Pediatric Clinic Industry Report: Healthcare Resources Shifting to Primary Care, Rise of Private Pediatric Chain Clinics

In recent years, chain pediatric clinics have been emerging continuously in first- and second-tier cities. Private pediatric clinics, characterized by child healthcare and disease prevention, featuring child-friendly décor, and integrating physician resources from the public healthcare system, are experiencing explosive growth. Recently, Probe Capital produced an annual industry report on this sector, exclusively released by VCBeat (WeChat ID: vcbeat).

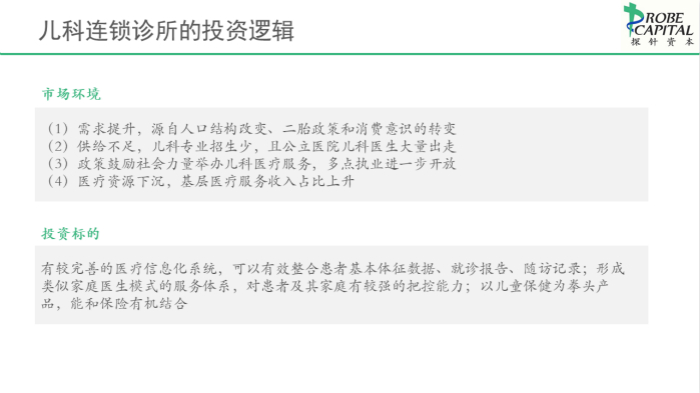

The continuous rise in pediatric care demand has been a notable trend in recent years, driven by several factors:

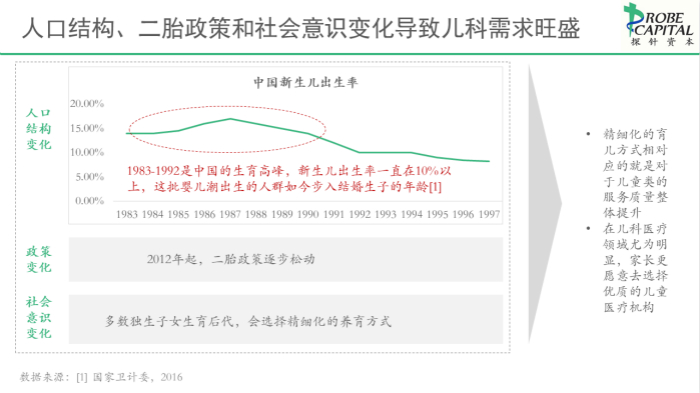

(1) Demographic shifts: From 1983 to 1992, China experienced a baby boom, with the neonatal birth rate consistently exceeding 10%. This cohort, born during the baby boom, has now reached the age of marriage and childbearing, leading to an increase in newborns and children.

(2) The relaxation of the two-child policy has further promoted childbirth, thereby increasing demand;

(3) Changes in societal child-rearing awareness: as this generation of only children becomes parents, they are more inclined to adopt meticulous parenting approaches, which has driven an overall improvement in the quality of child-focused services. This trend is particularly evident in pediatric healthcare, where parents are increasingly willing to choose high-quality pediatric medical institutions.

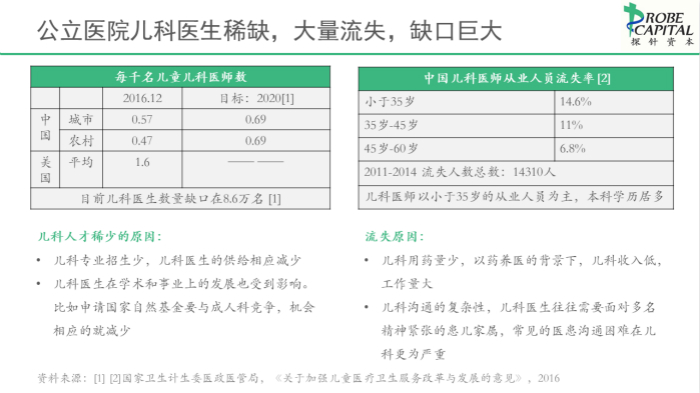

However, public hospitals face a substantial shortage of pediatricians, with already limited supply further exacerbated by significant attrition. The White Paper on the Current Status of Pediatric Resources in China indicates that the current deficit of pediatricians stands at 86,042, and this figure is projected to rise in the coming years.

