrease of 0.74%. In July this year, the monthly export volume reached 5,119.02 metric tons, a month-on-month increase of 4.2%, with an average unit price of $5.89 per kilogram, a month-on-month decrease of 7.58%.

According to data from SunSirs, the quoted price for feed-grade vitamin E in mid-August was 45 yuan/kg.Affected by environmental protection-related production restrictions, vitamin E prices may rise slightly, with the 2017 price range expected to be RMB 35–90 per kilogram.

Antibiotics

Taking penicillin industrial salt as an example. Penicillin industrial salt serves as a shared raw material for all penicillin-class antibiotics (those ending in "-cillin") and certain cephalosporin antibiotics, playing an extremely important bridging role in the antibiotic industry.

Among the downstream products of penicillin industrial salt, approximately 50% is used as raw material for 6-APA, and nearly 30% is exported, with India being the primary export destination. Most manufacturers of penicillin industrial salt have integrated downstream industry chains. Global demand stands at approximately 60,000–70,000 tons, while China’s production capacity exceeds 100,000 tons, resulting in significant overcapacity and poor industry profitability.

China's major manufacturers of industrial penicillin salts include CSPC Zhongrun Pharmaceutical, Henan Huaxing, The United Laboratories, North China Pharmaceutical Group, and Harbin Pharmaceutical Group. Among them, CSPC Group has an annual production capacity of 18,000 metric tons, ranking first in the industry.

Since the 1980s, the penicillin G potassium salt industry has experienced seven major price wars due to overcapacity, each of which led to a reshuffling of the industry landscape. After the 2008 financial crisis, prices for penicillin G potassium salt began to decline, dropping below RMB 60/BOU to as low as RMB 56/BOU. Since 2011, with the implementation of regulations restricting antibiotic use, penicillin prices have shown a slight upward trend. According to data from SunSirs, the current quoted price for penicillin G potassium salt is RMB 72.5/BOU. (BOU is an abbreviation for Billion Units, referring to one billion antibiotic activity units.)

Steroids

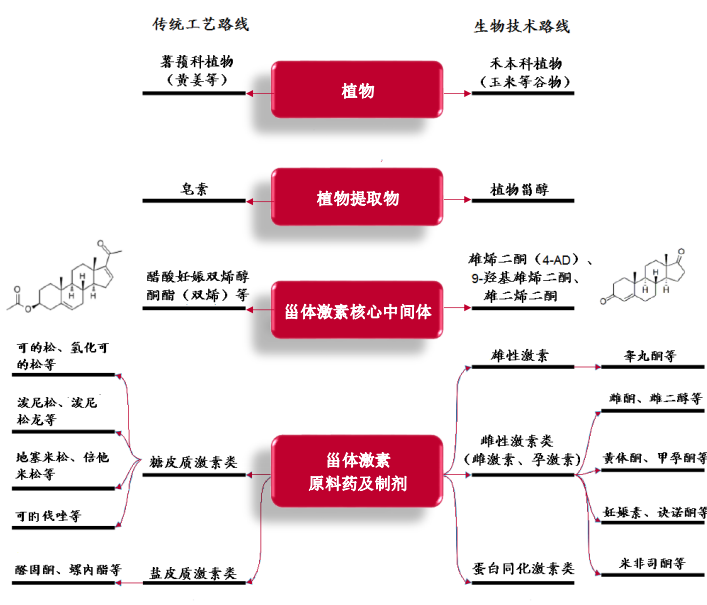

There are two manufacturing process routes. The traditional route uses Dioscorea plants (such as yellow ginger) as starting materials to obtain plant extract diosgenin, which is further processed into core steroidal hormone intermediates for the production of active pharmaceutical ingredients (APIs) and formulations. The biotechnological route uses Gramineae plants (such as corn and other grains) as raw materials to obtain phytosterols through microbial transformation, which are then used to prepare core intermediates such as androstenedione (4-AD) and 9-hydroxyandrostenedione, ultimately yielding steroidal hormone APIs and formulations.

Steroid Drug Production Pathway

Source: Saito Bio's Prospectus, Zhongtai Securities Research Institute

Currently, the domestic steroid drug and active pharmaceutical ingredient (API) industry is highly concentrated, with companies such as Tianjin Tianyao, Xianju Pharmaceutical, Zhejiang Xianju Junye Pharmaceutical, and Tianjin Jinjin Pharmaceutical occupying the majority of the market share.

Dienes are the most critical raw materials in the steroid pharmaceutical industry, with domestic demand exceeding 2,000 tons and a market value of over RMB 2 billion. The price of dienes rose from a low of RMB 400,000 per ton in 2007 to a peak of RMB 1.6 million per ton in 2013. Since 2013, prices have been on a continuous decline, with the current quoted price at RMB 1.05 million per ton.

