Year-End Review 2017: Matthew Effect Intensifies in Elder Care Industry as Cross-Sector Capital Pours In and Services Shift Toward Community- and Home-Based Models

In 2017, when reading reports related to the elderly care industry, one would often encounter headlines such as:

People's Daily Commentary: In the New Era, Elderly Care Services Call for an Upgraded Version

Jiangsu Province Elderly Care Industry Investment Fund Makes Its First Investment in Community-Based Home Care for the Elderly

Taikang Life Invests Over RMB 20 Billion in the Medical and Elderly Care Industries

Greenland Unveils Health and Wellness Industry Group, Plans to Invest RMB 20 Billion to Build 100 Health and Wellness Hotels

China Resources Land’s First Health and Elderly Care Project Officially Launched in Wuhan’s Central Urban Area

......

China has entered an aging society. Elderly care is no longer solely the responsibility of nursing homes and elderly care enterprises; it has become a critical issue of widespread concern across society. In 2017, multiple policies issued throughout the year provided guidance on elderly care models and business formats, such as home-based care and smart elderly care. With strong expectations for policy reforms, the development of the elderly care market has entered its golden age.

Although market development has entered the fast lane, this year, judging from capital’s reaction, the elderly care market is in a period of being “pessimistically viewed,” with startups still continuously exploring mature business models.

Another trend is that as major players in real estate, insurance, and other sectors ramp up their entry and investment, these enterprises—already successful in other fields—are increasingly optimistic about the economic impact driven by the substantial demand for elderly care, with market potential gradually being unlocked.