According to data released in the China Health Statistical Yearbook 2015, the total number of pediatricians in China decreased from 105,000 to 100,000 over the past five years. Currently, there are only 0.43 pediatricians per 1,000 children, a figure far below the national average of 2.06 physicians per 1,000 people.

There are several reasons for the scarcity of pediatric talent in China:

(1) The limited enrollment in pediatric programs has led to a corresponding decrease in the supply of pediatricians;

(2) The academic and career development of pediatricians has also been affected. For instance, when applying for grants from the National Natural Science Foundation, they must compete with specialists in adult medicine, thereby reducing their chances of success;

Moreover, certain China-specific national conditions have also led to a continuous exodus of pediatricians from the healthcare system:

(1) Pediatric medication dosages are low; under the backdrop of hospitals relying on drug sales for revenue, pediatric departments generate low income while facing heavy workloads.

(2) The complexity of pediatric communication: Pediatricians often need to address multiple anxious family members (including parents, grandparents, or maternal grandparents), making common doctor-patient communication challenges more severe in pediatrics.

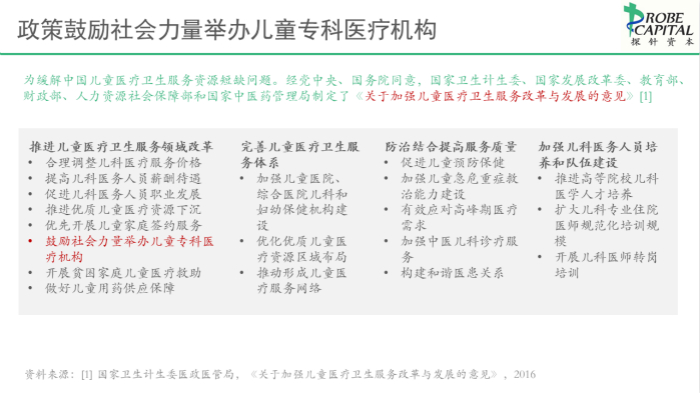

Policymakers have clearly recognized these issues; in 2016, measures were introduced to alleviate the shortage of medical and healthcare resources for children in China.

With the approval of the Central Committee of the Communist Party of China and the State Council, the National Health and Family Planning Commission, the National Development and Reform Commission, the Ministry of Education, the Ministry of Finance, the Ministry of Human Resources and Social Security, and the State Administration of Traditional Chinese Medicine have formulated the “Opinions on Strengthening the Reform and Development of Children’s Medical and Health Services,” which adopt an encouraging stance toward the establishment of specialized pediatric medical institutions by non-governmental social forces.

A review of the series of policy documents previously issued by various ministries and commissions reveals a consistent encouragement of non-governmental participation in healthcare delivery. For instance, the “Several Policy Measures on Promoting the Accelerated Development of Non-Public Healthcare Institutions” issued by the General Office of the State Council in June 2015, and the “Opinions on Further Encouraging and Guiding Social Capital to Establish Medical Institutions” adopted by the State Council in November 2010, explicitly stated that “social capital is encouraged to enter the medical services sector.”

In 2017, a series of policies were consecutively introduced to encourage the development of privately run healthcare institutions. For instance, the “Opinions on Supporting Social Forces in Providing Multi-level and Diversified Medical Services,” issued in May, further explicitly stated that “Develop a large number of private healthcare institutions with strong service competitiveness, establish several influential clusters of specialized health service industries, ensure that service supply basically meets domestic demand, and gradually form a new pattern of multi-tiered and diversified medical services.。”

In August, the National Health and Family Planning Commission issued the “Notice on Deepening the Reform of ‘Streamlining Administration, Delegating Power, and Improving Services’ to Stimulate Investment Vitality in the Medical Field,” which stated that,Further streamline the approval procedures for medical institutions by merging the establishment approval and practice registration into a single certificate for secondary-level and below medical institutions.. At the same time, it expands the scope of social investment and promotes the development of new business models in the health services industry. These are all favorable factors for establishing pediatric clinics.

