Commercial Health Insurance in 2017: Accelerating Licensing, Product Launches, Channel Expansion, and Integration into Medical Services – Market Size to Exceed RMB 400 Billion

On November 15, the China Insurance Regulatory Commission (CIRC) released the “Administrative Measures for Health Insurance (Draft for Comments)” to solicit public opinions, marking the first revision since the previous version came into effect in September 2006.In terms of changes, the new Administrative Measures have added “medical accident insurance” as a new product category and set forth detailed requirements for the integration of health insurance with basic medical insurance, which will have a significant impact on the future development of the health insurance industry.

2017 was a pivotal year for the development of health insurance: the China Insurance Regulatory Commission proposed amendments to the administrative measures for health insurance; pilot programs for individually purchased tax-advantaged health insurance were rolled out nationwide; numerous insurance institutions invested in medical facilities; and short-term health insurance along with online enrollment channels gained prominence.

VCBeat (WeChat ID: vcbeat) reviews the achievements of health insurance in 2017 from the perspectives of policy, industry, and case studies, and looks ahead to future development trends.

Policy: Proposed Revision of Management Measures and Rollout of Multiple Pilot Programs

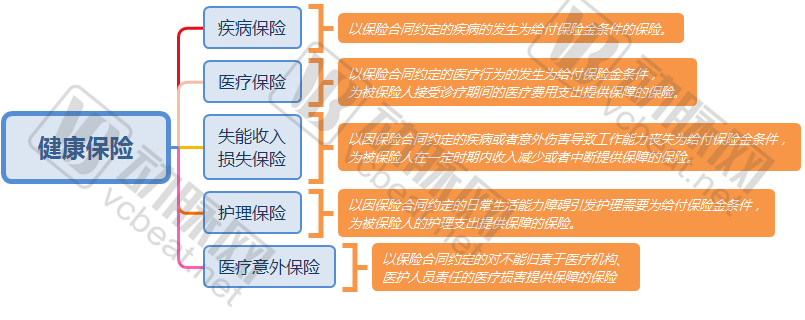

According to the “Health InsuranceManagementMeasures (Draft for Comments), health insurance includes disease insurance, medical insurance, disability income loss insurance, long-term care insurance, and medical accident insurance, etc.

Medical Accident Insurance is a newly added insurance product in this instance. It refers to insurance that provides coverage for the insured when unforeseen and unpreventable medical harm occurs, which cannot be attributed to the liability of medical institutions or medical personnel, as stipulated in the insurance contract.

In addition, the revised Administrative Measures have added provisions related to “Health Management and Cooperation with Medical Insurance,” including allowing the integration of health insurance products with health services to provide health risk assessment and intervention, as well as services such as disease prevention, health examinations, health consultations, health maintenance, chronic disease management, and wellness and healthcare, thereby reducing health risks and minimizing disease-related losses.

Meanwhile, insurance companies operating medical insurance should strengthen cooperation with healthcare service providers and health management service organizations, actively engage in the oversight of medical service practices, monitor the authenticity and legality of medical conduct, and provide recommendations on the reasonableness and necessity of medical expense expenditures. Insurance companies should proactively fulfill their role as a third party in the doctor-patient relationship, helping to alleviate information asymmetry and mitigate disputes between doctors and patients.

We believe that the revised “Administrative Measures for Health Insurance” sends a positive signal from regulators to promote the development of health insurance. The provisions integrating health insurance with health management and medical services align with the needs of commercial health insurance development and enrich the connotation of health insurance growth.