Currently, diene manufacturers are undergoing a transition in their process pathways, leading to reduced costs and an improved competitive landscape, with prospects of emerging from the current price trough. It is anticipated that, under increasing environmental regulatory pressure, smaller manufacturers will gradually exit the market, thereby further enhancing market concentration.

Specialty Active Pharmaceutical Ingredients

Mainly sartans and heparins.Sartans are currently the mainstream products in the field of hypertension treatment, representing the largest class of antihypertensive drugs on the global market, with total sales exceeding $25 billion.According to IMS data, most global sartan products have reached the blockbuster level of billions of dollars. Valsartan, which has long held the top position, once achieved sales exceeding $9 billion. Olmesartan currently ranks second with sales of $4.8 billion.

Sartan active pharmaceutical ingredients (APIs) are primarily used to manufacture sartan-class antihypertensive drugs. Major varieties include losartan, valsartan, irbesartan, candesartan, telmisartan, and olmesartan, as well as key intermediates such as sartan biphenyl. The first three exhibit the highest sales volumes. In China, the sartan APIs with relatively large production scales are mainly losartan, valsartan, and irbesartan, along with the core sartan intermediate: 2-cyano-4'-methylbiphenyl.

There are nine manufacturers in China producing sartan-class active pharmaceutical ingredients (APIs), such as valsartan and irbesartan. Among them, only Zhejiang Huahai Pharmaceutical and Zhejiang Tianyu Pharmaceutical (which obtained certification in 2010) have secured Certificates of Suitability (COS) for the European and U.S. markets; the remaining companies primarily serve the domestic market as well as those in Asia, Africa, and Latin America. Meanwhile, 70–80% of sartan drug sales occur in Europe and the United States.Moreover, generic drugs with patents expiring in the coming years are primarily marketed in Europe and the United States; therefore, companies that obtain regulatory approvals in these regions will determine the landscape of the active pharmaceutical ingredient (API) market.

Average Prices in July 2017: Valsartan at RMB 635/kg, with month-on-month price stability; Telmisartan at RMB 1,200/kg, with month-on-month price stability; Irbesartan at RMB 540/kg, with month-on-month price stability. With the rising prominence of these three sartan-class pharmaceuticals in the future, demand for active pharmaceutical ingredients (APIs) is expected to increase, potentially leading to a moderate price recovery.

Heparin active pharmaceutical ingredient (API) is prepared from crude heparin extracted from the small intestinal mucosa of healthy pigs. It serves primarily as a raw material for antithrombotic and anticoagulant drugs, such as low-molecular-weight heparin formulations. The global demand for heparin API is approximately 230 metric tons. Chinese manufacturers supply 60% of this global demand. With China’s heparin API production capacity standing at around 220 metric tons, domestic capacity utilization remains tight.

Developed countries in Europe and the United States are the primary global consumer markets for heparin-based drugs, as well as the main export destinations for China’s heparin active pharmaceutical ingredients (APIs).Currently, Hepalink holds approximately 40% of the domestic market share. Other major manufacturers include Nanjing King-Friend, Changzhou Qianhong, Yantai Dongcheng, and Hebei Changshan.

Customs export data show that the total volume of heparin exports in 2016 was 170.15 metric tons, a year-on-year increase of 13.96%. In July 2017, the export volume was 13.87 metric tons, a year-on-year decrease of 6.27%, while the average export price was $4,453.45 per kilogram, a month-on-month increase of 7.44%.Constrained by raw material supply and technical barriers, the supply of heparin active pharmaceutical ingredients (APIs) is not expected to undergo significant changes in the future, with prices remaining subject to minor fluctuations.

Appendix:

References:

High-Barrier Specialty Pharmaceutical Brand: Leading the Upgrade of Domestic Steroid Drugs

http://data.eastmoney.com/report/20170222/APPHhnIFZ4vvASearchReport.html

"Drug Administration Law of the People's Republic of China"

http://www.sda.gov.cn/WS01/CL0784/124980.html

Knowledge of Chemical Synthesis for Active Pharmaceutical Ingredients (APIs)

http://www.360doc.com/content/16/0610/23/723238_566621701.shtml

Zhejiang Province Issues Emission Standards for Atmospheric Pollutants from Chemically Synthesized Pharmaceutical Manufacturing, Strictly Controlling VOCs Emissions

http://huanbao.bjx.com.cn/news/20170104/801339.shtml

Chemical API Report - Regulatory System and Policy Regulations of China's Chemical API Industry in 2017

http://www.chinabaogao.com/site/zhengce/huagong/2017/05262tq22017.html

20170906-Industrial Securities-Monthly Report on Prices of Major Active Pharmaceutical Ingredients (APIs): Focus on Environmental Protection Variables and Emphasize Price Elasticity