Health Management in 2017 Year-End Review: Capital Concentration, State-Led AI and Big Data Drive, and Cross-Industry Players Entering the Market

As 2017 draws to a close, VCBeat is once again launching its annual flagship initiatives: the “Top 100 Future Healthcare Companies” ranking and the “Top 100 Future Healthcare” Forum. Prior to the announcement of the rankings and the convening of the forum, VCBeat has meticulously curated a comprehensive year-end review series. This series will sequentially summarize, analyze, and provide outlooks for various subsectors within the healthcare industry in 2017. By examining more than 30 specialized segments, it aims to offer insights into the industry as a whole, delivering a rich feast of content to our readers.

Let us first review the companies that made it onto the Top 100 list in 2016: Codoon, Meiyou, Dayima, Keep, Miao Health, Mommy Knows, Palm Sugar Doctor, WeTang, Runer Health, TangZhangKong (Diabetes Control), and Boohee Technology. If health management in 2016 was characterized by a spark igniting a prairie fire, then in 2017, the sector entered a phase of divergent development, with first-tier companies beginning to pull ahead.

In 2017, the expansion of health management companies did not accelerate, and capital investment was not as robust as in 2016. The lack of a clear positioning for health management became the primary reason why most companies gradually fell into obscurity.

In terms of policy, with the continuous advancement of the Healthy China strategy, policies related to health management, particularly chronic disease management, were frequently featured in major media reports in 2017, as the health industry gradually assumes a prominent position in top-level design.

In 2017, the health needs of the general population came to the forefront. With the integration of new technologies such as artificial intelligence and big data, along with the entry of more new players, the health management industry began to achieve economies of scale. Meanwhile, rational capital investment has made the “Matthew Effect” among enterprises increasingly pronounced. Service delivery targeting the smallest units has been implemented at the community level, which not only responds to the national call for tiered diagnosis and treatment but also reduces the cost of health management for the public. Health management has gradually evolved from an initial high-end service into a universally accessible one.

Data shows that China’s health industry has consistently maintained an annual growth rate of over 10%, with its market size exceeding RMB 3.2 trillion by the end of 2016. The market size for health management has surpassed RMB 110 billion and is projected to expand to RMB 203.9 billion by 2020. Coupled with the continuous development and maturation of high-tech innovations such as smart healthcare, the health management sector has evolved from single-dimensional self-management to specialized, real-time management, further enhancing service experience and public awareness.

I. Multiple macro-level plans have proposed health management, establishing its firm footing in national strategy

In October 2017, at the 19th National Congress of the Communist Party of China, Xi Jinping reiterated the implementation of the Healthy China strategy, proposing to improve national health policies and provide comprehensive, full-lifecycle health services for the people. The concept of “Healthy China” originated from General Secretary Xi Jinping’s slogan during his inspection tour in Zhenjiang, Jiangsu Province, in late 2014: “Without universal health, there can be no comprehensive well-being.” Since then, “Healthy China” has gradually been elevated to a national strategy.

In September 2017, the National Health and Family Planning Commission issued a notice requiring further verification and confirmation of impoverished rural residents with chronic diseases for inclusion in the family doctor contract service management. The initiative prioritizes coverage for patients with hypertension, diabetes, tuberculosis, and other chronic conditions, with plans to gradually expand to encompass all individuals with chronic diseases. The goal is to achieve full coverage of contract services for registered impoverished rural households by the end of 2017. Regions with adequate resources may gradually extend coverage to include rural residents receiving subsistence allowances, individuals in extreme poverty, and impoverished persons with disabilities.

In August 2017, the State Council issued the Guiding Opinions on Further Expanding and Upgrading Information Consumption to Continuously Unleash Domestic Demand Potential, which proposed strengthening online education and healthcare. It called for enhanced research and development of smart devices for home diagnosis, health monitoring, and analytical diagnostics; further promotion of online medical services such as appointment scheduling, online payment, and result inquiry; and the advancement of applications including online health consultations, home-based health services, and personalized health management.