Other major policies also include:

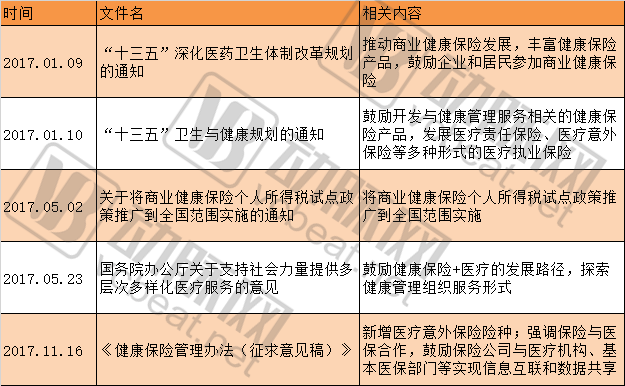

On May 2, 2017, the Ministry of Finance, the State Administration of Taxation, and the China Insurance Regulatory Commission jointly issued the “Notice on Expanding the Pilot Policy for Individual Income Tax Deductions on Commercial Health Insurance to a National Scale.” The notice pointed out that,Effective July 1, 2017, the pilot policy on individual income tax deductions for commercial health insurance was expanded to nationwide implementation.

According to the notice, expenditures incurred by individuals for purchasing compliant commercial health insurance products are allowed as pre-tax deductions when calculating taxable income for the current year (or month), with a deduction limit of RMB 2,400 per year (RMB 200 per month). Previously, the preferential individual income tax policy for health insurance had been piloted in 31 cities across China.

On May 23, 2017, the General Office of the State Council issued the “Opinions on Supporting Social Forces in Providing Multi-Level and Diversified Medical Services.” The document requires the implementation and improvement of insurance support policies, the enrichment of health insurance products, and the vigorous development of commercial health insurance that is orderly aligned with basic medical insurance. Meanwhile, commercial insurance institutions and health management institutions should be encouraged to jointly develop health management insurance products, strengthening health risk assessment and intervention.Support commercial insurance institutions and medical institutions in jointly developing insurance products targeting special-needs medical care, innovative therapies, advanced diagnostic and laboratory testing services, and the use of high-value medical devices.

2017 Health Insurance-Related Policies

In addition to national-level policies, many regions are currently piloting programs that allow the use of surplus funds from personal medical insurance accounts to purchase commercial health insurance. Pilot areas include Shanghai, Zhejiang, Fujian, and Hunan. Shanghai issued relevant documents in January this year, and the Changsha Municipal Government issued its documents in September this year.

It is also worth noting that the model of commercial insurance institutions participating in the management of medical insurance funds is being advanced, with models such as government procurement of services, entrusted management, and operational handling emerging, which also holds significant importance for the development of commercial health insurance.

The “13th Five-Year” Plan for Deepening the Reform of the Medical and Healthcare System stated, “Accelerate the separation of medical insurance administration from operation, and enhance the corporatization and professionalization of medical insurance agencies. Innovate service delivery models to foster a diversified competitive landscape.” This has created broader and deeper opportunities for commercial insurance to participate in the medical insurance system.

Overall, the 2017 policies related to health insurance or commercial medical insurance, building on previous pilot initiatives, placed greater emphasis on the coordination between commercial insurers, healthcare providers, and basic medical insurance schemes, with the aim of establishing a mutually complementary healthcare security system. This integration will be a key focus for the future development of the health insurance sector.

Industry: Diversification of Insurance Products and Distribution Channels, Accelerated Entry into Healthcare Services

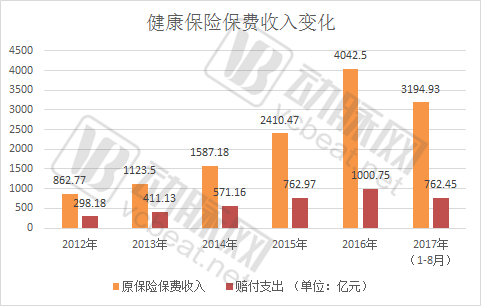

According to data from the Insurance Association of China, between 2010 and 2016, gross written premiums for commercial health insurance grew from RMB 69.172 billion to RMB 404.250 billion, a 4.8-fold increase; claims payments rose from RMB 26.402 billion to RMB 100.075 billion, a 2.8-fold increase. From January to August this year, the health insurance business recorded gross written premiums of RMB 319.493 billion, a year-on-year increase of 3.12%; claims and benefits paid amounted to RMB 76.245 billion, a year-on-year increase of 25.96%.

The expansion of the health insurance market has been driven by policy support, an increase in the number of health insurance companies, a more diverse range of products, and the development of online and other sales channels.

