2017 Year-End Review: Rapid Growth of Branded Chains and Boutique Clinics, Stabilization of Leading Aesthetic Apps, and Rise of Integrated Medical-Aesthetic Business Models

Medical aesthetics is one of the fastest-growing segments within the consumer healthcare sector. Large branded chains and boutique clinics are thriving, while mid-sized institutions with weaker brand recognition face significant challenges. Publicly listed capital firms are aggressively competing for market share and talent, and physicians, encouraged by policy incentives, are increasingly joining the entrepreneurial wave. From a technological perspective, minimally invasive procedures and energy-based devices are highly popular, light medical aesthetics is trending, and the coexistence of medical and lifestyle beauty services remains a long-standing industry norm.

So, what changes occurred in the medical aesthetics industry in 2017? Below is a summary of the key trends that emerged this year.

Since 2000, after a decade of golden development, medical aesthetics and plastic surgery have gradually transformed from a private consumption into a mainstream fashion trend.

Broadly speaking, prior to 2010, consumers’ attitudes toward medical aesthetics and plastic surgery were characterized by curiosity, avoidance, and resistance. It is now an undisputed fact that, although concerns about safety, efficacy, physician branding, and technical expertise persist, the overall acceptance among Chinese people has increased.

For a small subset of aesthetic seekers, medical aesthetics and plastic surgery have become a form of "addictive" affordable luxury consumption, necessitating consultations with plastic surgeons every few months.

Not only consumers, but also medical aesthetics practitioners, having witnessed the industry’s unchecked expansion, have evolved from initially being reluctant to discuss it to becoming active promoters, participants, and agents of change within the medical aesthetics sector.

Driven primarily by women, the medical aesthetics “beauty economy” has grown and matured amid controversy alongside sociocultural shifts, with its latent growth potential truly not to be underestimated.

To illustrate with an example, Gengmei, a leading medical aesthetics app platform, launched its new brand proposition in May this year: “Life Is Not Innate,” which is highly representative.

Mei’s new brand proposition, “Life Is Not Innate,” Resonates with Young People’s “Sang Culture”

Behind the brand’s advocacy of its core values, a wave of social discussion has been sparked. While you may uphold the notion that “natural is beautiful,” it seems hardly reprehensible to leverage emerging technologies to alter one’s appearance—or even one’s destiny.

In August, SoYoung, a leading medical aesthetics app platform, collected plastic surgery stories from over ten young women and selected some to produce a video. By sharing their wounds, pain, joys, and sorrows with the audience, it sparked heated discussion.

SoYoung’s New Brand Proposition, “Brave Change,” Voices the Aspirations of the New Generation of Women

Why do women consider undergoing minimally invasive cosmetic procedures? Are they compelled by environmental pressures? Is society sufficiently open-minded? What impact does plastic surgery truly have on one’s life? These questions delve into the realm of shifting values, worldviews, and social culture, and to some extent, reflect today’s societal emphasis on physical appearance.

This is an indispensable prerequisite for the development of the medical aesthetics industry. As the main consumer base now consists of the new generation born in the 1980s and 1990s, service models and philosophies must adapt accordingly.

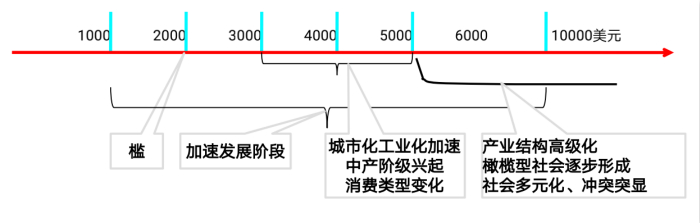

Furthermore, from the perspective of the broader economic environment, GDP per capita is a significant indicator: at different stages of GDP per capita, corresponding phenomena, problems, and solutions naturally emerge within individual experiences and society.

Along the trajectory of per capita GDP evolution, corresponding economic and social phenomena emerge at each stage, encompassing both industrial opportunities and risks.

The Relationship Between Per Capita GDP and Industrial Transformation

Specifically, urbanization begins to take off at $1,000; accelerates its development at $3,000; and sees entirely new expansion of urban development space at $5,000.

