E-Pharmacy in 2017: Prescription Drug Sales Halted Online, 'E-commerce + Healthcare' Emerges, and Prescription Diversion Becomes New Growth Driver

In 2017, the pharmaceutical e-commerce sector entered a year of opportunity. On the policy front, the sequential cancellation of the ABC license reviews further lowered entry barriers for pharmaceutical e-commerce. In terms of capital, hot money flowed into the sector, with more than ten companies securing financing throughout the year, totaling nearly RMB 1 billion. At the business level, the application of new technologies drove continuous innovation, giving rise to new models such as online-offline synergy and the integration of medical services with e-commerce. Pharmaceutical e-commerce is transitioning from single-function online pharmacies and internet-based pharmaceutical wholesale toward becoming diversified health service providers.

Take a Long-Term View. Currently, the pharmaceutical e-commerce industry is in a phase of rapid development and change; it is essential to clearly identify existing opportunities and advance the integration of “Internet Plus” with healthcare.

VCBeat (WeChat ID: vcbeat) reviewed the development and changes in the pharmaceutical e-commerce industry in 2017 from the perspectives of policy, industry, capital, and innovative cases, analyzing the opportunities and trends in its growth.

Policy: Lowered Barriers, Stricter Regulation

The pharmaceutical industry is a “policy-driven market,” and this is even more true for the online pharmaceutical e-commerce sector. Since the promulgation of the Interim Provisions on the Approval of Internet Drug Transaction Services in 2005, policies governing pharmaceutical e-commerce have undergone repeated reversals, including a temporary suspension of pilot programs for third-party online retail of drugs, which at the time plunged the sector into a “deep freeze” in its development.

As the 13th Five-Year Plan entered its inaugural year, the pharmaceutical e-commerce sector witnessed multiple rounds of deregulation. First, the Class B and Class C licenses for pharmaceutical e-commerce were abolished, thereby granting approval to online pharmacies. Next, new delivery models such as “online ordering with in-store pickup” and “online ordering with store-based delivery” were encouraged to foster innovative services and business formats. Subsequently, various regions launched pilot programs for electronic prescriptions and the outflow of prescriptions from hospitals, creating opportunities for the “Internet Plus Healthcare” model. Finally, even the highly coveted Class A license was abolished, marking the comprehensive deregulation of pharmaceutical e-commerce.

Of course, while regulations are being relaxed, oversight of pharmaceutical e-commerce remains stringent. Requirements include strengthening Good Manufacturing Practice (GMP) and Good Supply Practice (GSP) certifications, exercising strict control over enterprises providing online drug transaction services, ensuring the fulfillment of primary responsibilities, establishing an online information disclosure system to facilitate public inquiries, and implementing a “blacklist” system. Crackdowns on illegal online drug sales will be intensified, and the red line prohibiting the online sale of prescription drugs must not be crossed.

Following this round of deregulation, the pharmaceutical e-commerce industry has entered an era characterized by "lenient market entry but strict oversight." Regulatory supervision of pharmaceutical e-commerce enterprises will become more scientific and routine. The extensive management model, under which a single license granted perpetual validity, is now a thing of the past, replaced by dynamic, normalized regulation with enhanced supervisory effectiveness.

Furthermore, the core policy logic to be grasped is “encouragement.” As mentioned in the “13th Five-Year Plan for Deepening the Reform of the Medical and Healthcare System,” it is necessary toPromote the transformation of distribution enterprises into smart pharmaceutical service providers, and promote the application of modern logistics management and technology; “Document No. 13” also mentions that it is necessary toSupport pharmaceutical distribution enterprises in strengthening cooperation with the internet, promoting the integrated development of online and offline channels, and fostering new business models.

Currently, China’s pharmaceutical distribution and retail sectors continue to face challenges characterized by fragmentation, disorganization, and uneven development, failing to fully meet drug supply demands and residents’ healthcare needs. It is essential to further enhance industry consolidation and service quality by cultivating large, leading enterprises with advantages in scale, technology, and service. The “Internet+” model serves as an effective channel and approach. Consequently, policies have strongly encouraged the integration of “Internet+” into the pharmaceutical sector, aiming for the industry to leverage new technological tools such as the internet to improve service capabilities and standards, thereby achieving industry consolidation and upgrading.

From the perspective of policy barriers, the model of “prescription drugs + e-prescriptions + online medical insurance payment” remains the ceiling constraining the development of pharmaceutical e-commerce, particularly online pharmacies.

