Medical Big Data: Weak Infrastructure Persists, but 2017 Saw Entry of National Champions and AI Firms—Poised to Ignite a Red Ocean Battle [2017 Year-End Review]

Looking back at the medical big data industry in 2017, we can broadly draw the following conclusions:

1. The foundation of medical big data remains underdeveloped;

2. The national team’s role as an industry benchmark and model in medical big data may drive the development of the entire medical big data sector;

3. Medical big data companies are transitioning from an exploratory phase to a mature phase, with breakthroughs in both the depth and breadth of their business operations;

4. AI companies may engage in market competition with medical big data firms over data analytics.

Top-Level Policies Establish Three Major Data Development Frameworks

The “Guiding Opinions of the General Office of the State Council on Promoting and Standardizing the Application and Development of Health and Medical Big Data,” issued in June 2016, set the tone for the development of health and medical big data. With the further advancement of the “Healthy China 2030” Planning Outline, health and medical big data has become an important foundational strategic resource for the nation.

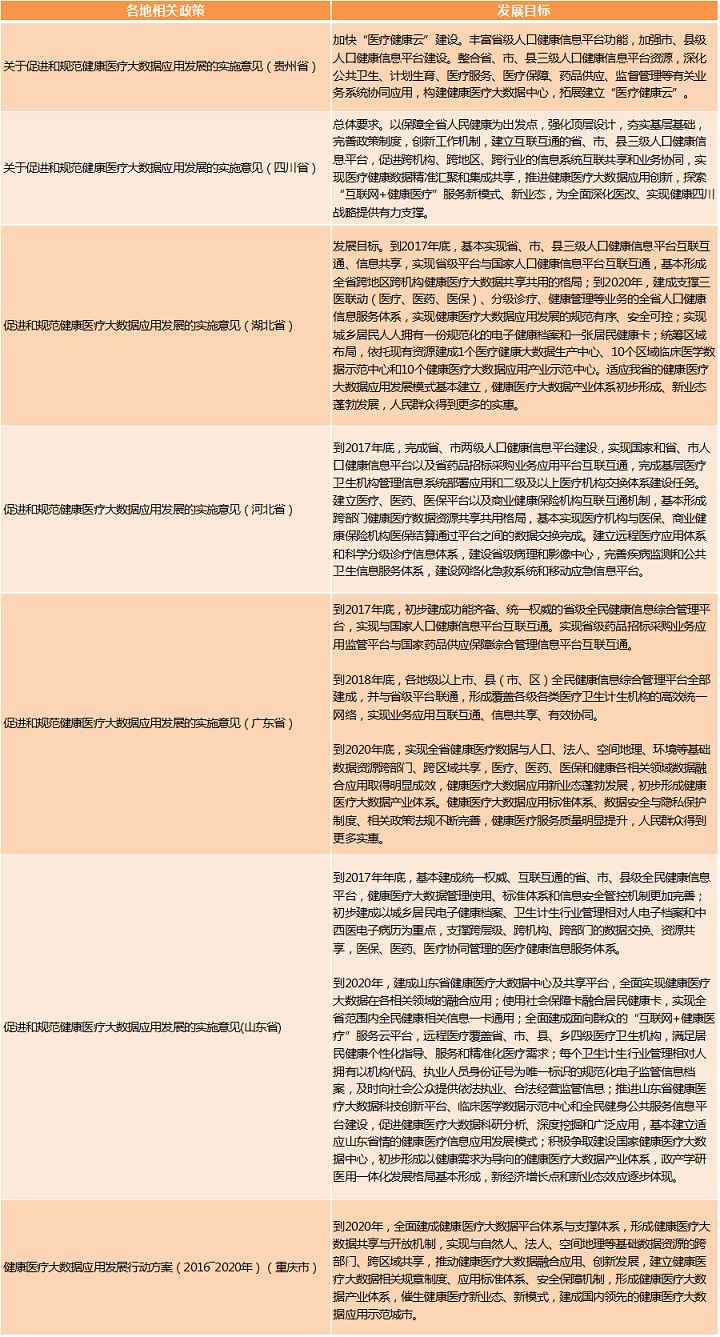

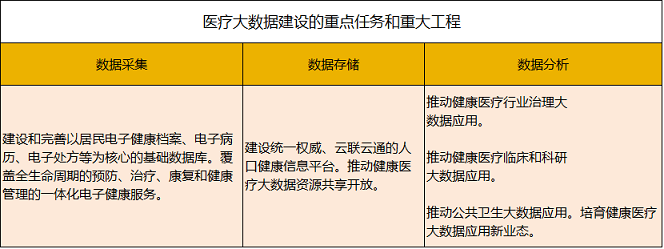

VCBeat has reviewed the policies outlined in the “Implementation Opinions on Promoting and Regulating the Application and Development of Health and Medical Big Data” issued by seven provinces across China from late 2016 to 2017. By summarizing their development goals and key tasks, we have identified the following three core elements (as shown in the figure):

As shown in the figure, if the data is divided into three core segments, it can be categorized into data acquisition, data storage, and data analysis.

At the China Hospital Information Network Conference (CHINC) held in August 2017, the Electronic Medical Record Pilot Office of the Hospital Management Institute under the National Health and Family Planning Commission released, through data collection and analysis of results,List of Hospitals with High Ratings in the Latest Electronic Medical Record Grading Evaluation。

Source: China Digital Medicine

By consolidating the old and new lists, we find that there are currently 24 hospitals at EMR Level 5, 12 at Level 6, and 2 at Level 7.

In late April 2017, the Statistical Information Center of the National Health and Family Planning Commission released the latest data on medical and health institutions nationwide. The data showed that there were currently 2,267 tertiary hospitals across China.If analyzed by the proportion of tertiary hospitals, only 1.6% of tertiary hospitals in China have achieved Level 5 or above in electronic medical records (EMR) maturity.

In addition, the pharmaceutical media outlet Sina Medicine recentlyAccording to the official website of the National Health and Family Planning Commission (NHFPC), as of October 23, the NHFPC had approved the preliminary design proposals and investment estimates for the information platform construction of 11 tertiary hospitals. The total investment in the informatization construction of these 11 hospitals amounted to RMB 196.49 million, including RMB 138 million from the central budgetary investment and RMB 62.29 million raised by the hospitals themselves.