In July 2017, the State Council issued the “Notice on the Development Plan for the New Generation of Artificial Intelligence.” The Notice proposed strengthening population-based intelligent health management, achieving breakthroughs in key technologies such as big data analytics for health and the Internet of Things (IoT), and developing wearable health management devices and smart home health testing and monitoring equipment. These efforts aim to facilitate a transformation in health management from spot-check monitoring to continuous monitoring, and from short-process management to long-process management.

In January 2017, the State Council issued the Medium- and Long-Term Plan for the Prevention and Control of Chronic Diseases in China (2017–2025). The Plan pointed out the need to establish a long-term working mechanism for health management. It clarified the responsibilities of various parties, including the government, medical and health institutions, families, and individuals, in health management, and improved the content and processes of health management services. Appropriate technologies for early diagnosis and treatment of major chronic diseases, such as cancer and stroke, that meet specified conditions will be gradually incorporated into routine clinical practice in accordance with regulations. Efforts will be made to explore methods such as government procurement of services to encourage enterprises, public welfare and charitable organizations, and commercial insurance institutions to participate in risk assessment, health consultation, and health management for high-risk populations of chronic diseases, thereby fostering a health management service industry characterized by personalized services, membership-based operations, and holistic promotion.

In January 2017, the State Council issued the “13th Five-Year Plan for Health and Wellness.” The Plan stated that it is necessary to promote the interoperability and sharing of population health information. Relying on regional population health information platforms, the continuous recording of electronic health records (EHRs) and electronic medical records (EMRs) should be achieved, along with information sharing among medical institutions of different levels and categories. The “Internet+” health and medical services benefiting the public shall be fully implemented; telemedicine targeting central and western regions and grassroots levels, as well as online-offline integrated smart healthcare, shall be developed. This will foster the deep integration of information technologies—such as cloud computing, big data, the Internet of Things (IoT), mobile internet, and virtual reality—with health services, thereby enhancing the capacity of health information services.

Reviewing the major events related to health behaviors and health management in 2017, we can basically see two major development trends. First, health management has increasingly been incorporated into macro-level planning, with a broader scope; for instance, phased plans in sectors such as consumption and artificial intelligence have explicitly outlined content related to health management. Second, AI and health big data-assisted health monitoring and behavioral management have officially been integrated into national development plans.