Starting from a per capita GDP of $5,000, an olive-shaped society has gradually taken shape, characterized by social diversification. Healthcare and medical services have become a key driver of consumption growth, with urban complexes and large shopping malls emerging as the mainstream consumption ecosystems for urban residents. With China’s current per capita GDP reaching $8,000, demand for high-end medical aesthetic services is poised for further release.

According to the “2017 White Paper on the Medical Aesthetics Industry” released by So-Young in August of this year, it is estimated that 14 million Chinese people will enhance their appearance through medical aesthetic procedures in 2017, representing a year-on-year increase of 42% compared with 2016. This growth rate far exceeds the global average of 7%, making China the fastest-growing country in the global medical aesthetics market.

A 2017 Deloitte report indicates that China’s volume of formal medical aesthetic procedures (including surgical and non-surgical treatments) accounts for approximately 10% of the global total, making it the third-largest market worldwide.

The growth rate of China’s medical aesthetics market is expected to remain above 20% over the next five years, with the market size projected to exceed $10 billion in 2017. Amid the aggressive race for talent and market share, the density of domestic medical aesthetics institutions is rapidly approaching the levels seen in mature foreign markets.

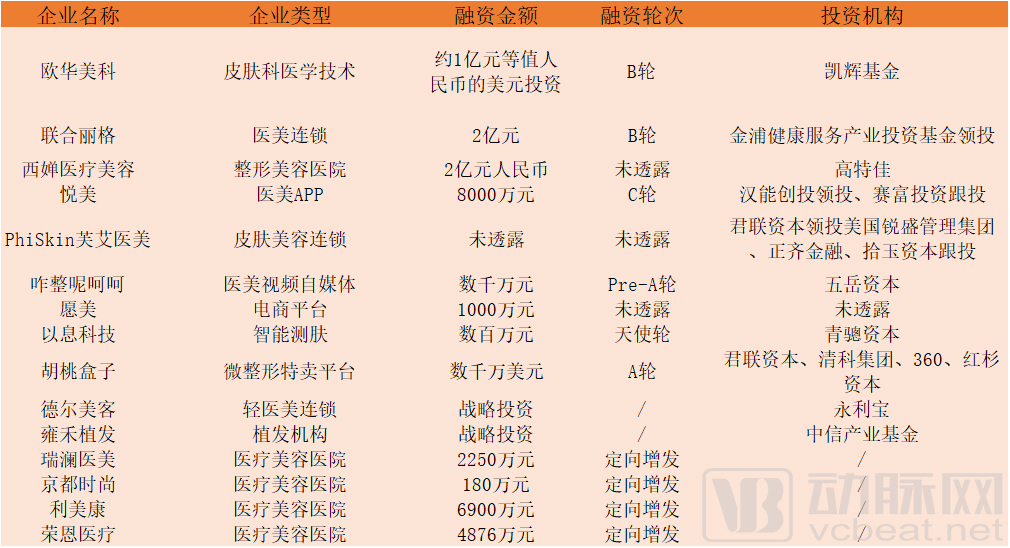

2017 Financing in the Medical Aesthetics Sector, Compiled from Public Sources

Previously, over 50% of the marketing expenses of medical aesthetic institutions were allocated to channels. With the advent of the internet, a transformative impact has been exerted on the redefinition of traffic rules and industry development, primarily manifested in two aspects: customer acquisition and patient education. Sensing these pain points, medical aesthetic apps have emerged as the fastest-rising players.

2016 marked a boom period for medical aesthetics apps to announce financing rounds. SoYoung (Series C), Gengmei (Series C), Yuemei (Series B), Meidaila (Series B), and Meili Shenqi (Series B) all secured funding. In 2016, Gengmei raised RMB 345 million in its Series C round, the largest single financing deal in the history of China’s internet-based medical aesthetics industry.

In August 2017, Yuemei announced that it had secured RMB 80 million in Series C financing, becoming the third app platform in the industry to announce the completion of such a round. The round was led by Haneng Venture Capital, with follow-on investment from Safeguard Partners, an existing investor. The funds will be primarily used for team building, efficient and targeted marketing promotions, and expanding its offline presence.

When first entering the market, medical aesthetics apps may have approached from different angles. Once a company figures out a relatively smooth and verifiable business model, other enterprises quickly follow suit, leading to increasing product homogenization. Previously, there were around 30 medical aesthetics apps on the market; after intense competition, only five or six remain this year.