First, the pilot policy for individual income tax, based on data released at the routine press conference of the State Taxation Administration,In the first three quarters of this year, a total of 300,000 person-times claimed pre-tax deductions for commercial health insurance premiums., with significant policy effects.

During the same period,A variety of short-term, mid-to-high-end medical insurance products have also emerged in the market.For example, Pacific Insurance’s Tai Xiang e-Bao, Ping An Insurance’s Ping An e-Sheng Bao, and ZhongAn Insurance’s Zun Xiang e-Sheng. The premiums for such short-term health insurance products are around RMB 300, with low eligibility requirements and coverage limits reaching the million-yuan level. Due to their affordability, they have become the preferred choice for some health insurance policyholders.

In terms of sales and promotion, such products adopt an “internet model,” rapidly expanding through social and online channels. This approach not only drives product sales but also contributes to the popularization of health insurance.

In insurance operations, a model integrating health insurance with health management has emerged this year. For instance, policyholders with chronic conditions such as diabetes and hypertension can increase their coverage limits by uploading physiological data; metrics related to physical activity and the maintenance of key health indicators may also serve as criteria for coverage increases or incentives.

A small number of health insurance products have also incorporated health intervention and management, gradually establishing comprehensive health management systems that encompass data collection, analysis, evaluation and feedback, and intervention, thereby creating a closed-loop model of “health insurance + health management.” In terms of data collection methods, innovative medical devices, wearable devices, the Internet of Things (IoT), and internet technologies are being applied.

At the industry level, the “insurance + healthcare” model also deserves attention.Insurance companies have gained experience in exploring managed care health insurance by entering the healthcare services sector through investments, acquisitions, and new ventures.

Take Sunshine Fusion Hospital, a large Grade A tertiary hospital jointly established by Sunshine Insurance Group and the Weifang Municipal Government, which has been in operation for one year as of this year. According to its publicly released data, the hospital has achieved positive results in discipline construction, health service models, and management practices. In integrating health insurance with medical care, Sunshine Insurance has developed several practical commercial health insurance products based on clinical pathways, participating in the medical service delivery process. This approach has provided valuable insights into the design of health insurance products, claims settlement models, and management frameworks.

Taikang Insurance is another strong proponent of the “insurance + healthcare” model. In June this year, Taikang Xianlin Gulou Hospital, a Grade-A tertiary hospital under Taikang Insurance Group, completed its name change. Alongside the renaming, the hospital will leverage internet-based solutions to provide chronic disease intervention, health management, and rehabilitation services to its affiliated senior living communities.

Previously, Taikang had already made significant investments in the elderly care industry, establishing senior living communities in first-tier cities such as Beijing, Shanghai, Guangzhou, Shenzhen, and Hangzhou, with a cumulative scale of 1.3 million square meters and 13,000 households.

Elderly care services are increasingly becoming a standard offering among insurers. Companies such as China Life, New China Life Insurance, Taiping Life, and Taikang Insurance have all invested in senior living communities, participating in the operation of elderly care and rehabilitation hospitals and communities through equity investments, debt financing, and industrial funds.

Insurance capital and healthcare exhibit strong symbiosis. By participating in the operation of medical institutions, health insurance companies can gain a comprehensive understanding of medical service delivery processes and develop insurance products tailored to patient needs—a model successfully explored by Sunshine Insurance. For hospitals, collaboration with insurers helps optimize internal governance and refine cost-control systems.

In addition, medical accident insurance and medical liability insurance have also seen significant popularity this year. Industry insiders told VCBeat that many private medical institutions, particularly clinics operated by individuals, have a strong willingness to purchase medical liability insurance, as it can effectively serve the economic compensation function of insurance and provide a certain level of protection for individual entrepreneurs in the healthcare services sector. Furthermore,With the rise of physician groups and independent medical practice, the future potential of medical liability insurance will be gradually unlocked.