II. Capital Becomes More Rational, Fitness Remains Booming, and the Head Effect Among Enterprises Begins to Emerge

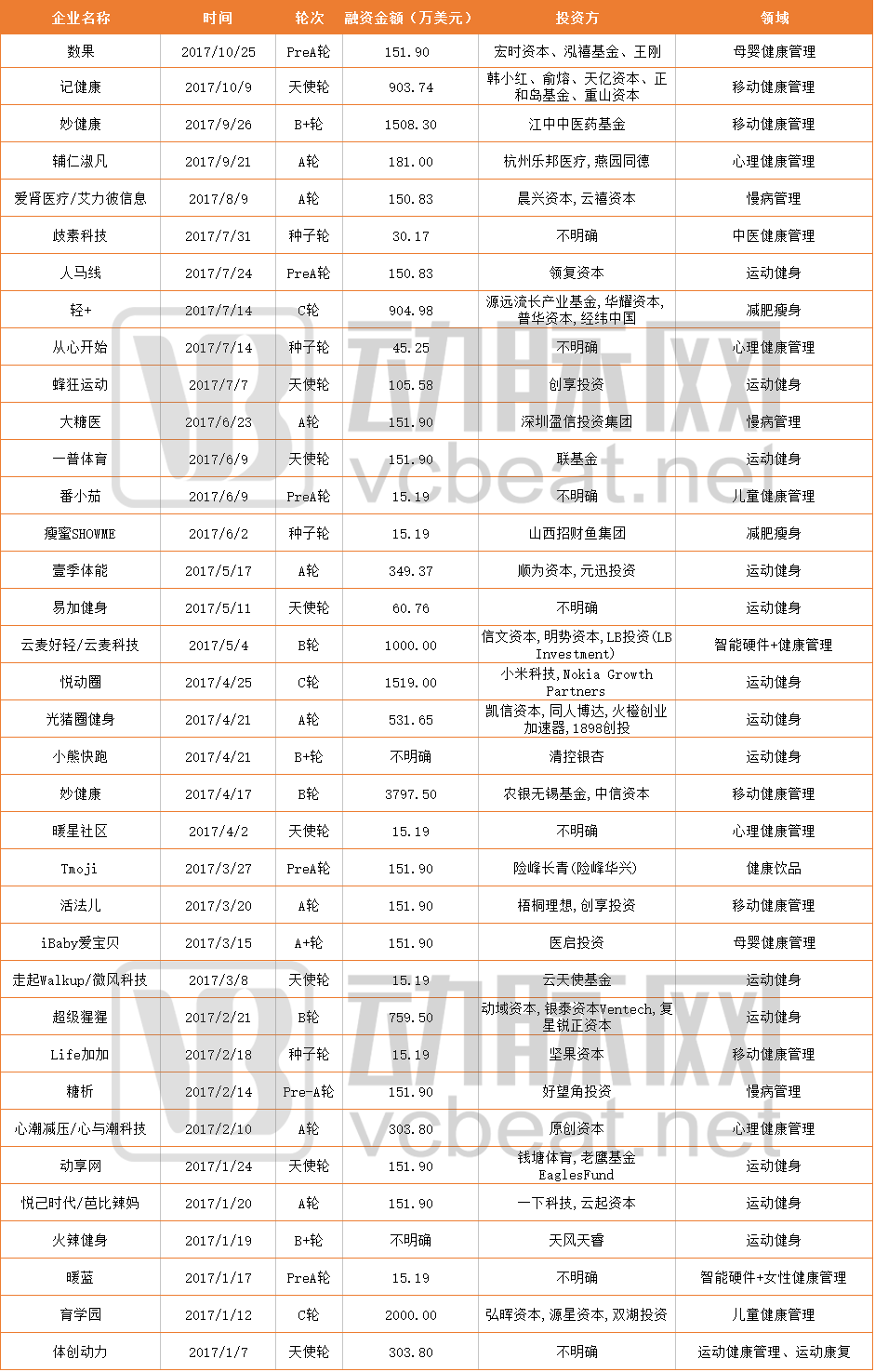

Financing Events in the Health Management Sector as of November 1, 2017

(Note: For companies that have not disclosed their financing amounts, conservative estimates are used: “several million RMB” is approximated as RMB 1 million, “tens of millions RMB” as RMB 10 million, and so on, with all figures converted into U.S. dollars.)

Distribution of Funded Enterprises by Sector

In the key focus areas, sports and fitness remained highly popular, with 13 financing rounds this year. Following closely were mobile health management, health management for special populations such as women and children, and mental health management.