As can be seen from the construction projects in the figure, the current focus of construction for Grade A tertiary hospitals is basically placed on information integration platforms and interoperability platforms.

In September, the National Health and Family Planning Commission approved the preliminary designs and investment estimates for big data-related projects at four hospitals—West China Hospital of Sichuan University, Fuwai Hospital of the Chinese Academy of Medical Sciences, Peking University People’s Hospital, and Children’s Hospital of Fudan University—with a total amount of RMB 67.71 million. Of this, RMB 42 million came from central budgetary investment, with the remaining funds raised independently by each hospital. Investment in information technology infrastructure at tertiary hospitals has significantly accelerated.

Based on the above information, it is evident that the level of basic big data application in China remains very low. In other words, even at the data collection stage, there is still a long way to go in the development of medical big data in China.

In terms of data storage, we take the Nanjing Jiangbei New Area Health and Medical Big Data Center as a case study.

Pilot Project for the Construction of the National Health and Medical Big Data Center and Industrial Park (Nanjing Campus) is located in the central area of Jiangbei New Area. It is planned to comprise four major functional zones under the framework of “One Center, Three Application Bases,” namely, the Health and Medical Big Data Storage Center, the International Health Service Community, Nanjing Bio-medicine Valley, and the Health Technology Industrial Park, with a total planned land area of approximately 17.3 square kilometers. The life health industry is one of the leading industries in Nanjing Jiangbei New Area.

[One Core] Establish a unified, authoritative, and interoperable population health information platform, and foster new business models in “Internet + Healthcare.”

[Three Application Bases] These are respectively positioned as comprehensive service application bases for healthcare big data in areas such as medical care, health preservation, elderly care, and training; application bases for biomedical research and development; and application bases for the research and development of advanced medical technologies.

Currently, the National Health and Medical Big Data Center project, which was established in Jiangbei New Area in October 2016, has completed the construction of its Phase I facilities and partial equipment procurement. The center’s globally most advanced high-throughput sequencers have been put into operation, positioning it to potentially become China’s largest human whole-genome sequencing center in the future.

As for the current state of data analysis, we will introduce it in the following section on the development of big data enterprises.

