Private Healthcare in China: 27 Listed Companies Engaged in Nearly 50 Hospital Projects with a Single Investment Peaking at RMB 1 Billion – Brand Building Emerges as a Strategic Priority (2017 Year-End Review)

Private HealthcarePrivate healthcare refers to medical institutions other than those owned by the state or collectives, including hospitals, clinics, and health centers, and constitutes an important component of the healthcare system. Encouraging private investment in healthcare to provide multi-tiered and diversified medical services, in parallel with the comprehensive reform of public hospitals, is a key task of China’s healthcare reform.

2017 marked a significant milestone in the development of private healthcare, as detailed rules encouraging social capital to establish medical institutions were implemented, qualifications for opening clinics were relaxed, multi-site practice for physicians was liberalized, and capital inflows surged, ushering in a year of breakthroughs and growth for the private healthcare sector.

VCBeat (WeChat ID: vcbeat) plans to review the development of private healthcare in 2017 from three perspectives—policy, industry, and operations—and engage in in-depth discussions with industry experts to interpret key terms shaping the sector’s growth, while outlining future trends and developmental pathways for private healthcare.

Policy: Sending a Positive Signal to Encourage the Development of Private Healthcare

Before analyzing the 2017 policy, let us briefly review the development of private healthcare in China. Currently, private medical institutions account for half of the total number of healthcare providers in China; however, they still lag behind public medical institutions in terms of patient visit volume, social status, and brand building.

According to data from the National Health and Family Planning Commission, as of the beginning of this year,There are 444,000 privately operated medical institutions in China, accounting for 45% of the total number of medical institutions; there are 16,900 private hospitals, accounting for 57.2% of the total number of hospitals.Since 2011, the number of privately run hospitals has doubled; however, a significant gap remains between the two sectors in terms of patient visits, with a ratio of approximately 9:1, i.e.,Approximately 90% of patients choose to seek medical care at public hospitals rather than private ones.

In recent years, policies related to private healthcare have focused on several key areas: first,Relax Market Access, encouraging social capital to invest in the health services industry; secondly,Preferential policies have been provided in terms of layout planning, fiscal and tax policies, medical equipment, and human resources.; Third,Strengthened ties between private healthcare, public healthcare, and health insurance have fostered synergy between reform and innovation.

In 2017, policies related to private healthcare largely continued to focus on the key areas mentioned above.

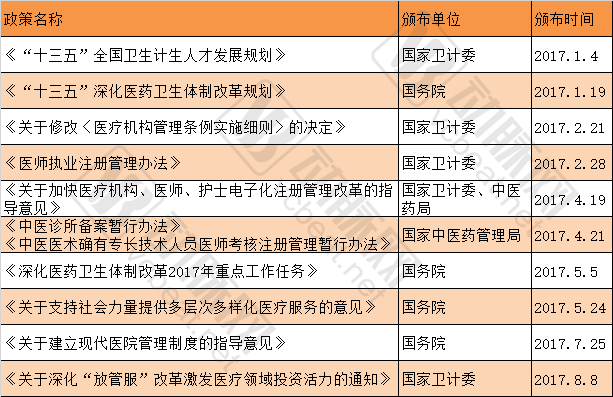

Table 1: Policies for the Private Healthcare Industry in 2017

In January 2017, the National Health and Family Planning Commission released the “13th Five-Year” National Plan for the Development of Human Resources in Health and Family Planning, proposing support for privately run medical institutions and further optimization of the policy environment.All medical institutions shall be treated equally in terms of key specialty development, professional title evaluation, and academic standing.Facilitated the flow of medical talent to private healthcare institutions.

In February 2017, the National Health and Family Planning Commission issued the “Decision on Amending the Detailed Rules for the Implementation of the Regulations on the Administration of Medical Institutions,”Added basic standards and management specifications for categories of medical institutions, including medical laboratory testing centers, pathological diagnosis centers, medical imaging diagnosis centers, hemodialysis centers, and hospice care centers., broadening the channels for social forces to participate in healthcare provision.