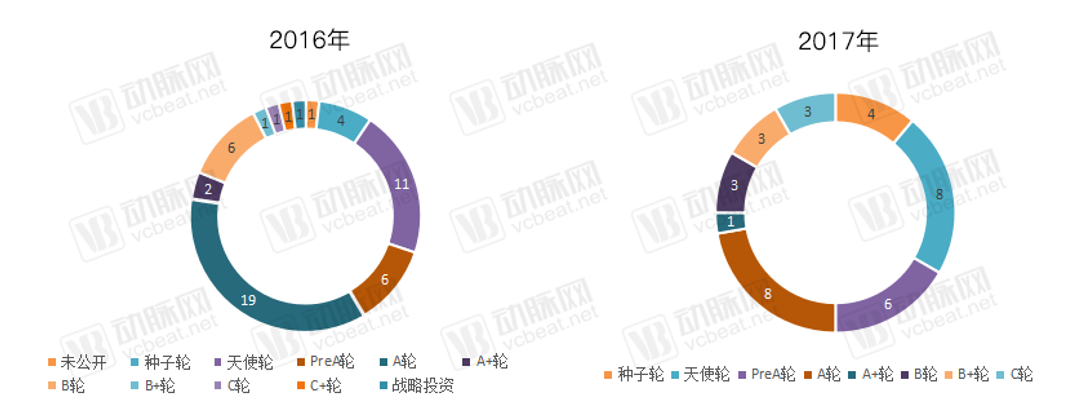

According to statistics from the VCBeat database, as of November 1, 2017, the total disclosed financing amount in the health management sector was approximately $160 million, with 36 financing events occurring and 35 companies receiving funding (Miao Jiankang completed two rounds of financing this year). Compared with the data for the same period in 2016, we find that as of November 1, 2016, there were 53 financing events, showing a clear advantage in number over 2017. However, based on the disclosed data, the total financing amount for the same period in 2016 was only $101 million.

Comparison of Financing Rounds in 2016 and 2017

In 2017, capital interest in the health management sector cooled significantly, with a sharp decline in financing activities. In 2016, there were 41 financing events at stages prior to Series A, accounting for 77% of the total, while only 12 companies secured funding beyond Series A. These data indicate that both investors and startups were still exploring this sector, with limited capital investment characterized by a “broad-spectrum” approach. Looking at the financing landscape for health management in 2017, deals remained concentrated at the Angel and Series A stages, with only nine companies advancing beyond Series A, largely continuing the development trend observed in 2016.

However, a clear trend is emerging in the health management sector: a “winner-takes-all” effect is taking shape, with capital increasingly concentrating on leading companies within the industry, and large-scale financing rounds becoming more common. Companies such as Qingjia, Yuedongquan, and Yu Xueyuan have entered Series C funding rounds. Their business models are relatively mature, and firms at this stage have typically achieved profitability at scale.

Notably, the mobile health management platform Miao Jiankang completed two rounds of financing this year—Series B and Series B+—with impressive figures. The company secured RMB 250 million and RMB 100 million in Q2 and Q3, respectively (totaling approximately USD 53.05 million). In 2017, a year marked by tighter capital markets, such substantial funding was rare in the health management sector.

III. The Emergence of New Technological Trends

1. Deep Integration with Big Data: Giants Such as Apple and Alibaba Are Actively Entering the Space

Health management embodies integrated medical technologies; its development is driven not by a single industry, but by the collaborative efforts of multiple sectors.

Currently, with the aid of technologies such as the Internet of Things (IoT) and big data, health is no longer the exclusive domain of medical enterprises. Multi-perspective explorations in health management are underway, and a coordinated development pattern involving multiple industries in the market is gradually taking shape.

As a range of health management applications and service providers have emerged, the practical application of industrial collaboration is deepening. Major conglomerates such as Apple, Alibaba, and Google have also entered the health management sector to varying degrees, leveraging their developmental advantages across multiple industries to gradually implement comprehensive technologies for health management services, thereby highlighting the unique strengths of their respective products.

Major Companies Strategize in Health Management, with Data as the Primary Key Factor

In September 2017, Apple released its latest Apple Watch, which first added a pulse sensor in terms of hardware to track the user's heart rate in real time and monitor their cardiac health.

Meanwhile, the Apple Watch also collects vast amounts of heart rate data, leveraging big data applications to drive related medical research in this field. Furthermore, the product has simultaneously integrated a series of Internet of Things (IoT) applications, such as exercise detection and sleep monitoring, further enhancing the company’s multi-sector layout in the health management industry.

According to the fiscal year 2017 performance announcement released by Alibaba Health, product development expenditures for FY2017 amounted to RMB 109 million (in RMB, unless otherwise stated), an increase of RMB 32.43 million from RMB 76.15 million in the previous year, representing a 42.6% growth primarily driven by an expansion in R&D personnel. During the year, Alibaba Health recruited additional information technology engineers to expand its healthcare service network and build a health management platform and a medical intelligent analytics engine.