All Eyes on the Prize: China’s National Big Data Team Enters the Arena

On April 27, 2017, the National Health and Family Planning Commission took the lead in establishing the National Health and Medical Big Data Security Management Committee, which is responsible for organizing and supervising two major corporate groups—“China Health and Medical Big Data Industry Development Co., Ltd.” and “China Health and Medical Big Data Co., Ltd.”—to ensure that these groups fulfill their national mandates, implement national pilot projects, and promote the application and development of health and medical big data in China.

With the establishment of state-capital-led health and medical big data groups, the “1+5+X” health and medical big data framework is gradually taking shape, signaling an imminent explosive growth in the sector.

In accordance with the requirements of the State Council, the master plan entails constructing one national data center and five regional centers, while establishing several application and development centers tailored to local conditions. This constitutes the “1+5+X” master plan for the application and development of health and medical big data.

A national center will house the health and medical big data of all citizens, forming a health technology industrial ecosystem with the vision of “Holographic Digital Humans.” This ecosystem will encompass full-process, full-lifecycle data covering physiological, psychological, social, and environmental aspects related to every citizen’s production, daily life, and lifespan. The scale of data collection and application is expected to exceed 1,000 ZB.

Five regional centers will be constructed in accordance with the national master plan and geographical layout. According to Jin Xiaotao, Deputy Director of the National Health and Family Planning Commission, “We have already launched the first batch of national pilot programs in South China and East China, establishing two regional centers each in Fujian Province and Jiangsu Province. The remaining regional centers will soon enter the formal construction phase following field research, expert review, and national approval.”

An analysis of the locations of the 13 companies reveals that, with the exception of Beijing, all other companies are based in coastal cities ranging from Liaoning Province to Guangdong Province.

It is evident that, with the exception of Beijing, coastal cities remain the primary focus for the initial promotion of health and medical big data.

From the service categories of the 13 enterprises, it is evident that these companies span diverse sectors, including financial asset management, financial trading, integrated intelligent information services, urban comprehensive services, cloud computing and big data services, and healthcare informatization. This indicates that the newly established “national team” will possess multifaceted advantages in capital, urban services, underlying technologies, and application software.

Regarding this incident, analysts believe that two issues have long hindered the development of the medical big data industry: one is the integration challenge of data interoperability, and the other is the issue of data-sharing mechanisms. Leveraging state power in conjunction with industrial capital will effectively address the integration challenges of data interoperability.

As the "Administrative Measures for the Security of Health and Medical Big Data" is set to be introduced, it will address security and privacy protection issues in data application and establish a reasonable sharing mechanism. The three major groups are promoting the construction of the platform layer for medical data, opening up data sharing to various application domains via APIs, which will bring data dividends to the application layer of medical big data.

Areas that will benefit directly include:

1. AI + Healthcare Sector: Against the backdrop of increasingly mature algorithms, the bottleneck for artificial intelligence applications in healthcare lies in data, specifically regarding data standardization and volume. The development of platforms will provide abundant data resources for AI applications, thereby accelerating the rapid growth of China’s AI capabilities in medical image recognition, assisted diagnosis, clinical drug trials, health management, and other fields;

2. Healthcare Cost Containment: Rational actuarial pricing is a major pain point for both public health insurance and commercial insurance. Data integration facilitates pricing and cost control for public health insurance, while also fostering innovation in product offerings and mechanisms for commercial health insurance.

Accelerated Market Expansion: Breakthroughs in Both Business Depth and Breadth

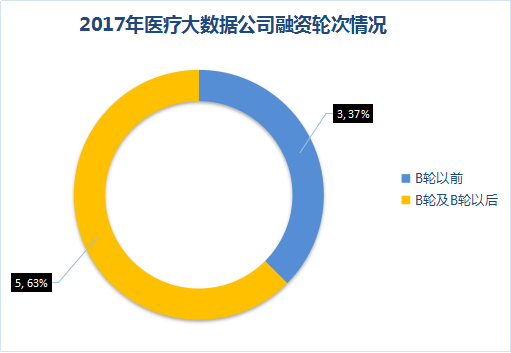

In 2017, the total financing amount for companies in the medical big data-related sectors reached approximately RMB 2.3116 billion. Although only a limited number of enterprises secured funding, the overall financing amounts were generally high.

From the perspective of financing rounds, companies at Series B and beyond account for the vast majority.