However, specific strategies and tactical approaches may vary across companies. Leading platforms typically focus on continuously expanding their scale and market share, leveraging economies of scale to establish competitive barriers. Companies with relatively smaller market shares may concentrate on specific niche segments, offering differentiated services.

For medical aesthetics apps, there may also be differences in product experience; more importantly, however, are the company’s positioning, strategy, and operations.

Broadly speaking, medical aesthetics apps primarily aggregate users through a combination of content, community, and e-commerce, or via appointment and referral services, thereby building a bridge for communication between B-side institutions and doctors and C-side customers. However, this year, various platforms have also implemented significant product upgrades to improve user decision-making efficiency and optimize the positioning and operational models of doctors and hospitals.

In terms of integrating the upstream and downstream segments of the industrial chain, such as large-scale medical device manufacturers, pharmaceutical companies, and insurance providers, these platforms are also extending their reach.

But have medical aesthetics apps completely resolved the issues of information asymmetry and transparency? VCBeat believes that contradictions in the patient education market will persist for a long time.

Users are not experts in internet products and have a long decision-making cycle for consumption. Therefore, various medical aesthetics KOLs are active on forums, communities, Tieba, WeChat groups, and Weibo. Next year, Meibei, which has already achieved profitability, will focus on cultivating in-house medical aesthetics KOLs to provide professional content.

Xiu Zhifu, the top influencer in medical aesthetics on Sina Weibo with over 2.8 million followers, and Wang Shihu, the leading influencer on Zhihu, have been popularizing the fundamentals of plastic surgery under cosmetic surgery topics to enhance patient education. Leveraging internet trends, they have built strong professional reputations for physicians.

Content generated through live streaming and short-form videos is, to some extent, more intuitive than plastic surgery diaries and static images. Live streaming content primarily takes three forms: clinic visits, user-generated educational content by physicians, and real-user experience sharing. In addition to dedicated live-streaming platforms, medical aesthetics apps have integrated various engaging live streams, thereby enhancing user stickiness.

This September, the medical aesthetics self-media account “Zha Zheng Ne Hehe” secured tens of millions of RMB in Pre-A round financing, with Wuyue Capital as the investor. Leveraging entertainment formats such as short videos, live streaming, WeChat Official Accounts, and Weibo, it delivers professional medical aesthetics content by inviting renowned plastic surgeons and guests to popularize cosmetic surgery knowledge through talk shows and guest dialogues, aiming to shorten the lengthy consultation process users typically undergo before undergoing procedures.

Patients of such physicians are typically loyal to the doctor themselves, traveling from across China to seek their care, and the fees charged are by no means low.

The internet is revolutionizing patient acquisition and education, with news articles, websites, Baidu Maps, and Baidu Phone becoming essential channels. Doctors and medical aesthetics institutions should leverage their resource advantages to maximize the efficacy of the internet.

Shifting Focus from Customer Acquisition to Operations

In the era when traditional advertising reigned supreme (print, television, PC search engine bidding, etc.), medical aesthetic institutions, particularly those affiliated with the Putian network, primarily focused on strategies to attract new customers. During that period, the impact of advertising was indeed remarkable; a well-crafted promotional campaign could generate significant momentum and drive explosive growth, as market competition was not yet intense.

However, the influence of traditional advertising has significantly waned. Search engine bidding, once an indispensable channel for most aesthetic medicine institutions, is now seeing declining effectiveness and has become a marginal asset; achieving a 1:2 return on investment through Baidu’s bidding system is considered favorable. The cost of acquiring new customers continues to rise, while their quality has deteriorated markedly compared to the past.

Large institutions, leveraging their brand recognition and scale, can invest millions each month in bidding for ad placements and outdoor brand advertising to drive customer conversions. Small institutions cannot sustain such expenditures, particularly in mature first- and second-tier markets. For instance, in the Chengdu area, rapid development over the past two years has led to more than 200 non-public plastic surgery clinics entering the market.

According to Huang Shitou (a pseudonym), a senior researcher on China’s private healthcare sector: “Some astute players from the Putian network have begun to shift their strategy toward prioritizing existing customers, leveraging quality and service to further tap into the resources of this loyal base and attract more high-quality new customers through referrals. This adaptation to the times is the fundamental reason why some Putian-affiliated medical aesthetic institutions continue to thrive.”