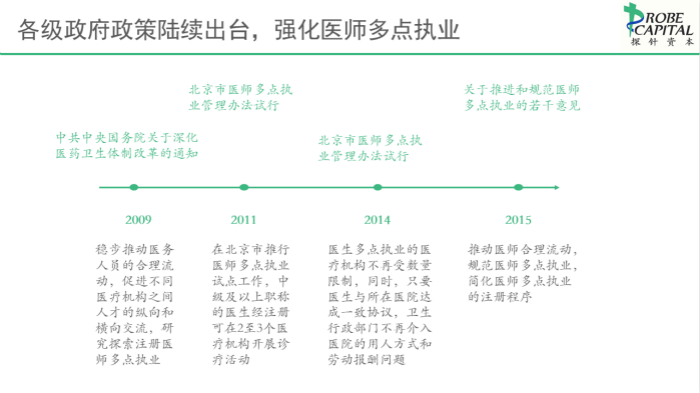

Furthermore, multi-site practice policies implemented by governments at all levels have also facilitated pediatricians’ ability to practice at multiple locations, thereby benefiting the development of pediatric clinic chains.

In the coming years, the decentralization of medical resources will be an inevitable trend. According to estimates by Ping An Securities Research Institute, while the proportion of inpatient services provided by hospitals will remain relatively stable, a significant share of outpatient services will shift toward primary care institutions. This transition presents an opportunity for the gradual rise of private pediatric clinic chains, which can absorb part of the shrinking pediatric business from public hospitals.

(1) Barriers to Medical Practice Qualifications

To rationally allocate medical resources and maximize the fulfillment of the public’s needs for healthcare services, China’s health authorities have implemented unified planning and scientific control over medical resources. The approval for establishing new medical institutions must strictly adhere to these plans to avoid redundant allocation and waste of medical resources.

Pediatric chain clinics must apply to the health authorities for a Medical Institution Practice License and are subject to strict restrictions on the scope of their approved medical specialties.

(2) Barriers to Medical Talent

Medical professionals are the core resources of the healthcare services industry and serve as the foundation for pediatric clinic chains to build their core competitiveness. A talent barrier signifies a company’s competitive advantages in professional expertise, services, and other areas. At present, highly trained pediatric medical professionals in China are primarily concentrated in large Grade IIIA hospitals and research institutions.

Offering competitive working conditions and career opportunities to attract medical professionals is a challenge that new entrants in this field must face.

(3) Management Barriers

There are currently few professional medical institutions that adopt a chain operation model for pediatric clinics to achieve rapid expansion. The primary reason is that the insufficient management capabilities and operational experience of new entrants may be one of the main factors constraining their expansion.

As a business model that places a premium on service quality, pediatric chain clinics differ significantly from highly standardized, equipment-dependent medical service providers such as ophthalmology and dental clinics.

Participants in this field must integrate their own management and operational characteristics into their development practices to establish a management and operational model that adapts to the external market environment. New entrants cannot expect to achieve growth and expansion in the short term by simply replicating the management and operational models of other companies.

(4) Brand Barriers

Brand awareness is a crucial component of brand equity, serving as a metric for assessing consumers’ recognition and understanding of a brand’s connotations and value. As an indicator of a company’s competitiveness, brand awareness can sometimes evolve into a core competitive advantage. This is particularly evident when parents select medical services, where the brand’s intrinsic meaning, trustworthiness, and the associated community culture become paramount.

The primary clientele of pediatric clinic chains consists of children and their parents. This consumer group possesses organic, inherent social transmission channels, tending to base their purchasing decisions on brand familiarity, trust, and cultural community identification with the pediatric clinic chain. Cultivating such consumer identification requires time; once established, it is difficult to shift, posing a significant challenge for late entrants in the industry.

(5) Geographic Radius Barriers

It is generally believed that the coverage radius of pediatric clinics is 3 kilometers; beyond this radius, consumers’ willingness to seek medical care decreases significantly.

