Pharmaceutical Retail in 2017: Benefiting from Separation of Medical Services and Drug Sales, Surge in Prescription Outflow, and Rising Market Consolidation

Pharmaceutical retail is a low-frequency, high-spending industry. Benefiting from the development of the broader health sector and opportunities arising from healthcare and pharmaceutical system reforms, its market size continues to expand. However, from an industry perspective, challenges such as fragmentation, disorderly competition, low market concentration, and limited professionalization persist.

In 2017, the pharmaceutical retail industry witnessed a flurry of policy developments, including the separation of prescribing from dispensing, the outflow of prescriptions from hospitals to retail pharmacies, and the expansion of electronic prescription pilots. At the industrial level, Dashenlin successfully completed its initial public offering (IPO), while Shuyu Civilian Pharmacy and Jianzhijia sequentially disclosed their prospectuses, marking the second wave of listings among chain pharmacy enterprises. Meanwhile, regional chain leaders such as Quanyi Health and Huakang Pharmaceutical received investments from industrial capital, facilitating regional consolidation...

VCBeat (WeChat ID: vcbeat) reviews the development and changes in the pharmaceutical retail industry in 2017 from the perspectives of policy, industry, and capital, and looks ahead to the future evolution trends of the pharmaceutical retail sector.

Policy: Multiple Tailwinds, Tighter Regulation

In 2017, the pharmaceutical retail industry benefited from multiple favorable factors, including the advancement of comprehensive reforms in public hospitals, the accelerated separation of prescribing from dispensing, and the expanded outflow of prescriptions. Meanwhile, the pharmaceutical retail sector entered an era of “strict regulation.” Following the abolition of GSP (Good Supply Practice) certification, unannounced inspections became frequent, making industry oversight more scientific and routine.

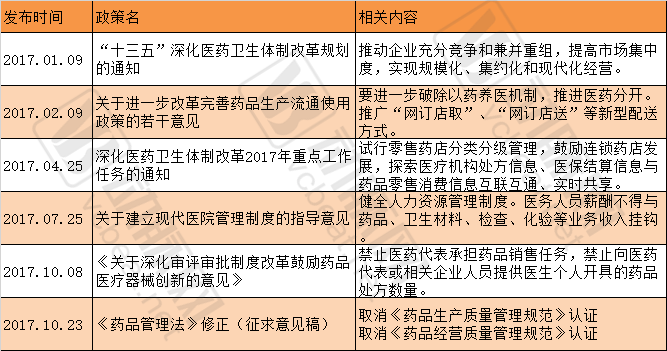

At the beginning of this year, the General Office of the State Council issued the “Several Opinions on Further Reforming and Improving Policies for Drug Production, Circulation, and Use” (hereinafter referred to as “Document No. 13”), setting the main tone for policy evolution in the pharmaceutical retail industry this year. Document No. 13 states that efforts should be made to further dismantle the mechanism of subsidizing healthcare with drug profits and to promote the separation of prescribing from dispensing. Outpatients shall have the autonomy to choose whether to purchase medications at medical institutions or retail pharmacies; medical institutions shall not restrict outpatients from purchasing drugs at retail pharmacies with prescriptions. Where conditions permit, exploration may be undertaken to separate outpatient pharmacies from medical institutions. Meanwhile, the initiative of “Internet + Drug Circulation” will be advanced, promoting new distribution models such as “online ordering with in-store pickup” and “online ordering with home delivery.”

Subsequently, the “Key Tasks for Deepening the Reform of the Medical and Healthcare System in 2017” stated that pilot programs for classified and graded management of retail pharmacies should be implemented, the development of chain pharmacies should be encouraged, and interconnectivity and real-time sharing of prescription information from medical institutions, medical insurance settlement information, and drug retail consumption information should be explored.

The progressive nature of the policies also reveals that regulators aim to achieve the separation of prescribing and dispensing by facilitating the outflow of prescriptions. The first step is to incentivize hospitals and remove barriers to prescription outflow, thereby enabling patients to decide independently where to purchase their medications. The second step involves enhancing patient convenience at social pharmacies and through other channels via measures such as integration with medical insurance systems and interoperability of prescription information, thereby creating a substantive “diversion” away from hospital pharmacies.