In fact, in October 2016, Alibaba Health launched the “Smart Care Initiative,” marking its first step toward building an intelligent personal health management platform. In collaboration with Alibaba Smart and nearly 20 well-known manufacturers of smart health devices and services—including Sinocare, Haier Medical, Pocket Sugar Doctor, Yuwell, Roche, Bayer Ascensia, and Omron—Alibaba Health introduced a comprehensive health management service platform for consumers.

In its fiscal year 2017 performance announcement, Alibaba Health explicitly stated: “The Group will collaborate with more like-minded partners to explore the application of big data analytics in establishing personalized electronic health records for the public, thereby promoting integrated health services that encompass prevention, treatment, rehabilitation, and health management across the entire lifecycle.”

Leveraging Health Big Data, Mobile Health Management Gains Popularity

In an era where health big data is becoming increasingly valuable, mobile health management platforms are emerging as key traffic gateways for services. As the highest-valued company in the health management sector, Miao Health has frequently attracted capital attention, completing RMB 450 million in financing within just 18 months. Leveraging health big data and integration with wearable devices, Miao Health has gradually carved out its path in mobile health management.

“Miao+” is the open platform for health data and services under Miao Health. It integrates data from over 300 smart wearable devices across 17 categories, including smart bands, blood pressure monitors, glucometers, body fat scales, thermometers, and fetal heart rate monitors. Additionally, it incorporates various health-related data such as physical examination results, genetic data, and insurance data. By leveraging open traffic entry points to collect massive amounts of health big data, the platform aims to achieve precise management of health behaviors.

In the view of Kong Fei, CEO of More Health, “the ability to manage one’s own health is also a hallmark of success.” More Health has pioneered the Health Behavior Index (M-Value) as a benchmark for assessing users’ health behaviors, leveraging “big data algorithms + artificial intelligence” to analyze daily health information. A higher M-Value indicates healthier behaviors, making health behaviors more visible to users. Based on this metric, a personalized library of health tasks—covering exercise, diet, sleep, and more—is established to help users improve their health behaviors.

In August 2017, the Miao Health Behavioral Index (M-Value) passed acceptance review by an expert panel composed of multiple national professional associations and institutions, including the Chinese Association for Health Promotion and Education, the Health Development Research Center of the National Health and Family Planning Commission, and the Institute of Health Communication at Tsinghua University. It became China’s first comprehensive index to assess individual health behaviors using a quantitative scoring system.

Validated by national authorities, this milestone underscores the boundless application prospects of big data in health behaviors. By leveraging technologies such as big data, cloud computing, and the Internet of Things (IoT), wearable medical and health devices have become a critical gateway for information acquisition in future smart healthcare, enabling the real-time collection of extensive user health data and behavioral patterns.

When these health data and vital sign indicators are aggregated and analyzed through big data and artificial intelligence, they will inevitably drive the integration of prevention, treatment, rehabilitation, and health management across the entire life cycle.

2. Artificial Intelligence Remains a Hot Topic as the Nation Opens the Door to AI Applications in Health Research

2017 was hailed as a turning point in the development of artificial intelligence, marked by the accelerated commercialization of AI-driven medical technologies. Within the industry, capital investment surged, with AI-related companies successively securing substantial funding rounds. In Q3 2017 alone, the total disclosed financing in the AI sector exceeded $50.25 million, equivalent to approximately RMB 330 million.

According to the “2017 Report on the Medical Big Data and Artificial Intelligence Industry” released by VCBeat this September, health management combined with smart hardware can theoretically achieve comprehensive human health management. However, due to current limitations in sensor and hardware development, as well as insufficient accumulation of disease-related data, the primary applications are currently focused on diabetes management, chronic disease management, blood pressure management, breast health management, and fetal heart rate monitoring.

Key health-related applications of artificial intelligence include risk identification, health assessment, mental health monitoring, and health interventions. According to statistics from VCBeat, there are currently eight AI companies in China involved in health management, including iCarbonX, YueTang, YiSuiFang, and Jinglun Shiji, with their business areas primarily focused on chronic disease and specialized disease management.

In January 2017, iCarbonX, together with its digital life ecosystem partners, officially launched Meum™, a digital health management platform, and invested RMB 400 million to establish the Digital Life Alliance.