As previously mentioned, this strategic shift is driven by the advent of an era characterized by repeat consumption in the medical aesthetics industry. Against the backdrop of increasing information transparency, aesthetic seekers have raised their expectations regarding surgical outcomes, safety, physician branding, and service quality. Physicians who excel in technical expertise, professional image, and communication are more likely to build their own intellectual property (IP) and cultivate a loyal fan base. This results in high patient retention and even proactive referrals to friends and family.

In terms of customer acquisition, certain standardized procedures—such as minimally invasive aesthetic treatments like “Three Injections and One Thread” and medical-grade facials—have low barriers to entry and are priced affordably. These low-cost offerings primarily serve as lead-generation tools, with their affordability marking a trend toward mainstream mass-market adoption in the medical aesthetics industry.

Some procedures rely on individual surgical skill and are non-standardized, such as suture double eyelid surgery, rhinoplasty, and autologous fat grafting. Customers, driven by trust in the physician and the institution’s brand, exhibit low price sensitivity, allowing these high-priced services to generate profit margins.

This trend is particularly evident in the consumer healthcare sector, such as medical aesthetics and dentistry. Maintaining strong relationships with existing clients not only generates stable revenue but also leverages these highly influential beauty-seeking patients, who play a crucial role in building physicians’ reputations.

Currently, only a few enterprises that prioritize channel dominance—those dealing exclusively with beauty salons, nightclubs, and similar venues, offering 50% rebates to channels, and avoiding online advertising—continue to thrive. This is largely due to their high average transaction values, and in some cases, even overtreatment.

Under the influence of mobile internet, companies such as Yumeiren, Weikai, and Baihe, as well as Heli—which rose to prominence in recent years through its exposed “crowdfunding rebate” model—are also undergoing deep fission.

After illegal micro-plastic surgery studios, influencer-led studios, and surgical procedures performed in beauty salons were classified as illicit operations and cracked down on by authorities, the unique business model of such companies attracted a large volume of clients from these channels, making them a distinctive product of the times.

From a national policy perspective, while the development of private hospitals is being encouraged, regulatory oversight of the medical aesthetics industry is simultaneously being strengthened. Opportunities to generate quick profits by acquiring new customers are dwindling, particularly in first-tier cities where supply is abundant. Institutions with low operational efficiency and uncompetitive business models face significant pressure on profitability.

Jason Jia, Executive President of Suning Universal Capital and President of SuYa Medical Aesthetics, shared his insights at the recently held “Asia-Pacific Launch Event on Trending Minimally Invasive Cosmetic Procedures for Enhanced Facial Aesthetics.” He stated, “Medical aesthetics is fundamentally a service industry with inherent medical attributes. Its future lies in genuinely prioritizing each customer’s interests, delivering utmost quality and service, and ensuring reasonable pricing. Institutions that profit from information asymmetry and treat customers as easy prey will inevitably be eliminated.”

Since 2015, substantial capital has begun to position itself within the medical aesthetics industry. Financial investors such as Sequoia Capital, Matrix Partners, IDG Capital, and SAIF Partners have taken equity stakes in medical aesthetics apps, while industrial capital from companies like Evergrande, Langzi Shares, Suning, Huapont Life Sciences, and Fosun Group has invested in medical institutions. The large-scale entry of publicly listed capital into the medical aesthetics sector is poised to disrupt the industry’s established rules.

Limeikang, dubbed the “No. 1 Stock of New Third Board Breast Augmentation,” embarked on its IPO journey in 2017.

Limeikang’s primary revenue stream comes from plastic surgery procedures, such as double eyelid surgery, cosmetic rhinoplasty, breast augmentation, and liposuction for weight reduction. Approximately 80% of its clients are women aged between 20 and 40. In 2016, the company reported revenue of RMB 194 million, a year-on-year increase of 37.36%, and net profit of RMB 23.7 million, up 44.39% year on year. This April, it completed a new round of private placement, raising a total of RMB 69 million.

Is the medical aesthetics market truly that large? Data from the past five years alone indicate explosive growth in this sector. Moreover, the medical aesthetics industry demonstrates strong extensibility, with the potential to penetrate the markets for lifestyle beauty services and skincare products. Currently, clinics remain the predominant type of medical aesthetics institution, with fewer than 100 large-scale chain operators.