Trend: Health Insurance to Enter an Era of Rapid Growth

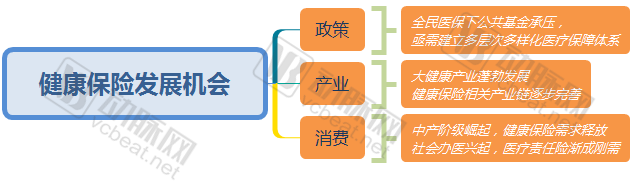

Driven by policy guidance and proactive industry initiatives, the health insurance market is poised for explosive growth. According to securities research reports, the scale of China’s commercial health insurance sector is projected to reach RMB 500–700 billion within five years, establishing it as one of the three major business segments alongside property and casualty insurance and life insurance.

The fundamental condition for the surge in health insurance lies in its alignment with the space for institutional reforms in medical insurance. From a holistic perspective of China’s healthcare security system, the government-led insurance framework comprises three tiers: basic medical insurance, medical assistance, and critical illness insurance. Under the universal health coverage model, the immense expenditure pressure on medical insurance funds has necessitated strict control over the scope of benefits, imposing rigorous restrictions on the drug formulary, covered diagnostic and treatment procedures, and the list of reimbursable medical facilities and equipment.

From the perspective of actual changes in health expenditure, the growth rate of domestic medical expenses in recent years has exceeded the rate of fundraising for public medical funds. Under the condition of universal health coverage, increases in funding can only rely on a substantial rise in contribution levels, which is not realistic in the short term.Therefore, commercial health insurance will partially assume the functions of medical insurance, serving as a supplement to the basic medical insurance system.

In tandem with adjustments to the medical insurance system, the rise of the middle class has stimulated the willingness to purchase commercial health insurance. According to McKinsey’s projections, 76% of Chinese urban households will have reached middle-class income levels by 2022. Among the consumption preferences of the middle class, spending related to “health status” is highly prioritized.

From the perspective of development trends in the health and wellness sector, the industry is poised for comprehensive growth over the next five years. Top-level planning projects that the health and wellness industry will reach a scale of 8 trillion yuan by 2020, which will also create opportunities for the development of commercial health insurance.

Early domestic players in the health insurance sector include PICC Health, Ping An of China, Kunlun Health Insurance, Hexie Health Insurance, and CPIC-Allianz. PICC Health and Hexie Health are market leaders, with Hexie Health commanding the largest market share and annual gross written premiums exceeding RMB 30 billion.

In addition to traditional giants, new entrants are continuously flooding the market. In January this year, the China Insurance Regulatory Commission (CIRC) officially approved the opening of Fosun United Health Insurance Company. Following Fosun United Health, Ruihua Health Insurance was approved for preparatory establishment, marking the beginning of an expansion in the number of health insurance companies.

According to market information, China Life Insurance, Sunshine Insurance Group, Kangmei Pharmaceutical, Neusoft Corporation, and Meinian Onehealth are currently applying for specialized health insurance licenses, with more than 50 institutions having submitted applications overall.

Despite the enthusiasm of new entrants, the health insurance market faces pressing challenges that require urgent resolution. First, there is a lack of product innovation, with severe homogenization among insurance offerings, making it difficult to meet policyholders’ needs. Second, the level of specialization is insufficient; actuarial systems remain underdeveloped, leading to significant operational risks and causing many companies to operate at a loss. Finally, no effective business model has yet emerged. Although attempts have been made in health management, medical services, and medical insurance fund administration, these efforts have not established robust operational frameworks or data support, lacking long-term sustainability.

In summary,The opportunity for the development of health insurance lies in deep integration with healthcare services, leveraging disease-specific data and clinical data to establish more refined and accurate actuarial standards, enriching the portfolio of insurance products, and comprehensively meeting the needs of policyholders across diverse populations and varying requirements.

Furthermore, it should be emphasized that the integration of health insurance with the Internet creates greater opportunities, including combinations such as pharmaceutical e-commerce plus insurance, online healthcare plus insurance for diagnosis, treatment, and disease management, as well as models leveraging internet technology for process control and precise cost containment.

Overall, the development of health insurance aligns with the evolving trajectory of national healthcare security needs. Its integration with medical services and the internet represents an inherent demand, and the potential of health insurance will be gradually unlocked in the future.