In the same month, the National Health and Family Planning Commission issued the “Administrative Measures for Physician Practice Registration,” establishing a system of regional physician registration, electronic registration, and public disclosure and inquiry of registration information.Improve the administration of physician practice registration to facilitate the steady, orderly flow and scientific allocation of high-quality medical resources., alleviating the talent shortage hindering the development of private healthcare.

In April 2017, the National Administration of Traditional Chinese Medicine released two documents for public comment—the Interim Measures for the Filing and Registration of TCM Clinics and the Interim Measures for the Examination, Registration, and Administration of Physicians with Demonstrated Expertise in Traditional Chinese Medical Techniques—providing specific details on the transition of TCM clinic establishment from an approval-based system to a filing-based system.TCM Clinics Can Be Established Upon Filing。

In May 2017, the General Office of the State Council issued the “Opinions on Supporting Social Forces in Providing Multi-level and Diversified Medical Services,” proposing to strive for a significant enhancement in the capacity of social forces to operate medical institutions by 2020, with marked improvements in medical technology, service quality, and brand reputation.Cultivate a large cohort of private medical institutions with strong service competitiveness, the supply of services basically meets domestic demand.

In August 2017, the National Health and Family Planning Commission issued the “Notice on Deepening the Reform of ‘Delegating Power, Improving Regulation, and Upgrading Services’ to Stimulate Investment Vitality in the Medical Sector,” proposing ten specific key reforms. These include: abolishing the approval requirement for clinics established within elderly care institutions;Integration of the Two Certificates: Approval for Establishment and Practice Registration for Medical Institutions at Level II and Below; for clinics established by foreign medical institutions, companies, enterprises, and other economic organizations in the form of joint ventures or cooperation,Relaxing the restriction that foreign equity participation shall not exceed 70%, etc.。

The aforementioned policies have streamlined administration and delegated power while strengthening guidance across multiple dimensions—including market entry thresholds, talent development, scope of medical practice, approval processes, fiscal and taxation policies, and regulatory oversight. These measures have created a favorable policy environment for social capital to enter the healthcare sector, invigorated privately run medical institutions, and diversified both investment entities and investment models.

High Capital Enthusiasm: M&A, Investment, and Greenfield Projects as Primary Entry Modes

Under favorable policy guidance, social capital’s enthusiasm for participating in the healthcare sector has reached an unprecedented high. According to incomplete statistics from VCBeat,As of the end of October this year, 27 listed companies have participated in the construction of nearly 50 hospital projects., covering areas such as general hospitals, specialized hospitals, rehabilitation centers, and the renovation of public hospitals, with primary modes of participation including acquisitions, investments, and new construction.

Table 2: Overview of Listed Companies’ Participation in Hospital Projects

Below, we select several key cases to analyze the sectors and methods through which social capital engages in healthcare.

Changbao Shares(002478, SZ) released an announcement on January 26 this year regarding the issuance of shares to purchase assets and raise matching funds, which constitutes a related-party transaction. The company plans to acquire 100% equity interest in Shifang Second People's Hospital, 90% equity interest in Yanghe People's Hospital, and 100% equity interest in Ruigao Investment (which holds a 71.23% equity interest in Shanxian Dongda Hospital). The respective valuations for these three transactions are RMB 228 million, RMB 351 million, and RMB 413 million, with a combined total valuation of nearly RMB 1 billion.

With a one-time investment of nearly RMB 1 billion to acquire three hospitals, Changbao Shares’ enthusiasm for healthcare investment is evident.

Changbao Shares is primarily engaged in the research and development, production, and sales of specialized steel pipes, including pipes for natural gas, boiler tubes, and mechanical tubing, making it a quintessential manufacturing company. In 2016, its revenue amounted to RMB 2.205 billion, with a net profit attributable to shareholders of the listed company of RMB 110 million.

Affected by the industry downturn, falling international oil prices, and fluctuations in raw material prices,Changbao Shares' performance has declined significantly in recent years.Its 2016 revenue was nearly halved compared to the RMB 3.988 billion recorded in 2013; it was under these circumstances that Changbao SharesPursuing Diversified Exploration and Strengthening Efforts in the Big Health Industry.

