Pharmaceutical Industry in 2017: Landmark Policies Implemented, Strong Growth and Value-Driven Investment & M&A Activities — Year-End Review

The pharmaceutical industry, as the most fundamental and core component of the healthcare sector, underwent multiple transformations in 2017.

Policy Level: Continued strengthening of incentives for pharmaceutical innovation, with multiple supportive policies implemented; in-depth advancement of consistency evaluations, expansion of clinical trial institutions, and release of reference listed drugs, driving Chinese generic drugs to move beyond "me-too" toward "me-better"; formal implementation of the "Two-Invoice System," bringing about drastic changes in pharmaceutical distribution; comprehensive elimination of the practice of subsidizing healthcare through drug sales, with zero-markup policies and pilot programs for prescription outflow launched in multiple regions.

Industry Level: The pharmaceutical manufacturing, distribution, and retail sectors have seen steady growth, with the market share gradually expanding. Financial data from listed companies has improved, showing increases in both revenue and net profit. There is a surge in enthusiasm for IPOs among pharmaceutical companies, with the number of initial public offerings far exceeding previous levels. Continuous industry mergers and acquisitions, including organic growth, external expansion, regional integration, and overseas M&A, are driving the industry towards greater scale and concentration.

VCBeat (WeChat ID: vcbeat) plans to review the development of the pharmaceutical industry in 2017 from the perspectives of policy, industry, and capital, and to look ahead to 2018.

Policy: Standardization of the Entire Process from R&D to Distribution

Reviewing this year’s pharmaceutical regulatory policies, “standardization” emerges as the most critical keyword. Drug innovation and detailed rules for consistency evaluation have been promulgated; the “Two-Invoice System” coupled with distribution rectification has driven the pharmaceutical distribution sector toward greater standardization; public hospital pharmaceutical reforms have deepened, ushering in transformative changes in pharmaceutical retail.

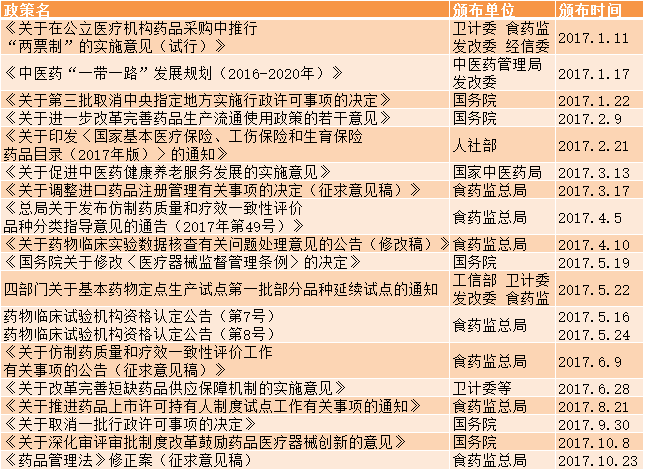

Summary of Key Pharmaceutical Policies in 2017

We will gradually analyze pharmaceutical policies by following the trajectory of the pharmaceutical industry chain, starting with pharmaceutical supply. This involves a step-by-step breakdown of areas such as pharmaceutical innovation, the quality and efficacy consistency evaluation of generic drugs, imported drug registration, Good Manufacturing Practice (GMP) for drugs, and drug registration.

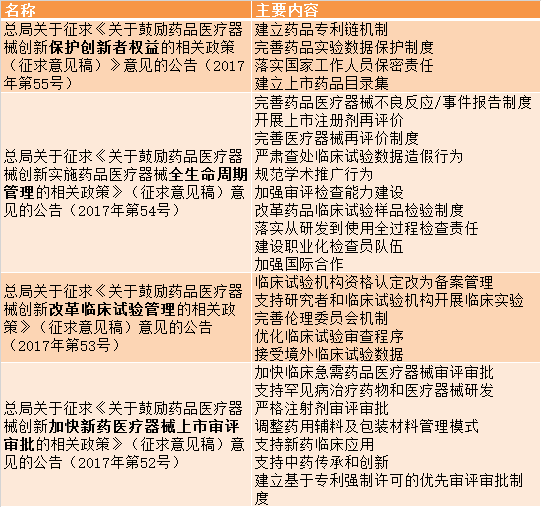

Let’s first look at pharmaceutical innovation. In May, the China Food and Drug Administration (CFDA) successively issued four policy documents aimed at encouraging innovation in drugs and medical devices. On October 8, the General Office of the Communist Party of China Central Committee and the General Office of the State Council jointly released the “Opinions on Deepening the Reform of the Review and Approval System to Encourage Innovation in Drugs and Medical Devices,” hailed as a “milestone” reform for the industry’s innovative development.

