Oral Healthcare in 2017: Capital Fuels Chain Expansion, Dentists Become Partners, and Digital Dentistry Matures

The dental industry is a highly market-driven segment of consumer healthcare. Propelled by capital investment, large chain providers are rapidly expanding into second- and third-tier cities to capture market share and talent. Meanwhile, encouraged by policy reforms, dentists are increasingly engaging in multi-site practice and launching their own ventures. Acceptance and penetration of orthodontics, dental implants, and restorative procedures continue to rise. Technologically, the maturation of intraoral scanning, CBCT, and 3D printing has laid the groundwork for the development of digital dentistry. So, what changes occurred in the dental industry in 2017? The following section outlines the key trends observed this year.

In recent years, funds of various sizes, private capital, and private equity crowdfunding have continuously invested in the dental industry chain. Capital inflow into the dental economy did not cease in 2017. There have already been five financing rounds this year, each amounting to RMB 50 million or more.

In January, Yayi Guanjia announced that it had secured RMB 100 million in Series A financing, led by Ping An Innovation Investment Fund under the Ping An Group, with participation from Housheng Capital and Chende Capital.

In March, Malong Dental announced that it had secured RMB 110 million in Series C financing, led by Gopher Capital, with co-investment from Starvest Capital and Honghui Capital.

In August, Jinsong Dental Medical Group entered into a strategic cooperation agreement with Taikang Asset Management Co., Ltd., securing approximately RMB 200 million in financing;

In August, Arrail Group announced that it had secured $90 million in Series D financing, invested by Goldman Sachs Group and Hillhouse Capital.

In September, Shanghai Smartee Dental Technology Co., Ltd. announced the completion of its RMB 50 million Series B financing round, which was co-led by Venshare Capital and Chende Capital, with Dongzi No.1 Fund participating as a follow-on investor.

Apart from Dental Manager and Zhengya Orthodontics, the other three are all dental chains, which are precisely the core targets of significant capital investment; the trend of clinic expansion continues.