Currently, there are two common site selection strategies: one is to choose mid-to-high-end residential communities where the middle class congregates. These communities typically offer convenient transportation and are located near kindergartens and primary and secondary schools, providing an inherent advantage in customer acquisition. The other strategy is to select high-traffic shopping malls in mid-to-high-end commercial districts, locating adjacent to children’s clothing stores, toy shops, and children’s educational institutions, which also generates substantial foot traffic.

Given the effective radiation range of pediatric clinics, once a clinic secures a specific geographic location, achieves significant patient acquisition, and establishes brand recognition, it will create a formidable barrier to entry for new competitors.

Currently, a number of pediatric chain medical institutions have emerged across various regions; a brief overview is provided below:

Institution | Introduction | Region | Investor | Financing Status |

Yuxueyuan | Children's Health Management Center: Online Interaction + Offline Physical Clinic | Beijing | Yuanxing Investment Honghui Capital Shuanghu Capital Honghui Capital | Completed $20 million in Series C financing in December 2016 |

Vierne Pediatrics | Pediatric Diagnosis, Treatment, and Health Care Services: Adopting the American Family Physician Model | Shanghai Shenzhen Hangzhou | GTJA DaoTong Capital | Completed a $30 million Series B financing round in August 2017 |

Ruibao Pediatrics | High-End Pediatric Medical Service Provider. Outpatient Care + Digitalization, with 3 Service Centers in Shanghai | Shanghai | GGV Capital Maxing Investment Bencao Capital | Completed a Series B financing round of RMB 70 million in April 2016 |

MedInfo (Mommy Knows) | Maternal and Infant Care: Entering via Online Operations and SaaS, Then Establishing Offline Clinics | Shenzhen | Chow Tai Fook Fosun RZ Capital Morningside Venture Capital Hawthorn Capital SoftBank China | Completed tens of millions of yuan in strategic Series B+ financing for the Chow Tai Fook Group in February 2017 |

Sunshine Women and Children | Prenatal, Postpartum + Parenting, Online + Offline | Beijing | Daoming Optics Tongdu Capital | In January 2016, Daoming Optics completed a RMB 50 million strategic investment in Sunshine Women and Children |

Zhibei | Online consultations and paid WeChat classes as entry points, followed by establishing clinics | Guangzhou | Sequoia Capital | Completed a Series A financing round worth tens of millions of yuan in July 2016 |

Ding Ding Clinic | Offline Pediatric Clinic: Diagnosis and Treatment of Common Pediatric Diseases + Health Management for Childhood Obesity and Short Stature | Zhengzhou | N/A | N/A |

Little Apple | Pediatrician Group | Beijing | N/A | N/A |

Tian'ai Pediatrics | Offline Pediatric Outpatient Clinic | Guangzhou | N/A | N/A |

Vega Pediatrics | Offline Pediatric Outpatient Clinic | Changsha | N/A | N/A |

Teddy Bear Clinic | Offline Pediatric Outpatient Clinic | Hangzhou | N/A | N/A |

Dr. Yu Pediatric Chain | Currently, there are five outpatient clinics, with the first one opening in November 2016. Each clinic ranges from 200 to over 400 square meters in size, targeting middle-income populations and placing equal emphasis on the diagnosis and treatment of common diseases and pediatric healthcare services. | Chongqing | Yuedao Investment | Yuedao as an early-stage investor |