Policies encouraging innovation in pharmaceuticals and medical devices have had a profound impact on the industry by promoting innovation and guiding the establishment of a complete R&D-to-market pathway, covering areas such as new drug development, clinical trials, equity rights of owners, and marketing approval.

In fact, encouraging new drug research and development has always been the main theme of the industry. Looking back to August 2015, when the State Council issued Document No. 44, it clearly defined 12 tasks for the reform of drug and medical device review and approval processes. These included addressing registration backlogs, promoting consistency evaluations, piloting the Marketing Authorization Holder (MAH) system, and accelerating approvals for clinically urgent drugs, thereby essentially establishing the overarching tone of encouraging innovation.

Key highlights of the series of policies released by the China Food and Drug Administration (CFDA) in May include: establishing a drug patent linkage mechanism, improving the system for protecting experimental drug data, strictly regulating clinical data falsification, strengthening review processes, transitioning clinical trial institutions to a filing-based registration system, and supporting the clinical application of new drugs.

CFDA’s Series of Policies to Encourage Innovation in Drugs and Medical Devices

The “Opinions on Deepening the Reform of the Review and Approval System to Encourage Innovation in Drugs and Medical Devices,” issued on October 8, covers six major areas, including: 1) reforming clinical trial management to ensure that clinical trials are scientific, standardized, and authentic; 2) accelerating the review and approval of drugs and medical devices urgently needed for clinical use to address public medication needs; 3) encouraging innovation to promote the healthy development of China’s pharmaceutical industry; 4) fully implementing the Marketing Authorization Holder (MAH) system to strengthen lifecycle management of drugs and medical devices; 5) enhancing technical support capabilities to fully serve innovation; and 6) strengthening organizational leadership to ensure the effective implementation of reforms through rule-of-law thinking and approaches.

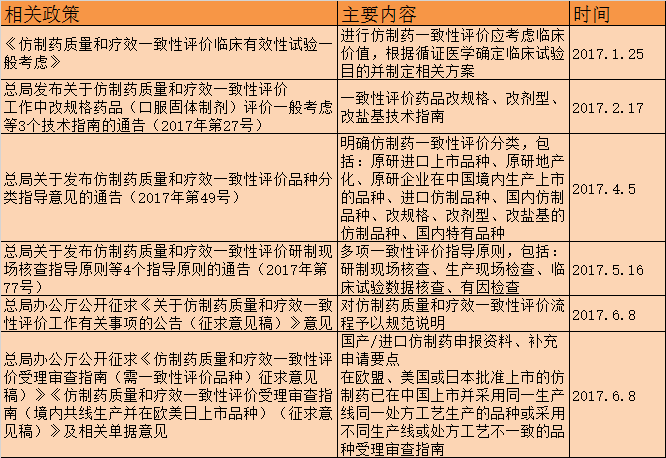

In addition to innovative drugs, detailed policies were also introduced this year for generic drugs, which currently hold the largest market share. These include guidelines for waiving human bioequivalence studies, technical guidelines for evaluating strength-changed drugs (oral solid dosage forms), and guidelines for on-site inspections, as well as measures for the determination of reference listed drugs and the expansion of clinical trial institutions. These policies have bolstered companies’ confidence in advancing consistency evaluations, enhancing the certainty and operability of policy implementation.

Policies on Generic Drugs Released in 2017

Innovation, along with stricter and clearer quality evaluations for generic drugs, aims to adjust the structure of drug supply and gradually align with international standards. In March, the China Food and Drug Administration (CFDA) issued new regulations on the registration of imported drugs, encouraging overseas unlisted new drugs to conduct clinical trials simultaneously inside and outside China after approval, thereby shortening the time gap between domestic and foreign market launches and meeting public clinical demand for new drugs; in June, China officially joined the ICH.