In terms of the transaction targets, Shifang Second People's Hospital is a Grade II Class A general hospital, with revenue of RMB 60.1867 million from January to August 2016; Yanghe People's Hospital is currently the only large-scale general hospital in the Yanghe area, with revenue of RMB 55.2324 million from January to August 2016; Shanxian Dongda Hospital is located in the Shanxian Economic Development Zone at the junction of Jiangsu, Shandong, Henan, and Anhui provinces, with revenue of RMB 148 million from January to August 2016. The combined revenue of the three hospitals amounted to approximately RMB 260 million.

Acquiring three companies with a combined annual turnover of nearly RMB 300 million for RMB 1 billion appears to be a favorable deal under any assessment. A securities representative of Changbao Shares stated in an interview, “The big health industry is a sunrise sector. Should the broader macroeconomic environment change in the future, we do not rule out further expansion into the big health industry.”

Similar to Changbao Shares,Yihua Health(000150, SZ) is also one of the companies actively transforming into the broader health industry. Formerly known as Yihua Real Estate, it was the first listed real estate company in eastern Guangdong Province. It completed its name change in 2015 to pivot towards healthcare and medical services, successively acquiring Zhongan Kang and taking a stake in Youde Yi. Through a series of successful capital operations and industrial layout adjustments in recent years,Yihua Health has established two core businesses: medical services and elderly care services., with a strategic focus on private general hospitals and mid-to-high-end elderly care communities.

Yihua Health completed six acquisitions or took controlling stakes in medical institutions this year., with targets including Jiangyin Baiyi Traditional Chinese Medicine Hospital, Kunshan Changhai Hospital, Yugan Renhe Hospital, Hangzhou Yanghe Hospital, Hangzhou Ci'ai Elderly Care Hospital, and Hangzhou Xiacheng Cihui Elderly Nursing Home.

Yihua Health stated in its semi-annual report that it will continue to accelerate the acquisition of high-quality medical institutions and constantly improve the construction of its medical institution service platform; steadily advance investment and operational activities in elderly care communities to create a chain-based, membership-model elderly care system; and accelerate the promotion of informatization while exploring the establishment of an information technology platform.

There are more examples in terms of investment, including collaborating with public medical institutions to establish new hospitals and investing in hospital management companies, etc. For instance,Guangzhou Improve Medical Instruments Co., Ltd. signed a PPP agreement with the Yizhang County People’s Government to jointly build the Yizhang County Hospital of Traditional Chinese Medicine; Zhongnan Construction participated in the PPP project for the Geriatric Care Center of Jining City Integrated Traditional Chinese and Western Medicine Hospital.

Another model isPublic Hospitals under Trusteeship, NEEQ-listed companyLuoman New MaterialsIn January of this year, with Wuhai Tonghe Hospital, Aksu City Tonghe Hospital, Aksu City Maria Gynecological Hospital, Ulanhot Jiuzhou Urology Specialist Hospital, Red Cross Tonghe General Outpatient Department, Bayannur Red Cross Tonghe Hospital, and Yan'an Union HospitalSeven hospitals signed trusteeship agreements.

Listed companies that have built new hospitals include Topchoice Medical, Chuangxin Medical, and Guangshengtang.On September 1, Guangshengtang announced the establishment of its wholly-owned subsidiary, Fuzhou United Family Guangsheng Women’s and Children’s Hospital Co., Ltd. Notably, this marks the first collaboration between United Family Healthcare, a well-known foreign-invested medical services brand, and a Chinese listed company, with United Family providing its brand and management expertise while domestic operations are handled by the local partner.

In addition to hospital targets,Clinics Are Also a Hotspot for Capital Investment, specializing in the chain clinic businessDistinct HealthCare and Johnson Medical also secured substantial financing this year; behind the clinics founded by internet-famous physicians such as Yu Ying and Ou Qian, venture capital firms are actively present.

We anticipate that, under the continued support of favorable policies, capital enthusiasm for private healthcare will remain robust, with investment entities and participation models becoming increasingly diversified.