VCBeat’s analysis suggests that medical big data companies have gradually transitioned from an exploratory phase to a mature stage. Compared with the initial stage, the mature stage is primarily characterized by changes in the following three aspects:

1. The pace of market expansion is accelerating

Taking Yidu Cloud as an example, in April 2016, the company announced that it had partnered with more than 20 hospitals in China. By early 2017, Yidu Cloud had established collaborations with over 70 top-tier hospitals in China and launched the DPAP Alliance. According to Sun Zhe, CEO of Yidu Cloud, the alliance currently comprises more than 10,000 physicians, covers over 3,000 disease types, involves 110+ research projects, and maintains more than seven specialized disease databases.

2. Deepening Big Data Operations

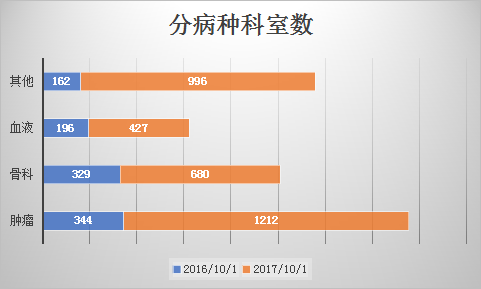

Taking Boshi Medical Cloud as an example, compared with the same period in 2016, the changes in the classification of major diseases focused on by Boshi Medical Cloud are as follows:

① The hematology and orthopedics departments experienced rapid growth, with year-on-year growth rates of 117.9% and 106.7%, respectively.

② The number of oncology-related departments has surged, with a growth rate far exceeding that of other specialty departments, reaching 252.3%.

③ The coverage rate of departments related to other diseases has also approached that of key diseases, with an overall growth rate of 514.8%.

④ The above figures represent the number of departments in Grade 3A hospitals in first- and second-tier cities that have established collaborations.

After consulting with the relevant person in charge at Boshi Medical Cloud, VCBeat also gained an understanding of their current development strategy and expectations:

① As two of the key therapeutic areas promoted since the inception of Boshi Medical Cloud, hematology and orthopedics have demonstrated accelerating growth, with departmental coverage in major priority regions exceeding 80%.

② As the most critical malignant disease, cancer impacts the lives of countless patients. With the annual incidence of cancer continuing to rise, a large number of new drugs and therapies are introduced each year. Oncology-related departments were also the key focus area for Boshi Medical Cloud’s development in 2017. Building on the solid coverage achieved in 2016, the total number of oncology-related departments covered nearly quadrupled in 2017.

③ As Boshi Medical Cloud’s brand recognition has grown and the number of collaborating departments has increased, departments specializing in non-core target conditions from the startup phase—such as neurology, rheumatology, transplantation, and psychiatry—have proactively reached out to express interest in the novel electronic medical record system, ultimately leading to collaborative partnerships.

3. Business scope is gradually expanding.

Taking LinkDoc Technology as an example, according to a relevant person in charge at LinkDoc, in 2016, the company primarily focused on research into healthcare big data, striving to unlock the intrinsic value of big data through data integration, management, analysis, sharing, and value presentation.

Leveraging its independently developed intelligent medical record entry system, LinkDoc has established the LinkDoc Real-World Oncology Database, covering more than 50 tumor types including lung cancer, gastric cancer, liver cancer, and breast cancer. The database encompasses all clinical modules, and through structured processing of large volumes of de-identified medical records, it transforms electronic health record information into research-grade data.

Meanwhile, by integrating patients’ clinical diagnosis and treatment data with out-of-hospital follow-up and rehabilitation data, as well as genomic data, a comprehensive, high-quality oncology database is established.

Building on a foundation of high-quality data, LinkDoc Technology began developing the Hubble AI-assisted decision-making platform in 2017. Leveraging vast amounts of real-world case data from cancer patients as training samples, and integrating multidimensional data such as medical knowledge graphs, drug utilization profiles, and patient clinical pathways, the platform employs technologies including deep learning, natural language processing, and neural networks. Specifically tailored for the oncology field, it constructs precise diagnostic and therapeutic models that provide treatment recommendations backed by underlying data support, thereby offering physicians a visualized, scenario-based, and intelligent systemic solution for diagnosis and treatment.