Regarding the pilot programs for electronic prescriptions, in addition to the “ice-breaking” regulatory advancements at the national level, local pilots have taken the lead. For instance, in May this year, the Xi’an Food and Drug Administration issued the *Work Plan for Promoting Electronic Prescription Services by Drug Retail Enterprises (Trial)*, intending to implement electronic prescription services among chain drug retailers and qualified standalone retail pharmacies in the city.

Prior to the Xi’an Food and Drug Administration’s initiative, the Chengdu Food and Drug Administration had already launched a pilot program for electronic prescriptions in retail pharmacies across the city last September. According to data from the Chengdu FDA, the cumulative number of various prescriptions exceeded 500,000 by the end of last year.

Since the launch of “healthcare reform,” “separating medicine from medical services” has been a key focus. The objective of this separation is to exclude drug revenues from the income of medical institutions, sever the direct financial ties among drug tendering and procurement processes, medical institutions, healthcare professionals, pharmaceutical companies, and drug distributors, and establish a system in which clinical diagnosis and treatment operate independently from medication prescribing.

Under this overarching premise, a series of policies—including zero markup on drug sales, the separation of prescribing and dispensing, and electronic prescriptions—have been progressively implemented, with pharmaceutical retail gradually replacing hospitals as the primary channel for drug distribution.

The policy direction of "separating prescribing from dispensing" is expected to continue in the future. Benchmarking against developed countries in Europe and the United States, over 90% of patients in Europe obtain medications through retail pharmacies, and more than 80% of drugs in the U.S. are sold via retail pharmacies. In contrast, the current ratio between hospital and retail channels in China is approximately 7:3, indicating that there is still a long road ahead for reform.

Relevant Policies for Pharmaceutical Retail in 2026

Industry: Embracing Capital, with M&A Integration as the Main Theme

At the industry level, the most prominent events in the pharmaceutical retail sector this year have been the attempts by several leading chain enterprises to enter the capital markets, as well as the initiation of mergers, acquisitions, and cross-regional expansion by regional leaders, bolstered by capital support.

On July 31, Dashenlin was officially listed on the Main Board of the Shanghai Stock Exchange. After entering the capital market, its market capitalization once exceeded RMB 20 billion, making it the “first stock in pharmaceutical retail.”

On November 4, Dashenlin announced that it plans to invest no more than RMB 75 millionAcquisition of relevant assets and equity interests in Fujian Guosheng Pharmaceutical Chain Co., Ltd., which operates more than 50 pharmaceutical retail stores; following Dashenlin’s listing, the effects of industrial integration have become prominent.

Following Dashenlin, Shuyu Civilian Pharmacy and Jianzhijia have also disclosed their initial public offering (IPO) prospectuses, marking a wave of listings for retail pharmacy chains this year. Previously, Yixintang, Laobaixing, and Yifeng had already entered the capital market as pharmaceutical retail stocks. As a niche segment within the pharmaceutical and biotechnology industry, pharmaceutical retail is continuing to grow and expand.

This year, these listed companies share a common trait: expansion. Taking Yixintang as an example, the number of its stores stood at 4,085 at the end of last year; by the time its semi-annual report was disclosed this year, it had 4,713 stores. This represents an increase of nearly 700 stores in just six months, equivalent to adding 2–3 stores per day.

Yixintang’s primary expansion strategy has been mergers and acquisitions (M&A). According to its public announcements, the company’s store count nearly doubled after its initial public offering (IPO). The main targets of Yixintang’s M&A activities are independent pharmacies and small pharmacy chains, with a regional focus on Sichuan, Guangxi, Chongqing, and other areas.

Yixintang’s expansion strategy centers on deepening its presence in Yunnan Province and focusing on the Sichuan-Chongqing region. With over 3,000 stores in Yunnan, the company has achieved high consumer awareness and brand recognition. Following its initial public offering, it leveraged the capital-raising capabilities of the public markets to sustain its merger and acquisition momentum.

Currently, Yixintang has maintained stable profit levels during its ongoing M&A activities, indicating that newly acquired stores have not experienced significant performance fluctuations, with their subsequent profitability expected to be gradually realized.

While Yixintang’s revenue and profitability are comparable to those of Laobaixing Pharmacy, the latter has maintained a higher return per store. A comparison shows that in the first half of this year, Yixintang generated RMB 3.651 billion in revenue and RMB 216 million in net profit, whereas Laobaixing reported RMB 3.454 billion in revenue and RMB 191 million in net profit. Notably, however, Laobaixing operates only 1,924 directly-owned stores, less than half the number operated by Yixintang. In the first half of this year, Laobaixing Pharmacy added 101 new stores through a combination of self-built outlets and mergers and acquisitions.