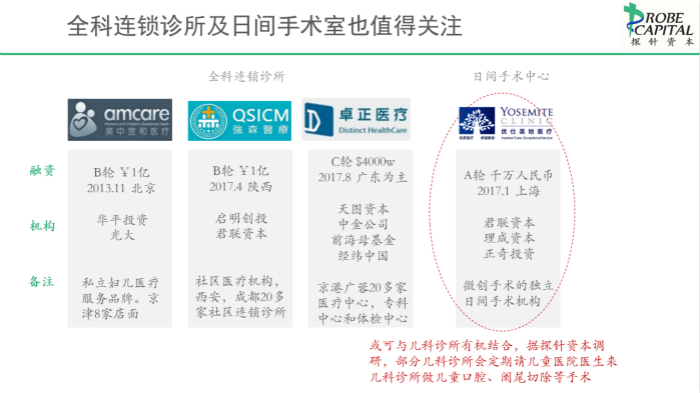

At present, pediatric clinics in Beijing, Shanghai, Guangzhou, and Shenzhen are undoubtedly the focus of capital attention, with all funded pediatric medical institutions located in these regions. In addition, central cities with large populations, rapid economic growth, relaxed household registration systems, and sufficient middle-class consumption capacity—such as Chengdu-Chongqing, Wuhan, and Zhengzhou—may also see the emergence of large-scale pediatric healthcare chains.

Furthermore, certain aspects of the business models, customer acquisition strategies, clinic decor, and human resource management systems of general practice clinics and ambulatory surgery centers can serve as valuable references. For instance, it is worth exploring whether ambulatory surgery centers can be organically integrated with pediatric clinics.

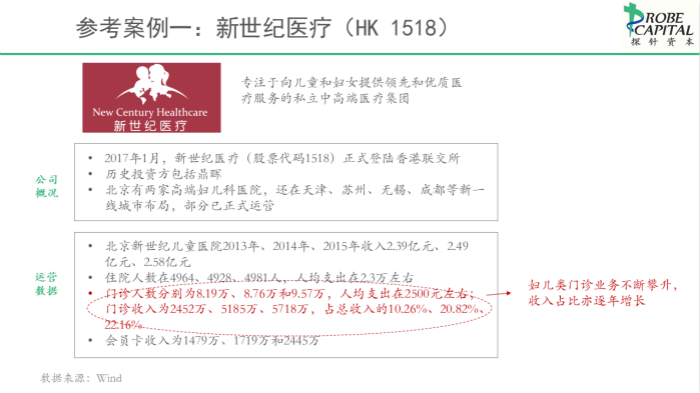

(I) New Century Healthcare

New Century Healthcare is a chain of hospitals backed by CDH Investments, focusing on mid-to-high-end comprehensive pediatric care complemented by premium obstetric services. It was listed in Hong Kong in January 2017 under the stock code 1518. The group uses Beijing New Century Children’s Hospital as its benchmark model and collaborates with the leading—and in many cases, the only—public Grade 3A children’s hospitals and obstetrics and gynecology hospitals in Beijing, Tianjin, Chengdu, Suzhou, and Dalian.

Currently, six pediatric and women’s and children’s hospitals are in operation across five cities: Beijing, Tianjin, Chengdu, Suzhou, and Dalian. In 2013, 2014, and 2015, the number of outpatient visits reached 81,900, 87,600, and 95,700, respectively, with both outpatient revenue and its proportion of total revenue increasing year by year. This trend also indirectly highlights the promising business prospects for chain pediatric clinics.

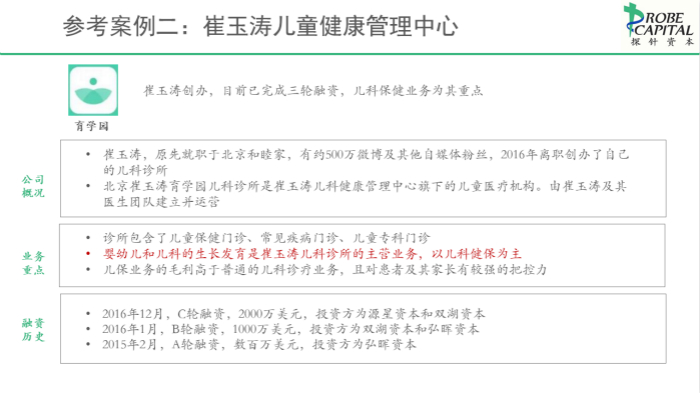

(2) Yu Xue Yuan

Beijing Cui Yutao’s Yu Xue Yuan Pediatric Clinic is a pediatric medical institution under the Cui Yutao Pediatric Health Management Center. It was established and is operated by Dr. Cui Yutao and his team of physicians. Dr. Cui Yutao, formerly affiliated with Beijing United Family Hospital, has approximately 5 million followers across Weibo and other self-media platforms. He left his position in 2016 to found his own pediatric clinic.