Currently, LinkDoc Technology is developing medical AI products with independent Chinese intellectual property rights across multiple fields, including intelligent imaging diagnosis, intelligent pathology diagnosis, and assisted diagnosis and treatment (encompassing assisted diagnosis, assisted therapy, and risk prediction).

An analysis of the product portfolios of mainstream healthcare big data companies, based on data acquisition, storage, and analytics, reveals that these firms are transitioning from data acquisition and storage to data analytics.

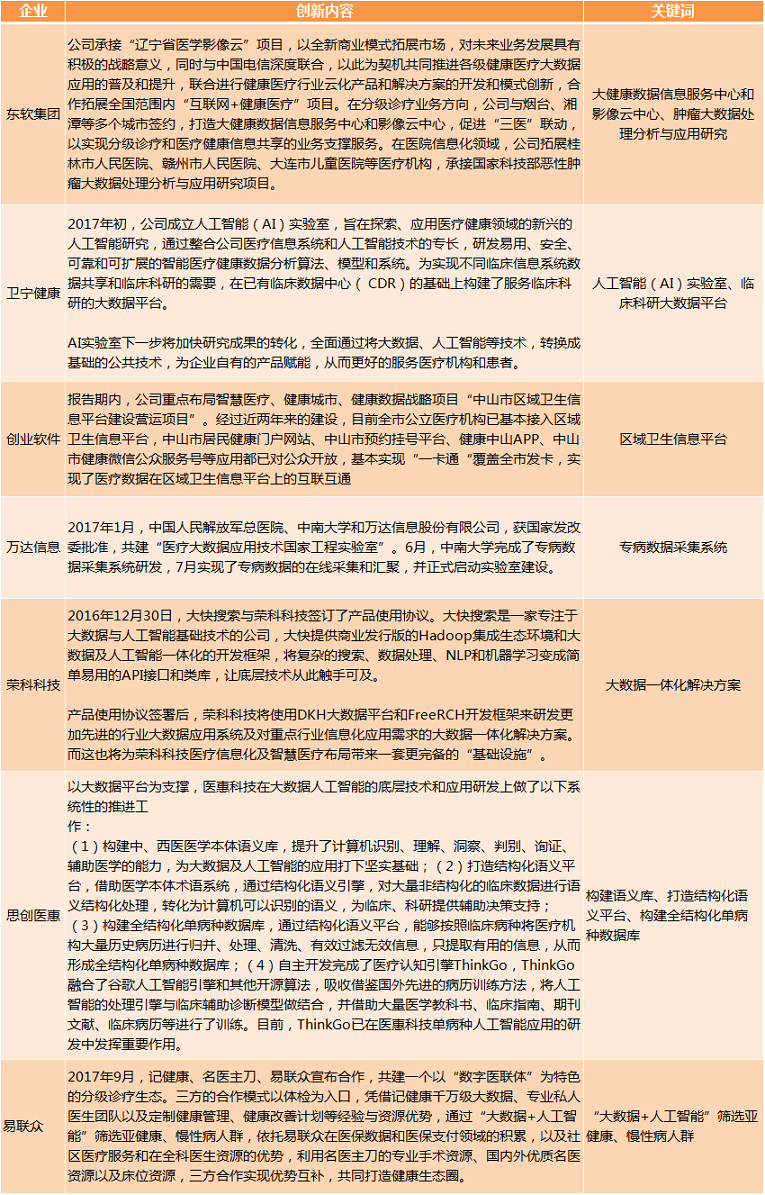

This point can also be concluded by combining the information in the 2017 semi-annual reports of listed companies in the medical informatization industry:

Previously, we had in "Healthcare Informatics: Market Growth Stagnated in 2017—How Should Companies Identify New Growth Engines?》As analyzed in this article, by 2017, most domestically listed healthcare IT companies had begun to lay out their AI strategies. In this report, we have extracted the innovative aspects related to medical big data. As shown in the figure above, in addition to venturing into artificial intelligence, these listed companies are also accelerating their efforts in a series of data analytics-related businesses, including medical big data collection, analysis, and scientific research.

Based on the above information, VCBeat judges that, with the continuous investment by domestic medical big data enterprises and listed medical informatics companies, coupled with the participation of artificial intelligence enterprises,Hospital Data Market Is About to Enter a New RoundFeeding Frenzy Phase.