Overall, the four listed companies primarily engaged in pharmaceutical retail each exhibit distinct operational characteristics. Yixintang, Laobaixing, and Dashenlin have relatively comparable revenue and profit levels, with Yifeng Pharmacy trailing slightly behind. In terms of expansion strategies, all adopt a combination of organic and inorganic growth, though they differ in their primary strategic focuses and geographic footprints.

Overall, Yixintang is deeply rooted in Yunnan and focused on Sichuan and Chongqing; Laobaixing is concentrating its efforts on the Central-South region; Yifeng excels in refined management; Dashenlin, newly listed, will leverage its IPO advantages to intensify its market presence. In the future, the four publicly listed companies will continue to dominate their respective regions, resulting in a fragmented regional landscape across China.

Beyond the strategic moves of already-listed companies, some regional industry leaders are also embarking on capital operations and mergers and acquisitions.

On October 31, Quanyi Health announced that it had secured a Series B financing round amounting to billions of yuan, which may pave the way for large-scale expansion. Established in April 2016, Quanyi Health is a retail pharmacy management platform that has previously integrated multiple small chain pharmacies in Jiangsu, Zhejiang, Hebei, and other regions. Its sales volume is projected to exceed RMB 6 billion in 2017.

Earlier, Xi'an Yikang Pharmaceutical, the leading pharmaceutical retail chain in Shaanxi Province, secured a Series B financing round worth hundreds of millions of yuan from Huakang Fund, with plans to expand its store count to 1,500 by 2018.

The above represents two pathways for consolidation by regional leaders: one involves establishing a management platform through capital investment to acquire small and medium-sized chains; the other entails leading regional M&A consolidation by securing external financing. Driven by cost advantages, economies of scale, and policy incentives, M&A consolidation in the pharmaceutical retail industry will continue, becoming the dominant theme in the near future.

TrendTrend: The market size continues to expand, and competition intensifies

The pharmaceutical retail industry is a low-frequency, high-margin, and low-concentration consumer sector.

In terms of purchase frequency, retail pharmacies receive approximately 50 customers per day, which is lower than convenience stores, supermarkets, and other retail outlets. Regarding profit margins, the average profit margin in pharmaceutical retail stands at around 30%, with large chain pharmacies achieving margins as high as 40%. In terms of market concentration, the revenue concentration of directly operated stores among China’s top 100 retail pharmacy chains is only about 20%, significantly lower than the levels observed in developed countries.

Upon closer examination, each of the aforementioned characteristics has its underlying causes. The low purchase frequency stems from the fact that pharmacies primarily sell pharmaceuticals (accounting for approximately 70% of sales), as medication consumption is not a high-frequency demand. The high profit margins arise from the specialized nature of pharmaceutical products, which creates certain entry barriers and allows for a premium on professional services.

Low market concentration is driven by multiple factors, with stringent regulation and local protectionism being the primary causes. Prior to 2000, retail pharmacies in China were typically embedded within the traditional pharmaceutical distribution system, dominated by state-owned sales stations. After 2000, the emergence of low-cost, large-scale supermarket-style models propelled the pharmaceutical retail sector into a phase of rapid market-oriented growth. Meanwhile, stringent regulation and local protectionism have accompanied this development. As part of the healthcare sector, retail pharmacies are subject to oversight by multiple authorities, including health administration, food and drug supervision, industry and commerce administration, and medical insurance systems. Cumbersome policies regarding taxation and administrative approvals have further restricted the cross-regional expansion of retail pharmacies.

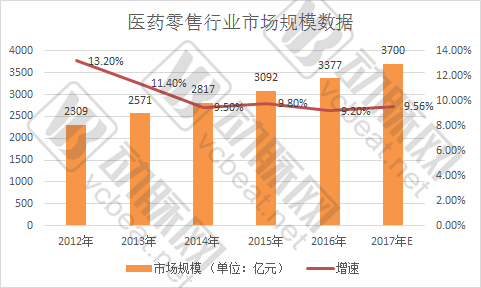

In recent years, both the market size and market concentration of the pharmaceutical retail industry have been increasing. According to data from Zhongkang CMH, the market size of pharmaceutical retail reached RMB 337.7 billion last year, maintaining an average annual growth rate of nearly 10% over the past three years. Based on this trend, it is projected that the market size of the pharmaceutical retail industry will exceed RMB 370 billion in 2017.