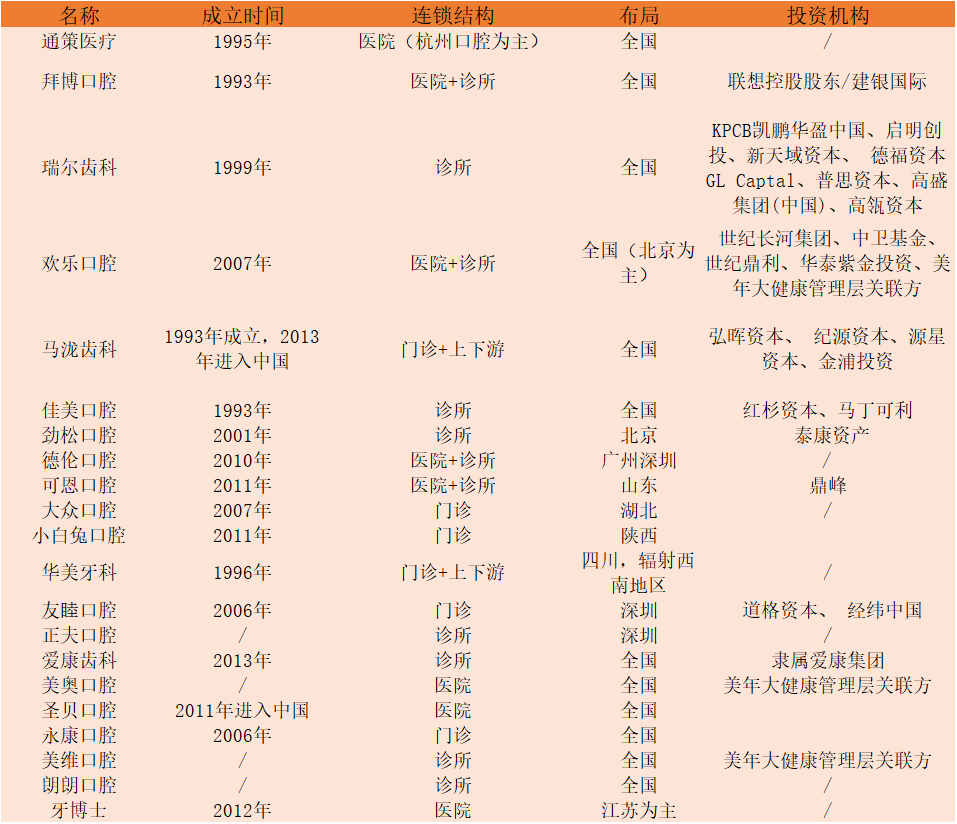

Major Dental Chain Clinics in the Market, Compiled from Public Sources

According to VCBeat statistics, there are 18,300 public general hospitals and specialized dental hospitals in China, along with 80,000 private dental hospitals and clinics, achieving a compound annual growth rate of 30%. However, the total number is only one-quarter that of the United States, while the number of patients covered per dentist in China is eight times that in the U.S.

Drawing on the development trajectory and pace of large chain clinics in the United States, and against the backdrop of high disease prevalence yet low consultation rates in China, it is foreseeable that as household incomes rise and awareness of dental care consumption strengthens, the total number of large and medium-sized public hospitals will grow slowly while their market share declines. Non-branded individual dental practices will be gradually replaced by branded dental chains, although small, single-site clinics currently remain dominant.

In addition to private capital, central state-owned enterprises (SOEs), provincial SOEs, municipal and prefectural local SOEs, and research institutes have also joined the strategic expansion of the dental industry. On April 25, Huaxi Dental Co., Ltd. was officially unveiled, with plans to establish a nationwide chain of 500 dental healthcare service terminals by 2025.

Data shows that Huaxi Dental has five major shareholders: Sichuan Provincial Investment Group Co., Ltd., Sichuan University, Sinopharm Holding Co., Ltd., China Life Chengda (Shanghai) Health Industry Equity Investment Center (Limited Partnership), and Ziyang Development Zone Investment Co., Ltd. The registered capital is RMB 1.8 billion, and 13 banks have jointly extended a credit line of RMB 212 billion to the company.

Huaxi Dental focuses on six major business segments: dental industry manufacturing, healthcare services, R&D and outcome incubation, education and training, commercial insurance, and products and commercial services, thereby covering nearly the entire dental “industry chain.”

It is worth noting that, in terms of property format, dental clinics have also become standard tenants in the increasingly popular “Medical Mall” model this year. On April 6, Wanda Group signed an agreement with the Chengdu Municipal Government to invest RMB 70 billion in building a medical industrial park in Chengdu’s healthcare sector, aiming to develop and operate a batch of world-class healthcare industry projects.

Meanwhile, Wanda also plans to invest RMB 9 billion in a strategic partnership with West China School of Stomatology to open 300 dental clinics across Wanda Plazas nationwide.

Compact yet exquisite dental clinics, complemented by premium services, have established a strong complementary relationship with other business models in Wanda Plaza, effectively integrating existing advantageous resources. In terms of resource integration, Tianyi Group and the Meinian ecosystem have also made significant strides in strategic layout and consolidation within the oral care sector.

In the long term, given China’s large population base and high prevalence of dental diseases, along with the increasingly widespread acceptance of high-value orthodontic, implant, and restorative procedures, the oral care industry boasts broad prospects. With the current low level of asset securitization in the sector, the oral care industry will continue to attract significant capital attention.

However, dental chain clinics exhibit strong regional characteristics, with customer acquisition primarily driven by local markets; thus, brand synergy cannot be established in the short term.

As a highly marketized sector, dental clinics face relatively low medical risks and are indeed one of the most active areas for private capital. However, contrary to expectations, the profitability of dental institutions has not been as robust as anticipated.