This year, significant adjustments have been made to the national healthcare reform policy framework. Favorable policies continue to be introduced, such as encouraging private capital investment in the medical services sector and promoting multi-site practice for physicians. Physician entrepreneurship is also an observable trend this year.

VCBeat believes that two types of medical aesthetic institutions have promising development prospects.

The first type comprises large medical aesthetics groups, such as Mylike, which feature institutionalized management models, strong technological advantages, and robust resources in academic research and overall capabilities. Currently, it operates 33 asset-heavy large-scale hospitals across China.

Adapting to the times, Mylike has also established an Internet Center to study the characteristics of various online channels and determine how to better align them with Mylike’s resource advantages. The old Putian-style model will eventually become a thing of the past. Other large branded medical aesthetics groups include Yestar, Emeireal, Lidu, Huahan, and United Lige.

As a leading medical aesthetics group and incubation platform for entrepreneurial physicians in China, United Bionic has opened nearly 30 high-end medical aesthetic institutions across major cities nationwide within four years of its establishment.

In June this year, Bontec Group completed a RMB 200 million Series B financing round. Li Bin, founder of Bontec Group, previously stated, “Following the financing, our first priority is to strengthen existing operations and accelerate the nationwide expansion of our medical aesthetics network, particularly in the Chengdu-Chongqing region and the Pearl River Delta. Second, we will continue to invest in high-quality physicians, aiming to become China’s premier entrepreneurial platform for top-tier medical aesthetics doctors.”

In September, Union Beauty First Medical Aesthetic Hospital officially opened its doors. The “Medical Aesthetics Dream Team” physician group, jointly led by Professor Cao Yilin, an internationally renowned tissue engineering expert and the pioneering scientist behind the world-famous “human-ear mouse,” and Professor Guo Shuzhong, the lead surgeon for the world’s second and China’s first face transplant surgery, has relocated en masse to Union Beauty First Medical Aesthetic Hospital. New Oxygen is also among the investors in this funding round.

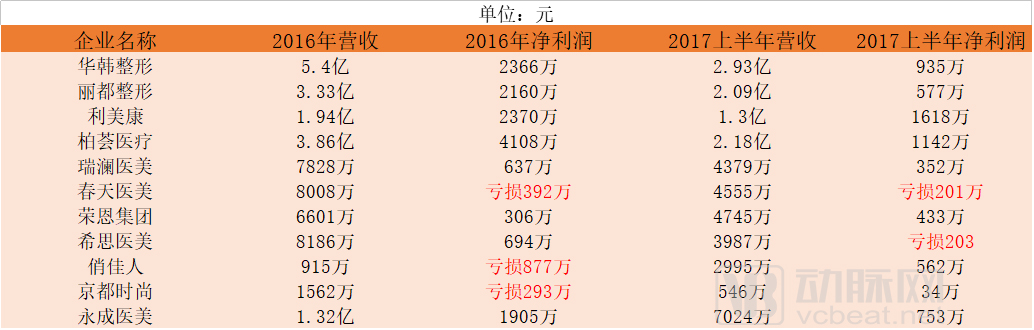

Profitability of Medical Aesthetics Companies on the NEEQ: Data Sourced from Annual Reports; Yimeier Has Delisted

The second type consists of small, distinctive boutique aesthetic medicine clinics that either specialize in a specific niche procedure, such as rhinoplasty, or are backed by renowned physician groups.

Beijing Shengjiaxin Medical Aesthetic Hospital is a plastic surgery institution distinguished by its “Renowned Physician Partnership Model.” Demonstrating strong growth momentum, the hospital was co-founded by Director Li Zhen, an expert in body contouring via liposuction; Director Zhang Xiaotian, an expert in facial refinement; and Director邱立东 (Qiu Lidong), an expert in micro-liposculpture.

Shengjiaxin has abandoned the traditional hospital management model based on physician employment, instead adopting a department-leadership approach driven by renowned specialists. This strategy ensures multiple benefits, including direct consultations with experts, technical authority, controllable risks, guaranteed outcomes, and high-quality service. It forms a benefit plan that offers more personalized customization and humanistic care for patients, driving upgrading and development toward specialization.