The clinic offers pediatric health check-up services, general disease outpatient care, and specialized pediatric consultations. Pediatric health management is the core business of Cui Yutao Pediatric Clinic, focusing on the growth and development of infants, young children, and older children. Compared with conventional diagnosis and treatment of pediatric diseases, pediatric health management services yield higher gross margins and provide stronger engagement and influence over both patients and their parents.

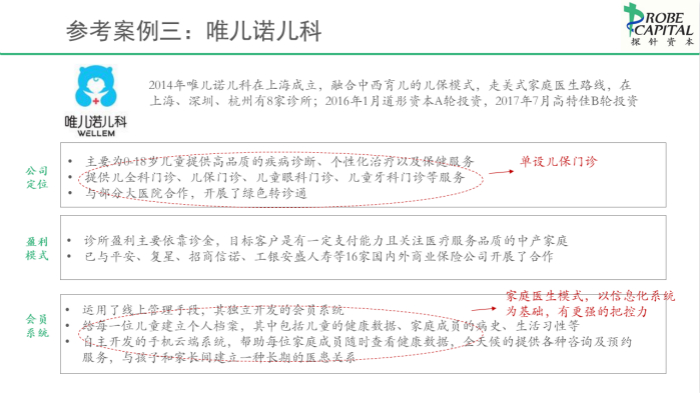

(3) Weier Nuo

In 2014, Weier’nuo Pediatrics was established in Shanghai. Integrating Chinese and Western child-rearing approaches into its child healthcare model and adopting the American family physician practice style, it operates eight clinics in Shanghai, Shenzhen, and Hangzhou. It primarily provides high-quality disease diagnosis, personalized treatment, and preventive healthcare services for children aged 0–18 years. Services include general pediatrics, child healthcare, pediatric ophthalmology, and pediatric dentistry clinics. In collaboration with select major hospitals, it has implemented a green referral pathway.

Furthermore, information technology integration is another distinguishing feature. The stores employ online management tools and have independently developed a membership system that creates individual profiles for each child, encompassing health data, family medical history, and lifestyle habits. Additionally, a mobile cloud-based system has been developed to enable family members to access health data at any time, while providing round-the-clock consultation and appointment services. This approach facilitates the establishment of long-term relationships with children and their parents and serves as one of the key strategies for implementing family physician services.

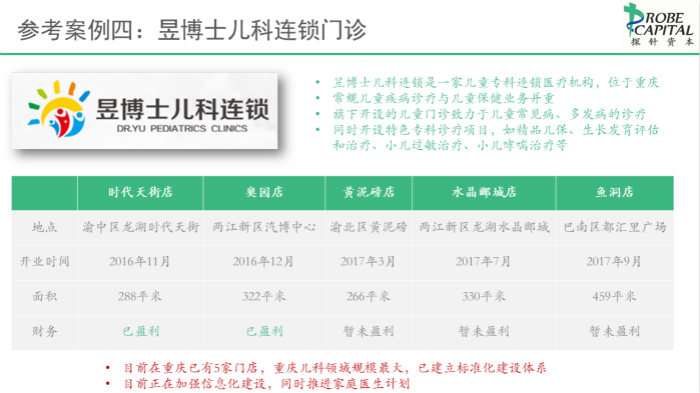

(4) Dr. Yu Pediatric Chain

Dr. Yu Pediatric Chain is a specialized pediatric chain organization based in Chongqing. As of September 2017, it operated five outpatient clinics, making it the largest provider in Chongqing’s pediatric sector, with a fully established standardized system. Dr. Yu’s pediatric clinics focus on the diagnosis and treatment of common and frequently occurring childhood diseases, while also offering specialized child healthcare services, such as premium well-child care, growth and development assessment and therapy, pediatric allergy treatment, and pediatric asthma management. The organization is currently strengthening its information technology infrastructure and advancing its family doctor program.