On November 14, the China Food and Drug Administration released the “Measures for the Supervision and Administration of Online Pharmaceutical Operations (Draft for Comments),” which stipulates thatThe scope of online drug sales shall not exceed the scope permitted under the enterprise’s Drug Operation License. If the operator is a drug manufacturer or wholesaler, it shall not sell drugs to individual consumers. If the operator is a chain drug retailer, it shall not sell prescription drugs or drugs subject to special state management requirements through online channels.Websites selling pharmaceuticals to individual consumers are prohibited from publishing information on prescription drugs online. This regulation may have a significant impact on the current pharmaceutical e-commerce sector, particularly for online pharmacies. The online sale of prescription drugs remains a Sword of Damocles hanging over the pharmaceutical e-commerce industry.

Due to safety concerns, the online sale of prescription drugs has long remained restricted, while national oversight and penalties for such activities have been steadily intensified. However, it is important to recognize that online sales of prescription drugs not only meet consumers’ practical needs and provide convenience but also stimulate a substantial market, creating opportunities for industry growth. Therefore, under the premise of ensuring regulatory compliance, authorities have launched pioneering pilot programs, with electronic prescriptions emerging as a particularly significant direction.

For instance, both Chengdu and Xi’an have rolled out pilot policies for electronic prescriptions. In Chengdu’s pilot program, over 500,000 e-prescriptions have been issued, benefiting more than 3,000 pharmacies in the city and tens of thousands of patients. Companies such as Wuzhen Internet Hospital, WeChat, and Ali Health are also actively facilitating the external circulation of electronic prescriptions beyond hospitals, partnering with retail pharmacies and pharmaceutical e-commerce platforms.

Against the backdrop of abolishing the “drug-revenue-dependent” hospital financing model, the future trend will see prescriptions increasingly fulfilled outside hospitals, creating opportunities for pharmaceutical e-commerce.

Online Medication Purchasing via Medical Insurance and Electronic PrescriptionsThe situation regarding online medication purchasing through medical insurance is similar to that of electronic prescriptions. Although there are no explicit market access regulations, supportive policies have already been introduced. For instance, the “Internet + Human Resources and Social Security” 2020 Action Plan states that human resources and social security authorities will collaborate with third-party payment platforms such as WeChat and Alipay to establish a unified and open data exchange interface for medical insurance settlements. Under safe and controllable conditions, this initiative will support relevant institutions in launching applications such as online medication purchases. It is reasonable to believe that, under standardized pilot programs, online medication purchasing will be gradually expanded.

In summary, it is essential to clarify the two main thrusts of regulatory authorities regarding pharmaceutical e-commerce: one is to promote the integration of “Internet Plus” with pharmaceuticals, guiding industry transformation and upgrading; the other is to effectively safeguard consumer interests, ensuring the safety of pharmaceutical distribution and medication use. Under these two overarching themes, while policies may experience fluctuations, the broad direction remains certain: “Internet Plus” represents a key opportunity for the development of the pharmaceutical distribution industry.

2017 Policies Related to Pharmaceutical E-commerce

Industry: New Business Models Emerge, and Business Boundaries Dissolve

This year, we are pleased to observe that pharmaceutical e-commerce enterprises are no longer confined to online wholesale and retail of drugs; instead, they are actively exploring new models such as internet healthcare, O2O (online-to-offline), new retail, supply chain services, and smart healthcare.The integration of pharmaceutical e-commerce with medical services and pharmaceutical supply chain services is becoming increasingly evident, leading to deeper penetration across the industry value chain., we will find the answers from innovative cases below.

First came the “healthcare + pharmaceuticals” model of pharmaceutical e-commerce. This year, pharmaceutical e-commerce platforms such as Ali Health, Jianke, and Qilekang have all made attempts in the healthcare services sector.

Alibaba Health’s healthcare initiatives include: in March, acquiring a stake in Wanli Cloud to build a large-scale medical imaging platform; in April, co-establishing Hubei Province’s first provincial-level internet hospital with Wuhan Central Hospital, driving the hospital’s transformation into a smart hospital; in July, officially launching the medical AI product “Doctor You,” leveraging technology to empower healthcare; and in August, unveiling the Changzhou Blockchain Medical Consortium, applying blockchain technology to the underlying technical architecture of the medical consortium...

As Alibaba Group’s flagship platform in the healthcare sector, AliHealth’s core businesses include pharmaceutical e-commerce, smart healthcare, product traceability, and health management. Its objective is to build a comprehensive platform and infrastructure, making its every move a benchmark for the industry.

Jianke, one of the earliest pharmaceutical e-commerce platforms to emerge in China, has extensively expanded its offline presence this year. In March, it completed the acquisition of Guangzhou Jingtai Hospital to explore the internet hospital model and accommodate the outflow of prescriptions. In June, it announced the acquisition of Wuhan Xiongchu Integrated Traditional Chinese and Western Medicine Hospital, officially established its Southwest Center in Chongqing, planned to build an “Internet + Chronic Disease Management” hospital, signed an agreement with the Qionghai Municipal Government in Hainan Province, and launched the International Cloud Hospital project in Boao Lecheng. In September, it acquired Hangzhou Chang’an Hospital, extending its medical footprint into East China.