In October 2017, Ping An Insurance (Group) Company of China and Tsinghua University established an industry-academia-research partnership. One key outcome of this collaboration was the establishment of the Global Medical and Health Research Center under the guidance of the National Health and Family Planning Commission. The project aims to focus on research topics such as AI applications in medicine, personal health risk assessment, healthcare institution management, health economics, and health big data. It seeks to enhance the academic level of domestic medical theoretical research and strengthen the translation of research findings into practice, thereby actively promoting greater participation by the nation and enterprises in global health development and contributing to the realization of the “Healthy China” initiative.

Liu Wenxian, Deputy Director of the Department of Planning and Information under the National Health and Family Planning Commission (NHFPC), stated at the cooperation ceremony, “The NHFPC is assembling a ‘national team’ to enter the health and medical industry.”

During the same period, Zhang Jing’an, an Academician of the International Eurasian Academy of Sciences and Vice Chairman of the China Science Center of the International Eurasian Academy of Sciences, pointed out at the inaugural International Summit Forum on “Smart Health Management” that, as artificial intelligence and big data become increasingly integrated with the broader health sector, the industry has entered a new era of “digital health management.” This development has provided solutions to two major pain points in the field—namely, the difficulty in acquiring health data and the lack of intervention measures despite the availability of such data—thereby making the concept of “preventive treatment” a reality.

Based on the series of national and corporate initiatives in 2017, the exploration of artificial intelligence applications in the field of health management is evolving toward a government-led, multi-stakeholder participation model.

3. Implementation of Community Health Management: Family Doctor Contracting Promotes Resident Health Management

Community Health Management refers to the application of various techniques and knowledge from preventive medicine, clinical medicine, social sciences, and management science. Leveraging community health service centers (and stations) as operational platforms, it provides residents within the community with technical services including health monitoring, health risk assessment, health education, health interventions, and disease management.

On September 26, 2017, the National Health and Family Planning Commission issued a notice requiring further verification and confirmation of patients with chronic diseases among the rural impoverished population, so as to include them in the management of family doctor contracted services. Priority coverage shall be given to patients with hypertension, diabetes, tuberculosis, and other chronic diseases, with gradual expansion to cover all individuals with chronic conditions. Efforts shall be made to achieve full coverage of contracted services for registered rural impoverished households by the end of 2017. Regions with appropriate conditions may gradually extend coverage to rural residents receiving subsistence allowances, individuals in extreme poverty, and impoverished persons with disabilities.

The state mandates full coverage for chronic disease management and resident health, positioning communities as the “gatekeepers” of residents’ health.

Responding to the Tiered Diagnosis and Treatment System, Achieving Broad Coverage of the “Smallest Unit” of Health Management

With the introduction of tiered diagnosis and treatment and the incorporation of chronic disease prevention and control into top-level design, health management services provided by primary healthcare institutions have gained widespread popularity, making health management based on community health service centers and family doctor services a major trend.

In May 2017, the Liangjiang New Area communities partnered with Boao Yihe Leijingtang Health Management Co., Ltd., and joined forces with the Jinshan Branch of the First Affiliated Hospital of Chongqing Medical University, Chongqing Liangjiang New Area First People’s Hospital, and Chongqing Liangjiang New Area Second People’s Hospital to jointly advance a public welfare project for diabetes health management.

Over the next two years, the project will provide prediction, screening, and treatment for diabetes and its complications to 150,000 permanent residents across eight sub-districts in Liangjiang New Area, effectively reducing the incidence of diabetes among community residents in the area.

In terms of chronic disease prevention and control, it is essential to mention the current initiative of “family doctor contract signing” to achieve chronic disease management at the community level, which serves as the “smallest unit.”

At the 2017 National Conference on Primary Healthcare, Li Bin, Director of the National Health and Family Planning Commission, stated that in 2016, the family doctor contract signing rate in pilot cities across China had reached 22.2%, with a signing rate of 38.8% among key populations, thereby exceeding the annual targets. According to data from the National Health and Family Planning Commission, 26 provinces, autonomous regions, and municipalities have issued guidance documents or implementation plans to promote family doctor contract services, which are set to expand to more than 85% of prefecture-level cities this year.