Institutions of this scale, typically covering a few hundred square meters, generally have relatively low labor, property, and operational costs. In some cases, the physician is also the owner, with a base of loyal clients or referrals driven by word-of-mouth reputation. By leveraging high-efficiency operational models, these entities can capture a certain market share in various regions. However, compared to large branded chains, it is more challenging for them to become mainstream players; their success ultimately depends on whether their market operation model is competitive.

In the course of growth, many mid-sized institutions often face the fate of nearing bankruptcy or being acquired.

These institutions lack the capital and resource advantages of larger organizations, suffer from non-institutionalized management, and struggle to retain talent. Consequently, they are ill-equipped to adopt asset-heavy replication models, making them highly susceptible to growth impediments in a market characterized by fierce competition for talent and market share, or to being merged with or acquired by larger entities and drawn into new capital valuation adjustment mechanisms (VAMs).

Light Medical Aesthetics: Characterized by its ease, convenience, and simplicity, this approach to medical aesthetics prioritizes professional safety while employing various non-surgical medical techniques—such as laser skin rejuvenation, injectable fillers, botulinum toxin injections for slimming and wrinkle reduction, and non-invasive cosmetic procedures—to replace traditional surgical interventions. Its objectives include skin tightening and wrinkle reduction, facial micro-contouring, facial rejuvenation, body slimming and contouring, and the treatment of dermatological conditions.

VCBeat has learned that laser treatments and minimally invasive injectable procedures emerged relatively early, initially adopted by private hospitals before gradually gaining acceptance in public hospitals.

At the media launch of the “2017 White Paper on the Medical Aesthetics Industry,” Jin Xing, founder of SoYoung, stated: “Overall, minimally invasive procedures account for the largest share of orders on the SoYoung platform, reaching 70%. In fact, the minimally invasive market sees new trending treatments emerge each year, such as skin boosters, Thermage, and Theralift, with relatively rapid updates and iterations.”

The medical aesthetics industry remains highly profitable. Unlicensed “black market” operators and so-called “black doctors” who begin practicing after only a few days of training have created fertile ground for botched procedures and exorbitant profits.

Lower pricing is an inevitable trend. In the long run, with the emergence and widespread adoption of each new technology, the gross profit margin of an industry invariably declines. The medical aesthetics sector is no exception, particularly in the area of laser-based skin rejuvenation services.

Ouhua Medical Aesthetics Group, a benchmark in the field of non-invasive medical aesthetics and China’s earliest chain of non-surgical aesthetic clinics, has maintained distinct characteristics since its inception. Committed to serving as consumers’ personal skin care physicians, the group has expanded rapidly from a small startup team to covering dozens of large and medium-sized cities across China, with over 30 affiliated institutions.

Dermeck covers 23 provinces and 52 cities across China, with nearly 100 clinics offering light medical aesthetic solutions such as skin management, minimally invasive procedures, facial plastic surgery, facial rejuvenation, and medical tattooing. The chain brand aims to reduce costs through joint procurement. Hongtai Fund invested in the angel round, and this August, the company secured strategic investment from Yonglibao.

Meidaila App has launched its offline light medical aesthetics brand, Time Sea Scientific Beauty, in South China. Ningyue Clinic does not provide surgical services; it exclusively offers three types of light medical aesthetic services: medical skincare, appearance management, and overall condition enhancement. Fanxing Light Medical Aesthetics, established earlier this year, is positioned to provide dermatological cosmetic treatments and one-stop anti-aging solutions, with its first offline clinic opening in Xi’an in July.

PhiSkin, a premium medical institution specializing in skin management and minimally invasive aesthetic procedures, originated in the United States. In May this year, PhiSkin secured financing led by Legend Capital, with participation from Ares Management Corporation, Zhengqi Finance, and Shiyu Capital.

In December, Meibeier Group, a major domestic chain of medical aesthetics institutions, entered into a strategic partnership with Wanda Group. All chain stores under “SULI,” Meibeier Group’s newly launched light medical aesthetics brand, will gradually be established in multiple Wanda Commercial Plazas across China, becoming a regular component of their business formats.

Moreover, certain niche segments within the medical aesthetics industry also hold significant market potential. On September 20, CITIC Private Equity Fund announced its investment in Yonghe Hair Transplant, with the strategic partnership aimed at reshaping the brand strategy and visual identity system.