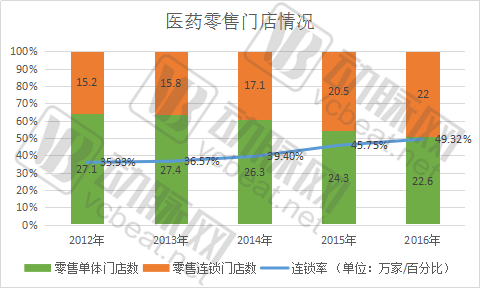

According to the statistical bulletin released by the China Food and Drug Administration, the pharmaceutical retail industry has undergone a trend of “decline in independent stores and rise in chain stores” over the past five years. While the total number of retail outlets increased by only about 20,000, the number of chain store locations grew by nearly 70,000. Meanwhile, approximately 50,000 independent retail pharmacies disappeared from the market. Most of these vanished independent stores were acquired and integrated by industry leaders, as exemplified by the mergers and acquisitions involving Yixintang, Laobaixing, Quanyi, and Huakang, among others.

Data Source: Statistical Bulletin of the China Food and Drug Administration; 2016 data are as of November.

It is worth noting that the density of retail pharmacies in China is already very high. Based on 2016 data, with a population of 1.375 billion and 446,000 stores, the ratio was approximately 3,082 people per store, whereas the “saturation standard” in developed countries is 2,500 people per store. This implies that, barring significant changes in population size, opening new stores will not be the primary mode of entry into the pharmaceutical retail sector in the future.

In terms of market concentration, data from the Ministry of Commerce shows that in 2016, the top 100 pharmaceutical retail enterprises in China operated a total of 54,300 stores, accounting for 12.2% of the national store count; their sales revenue reached RMB 107 billion, representing 29.1% of the total retail market share; and the combined market share of the top three retail enterprises was only 6.7%. In contrast, U.S. data indicates a chain store penetration rate of approximately 75%, with the top three enterprises holding over 80% of the total market share. There remains significant room for improvement in China’s chain store penetration rate and market concentration.

Recent policies have also facilitated the increase in industry concentration. For instance, the “Development Plan for the Pharmaceutical Distribution Industry (2016–2020)” stated that the chain pharmacy rate should exceed 50% by 2020. Meanwhile, an increasingly stringent regulatory and industrial environment has made independent and small-scale chain pharmacies more willing to join forces with industry giants, with franchising or being acquired becoming highly cost-effective options. All these factors will contribute to higher industry concentration.

Ultimately, it should be recognized that the “Internet + Healthcare” model holds immense potential. The integration of the internet with pharmaceutical distribution and the rise of online pharmacies are gaining acceptance within the industry and will also reshape the landscape of pharmaceutical retail.

For instance, the B2B pharmaceutical e-commerce sector has approached a scale of nearly RMB 100 billion, and is poised to unlock greater potential against the backdrop of supply chain finance and industrial consolidation. The rise of online pharmacies, which have already reached a market size of tens of billions of RMB, is directly impacting pharmaceutical retail. The new pharmaceutical retail model featuring “online ordering with in-store pickup” and “online ordering with home delivery” is also gaining traction, demonstrating a significant reshaping effect on the industry. This year, the State Council issued a document abolishing the qualification review for pharmaceutical e-commerce operators. It is anticipated that more players will enter the “Internet + Healthcare” space, further accentuating the disruption and transformation within the industry.

In summary, pharmaceutical retail remained a highly coveted “lucrative business” in 2017, with continuous favorable developments in policy, capital, and industry sectors driving industrial transformation and reshaping. The high growth trajectory of the pharmaceutical retail industry is expected to persist.

If you are following “pharmaceutical distribution,” you are welcome to register for the event to be held in Beijing from December 15–17.“2017 Top 100 Future Healthcare” Forum, we will establish a dedicated“Parallel Forum on Pharmaceutical Distribution”, inviting renowned industry experts and multiple corporate executives to explore how policies, new technologies, and e-commerce are influencing the pharmaceutical distribution sector. Long-press the image below to scan the QR code and register.