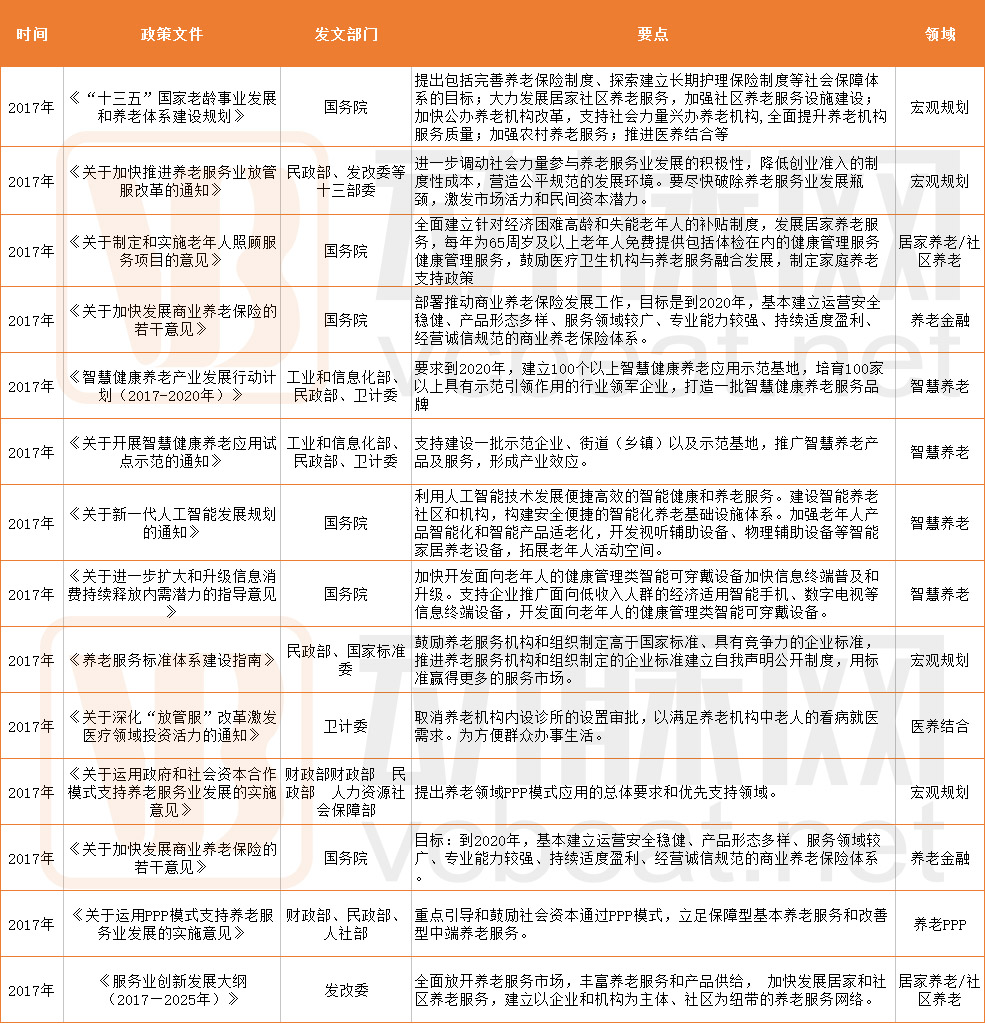

I. Continuous Policy Advancement in the Development of Elderly Care Services

2017 Elderly Care Policies

In October 2017, the report to the 19th National Congress of the Communist Party of China proposed establishing a policy framework and social environment for elderly care, respect for seniors, and filial piety, promoting the integration of medical and elderly care services, and accelerating the development of undertakings and industries related to aging. The Government Work Report presented during the Two Sessions also mentioned elderly care six times. The requirements and emphasis set forth in the top-level design served as the most steadfast guide for the development of elderly care in 2017.

2017 is a crucial year for implementing the 13th Five-Year Plan and deepening supply-side structural reform. Currently, the overall shortage of elderly care beds coexists with significant vacancy rates among existing facilities, representing a severe structural imbalance on the supply side. Therefore, supply-side reform in the elderly care sector will be a key direction for the development of eldercare services in 2017.

In addition to the documents issued at the national level, provinces and municipalities across China also responded in 2017 by aligning with the requirements of various national policies related to the elderly care industry, while taking into account local actual needs for elderly care services and market characteristics.

Following the joint release of the Notice on Accelerating the Streamlining of Administration, Delegating Power, and Improving Services (Fang Guan Fu) Reform in the Elderly Care Service Industry by thirteen ministries and commissions, including the State Council, in February 2017, thirteen departments in Hunan Province, such as the Provincial Development and Reform Commission and the Department of Civil Affairs, promptly issued the Implementation Opinions on Accelerating the Fang Guan Fu Reform in the Elderly Care Service Industry in August. These measures aimed to remove bottlenecks in the elderly care service industry by simplifying administrative approvals and strengthening supervision. Furthermore, in September, eleven departments, including the Hangzhou Municipal Bureau of Civil Affairs, also released the Notice on Accelerating the Fang Guan Fu Reform in the City’s Elderly Care Service Industry.

From central implementation to various provinces and cities, from this perspective, 2017 was the year of concentrated implementation of elderly care policies.

II. Startup Ventures Face a Cold Reception; Business Models Urgently Need Exploration

In March 2017, Anxin Qiao, an intelligent home-based elderly care system, completed a pre-A round of financing amounting to RMB 5 million, with Yunchuang Century as the investor;

In September 2017, the home-based elderly care sharing platform “Yang Ni Yi Bei Zi” completed its Pre-A round of financing, raising RMB 20 million from Mayi Investment.

In September 2017, Utopia Sanatorium Village, a shared convalescent (elderly care) village, completed its seed round of financing amounting to RMB 10 million, with the China Tea Expo as the investor.

Compared with 13 investment deals in 2016, financing and investment in the elderly care industry in 2017 dropped to a “freezing point.” As of November 1, 2017, there were only three financing deals across the entire sector, all small in scale, with a total amount of just RMB 35 million.

Despite a favorable policy environment, the vitality of social capital in the elderly care sector has yet to be fully unleashed. The industry is characterized by pronounced brand effects and concentrated resources, while mature profitability models remain to be established. Furthermore, given the public-service nature of elderly care, most institutions operate on a non-profit basis, with government-led industrial development being prevalent. Consequently, social capital largely remains on the sidelines. This explains why the market has failed to take off despite the elderly care needs of 230 million people in China.