In Hangzhou, a national leader in family doctor contract services, the development of the general practitioner workforce has become key to the success of these contracts. Currently, 97% of general practitioners in Hangzhou have participated in rotational training. The specific health management and home-based medical services provided include prevention, public health management, clinical care, health management, remote health monitoring, and health assessment.

Furthermore, the health management component embedded within community health service centers has also received significant attention. Policies such as subsidies and accountability systems have contributed to enabling family doctors to fulfill their health management obligations under contracted services and facilitating the implementation of community-based health management.

Smart Systems Support Grassroots Health Management and Empower Community Physicians

Community healthcare at the grassroots level relies on the establishment of intelligent information systems. In the advanced “Hangzhou Model,” Gongshu District, as a national model for community health service centers, completed the construction of a general practitioner service support system and a two-way referral system based on the regional health information platform in 2016. In 2017, the “Healthy Gongshu” platform was launched and integrated with public health business systems, achieving interoperability of residents’ health data and leveraging informatization to empower family doctors in serving the public.

As one of China’s earliest general practitioners, Li Xiaoxia, founder of Kangbairui, is well aware of the pain points in physicians’ work. Therefore, Kangbairui is committed to developing intelligent systems to empower family doctors in their practice.

In 2017, Kangborui further accelerated the implementation of primary healthcare management solutions, launching smart community services in Shenzhen, Yinchuan, Qinghai, Hebei, and other regions. The company established an efficient workflow system for tiered diagnosis and treatment, community-based chronic disease management, medical and health service management, and family doctor services. Built upon the physician workstation system, it promoted standardized community health management processes and provided primary care physicians with structured clinical pathways for health management.

Li Xiaoxia stated, “Kangborui productizes community health management solutions by generating population profiles and developing intelligent management plans and health prescriptions for individuals requiring health management services. This approach clarifies ‘how to manage’ for physicians and, through an efficient physician workflow system, supports contracted family doctor services at the community level, the smallest operational unit.”

It is reported that this year, Kangbairui will also collaborate with the Information Center of the Shenzhen Municipal Health and Family Planning Commission to carry out research on the informatization of health management. As Shenzhen is one of the pilot cities for community-based chronic disease management under the national healthcare reform initiative, Kangbairui has authorized workstations for physicians at more than ten community health service centers across Shenzhen, enabling them to manage chronic disease patients in their communities more efficiently.

IV. Contraction or Expansion? More New “Players” Enter the Arena

From the perspective of service nature, the concept of health management has narrowed; however, from an industrial standpoint, the opposite is true, as the scope of health management has actually expanded. In 2017, companies from various sectors continued to cross industry boundaries and enter the health management field, aiming to secure a share of this vast market.

1. Real Estate Has a Natural Advantage in Embedding Community Health Management

When it comes to community management, real estate developers have always held a natural advantage. Taking Evergrande as an example, according to incomplete statistics, the company owns more than 400 residential communities across over 200 cities in China, serving 3.7 million homeowners and adding 700,000 to 800,000 new residents annually, making it an industry leader. Coupled with peripheral community resources, Evergrande possesses unique advantages for operating internet-based community hospitals, which is one of the core businesses of Evergrande Health.

Other real estate companies largely follow this same pattern. By leveraging their substantial customer bases, they ensure a broad population coverage for health services, prompting an increasing number of real estate enterprises to join the health management sector. In the early stages of development, these efforts are primarily centered on small-scale health management facilities within residential communities.

In September 2017, WeDoctor and Luneng Group signed a project cooperation agreement in Beijing to accelerate the deep integration of “Internet + Family Medicine + Real Estate.” WeDoctor’s new type of medical institution, the WeDoctor General Practice Center, settled into Taishan No. 9 in Jinan, providing comprehensive, in-depth healthcare services featuring “general practice + specialty care + home smart terminals” to the owners of Taishan No. 9 and the 80,000 residents of the surrounding Lingxiu City area.