In early 2017, the large standalone Aux Dental Clinic, which had been in operation for less than 11 months, announced its closure. A rough estimate of its costs revealed that with a business area of 3,030 square meters located on the East Third Ring Road in Chaoyang District, Beijing, monthly rent and property management expenses amounted to as high as RMB 1 million. In terms of physician costs alone, the fixed monthly personnel expenditure was estimated at approximately RMB 280,000. These two items alone resulted in fixed monthly costs totaling RMB 1.28 million.

At its inception, Aux Group planned to invest RMB 3 billion over three to five years to establish a nationwide dental care network of 30–50 clinics through mergers and acquisitions and new builds, aiming to become a leading dental chain in China. Profitability concerns have loomed like the Sword of Damocles over capital-backed dental chains.

Profitability of Listed Oral Care Companies (Non-Device)

As the largest private dental chain in China, Bybo Dental received strategic investment from Legend Holdings in July 2014. As of June 30, 2017, Legend Holdings held a 54.90% equity stake in the company.

Legend Holdings’ interim report shows that Bybo Dental had 207 outlets, including 55 hospitals and 152 clinics, representing a 15% increase from the 180 outlets recorded at the end of June 2016, with coverage across 25 municipalities and provinces. The number of dental chairs increased from 2,290 in mid-2016 to 2,742 in 2017.

Looking at the profitability, the revenue in the first half of the year was 650 million yuan, a year-on-year increase of 13%, and the net loss increased from 367 million yuan in the first half of 2016 to 406 million yuan. Comparing with the full-year data of 2016, the revenue was 1.257 billion yuan, and the net loss was 795 million yuan.

Bybo Dental's Profitability Over Three Consecutive Years

Regarding the reasons for the simultaneous growth in revenue and losses, the report points out that the main factors include: the growth of mature stores has slowed down due to the opening of new stores by other brands in the same city and industry competition; meanwhile, there is a large number of hospitals and clinics that have been established for less than one year, with their business still in the ramp-up phase, and significant financial expenses during the expansion period.

This broadly reflects the current market conditions for dental chain clinics this year. Since the inception of dental chains in 2000, followed by the capital frenzy after 2010, various factors—including shortages of professional talent, high rental and property costs, expensive customer acquisition costs, and lagging training—have led to a situation where, while capital has driven rapid growth in the number of outlets, enterprises have often become trapped in asset-heavy business models.

Currently, the expansion of large dental chains has slowed down. Compared to 2016, Bybo Dental added only seven clinics in the first half of 2017, aiming to adopt a headquarters-direct management model. Similarly, Jia Mei Dental and Arrail Dental have also decelerated their aggressive expansion from previous years and are now in a transitional adjustment phase.

Unlike Bybo Dental’s asset-heavy model, some dental enterprises have entered the market with an asset-light approach, notably Meiwei Dental and Langlang Dental. Of course, there are significant differences between the two in terms of their business models, operational methods, and industrial resource synergies. In addition to physical clinics, they also leverage synergistic resources such as software and cloud platforms.

Meiwei Dental adopts a “partnership + self-development” model, acquiring regionally dominant brands such as Xinqiao Dental and Zhongshan Stomatological Hospital, which has collaborative ties with academic institutions, with a primary focus on acquisitions in the early stages.

Co-founder Julia stated in an interview with 39 Health Network, “We will seek controlling stakes, but this is not merely a financial investment. We will not change the brand name; instead, we aim to establish a business partnership model built on mutual tolerance, understanding, and support. We will provide comprehensive support to our business partners in customer acquisition, management, training, and expert talent.”

Langlang Dental also boasts a strong investor background. Its expansion strategy involves partnering with independent clinics through non-cash arrangements, imposing requirements on partners’ profitability and performance growth, while allowing clinic owners to retain significant operational autonomy.