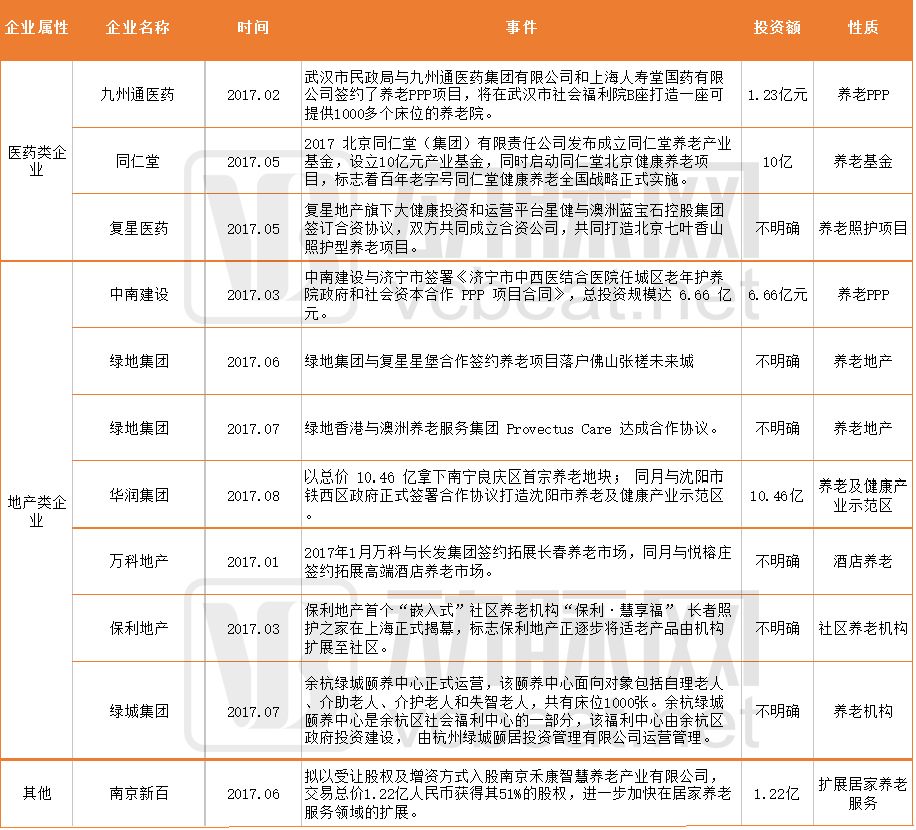

III. Capital from Various Sectors Accelerates Investment in Senior Living Real Estate, Entering a Golden Period for Strategic Market Entry

According to a research report by Everbright Securities, although capital inflows have cooled, certain developments in the elderly care sector in 2017 still reveal accelerated strategic positioning by companies in industries such as real estate, pharmaceuticals, and insurance.

2017: Companies Rush to Enter the Elderly Care Market

Amid the “beachhead landings” by various investors, real estate developers have leveraged their extensive operational expertise to rapidly enter the senior housing development sector, creating high-end senior living communities that address elderly needs starting from the most immediate, granular level.

Using “elderly care” as a gimmick for land acquisition and promotions has become a thing of the past. Real estate developers, insurance companies, and medical institutions are joining forces to integrate the entire development and operation process through age-friendly product designs in elderly-care real estate and integrated medical-care models. Leveraging brand strength and meticulous product design, several leading real estate firms and insurance-backed entities have established reputable elderly-care product lines, such as Vanke’s Suiyuan, Poly’s Huixiangfu, Greentown’s Wuzhen Yayuan, Taikang Community, Sino-Ocean Chunxuanmao, and Fosun Starcastle. Capital from various sectors is accelerating its layout in the elderly-care real estate market.