On October 23, the China Food and Drug Administration (CFDA) released the draft amendments to the Drug Administration Law, stipulating that the Marketing Authorization Holder (MAH) shall bear full responsibility for the safety, efficacy, and quality of drugs. Meanwhile, the certification requirements for Good Manufacturing Practice (GMP) and Good Supply Practice (GSP) were abolished. Following the elimination of these dual certifications, pharmaceutical production and distribution will be subject to more routine regulatory oversight and standardization.

The “Two-Invoice System” (trial) was promulgated at the beginning of this year, requiring that “the Two-Invoice System be gradually implemented in drug procurement by public hospitals.” Subsequently, detailed implementation rules were rolled out across various regions. On October 16, the Tibet Autonomous Region officially released its implementation measures for the Two-Invoice System, marking the point at which all provincial-level administrative divisions in China had issued their respective detailed rules. The national-level official document for the Two-Invoice System is currently being drafted and is scheduled to be released by the end of 2017.

Another aspect involves the components of comprehensive public hospital reform related to drug use, such as the separation of pharmaceuticals from medical services, the outflow of prescriptions, and pharmaceutical care service fees. This year’s “healthcare reform” tasks require that comprehensive public hospital reform be fully rolled out by the end of September, with all public hospitals abolishing drug markups (except for traditional Chinese medicine decoction pieces). In terms of specific implementation pathways, there are both the Beijing model, which adjusts the pricing structure of pharmaceuticals and medical services, and the Guangdong model, which links drug and health insurance fund management with comprehensive reforms in pharmaceutical distribution.

In addition to the policies mentioned above, other measures—such as drug approval reforms, adjustments to the national reimbursement drug list, policies on traditional Chinese medicine, supply guarantees for shortage drugs, and the cancellation of qualification certification for online pharmaceutical e-commerce—have also exerted varying degrees of impact on the industry.

Overall, the pharmaceutical industry is heavily regulated, and the introduction of new policies will significantly influence market trends. Fortunately, the strong continuity in pharmaceutical regulation provides practitioners with ample room for transition.

Industry: Strong Growth, Booming IPOs

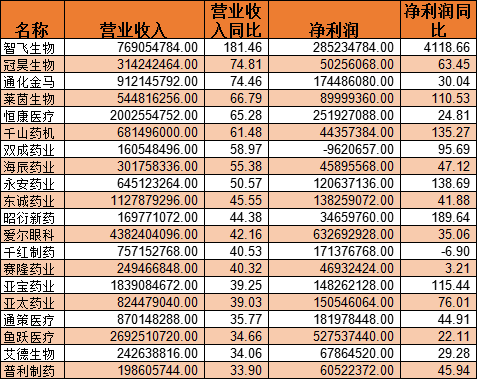

According to Choice data, as of October 25, 71 listed pharmaceutical and biotechnology companies had disclosed their financial reports for the first three quarters of this year. Among them, 62 companies reported positive growth in performance, accounting for nearly 90% of the total number of companies.

Top 20 Companies by Revenue Growth in the Pharmaceutical and Biotechnology Industry

(Data source: Choice, as of October 25)

From a sectoral perspective, concept stocks in biological drugs, medical services, medical devices, and innovative drugs have shown relatively rapid growth. This is primarily driven by the heating up of the biological drug market, increased interest in privately run healthcare institutions, and accelerated approval processes for innovative drugs. In terms of specific performance, companies such as Zhifei Biological Products, Guanhao Biotech, and Layin Bio-technology have experienced rapid revenue growth. Zhifei Biological Products saw a year-on-year revenue increase of 181%, while Guanhao Biotech, Layin Bio-technology, Hengkang Medical, and Qianshan Pharmaceutical Machinery all recorded revenue growth exceeding 60%.