In May 2017, Vanke Emerald Alliance formally entered into a strategic partnership with Shanghai Maple International Women’s and Children’s Hospital, a premium international healthcare institution. The collaboration aims to introduce world-class medical and health management services to Vanke’s Emerald-series communities. Concurrently, the first “Emerald Community Medical Health Center” was officially inaugurated at the Vanke Emerald Binli Jin Clubhouse.

Health management services for real estate projects can be viewed as an enhancement to property amenities, but more importantly, they represent a one-stop, closed-loop service that integrates behaviors related to living, lifestyle, and health.

2. Insurers Rush into Health Management, Profit Models Yet to Be Explored

The “Insurance + Health Management” model is gaining increasing recognition from a growing number of institutions.

In August 2017, CPIC Life Insurance’s equity investment in Pacific Medical Health Management Co., Ltd. received approval from the China Insurance Regulatory Commission (CIRC). Recently, CPIC Group disclosed that its board of directors had approved a capital increase of RMB 700 million to CPIC-Allianz Health Insurance, with the company and other shareholders of CPIC-Allianz Health Insurance contributing in proportion to their respective shareholdings.

At this point, all four A-share listed insurance companies have fully rolled out their layouts in health management firms.

In September 2017, ZhongAn Online entered into a strategic partnership with Guokang Private Doctor Group, a health management service provider, whereby the latter provides private doctor health management services to ZhongAn’s customers. This past September, ZhongAn Insurance successfully listed on the Main Board of the Hong Kong Stock Exchange, marking the debut of the first internet insurance stock.

From a market perspective, the “insurance + health management” model creates a win-win situation for both policyholders and insurers. Policyholders can improve their physical condition by meeting specified health targets, thereby qualifying for partial premium reductions, while insurers can lower their claims payout ratios by encouraging healthier lifestyle habits among users.

However, at present, collaborations between insurance companies and health management organizations remain in an exploratory phase. Drawing from the model in the United States, the birthplace of health management, it is an inevitable trend for insurers to provide health management services to their clients. Yet, in China’s insurance market, establishing dedicated health management subsidiaries or investing heavily in partnerships with health management firms has increased both policyholders’ costs and insurers’ operational expenses. The effectiveness of such initiatives has not yet been substantiated by data, and the sector as a whole remains in a stage of practical exploration. Investors are advised to remain patient.

In summary, VCBeat believes that in 2017, health management transitioned from the “1.0” era, which was primarily characterized by health consultations and high-end private physicians, into the “2.0” era, led by cutting-edge technologies such as big data and artificial intelligence. Based on the above analysis, the health management industry in 2017 can be summarized as follows: rational capital investment, government-led development, technology-driven innovation, and multi-party participation.

As national strategies are upgraded and the public places increasing emphasis on health needs, the pre-consultation market has emerged as a blue ocean. With various sectors crossing over into the healthcare field, the health management industry, boasting a broad consumer base, has become a fiercely contested battleground for enterprises.

Health management is an academic concept, a health philosophy, and now a national strategy incorporated into top-level design. Yet, at its core and in terms of commercial essence, it remains an industrial concept. With the widespread adoption and application of artificial intelligence and big data technologies in the health management industry, we can foresee that the era of personalized precision health management is drawing nearer.

In early 2017, the “Medium- and Long-Term Plan for the Prevention and Control of Chronic Diseases in China (2017–2025),” issued by the State Council, stated that support should be provided for the widespread adoption and application of new technologies and products, such as genetic testing, in the field of chronic disease prevention and control.Seen as a positive signal driving the development of the consumer-grade genetic testing industry. ButAs policy regulation lags behind the market, it will take time to validate the widespread application of genetic technologies in the field of health management. Whether consumer-grade genetic testing can become a driver for personal health management remains uncertain. However, with BGI Genomics leading the way through its IPO in 2017, the market may be signaling that more “players” are poised to capture a share of this industry.