VCBeat believes that asset-light operating models, whether structured as partnerships or involving valuation adjustment mechanisms (VAMs) with investors, must address comprehensive challenges including talent and technology acquisition, internal management, integration of external cross-industry resources, and marketing. Furthermore, requirements for subsidiary companies will continue to increase over time. With the addition of other branded chains, chain operations and management models remain in a state of dynamic evolution even after capital intervention.

Branded chain clinics are not the end of the business model; this is merely the beginning. The dental industry will become a battleground for talent in the future, with the costs of professional dentists and management and operational personnel continuing to rise.

Relatively speaking, individual practitioners or community clinics with a strong physician-led brand identity have demonstrated robust profitability. For instance, Huajing Dental, founded by He Zhou, benefits from a high-quality customer base acquired primarily through word-of-mouth referrals. While such high-value patients are expected to constitute the majority in the future, not every clinic possesses the combination of technical expertise, team capability, strategic direction, and medical ethics exemplified by physicians like He Zhou.

In VCBeat’s 2016 annual review, a total of 36 companies were cataloged across the sectors of dental SaaS, internet-based patient referral, B2B services, and physician services. These companies shared the common characteristic of “dentistry + internet,” with their core clientele being dental clinics and dentists. In 2017, from a financing perspective alone, this category was not a major focus; apart from Yayi Guanjia (which offers both software systems and dental equipment/devices), there were few publicly disclosed funding rounds.

This year, apart from the aforementioned clinics, the types of companies in the dental industry that have secured financing are mainly focused on devices, technology, and marketing operations, such as Smartee (clear aligners), Youyiji (medical devices and equipment), Aircon Medical (medical devices and equipment), Byndent (service platform), and LeShasha (orthodontic treatment).

After several years of exploration and development, oral care internet companies have entered various stages and situations, including ceasing operations, seeking financing, establishing stable niche businesses, or beginning to transform. Leya Network, Aiya Ku, and Aiyouya have gradually emerged as leading platforms with strong development momentum.

Certainly, the development and evolution of the industry are inseparable from policy support. This year, the most significant influences have been the opening up of multi-site practice for physicians and policy incentives encouraging socially run medical institutions.

In the dental industry, talent is in severe shortage and is widely recognized as a bottleneck constraining industry development. The pace at which excellent dentists are trained falls far short of market demand, creating a theoretical market for multi-site practice.

Large institutions are actively seeking talent through external technological collaborations, talent recruitment, and internal development programs. For instance, Deng Feng, President of Bybo Dental Medical Group, formerly served as Dean of the Stomatological Hospital of Chongqing Medical University and Director of Chongqing Stomatological Hospital.

On February 21, the National Health and Family Planning Commission issued the “Decision on Amending the Detailed Rules for the Implementation of the Regulations on the Administration of Medical Institutions” (National Health and Family Planning Commission Order No. 12), which removed the provisions in the original rules that restricted practicing physicians from engaging in multi-site practice and independent entrepreneurship.

On April 25, the General Office of the State Council issued the "Key Tasks for Deepening the Reform of the Medical and Health Care System in 2017," proposing to prioritize the advancement and implementation of tasks such as "formulating guidelines for establishing a modern hospital management system" and "developing opinions to support social forces in providing multi-level and diversified medical services."

The “Opinions on Supporting Social Forces in Providing Multi-Level and Diversified Medical Services,” issued in May, further clarified the objectives. It requires that by 2020, the capacity of socially operated medical institutions be significantly enhanced; medical technology, service quality, and brand reputation be markedly improved; support systems such as professional talent, health insurance, and pharmaceutical technologies be further strengthened; and the overall environment for industry development be comprehensively optimized. The goal is to build a large number of socially operated medical institutions with strong service competitiveness.

In August, the National Health and Family Planning Commission issued the "Notice on Deepening the Reform of 'Streamlining Administration, Delegating Power, Improving Regulation, and Upgrading Services' to Stimulate Investment Vitality in the Medical Field," which stated that the approval procedures for medical institutions should be further simplified, and the setup approval and practice registration for secondary and lower-level medical institutions should be merged into a single certificate.