Not only medical institutions, but Jianke also strengthens its offline physical presence through pharmacies and DTP (Direct-to-Patient) pharmacies. The logic behind Jianke’s reinforcement of offline operations is that only by integrating online and offline services can it comprehensively meet the diverse needs of consumers, provide high-quality medical services and pharmaceutical supplies, and build a closed-loop “smart healthcare service” ecosystem.

Qilekang is also actively expanding its medical services portfolio. In June this year, Qilekang announced the launch of the “1 Billion Yuan Doctor Entrepreneurship Fund,” which provides a range of support—including funding, workspace, and staffing—to physicians practicing on the Qilekang Internet Hospital. This initiative aims to help doctors access richer entrepreneurial resources, facilitate a smoother transition into independent practice, and maximize their professional value. As the largest entrepreneurship support program for physicians in the mobile health sector, this move is expected to aid Qilekang in continuously expanding its network of connected physicians.

Pharmaceutical e-commerce companies are racing to establish a foothold in the healthcare sector, driven by both business development imperatives and profit motives.The inherent correlation between medicine and pharmaceuticals is causing the boundaries between internet healthcare and pharmaceutical e-commerce to disappear, as business models aimed at meeting consumer demand are being established.

Some companies have also ventured into new models such as O2O, New Retail, DTP (Direct-to-Patient), and prescription sharing. In the O2O sector, KuaiFang SongYao released its smart pharmacy system in June, aiming to provide retail pharmacies with IT solutions and delivery services to “empower” them, while launching a nationwide expansion plan. Dingdang Kuaiyao introduced AI robots, intelligent medication vending machines, and its Smart Pharmacy 3.0 system in August, and unveiled its “Smart Pharmacy.”

“New Retail” is also a key focus area for pharmaceutical e-commerce platforms. By leveraging big data analytics to uncover consumer needs and purchasing tendencies, and employing strategies such as product bundling and personalized recommendations, these platforms can effectively identify consumer demand while significantly boosting platform traffic and user stickiness.

Overall, by leveraging new technologies and extensively expanding their online and offline presence, pharmaceutical e-commerce companies are seeing the boundaries of their business disappear, with a clear trend toward the integration of various business formats.

Trend: Market Size to Exceed RMB 100 Billion, with the Strong Getting Stronger

Fueled by multiple favorable policies and industry conditions, coupled with active exploration and breakthroughs by companies within the sector, the pharmaceutical e-commerce industry is poised to exhibit the following trends: continuous expansion of market scale, increased concentration with a “the strong get stronger” dynamic; enhanced specialization and deeper penetration into healthcare services; differentiated e-commerce platforms focusing on chronic diseases and novel specialty drugs will thrive; and online-offline integration will blur business boundaries.

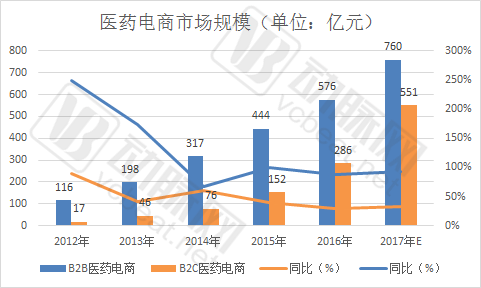

First, let us examine the market size. According to data from the Market Order Department of the Ministry of Commerce, the total sales revenue of pharmaceutical e-commerce enterprises under direct reporting reached RMB 61.2 billion in 2016. Among this, B2B business sales amounted to RMB 57.6 billion, while B2C business sales totaled RMB 3.6 billion. Additionally, data from Choice indicates that the scale of B2C pharmaceutical e-commerce was RMB 28.6 billion in 2016.

In terms of growth, the B2B pharmaceutical e-commerce sector has achieved a compound annual growth rate (CAGR) of 40% over the past five years, with the transaction volume expected to reach RMB 76 billion in 2017. The B2C pharmaceutical e-commerce sector has recorded a CAGR of over 100% in the same period, with its 2017 transaction volume projected to exceed RMB 50 billion. Overall, the total scale of China’s pharmaceutical e-commerce market is anticipated to surpass RMB 100 billion in 2017.

Data sources: Department of Market Order, Ministry of Commerce; Choice; VCBeat

From the perspective of market share, although the barriers to entry for pharmaceutical e-commerce have been lowered and the number of new entrants has increased, top-tier traffic remains dominated by established platforms. The trend toward market consolidation is evident, with leading players continuing to strengthen their dominance.

Major platforms such as Alibaba and JD.com have both launched self-operated businesses. Alibaba has integrated the revenue from its Tmall Pharmacy channel and established the AliHealth Pharmacy; JD.com operates self-run pharmacies, pharmaceutical wholesale, and O2O pharmaceutical services, and recently announced plans to recruit physicians and build an internet hospital.Full-Scale EntryPharmaceutical Business.