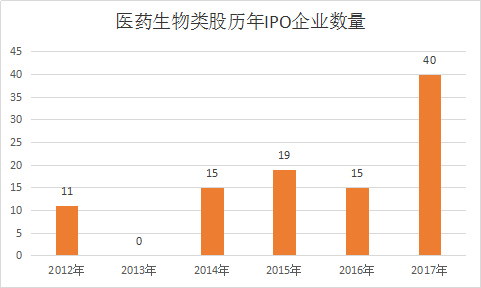

As of October 20, 40 new stocks in the pharmaceutical and biological sector successfully completed their IPOs, setting a record high for any year.

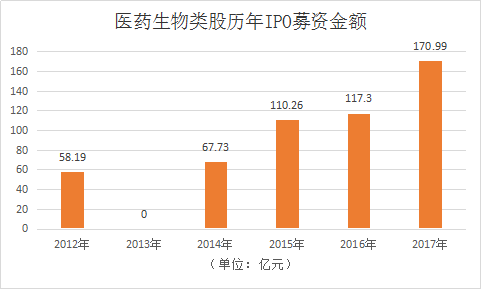

In terms of initial offering proceeds, newly listed pharmaceutical and biotech stocks have raised a total of over RMB 17 billion this year, reaching the highest level on record.

From the perspective of individual stocks, BGI Genomics, Kangtai Biological Products, Dashenlin Pharmaceutical Group, KingMed Diagnostics, and Double Medical Technology have all achieved post-IPO market capitalizations exceeding RMB 10 billion. BGI Genomics broke into the top ten pharmaceutical and biotechnology stocks by market capitalization with a value of RMB 64.428 billion, while Dashenlin Pharmaceutical Group became the “leading stock in pharmaceutical retail” with a market capitalization surpassing RMB 17 billion.

From the market’s response, capital has shown strong recognition of newly listed biopharmaceutical stocks. BGI Genomics and Kangtai Biological Products saw their market capitalizations increase more than tenfold after going public; AmoyDx, Poly Pharma, and KingMed Diagnostics also posted solid growth.

Market Capitalization Growth of 2017 IPOs in the Pharmaceutical and Biotechnology Sector

The growth of newly listed and recently listed stocks in the pharmaceutical and biotechnology sectors is primarily driven by concepts such as genomics, biopharmaceuticals, innovative drugs, and healthcare services.

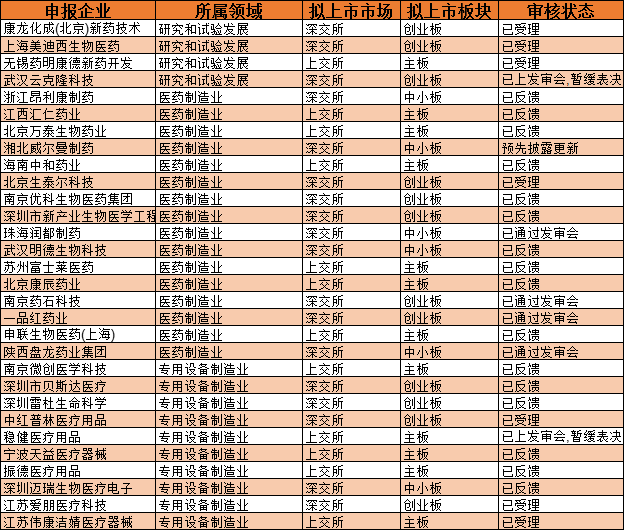

According to data from the China Securities Regulatory Commission (CSRC), as of October 19, there were still 30 pharmaceutical and biotechnology companies waiting in line for initial public offerings (IPOs). These include companies with significant future market potential, such as WuXi AppTec, Panlong Pharmaceutical, Winner Medical, and Mindray Bio-Medical.

IPO Queue Status of Pharmaceutical and Biotechnology Companies

Capital: M&A Cools Down, Financing Grows Rapidly

In 2017, capital remained highly active in the pharmaceutical and biotechnology sector, with annual M&A financing exceeding RMB 100 billion. After experiencing the “capital winter” and “de-bubbling” in venture capital, industrial investment has become more rational, returning to value-driven principles.

According to Choice data, as of October 25, there were 223 M&A transactions involving listed companies in the pharmaceutical and biotechnology sector, with a total transaction value of approximately RMB 49 billion.