These policies play a significant role in promoting multi-site and independent practice among physicians, stimulating their enthusiasm for providing medical services, encouraging private capital investment in the healthcare industry, and accelerating the development of privately run medical institutions.

Specifically in the dental industry, the following trends are quite evident:

Dental SaaS companies, such as Linker Health and Qiezi Dental Cloud, are not only racing to capture market share by signing up clinics of all sizes but also ramping up their sales of consumables and equipment, as well as expanding into financial installment services.

Internet referral platforms, such as Haoyaishi, have begun to penetrate the offline market after initially aggregating physician resources, deeply engaging in clinic operations through self-built, acquired, or managed models.

B2B and physician services, multi-site practice, and physician groups are market-validated viable models.

Yabohui Dental Physician Group addresses the capital and technical needs of dentists establishing clinics by focusing on chain clinics through talent development, expert technical support, standardized software and hardware modules, and centralized equipment procurement. The York Dentist Platform facilitates multi-site practice for dentists. Aiya Ku, a B2B vertical e-commerce platform under Yabang, enters the market through basic consumables and small equipment, deeply connecting dental consumable manufacturers with hospitals to replace traditional distributors.

In addition, there are enterprises such as Aiya Youxuan that assist dental hospitals in conducting oral care education and popular science initiatives, help doctors build their personal brands, and establish a “dentist + professional manager” model.

For such enterprises, whether the entities involved are dentists, clinics, or upstream and downstream suppliers of consumables, equipment, and dental prosthesis processing plants, mastering data is crucial. Only by forming a complete closed loop of "data + capital + technology," especially with global technological resources, can they maintain the greatest competitive advantage in future competition.

Benefiting from the “universal two-child” policy, data from the National Bureau of Statistics shows that 17.86 million babies were born in China in 2016, a year-on-year increase of 7.9%, with a significant rise in the birth rate, presenting favorable opportunities for the maternal and infant health sector. The National Health and Family Planning Commission predicts that approximately 3 to 4 million additional newborns will be added annually in the coming years, heralding the arrival of China’s fourth baby boom.

China’s pediatric dentistry market lags far behind that of the United States, presenting substantial room for growth. China’s dental services market is currently valued at approximately RMB 100 billion, and it is entirely plausible that it will evolve into a trillion-yuan market within the next decade—reaching the same scale as the U.S. market today. The pediatric dentistry segment alone is poised to become a market worth at least hundreds of billions of yuan. This represents a significant opportunity for all entrepreneurs.

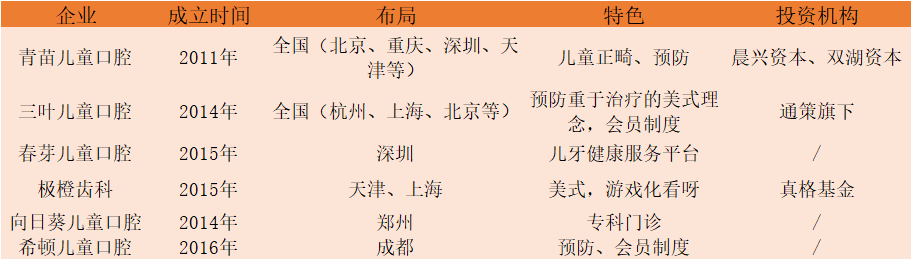

Branded Pediatric Dental Chains and Health Management Platforms on the Market

Oral health in children is the cornerstone of overall health, the foundation for cultivating good dietary habits, and has a significant impact on the morphology of the maxillofacial region and systemic development. Interventions for dentofacial deformities primarily follow American and Japanese models.

The American Academy of Pediatric Dentistry recommends that most children undergo oral examinations at least twice a year. Depending on individual risk factors for dental caries, developmental abnormalities, or poor oral hygiene, some children may require more frequent visits. Commonly performed procedures include pediatric dental treatment under general anesthesia, management of traumatic injuries to primary teeth, and intervention for malocclusion.