In addition, strengthened policy guidance and enhanced fiscal and financial support have propelled elderly care public-private partnership (PPP) projects into a period of rapid development. According to WIND data, the number of elderly care beds in China grew rapidly from 1.58 million in 2005 to 7.3 million by the end of 2016. Investment in PPP elderly care projects surged from RMB 122.7 billion at the beginning of 2016 to nearly RMB 190 billion by August 2017.

Insurance-Linked Elderly Care Projects

Insurance-affiliated companies are also actively integrating into the investment and operational management of institutional elderly care, leveraging their large capital scale, long investment horizons, and the inherent synergy between insurance products and eldercare services.

According to incomplete statistics from VCBeat, a total of eight insurance institutions are currently involved in the development of senior living communities, with their primary presence concentrated in first-tier cities such as Beijing, Shanghai, and Guangzhou, along with their surrounding metropolitan areas, as well as in cities including Wuhan, Shenyang, Dalian, and Suzhou. Among these, Taikang Life Insurance has the broadest reach, having invested over RMB 5 billion in its integrated medical and elderly care projects. It has already established senior living communities in eight locations—Beijing, Shanghai, Guangzhou, Sanya, Suzhou, Chengdu, Wuhan, and Hangzhou—and plans to expand to 15–20 communities over the next five to eight years.

IV. Smart Elderly Care Facilitates Efficient Management of Community- and Home-Based Elderly Care

In 2017, the Ministry of Industry and Information Technology, the Ministry of Civil Affairs, and the National Health and Family Planning Commission jointly issued two documents. From the “Action Plan for the Development of the Smart Health and Elderly Care Industry (2017–2030)” to the notice on pilot standardization, a series of action plans for smart elderly care were introduced, and pilot programs were intensively implemented. The outcomes of smart elderly care will become indispensable tools for providing auxiliary services in the offline elderly care industry.

In May 2017, the Department of Electronic Information of the Ministry of Industry and Information Technology (MIIT) convened the 2017 National Electronic Information Industry Work Symposium in Nanjing, Jiangsu Province. At the meeting, Qiao Yueshan, Deputy Director of the MIIT’s Department of Electronic Information, pointed out that it is necessary to promote smart health and elderly care and leverage information technology to revolutionize traditional eldercare models. By integrating and applying next-generation information technology products, smart health and elderly care can facilitate the optimized allocation and improved utilization efficiency of existing medical, health, and eldercare resources, thereby meeting the multi-level and diversified health and eldercare service needs of families and individuals.

The national plan for smart elderly care fully leverages the rapid development of informatization and the Internet of Things (IoT), aiming to achieve efficient and high-quality elderly care management, with the goal of basically establishing a smart health and elderly care industrial system covering the entire life cycle by 2020.

Of the handful of financing rounds that have taken place this year, two were related to smart elderly care systems and smart elderly care platforms.

The integration of the Internet into the elderly care sector leverages its advantages in information exchange, processing, storage, maintenance, and big data mining. By combining computers, servers, information management centers, and mobile terminal devices with the Internet of Things (IoT), personalized services are provided to seniors, encompassing daily living assistance, health management, medical nursing, and emotional support.

Leveraging the “Internet + Elderly Care” model, intelligent and diversified elderly care services will effectively address the current challenges faced by the majority of older adults in accessing adequate care. Older adults aging in place can receive comprehensive, round-the-clock care and nursing support through “Internet +” technologies. Smart elderly care solutions can significantly enhance management efficiency for elderly care institutions and communities, thereby making home-based and community-based elderly care viable and sustainable.

V. Shifting Elderly Care Models Toward Community- and Home-Based Services

The Elderly Care System Is Gradually Maturing

“With the advent of the 13th Five-Year Plan period, home-based elderly care services and the cultivation of the market and industry for such services began to gain momentum and heat up.”

As the population of disabled elderly individuals grows and pressure on the younger generation intensifies, hiring professional caregivers may become an increasingly common choice for families. As early as in the “12th Five-Year Plan for the Development of the Social Elderly Care Service System (Draft for Comments)” issued by the Ministry of Civil Affairs in 2011, it was projected that by 2020, the potential market size for elderly nursing services and daily living assistance in China would exceed RMB 500 billion.