This figure represents a significant decline compared with previous years. Historical data show that in 2016, the pharmaceutical industry completed 428 mergers and acquisitions (M&A) transactions, with a total value exceeding RMB 180 billion. It should be noted that these figures encompass both listed and unlisted entities as acquirers or targets, and include overseas M&A activities by Chinese companies; therefore, they differ somewhat from M&A data specifically for listed pharmaceutical and biotechnology companies. Nevertheless, they do provide some support for the assessment that M&A activity in the industry is cooling down.

The decline in M&A activity within the pharmaceutical industry is attributed to the fact that intensive M&A efforts in previous years have already identified high-quality targets, thereby reducing available opportunities. Additionally, the resumption of IPOs and the recovery of IPO activity in the pharmaceutical sector have also exerted a certain impact on industry M&A.

From the perspective of transaction purposes, industry consolidation and diversification strategies are the primary drivers behind listed companies’ enthusiasm for acquisitions. Additionally, asset restructuring, business transformation, and financial investments also account for a certain proportion.

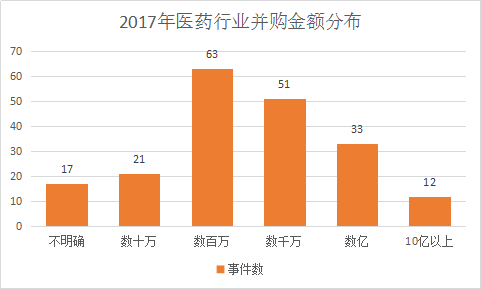

From the perspective of value distribution, the majority of M&A transactions were concentrated below RMB 100 million. There were 33 deals in the RMB 100 million to RMB 1 billion range, and only 12 deals exceeded RMB 1 billion.

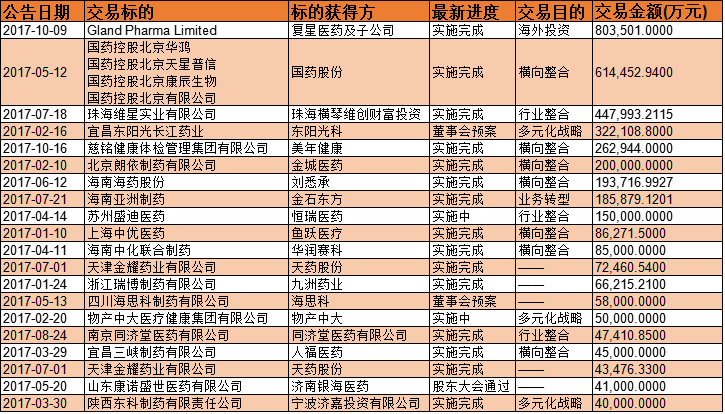

In terms of transaction targets, Gland Pharma, Sinopharm-controlled subsidiaries, Zhuhai Weixing Industrial, and Yichang HEC Changjiang Pharmaceutical were among the largest acquisition targets this year.

Top 10 Mergers and Acquisitions in the Pharmaceutical and Biotechnology Industry in 2017

In early October, Fosun Pharma announced that it had completed the acquisition of a 74% stake in Indian pharmaceutical company Gland Pharma, with the relevant shares transferred on October 3. The bidding process for Gland Pharma lasted nearly a year and cost approximately RMB 8 billion, making it the largest acquisition completed by a listed company in the pharmaceutical and biotechnology sector this year.

The equity transfers among four subsidiaries announced by Sinopharm Group Co., Ltd. and Sinopharm Holding Co., Ltd. on May 12 have become the second-largest M&A deal, involving Sinopharm Holding Beijing Huahong, Beijing Tianxing Puxin, Kangchen Biologics, and Sinopharm Holding Beijing, with a total transaction value of RMB 6.144 billion. Both Sinopharm Group Co., Ltd. and Sinopharm Holding Co., Ltd. are subsidiaries controlled by China National Pharmaceutical Group Corporation (Sinopharm), making this acquisition an internal consolidation within the group.

Other major transactions, such as HEC Pharm’s acquisition of Yichang HEC Changjiang Pharmaceutical, Meinian Onehealth’s acquisition of Ciming Health Checkup Management Group, and Jincheng Pharmaceutical’s acquisition of Beijing Langyi Pharmaceutical, also involved substantial amounts, driven largely by considerations of industry consolidation and diversification strategies.