Early prevention and intervention are particularly critical components of pediatric oral health management.

There are few institutions in the market specifically dedicated to pediatric dentistry. Only slightly over 2,200 pediatric dentists are registered with the Pediatric Dentistry Committee of the Chinese Stomatological Association, resulting in significantly limited options for children’s dental care. Many clinics simply do not treat very young children. The key challenge in pediatric dentistry is children’s fear of dental visits. There is a notable lack of dental care settings where children feel unafraid.

VCBeat has compiled data on several pediatric dental brands, most of which were established after 2014. Operating these clinics generally requires moving beyond the conventional chair-side mindset. Concepts such as environmental design, assistant-led reception, and the consultation approach of pediatric dentists (who are currently mostly general practitioners) differ significantly from those in adult dentistry.

The primary dental issues in children are dental caries and malocclusion. The traditional view holds that the optimal time for orthodontic treatment of malocclusion is after the age of 12. However, by this stage, children have already completed the transition from primary to permanent dentition, which may necessitate tooth extraction as part of the orthodontic intervention.

Romu Chimeikang Appliance is a professional product specifically designed for early orthodontic treatment of malocclusion in children aged 5–12 years during the mixed dentition period, utilizing internationally prevalent and mainstream technologies. In 2011, Romu was introduced to China, with clinical studies initially conducted at Peking University School of Stomatology. Professor Ge Lihong from Peking University School of Stomatology carried out extensive clinical research, demonstrating the efficacy of Romu occlusal guidance.

Qingmiao Pediatric Dentistry has introduced this occlusal guidance technology, with a specialty in treating mild malocclusion in children aged 5–12. It has currently established clinics in Beijing, Shanghai, Guangzhou, Chengdu, Shenzhen, Tianjin, Chongqing, and other cities.

Dr. Zhang Ye, founder of Sanye Pediatric Dentistry, has many years of experience in pediatric dental care in the United States and Japan. Led by her, the technical team adheres to the American philosophy that “prevention is more important than treatment,” providing children with dental health services through a membership-based model and implementing family-oriented oral health management.

Overall, pediatric dental treatment in China is still in its early stages. Both technically and conceptually, many doctors and parents face challenges and concerns in clinical practice. Similarly, companies must address these issues in terms of talent acquisition, customer acquisition, patient education, and management.

On September 16, 2017, in the operating room of the Department of Dental Implantology at the Stomatological Hospital of Air Force Medical University in Xi’an, an autonomous dental implant surgical robot successfully performed immediate restoration with two dental implants for a female patient, following pre-programmed instructions and under the assistance of Professor Zhao Yimin, a renowned expert in prosthodontics in China, and his team.

During the surgery, a software system for oral implant planning, surgical navigation, and robotic control was developed, achieving precise planning of personalized implant schemes, real-time intraoperative navigation, and autonomous robotic control.

The successful implementation of this procedure marks the debut of the world’s first autonomous robotic system for dental implant surgery. Although it is still a long way off to declare that large-scale clinical treatment of oral diseases has entered the era of robotics, dental digital technology has indeed become increasingly mature compared to a decade ago, driven by the widespread adoption of 3D printing, intraoral scanning, and cone-beam computed tomography (CBCT) devices.

The rapid development of digital technologies in dentistry in recent years is primarily attributed, at the technical level, to their ability to enhance the precision of clinical diagnosis and treatment, reduce procedural risks, and improve diagnostic and therapeutic efficiency.

These technologies include intraoral scanning, cone-beam computed tomography (CBCT), digital diagnosis and design, digital manufacturing technologies and materials, robotics, and web-based integrated cloud services. They enable diagnostics based on 3D/4D dynamic imaging data, quantitative diagnostic analysis, treatment planning and prosthetic design, as well as precise, quality-controlled prosthetic fabrication and precision therapy.