In March 2017, the State Council issued the “13th Five-Year Plan for National Development of Aging Undertakings and the Construction of the Elderly Care System.” The plan proposed that by 2020, a multi-pillar, universally covered, more equitable, and more sustainable social security system would be further improved, and an elderly care service system—home-based, community-supported, institution-supplemented, and integrating medical and elderly care—would be more sound.

The market size of China's elderly care industry is expanding rapidly. In 2016, the market size was approximately RMB 5 trillion; it is projected to reach RMB 7.7 trillion by 2020, with a compound annual growth rate (CAGR) of 11.4%, and is expected to exceed RMB 20 trillion by 2030.

According to projections, by 2020, the number of disabled elderly people in China will reach 42 million, those aged 80 and above will reach 29 million, and elderly individuals living in empty-nest households or alone will reach 118 million.

This elderly demographic is a key focus of societal attention and central to addressing eldercare challenges. Empty-nest and solitary seniors primarily require daily living assistance and emotional companionship; the oldest-old, in addition to these needs, have a greater demand for medical nursing and palliative care; while disabled seniors require focused solutions for professional medical treatment and nursing care.

Targeted reforms in social elderly care are shifting from institutional facilities to community-based models, with a strong emphasis on home-based care. The concept of the “nursing home without walls,” supported by smart elderly care technologies, offers a novel approach to resolving current challenges in home-based care. It maximizes the service radius of professional caregivers while alleviating the caregiving burden on family members.

Community-based Elderly Care Centers and Day Care Centers Adapt to Diverse Aging Needs

During the 2017 "Two Sessions," Huang Shuxian, Minister of Civil Affairs, stated that strong support would be provided this year for home-based and family elderly care, community-based elderly care services would be accelerated, market mechanisms would be leveraged, and elderly care institutions adapted to multi-level needs would be established. Although top-level design supports elderly care, its implementation depends on the specific conditions of each province and city.

In 2016, Beijing launched a pilot program for elderly care service stations. As part of the government’s basic public services, these stations operate under a model in which the government is responsible for providing facilities, district and sub-district authorities offer venue support to communities free of charge, and professional elderly care service enterprises handle operations. By the end of 2016, 150 elderly care service stations had been established across the city, with 70% operating under branded chain models.

By 2017, Beijing will have 200 elderly care service stations operating on a pilot basis, with the total number reaching 350 by the end of the year. By 2020, the total number of community-based elderly care service stations will reach 1,000, basically achieving full coverage in areas with larger elderly populations.

The Chongqing Municipal Civil Affairs Bureau plans to add 200 new urban community elderly care service facilities in 2017. By the end of 2017, the city will have completed the addition of 1,000 such facilities, achieving the goal of creating a “wall-free nursing home” and enabling seniors to access socialized elderly care services.

In June 2017, the Zhejiang Provincial Government recently released the “13th Five-Year Plan for the Development of Aging Causes in Zhejiang Province,” requiring the integration of community service resources and accelerating the construction of comprehensive facilities for urban and rural home-based elderly care services. By 2017, full coverage of home-based elderly care service centers in rural communities was basically achieved, forming a 20-minute home-based elderly care service circle in urban and rural communities across the province.

In 2016, Zhejiang Province added 3,300 urban and rural community-based home care service centers. In 2017, an additional 1,000 such centers were established, bringing the cumulative total to 23,000 during the 13th Five-Year Plan period. This expansion has accelerated the development of an elderly care service system that is home-based, community-supported, institutionally supplemented, and integrates medical and elderly care services.

According to the 2016 Statistical Bulletin on Social Service Development issued by the Ministry of Civil Affairs, there were 140,000 elderly care institutions and facilities across China, representing a year-on-year increase of 20.7%. Among these, there were 29,000 registered elderly care institutions, 35,000 community-based elderly care institutions and facilities, and 76,000 community mutual-aid elderly care facilities. The total number of elderly care beds reached 7.302 million, an 8.6% increase from the previous year (with 31.6 beds per 1,000 elderly people, a 4.3% year-on-year increase), including 3.229 million beds for community residential stay and daytime care.