Yonghe Hair Transplant, established in 1999, is currently a hair transplant institution in China that holds independent intellectual property rights for its hair transplantation technologies and has obtained authoritative ISO certification. It is also a large-scale specialized hair transplant hospital with a nationwide presence.

It is worth considering how much incremental customer acquisition shopping mall locations can truly deliver, and whether site selection remains meaningful. Does the positioning of light medical aesthetics still hold competitive advantage? Given the current overheating in certain local markets, saturated competition will inevitably lead to price wars. Leading brands, leveraging their team capabilities, financial strength, and business model barriers, are poised to rapidly break through and scale up via asset-light replication models.

It is impossible to discuss medical aesthetics without addressing lifestyle beauty services. Beauty salons were once a significant channel source, an issue that cannot be avoided, although practitioners are increasingly advocating for a return to the essence of medical care, with their voices growing louder.

The integration or transformation between medical aesthetics and lifestyle beauty has become a market-validated successful model. While lifestyle beauty businesses control key traffic entry points, their transition into medical aesthetics faces practical challenges such as lack of medical technical expertise, non-standardized team management practices, and differences in operational and service models. These challenges have, to some extent, spurred the emergence of well-regarded consulting firms such as Huicheng Consulting (specializing in medical aesthetics) and Meimei Consulting (specializing in lifestyle beauty).

Furthermore, in the digital transformation of offline chain clinics, Hongmai and Huicheng Medical Aesthetics have been continuously exploring medical aesthetics SaaS solutions. While this represents a long-term trend, a key challenge remains: how to achieve highly standardized applicability despite the differing business logic across individual clinics.

While traditional aesthetic services may expand more rapidly in terms of replication and scaling, the growing demand for beauty enhancement and increasing acceptance of minimally invasive procedures are driving a sustained trend toward their effective integration and complementarity. Mutual penetration and cross-industry operations are likely to emerge as the ultimate business model.

Xiuyu and Beauty Farm are two highly representative companies, both of which have received investments from venture capital and industrial funds.

Founded in 1993, Beauty Farm Group has evolved into a company spanning three major sectors: lifestyle beauty, medical aesthetics, and anti-aging healthcare. The group operates over 210 high-end Beauty Farm chain stores, 16 CellCare professional medical aesthetic clinics, and three Qiyuan International Anti-Aging Medical Centers, covering 65 key cities across China. It continues to expand its scale through replication and franchising, as evidenced by its strategic investment in Belleskin last year, and this year’s strategic investments in Meiyuehui and Kangman, among others.

In addition, Beauty Farm has established a set of service standards to improve efficiency in quality management, organizational optimization, information technology infrastructure, and process management.

Xiuyu Group, established in 2005, operates nearly 1,000 wholly-owned direct-sale lifestyle beauty chain stores. Its business portfolio spans slimming, facial and body care, wellness, and minimally invasive medical aesthetics. Under its umbrella, the medical aesthetics chain brand Chunyu boasts over 30 locations. Earlier this year, the group announced its “New Tech-Beauty Strategy” for 2017 and completed a $100 million Series B financing round led by Morgan Stanley, with participation from New Horizon Capital and Kaixin Investment.

VCBeat believes that, regarding the expansion model of offline brand stores, medical aesthetics involves surgical procedures, which inevitably carry the risk of safety incidents. Any such occurrence would have a significant impact on the brand; therefore, expansion and franchising strategies should be more cautious than those in the life beauty sector.

Unlike medical aesthetics, the mainstream expansion strategy for lifestyle beauty brands is through chain operations. While traditional franchising may be the optimal choice at certain stages, from the perspective of a company’s long-term positioning and business logic, it is foreseeable that those with strong operational performance will generally adopt the direct-operated model.

Medical devices and consumables occupy the upstream segment of the medical aesthetics industry. Device categories primarily include laser aesthetic devices, radiofrequency (RF) aesthetic devices, cosmetic injectors, and liposuction machines. Aesthetic devices generally offer higher profit margins, with most major manufacturers being European or American companies, such as Lumenis and Cynosure from the United States, and Alma Lasers from Israel; domestic Chinese manufacturers include Chirson Laser.