Furthermore, the demand for orthodontic, implant, and restorative surgical procedures is growing. For instance, with the continuous improvement of hardware and software, guide systems have effectively reduced errors.

In early October this year, VCBeat conducted a market scan of the intraoral scanner and CBCT sectors. Currently, dentists, clinics, and hospitals have widely and fully accepted intraoral scanners, CBCT devices, and their accompanying software. CBCT is an essential adjunct to dental implant services; any facility offering implants must be equipped with CBCT. The introduction of such new services provides clinics and hospitals with additional promotional angles and revenue streams, ensuring their ready acceptance.

Currently, more than ten intraoral scanning systems have been launched internationally, including those from 3Shape (Denmark), iTero (USA), Lythos (USA), CEREC (Germany), 3M Lava (USA), Dental Wings (Canada), and Planmeca (Finland). In China, companies such as Guangdong Langcheng, Shenzhen Fussen, and Hangzhou Shining 3D Technology have also introduced their intraoral scanning systems. In the domestic market, the installed base of dental CT scanners of various specifications exceeds 23,000 units, with approximately 4,000 CBCT units across the entire market. In addition to foreign brands such as Sirona, KaVo, Morita, Planmeca, and NewTom, Meiya Optoelectronic, LargeV, Fussen, and Born Dental are all Chinese manufacturers possessing independent intellectual property rights for CT technology.

For instance, when integrated with orthodontic software such as 3Shape and ExoCAD, CBCT enables clinicians to pay closer attention to the thickness, height, and functional remodeling of the labial and lingual bone plates during orthodontic treatment. This is crucial for achieving high-quality orthodontic outcomes, ensuring long-term post-treatment stability, and maintaining periodontal health.

With the assistance of implant planning software such as Simplant, Nobel Clinician, and 3Shape, CBCT devices can facilitate the design of implant surgeries and the fabrication of surgical guides. This enables precise control over implant position, angulation, length, and diameter, thereby ensuring the success of both the surgical procedure and subsequent prosthetic restoration. Minimally invasive implant techniques have also emerged as a prominent trend this year. Companies like Cai Lifang and GuideMia Technology have accumulated a substantial client base and data resources in the field of digital surgical guides, gradually establishing dental implants as a significant niche market.

The dental care market is in a phase of steady development, creating opportunities for the growth of the denture processing industry. Meanwhile, patients and medical institutions have raised higher expectations for the quality of denture products, as well as for the service standards and management compliance of denture manufacturers. Regulatory authorities have also intensified their oversight of the industry.

(New Third Board Listings: Jiahong and Huge Terminate Listings) Profitability of denture processing, medical device manufacturing, and sales companies is better than that of clinics.

Thus, a visible trend this year is that many companies are continuously increasing their R&D investments, particularly in the digital sector, while introducing imported high-end precision manufacturing equipment to enhance their production capabilities for high-precision products, thereby significantly boosting product competitiveness.

The development of the dental industry relies heavily on new clinical technologies, as well as novel equipment and instruments. VR-Sens has innovatively applied VR technology vertically to the field of dental healthcare, which is highly dependent on manual dexterity and visualization technologies. By leveraging computer graphics systems and VR medical imaging systems, VR-Sens has established a VR-based environment for dental education and surgical simulation. Furthermore, through motion capture systems within the virtual platform, users can directly interact with people and objects in the virtual world, providing operators with an immersive experience for learning, surgical simulation, and hands-on practice.

Zhengya Dental, which announced the completion of its RMB 50 million Series B financing round this year, is primarily engaged in providing digital orthodontic technology services and developing clear aligner products. Its independently developed “SmartCheck Clear Aligner Treatment Planning System” and “Smartee Customized Clear Orthodontic Aligners” both possess complete independent intellectual property rights. As of September, Zhengya Dental had accumulated tens of thousands of cases, with cumulative sales revenue approaching RMB 100 million.

However, what remains lacking are robust training and after-sales support, as well as solutions to the challenges of managing data generated through digitalization and standardizing associated services.