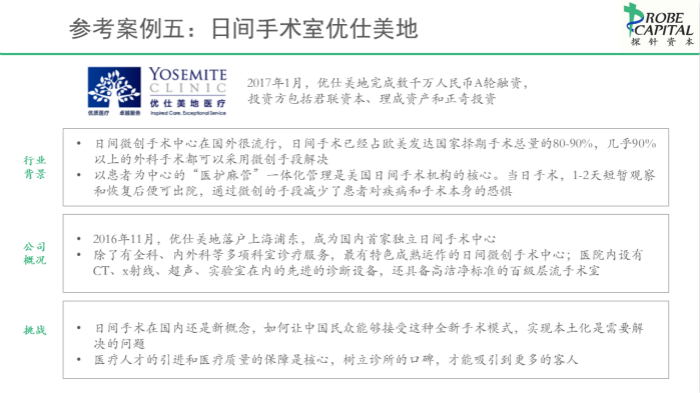

(5) Usmile

YouShiMeiDi is an ambulatory minimally invasive surgery center. Ambulatory surgery is highly prevalent abroad, accounting for 80–90% of all elective procedures in developed countries across Europe and the United States, with nearly 90% of surgical operations amenable to minimally invasive techniques. This model is still in its early stages in China; it may be beneficial to consider its organic integration with pediatric clinics as a reference.

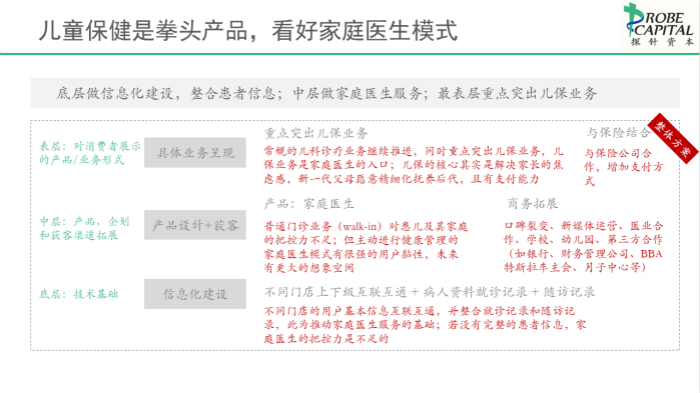

The business model favored by Probe Capital consists of: (1) building an IT infrastructure at the foundational level to integrate patient information; (2) providing family doctor services at the intermediate level; and (3) prioritizing pediatric healthcare services at the consumer-facing level.

The foundational layer of information technology infrastructure serves as the technical basis. It is essential to achieve interconnectivity of basic user information across different chain stores, and to integrate medical consultation records with follow-up records; this constitutes the foundation for promoting family doctor services. Without comprehensive patient information, family doctors lack sufficient oversight and management capability.

The mid-tier product model is the family doctor, as general outpatient services (walk-in) lack sufficient control over pediatric patients and their families, making it impossible to achieve genuine preventive care and health management. In contrast, the family doctor model fosters strong user stickiness and enables proactive health management, offering greater future potential, such as integration with insurance products.

In terms of customer acquisition for family doctors, in addition to initial word-of-mouth referrals, it is essential to explore channels such as new media operations, collaborations with medical institutions, schools, kindergartens, and third-party partnerships (e.g., high-net-worth clients of banks, financial management firms, BBA/Tesla owner clubs, and postpartum care centers).

The product/service model most directly presented to consumers is pediatric healthcare services. While routine pediatric clinical services must continue to advance, the emphasis should be placed on pediatric healthcare services, which serve as the entry point for family doctors.

At its core, pediatric healthcare aims to alleviate the anxiety of new-generation middle-class parents. These parents are willing and financially able to provide meticulous care for their children, making pediatric healthcare services the most direct solution to address their parenting concerns. Once this model is proven viable, collaborations with commercial insurance companies can be explored.