Although home-based elderly care service facilities in urban communities have basically achieved full coverage, their functions remain inadequate. The majority of community-based elderly care services focus on cultural, sports, and recreational activities, while services such as rehabilitation nursing and integrated medical and elderly care are significantly insufficient. With the advancement of urbanization, the grassroots elderly care service system will face greater pressure in service delivery, necessitating intensified efforts in infrastructure development.

Meanwhile, high-end community-based elderly care and integrated medical-care management centers are the domain of real estate developers.

Evergrande Health has leveraged health management and elderly care services as its entry point to precisely position its 12 nationwide “Internet+” Health Management Centers. Building upon existing community-based health diagnosis and treatment services, the centers have integrated rehabilitation and elderly care modules. Through collaborations with nearly 30 local Grade A tertiary hospitals and specialized hospitals of high caliber, Evergrande Health serves a population of approximately 200,000 residents in surrounding communities, thereby achieving an initial nationwide footprint for this business segment.

Currently, Evergrande Health has established 11 pilot community health centers across nine provinces in China, including in Guangzhou, Changsha, Nanchang, Wuhan, Chengdu, Jinan, Luoyang, Shijiazhuang, and Shenyang.

Vanke is a pioneer in the senior housing real estate sector. The initiation of Vanke Hangzhou’s “Suiyuan Jiashu” project in 2009 marked Vanke’s first step into elderly care. Currently, the three major product lines under the “Suiyuan Series” have begun large-scale operations.

As of the end of 2016, Vanke’s Suiyuan Home community-based elderly care services, centered in Hangzhou and Ningbo, had covered more than 100 day-care centers, marking the onset of large-scale operations. Over the next three years, it plans to establish 1,000 service outlets, directly serving over 50,000 clients and reaching a senior population of 600,000.

The "China Health and Elderly Care Industry Report (2016)" indicates that since the elderly care industry began its marketization in 2013, various enterprises have entered the field. This trend evolved from the influx of real estate, insurance, medical services, and rehabilitation aid companies in 2014; to the gathering of industry chain-related enterprises, including those in real estate, insurance, healthcare, nursing, medical devices, internet, and general health, in 2015; and further to the capital involvement and cross-sector entry of large state-owned enterprises and private corporate groups in 2016. The year-by-year evolution of the main players in market competition not only highlights the diversity of participants in the elderly care industry but also gradually reveals the future competitive landscape of the sector.

Thus, VCBeat believes that the elderly care industry will evolve toward a competitive landscape characterized by differentiated linkages between upstream and downstream sectors. The “Matthew Effect” in the market will become increasingly pronounced. Building on the wave of M&A activities seen in 2016, cross-sector competition and consolidation through mergers and acquisitions will emerge as the dominant trend, with a cohort of well-capitalized enterprises securing leading market positions.

Driven primarily by policy and characterized by significant government involvement, competition within the industry remains at an early stage. Most elderly care startups are small in scale and still exploring their business models. With low market concentration, neither industry monopolies nor brand effects have yet emerged, leaving substantial market potential to be unlocked.

Notably, companies that center on an asset-light model and build brand advantages through scalable chain replication—such as those providing in-home care and community-based adult day care services—are worth attention. The elderly care industry is heavily service-oriented, and these service-driven companies may carve out a new path in a sector traditionally dominated by asset-heavy models. Meanwhile, it is important to note the policy tailwinds benefiting the entire elderly care industry, including incentives for integrating medical and elderly care, as well as promoting community-based and home-based care models. As scale expands and performance gains materialize, leaders in niche segments will gradually emerge, potentially leading to market consolidation and monopolistic tendencies.

Faced with the needs of nearly 230 million elderly people, and buoyed by vast market potential and strong government support, China’s elderly care industry is currently experiencing an unprecedented golden age of development.