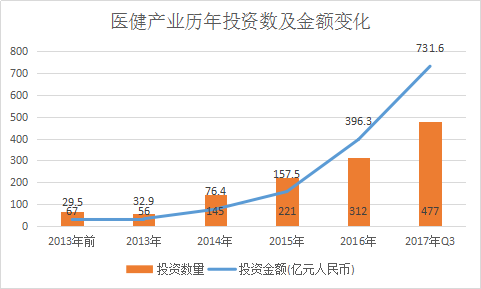

According to statistics from VCBeat, as of Q3 this year, China's healthcare industry completed 477 financing rounds, involving a total amount of $11.06 billion. This figure represents a significant increase compared to the same period last year, which saw 293 financing rounds totaling approximately $36 billion.

Data Source: VCBeat, VBInsight

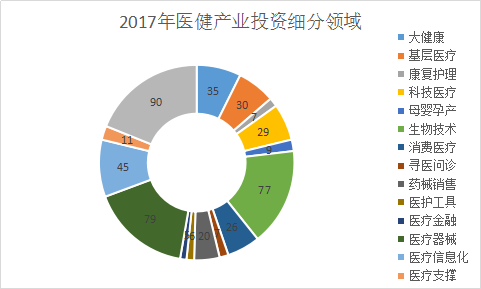

From a sectoral perspective, hotspots include general health, primary care, digital health, biotechnology, medical devices, healthcare IT, and pharmaceuticals, while investment in areas such as online medical consultation, maternal and child health, and rehabilitation nursing remains relatively limited.

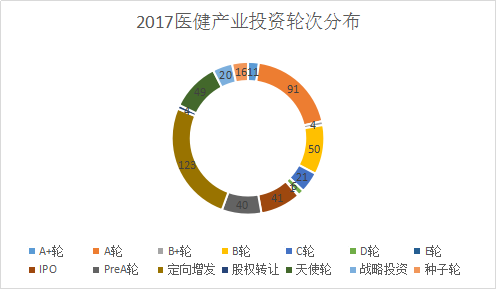

From the perspective of investment rounds, private placements by listed companies and Series A and later-stage projects accounted for the majority, collectively representing over 90% of the total number of investments. There were seven cases at Series D and beyond, including Haodf Online, Gushengtang, Lama Bang, and Arrail Dental. In the pharmaceutical and biotechnology sector, Songli Biotech and Changfeng Pharma secured Series D funding, while Paige Biopharma obtained Series E financing.

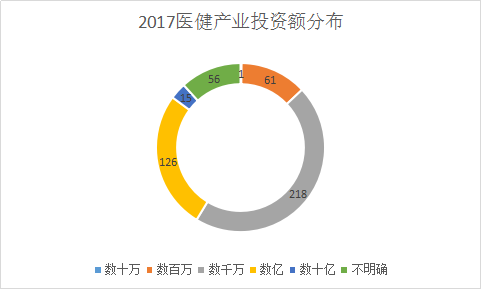

In terms of funding amount distribution, deals ranging from millions to tens of millions of RMB dominate the landscape, with a total of 279 cases accounting for nearly 60% of all investments. There were 126 deals at the hundred-million-RMB level, representing approximately one-quarter of the total number of investments. While billion-RMB-level deals are fewer in number, they involve substantial capital; the top 20 largest deals totaled $5.383 billion, accounting for roughly half of the total investment amount. This indicates that investment in the healthcare industry favors large-scale, late-stage targets, with more mature companies being more favored by capital.

The aforementioned investment data pertains to the entire healthcare industry. In the pharmaceutical and biotechnology sector, there were a total of 93 investment deals, including 14 deals at Series A or earlier stages, 20 deals at Series B or later stages, and a significant number of IPOs and private placements, totaling 54 deals, which accounted for more than half of the total investments.