Apart from Alibaba and JD.com, most other pharmaceutical e-commerce platforms have listed company backing, including Jointown Pharmaceutical Group’s Haoyaoshi, Taiantang’s Kangaiduo, and Renhe Pharmacy Network under Renhe Pharmaceutical. These pharmaceutical e-commerce platforms established by large corporations benefit from resource advantages, entered the market early, and have already secured a certain market position; they are expected to continue dominating the market in the future.

Even for non-listed companies, those that started early and have already been validated by the market are more likely to attract capital. According to our statistics, as of Q3 2017, there were 13 financing events in the pharmaceutical e-commerce sector, with a total financing amount of approximately $127 million, which was only half of the previous year’s figure (in the previous year, there were 10 financing events in the pharmaceutical and health sector, with a total financing amount of $267 million).

Based on the companies that secured funding this year, financing rounds were concentrated at Series A and beyond—including Jianke, Qilekang, Sinopharm Online, and Yaoshibang—with large amounts accounting for over 98% of the total funding. Very few newly established companies emerged; the three new startups—Didu Technology, Yilian Technology, and Taoshe Life—raised a combined total of only $4 million. These data indicate that,Entrepreneurship in the pharmaceutical e-commerce sector has entered its latter half, with capital increasingly favoring the cultivation of unicorns over angel investing.。

2017 Financing in the Pharmaceutical E-commerce Sector

In terms of enhanced specialization, this is mainly reflected in medical services. As previously mentioned, many pharmaceutical e-commerce companies have begun to venture into the healthcare sector. Conversely, numerous internet healthcare companies have also started to expand into pharmaceutical services, including WeDoctor’s acquisition of the pharmaceutical e-commerce platform Jinxing.com and the provision of medical service interfaces to multiple pharmaceutical e-commerce platforms. In addition, various pharmaceutical e-commerce companies are strengthening their teams of professional pharmacists to deliver specialized pharmaceutical care. Overall,E-commerce pharmaceutical companies have strengthened their capabilities in medical and pharmaceutical services through self-built platforms and partnerships, providing consumers with more professional and in-depth services.

It is also worth noting the rise of e-commerce for chronic disease medications and new specialty drugs, particularly the Direct-to-Patient (DTP) model. Originally designed as a channel to directly reach patients with new drugs—especially those not yet covered by national medical insurance—the DTP model is typically operated by pharmaceutical distribution companies and located near hospitals. As pharmaceutical e-commerce matures, the integrated “DTP + Pharmaceutical E-commerce” model is gaining traction. Pharmaceutical e-commerce platforms are not constrained by geography, enabling them to serve a broader patient population, while the specialized supply chain capabilities of pharmaceutical distributors for new and specialty drugs significantly enhance platform value. The e-commerce-enabled DTP model is expected to become an important niche segment within the pharmaceutical e-commerce market.

The integration of online and offline channels, along with multi-sector collaboration, is evident in both policy directives and industry practices. The state encourages the development of “smart pharmaceutical logistics,” and policies such as the “Two-Invoice System” and the “13th Five-Year Plan for Pharmaceutical Circulation” have explicitly called for further enhancing the adoption of internet technologies by pharmaceutical logistics enterprises.

Smart Pharmaceutical Logistics: At its core, it represents competition in supply chains and services. The competitive focus for distribution enterprises will shift from mere price and delivery capabilities to supply chain integration capabilities. Smart pharmaceutical logistics embodies the optimal model for such integration. B2B pharmaceutical e-commerce and its derived supply chain services undoubtedly possess strong competitiveness, aligning with policy directions and industrial development logic.

In the B2C and O2O sectors, online pharmacies are actively expanding their digital presence, while brick-and-mortar pharmacies are joining O2O alliances and partnering with various O2O platforms (such as JD Daojia, Meituan, and Ele.me) to extend their service reach. The boundary between online and offline channels is blurring, paving the way for direct competition between online pharmacies and retail pharmacies in the future.

Overall, the pharmaceutical e-commerce sector is gradually maturing. In the future, as relevant policies and industry practices are implemented, its development potential will be enormous. Trends such as mobile integration, specialization, diversification, intelligentization, and multi-form convergence will become increasingly prominent, disrupting traditional pharmaceutical distribution and retail.

If you are following the “pharmaceutical distribution” sector, you are welcome to register for the event to be held in Beijing from December 15–17.“2017 Future Healthcare Top 100” Forum, we will specially set up"Parallel Forum on Pharmaceutical Distribution", inviting renowned industry experts and multiple corporate executives to discuss how policies, new technologies, and e-commerce are impacting the pharmaceutical distribution sector. Long-press the image below to scan the QR code and register.