Operations: Brand Building Is the Key Word for the Development of Private Healthcare

We interviewed Guo Jun, former Vice President of a top-tier hospital and Executive Director and CEO of Wuhan Deli Wuhe Medical Technology Co., Ltd., as well as Li Zhiyong, head of Dongguan Fengtian Medical Investment Co., Ltd. Both provided practical insights into the key factors driving the development of private healthcare.

Guo Jun believes that, judging from the development trajectory of private healthcare, expectations for the sector have been steadily rising, both in terms of policy support and market dynamics. With evolving medical demands and shifting public health awareness, private healthcare providers must now break free from the constraints of their traditional operational strategies, take more decisive actions to address declining performance, and clearly define their positioning within the healthcare industry.“Brand Building” should be the keyword for the development of private healthcare in 2017.

Li Zhiyong stated,“Openness” was the keyword for the development of private healthcare in 2017.He stated that in 2017, the State Council consecutively issued multiple implementation guidelines for healthcare reform. As an important component of national healthcare reform, private medical practice has received significant policy support this year, such as the removal of planning restrictions and independent approval for specialty classifications. Although true parity with public institutions has not yet been fully achieved, this represents the most substantial opening-up in recent years. Meanwhile, to promote the mobility of medical talent, the state has vigorously encouraged physicians to practice at multiple sites. The emergence of physician groups marks a gradual break from the previous monopoly of public hospitals over medical talent. Medical professionals are being liberated and released into the broader society, thereby positively fostering the development of private healthcare.

From the perspective of the strengths and weaknesses of private healthcare development, key areas of focus include talent, management, positioning, brand, and public credibility.

Guo Jun believes that,Talent Is the Sole Capital of Private HealthcareOnly high-caliber talent can endow hospitals with strong appeal and competitiveness. Private hospitals should prioritize the recruitment of talent, particularly innovative professionals. “Without dedicated efforts in talent development, no one can achieve innovation or revitalization.”

In terms of positioning,Private healthcare providers should focus on developing specialized disciplines and premium medical services.“Overall, while a number of high-end medical service providers and international health cities have clustered in many first-tier cities, the performance ratio of high-end medical services remains relatively low compared with influential hospitals. This indicates that private healthcare still has room for improvement at this level,” said Guo Jun.

Li Zhiyong, however, believes thatThe advantage of private healthcare development lies in its flexibility.“Open if possible, close if not; in this regard, it is far more market-oriented than public healthcare.”

In brand building, private medical institutions should integrate commercial interests, public welfare, and social responsibility to deliver genuine value to patients., only by fully meeting patients' needs can one achieve self-development and gradually build credibility and brand recognition.

The development trends of private healthcare are moving in three directions:The first is specialty development, targeting niche segments presents the optimal opportunity; developing a specialized department into a center of excellence is the most effective strategy for the growth of private healthcare or for capital entry.Second, seize the opportunities presented by multi-site practice., transform medical institutions into platforms for physicians to practice at multiple sites, design robust management and compensation systems, and leverage human resource talent effectively;Third, leverage reforms in public healthcare institutions., such as the current implementation of tiered diagnosis and treatment, which aims to direct patients to primary care facilities. Private healthcare providers are more competitive than public primary care institutions; therefore, they should capitalize on the patient resources generated by tiered diagnosis and treatment, seize policy opportunities, and leverage the dual guarantees of policy support and market dynamics.

Regarding the key points for the next phase of development in private healthcare, Guo Jun stated that two core elements should be seized,One is to provide high-quality diagnostic and therapeutic services, and the other is to optimize process services and the patient experience.“Clarify your mission to enhance patients’ sense of security and satisfaction in healthcare services, safeguard patient safety, and thereby foster emotional trust.”

“Private medical institutions should have clear positioning, establish systems for talent acquisition and development, and improve internal management; break away from the traditional disease-treatment mindset, build professional disease-prevention systems, and proactively attract patients; enhance the level of specialty development to achieve technological competitiveness,” said Li Zhiyong. “Of course,The most crucial aspect remains operating with integrity, upholding medical ethics, and keeping in mind the benevolent heart of a healer.”