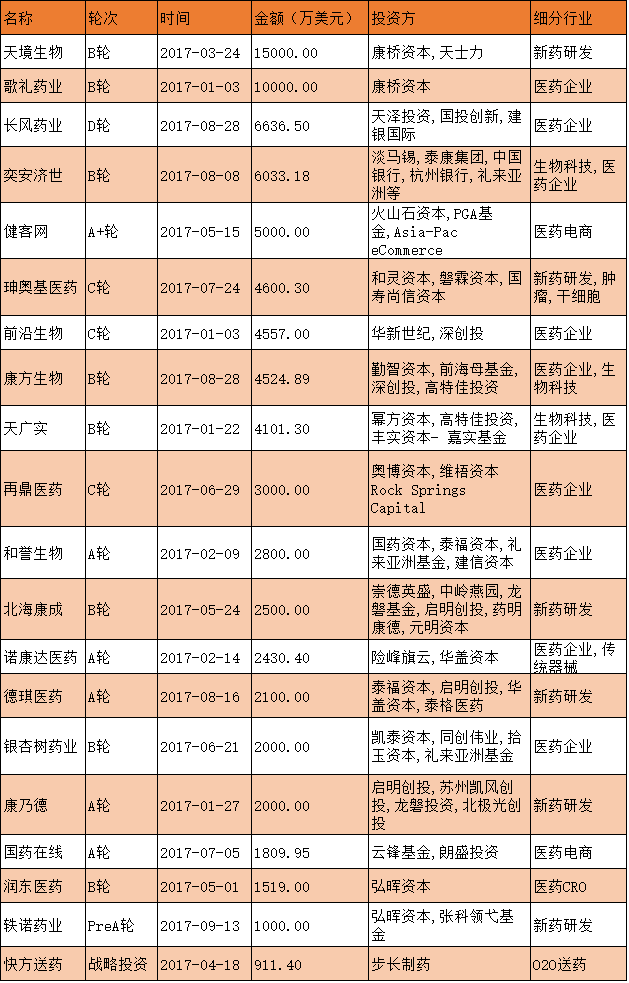

The top 20 companies in the pharmaceutical and biotechnology sector by financing amount include I-Mab Biopharma, Ascletis Pharma, Eternity Healthcare, Jianke.com, and RUIAOJI Pharmaceuticals. In terms of capital activity, investors such as Qianbao Capital, Tasly, Temasek, Shenzhen Capital Group, GTJA Innovation Investment, and Qiming Venture Partners demonstrated high levels of activity, with multiple investments throughout the year.

Top 20 Investment Deals in the Pharmaceutical and Biotechnology Industry in 2017

Overall, the healthcare industry’s capital landscape this year is characterized by cooling M&A activity alongside warming financing trends. This situation stems from multiple factors: first, capital has become more rational in industrial M&A, with many investment firms choosing to hold back; second, the pool of high-quality M&A targets has shrunk, as these companies have secured capital through IPOs, strategic investments, and partnerships with listed companies.

Financing and investment continued to maintain a high-growth trajectory, reaching record highs. This is because the entire healthcare industry is undergoing rapid transformation, with emerging opportunities in new drugs, genomics, medical services, and Internet-plus-healthcare driving a surge in startups and fueling robust investment activity.

Specifically within the pharmaceutical and biotechnology industry, trends share commonalities with, yet also differ from, those of the broader healthcare sector. The commonality lies in the consistent direction of innovation and investment and financing trends. The differences are characterized by larger scales and more concentrated targets, which are closely related to the high-investment, long-cycle nature of pharmaceutical innovation. This trend is expected to persist in the future.

2017 was a year of rapid transformation in the pharmaceutical industry. The above analysis has examined industry dynamics from the perspectives of policy, industry, and capital, with the hope of providing valuable insights for investors and innovators. VCBeat will continue to closely monitor innovation and change in the healthcare and pharmaceutical sectors, growing alongside innovators.

If you are interested in “pharmaceutical distribution,” you are welcome to register for the event to be held in Beijing from December 15–17.“2017 Top 100 Future Healthcare” Forum, we will establish a dedicated“Parallel Forum on Pharmaceutical Distribution”, inviting renowned industry experts and numerous corporate executives to explore how policies, new technologies, and e-commerce are impacting the pharmaceutical distribution sector. Long-press the image below to scan the QR code and register.