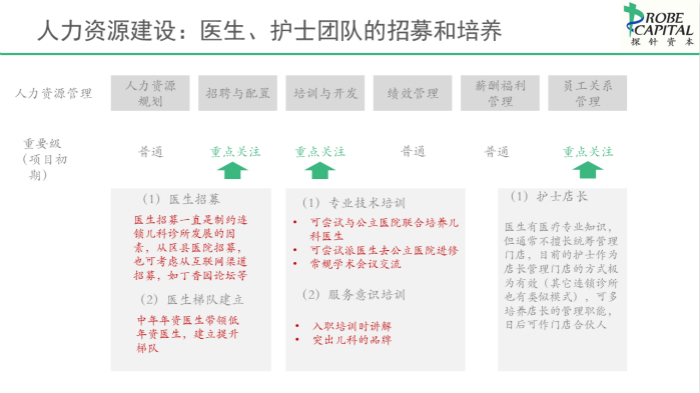

In the field of pediatric chain healthcare, human resource management focuses on three key areas: (1) recruitment and staffing, (2) training and development, and (3) employee relations management.

First, physician recruitment has consistently been a bottleneck constraining the development of chain pediatric clinics. While poaching talent from renowned tertiary hospitals or even overseas institutions is one approach, it incurs prohibitively high costs. Currently, recruiting from district- and county-level hospitals represents a more feasible and cost-effective model. Additionally, online channels, such as recruitment via the DXY Forum, can be leveraged. Meanwhile, establishing a structured physician hierarchy is also critical; for instance, mid-career physicians can mentor junior doctors in their professional onboarding.

Secondly, employee training is an area that requires significant investment of effort. Training is divided into two main categories: (1) professional technical training and (2) service awareness training. The former constitutes the foundation of the entire service. Unlike medical services in fields such as dentistry, ophthalmology, and medical aesthetics, which rely heavily on equipment and feature highly standardized processes, pediatric medical care demands more comprehensive professional competencies from doctors and nurses. Therefore, providing staff with training in professional skills is of paramount importance. In addition to lectures and guidance provided by senior physicians within the organization, it is also crucial to offer employees access to various channels for academic exchange.

If feasible, joint training of pediatricians by private chain pediatric medical institutions and public hospitals is a promising approach. The latter refers to the cultivation of service orientation; there is often significant room for improvement in the service mindset (such as approachability) among physicians within the public system, which can be addressed during onboarding training. If implemented effectively, this service orientation will be integrated into daily operations and become an integral part of the pediatric brand.

The final point to address separately is the selection of candidates for the role of clinic manager. After interviewing various private clinics, we recommend appointing nurses as managers for pediatric clinics, a suggestion aligned with the specific characteristics of pediatrics. While pediatricians possess strong medical expertise, they are typically less skilled in overall clinic management. Furthermore, given the diversity and low standardization of pediatric services, pediatricians are not the optimal choice for clinic managers. In contrast, nurses already coordinate numerous managerial functions, making them more suitable for the role of clinic director, with potential development toward becoming clinic partners.

The external market environment has undergone and is undergoing transformation. Driven by demographic shifts, the stimulus of the two-child policy, and heightened parental awareness regarding child-rearing consumption, demand for pediatric medical services continues to rise. However, on the supply side, there is a severe shortage; the recruitment of specialized pediatricians has long been limited, while public hospitals are experiencing a significant exodus of pediatric staff.

Policymakers have recognized the imbalance between supply and demand in pediatric healthcare, leading to the introduction of a series of policies encouraging non-governmental entities to establish pediatric medical services and promoting further development of multi-site practice.

Regarding investment targets, we favor a model characterized by: a robust underlying information system that effectively integrates patients’ basic vital signs data, medical visit reports, and follow-up records; a mid-layer service system centered on the family doctor model, which exerts strong oversight over patients and their families and actively promotes health management rather than merely providing routine diagnosis and treatment for pediatric diseases; and a surface layer featuring child healthcare as its flagship product, coupled with the capability to collaborate with commercial insurance companies.

Probe Capital is a corporate management and financial advisory firm established in 2017. Specializing in the healthcare sector, the company provides financial advisory, strategic planning, financial restructuring, product commercialization, and executive recruitment services to enterprises that have previously received healthcare investments. It has currently completed its angel financing round. The founding team hails from leading domestic healthcare funds, healthcare-focused financial advisory firms, and publicly listed companies.