Medical consumables mainly include hyaluronic acid (HA) and Artecoll (a collagen-based filler) for aesthetic filling, botulinum toxin type A for wrinkle reduction, and collagen for moisturizing and repair. Leading companies in this sector include Haohai Biological Technology, Bloomage Biotechnology, Double-Crane Pharmaceutical, Dongbao Biological, and Shanghai Qisheng.

Botulinum toxin products are primarily represented by the domestically produced Lanzhou Hengli and the imported Botox from Allergan (USA). In terms of hyaluronic acid production, the technical barriers are increasingly lower, with a growing number of companies entering the market.

In 2008, Galderma’s Restylane hyaluronic acid filler received approval from the China Food and Drug Administration (CFDA), becoming the first compliant imported hyaluronic acid product in China. Currently, 90% of dermal fillers are made from hyaluronic acid. In 2016, a total of 10 million syringes of hyaluronic acid were sold by accredited hospitals across China.

Hyaluronic acid fillers range in price from 300–400 yuan to tens of thousands of yuan per syringe, covering various market segments, from premium brands like Juvederm to more affordable options such as Haiwei. In 2016, the global hyaluronic acid market reached $1.7 billion, becoming a substantial niche segment.

The focal point of competition between domestically produced and imported hyaluronic acid products lies primarily in their adhesive content, which is the factor that truly impacts consumers. Currently, South Korean brands such as Yvoire continue to hold a tentative lead.

This August, medical aesthetics company SunCro announced that Princess® hyaluronic acid from Austria would fully enter the Chinese market starting in the third quarter of 2017. In addition, the currently compliant hyaluronic acid products in the Chinese market are mainly as follows; it is predictable that the number of registered products will continue to increase. In comparison, Europe already has more than 100 brands.

Four imported hyaluronic acid products: Restylane 2 (Sweden), Juvederm (USA), Yvoire (South Korea), and Elravie (South Korea);

12 Domestic Hyaluronic Acid Brands: Runbaiyan, Haiwei, Shuyan, Deman, Yimei, Bonita, Aifulei, Jiaolan, Xinfeiling, Fascian, Fumeideng, and Bofei.

In July this year, Imeik officially released its prospectus, planning to list on the ChiNext board. From 2014 to 2016, Imeik’s operating revenues were RMB 75.1241 million, RMB 112 million, and RMB 141 million, respectively, with nearly 800 partner hospitals.

The gross profit margins of the company’s three hyaluronic acid products—Bonita, Yimei, and Aifulei—reached 98.23%, 87.8%, and 85.96%, respectively. The combination of low production costs and high end-user prices indirectly reflects the high profitability of the current hyaluronic acid industry. However, with increasing brand diversification in the Chinese market, product prices and corporate profit margins are inevitably poised to decline.

Consolidation and mergers in the upstream market have become a trend. The top four global suppliers of medical aesthetic devices—Cynosure, Inc., Zeltiq Aesthetics, Inc., Syneron Medical Ltd., and Lumenis Ltd.—have all undergone significant mergers and consolidation in recent years.

This September, Sisram Med, the medical aesthetics device manufacturer under Fosun Pharma, successfully listed on the Main Board of The Stock Exchange of Hong Kong Limited. Its primary asset is its subsidiary, Alma Lasers.

The company’s four main product lines are: 1) the Soprano series for hair removal; 2) the Harmony series, a versatile multi-application platform with FDA clearance for up to 65 indications; 3) the Accent series for body contouring and skin tightening within the medical aesthetics portfolio; and 4) the FemiLift series, a minimally invasive medical aesthetic solution for female intimate rejuvenation.

According to HKG那点事, the energy-based medical aesthetic device market was the largest segment of the medical aesthetic device industry in both 2014 and 2016, with revenues reaching $2.7 billion last year. It is projected to remain a rapidly growing segment by 2021, an area in which Sisram is also actively engaged.

Based on 2016 sales revenue, Sisram ranked fifth among global medical aesthetics device suppliers and was the largest supplier of energy-based medical aesthetic devices in the Chinese market.

It can be inferred that in the booming Chinese medical aesthetics market, where devices and consumables constitute a critical and decisive segment, domestic companies’ acquisition of leading foreign brands will become a norm during certain stages of the industry’s development. This trend is driven by capital infusion and influenced by multiple factors, including technological patents and consumers’ trust in foreign brands.