Medical Devices: $15B Capital Injection and Top-10 Supportive Policies Drive Domestic Substitution; Six Core Segments Poised for Breakout – 2017 Year-End Review

On October 28, 2017, the China Association for Drug Administration Research, Social Sciences Academic Press, and the Editorial Committee of the Blue Book of Medical Devices jointly released the Report on the Development of China’s Medical Device Industry (2017).

This is the first blue book on China’s medical device industry. The blue book points out that, from an overall perspective of the past few years, China’s medical device industry has developed rapidly. The growth rate of main business income for manufacturing enterprises above designated size ranged from 11.66% to 22.20%, significantly higher than the growth rate of the national economy during the same period. The research and development and production of high-end medical devices have shown promising trends, with innovative products emerging at an accelerated pace.

So, in what specific aspects did “innovation” manifest itself in China’s medical device industry in 2017? What factors were driving these innovations? VCBeat provides a comprehensive interpretation and analysis for our readers.

New Technology Penetration Accelerates Transformation in the Medical Device Industry

2017 was hailed as a year marked by the convergent development of technologies such as artificial intelligence, big data, and 3D printing. Driven by emerging technologies, rapid technological iterations have intensified competition within the medical device industry. The sector may be on the verge of a new round of transformation; those who possess the most advanced technologies will secure an invincible position in this fierce competition.

1. Artificial Intelligence

In 2017, medical artificial intelligence continued to gain momentum. Traditional medical device manufacturers also targeted this emerging trend, dedicating significant resources to the research and development of AI-powered products, or partnering with AI companies to upgrade their offerings with intelligent capabilities. Among them, industry giants such as GE, Siemens, and United Imaging Healthcare demonstrated the most prominent performance. Notably, United Imaging Healthcare even established a dedicated AI subsidiary with an investment of RMB 300 million, aiming to launch fully intelligent high-end medical imaging and radiotherapy equipment.

However, for most traditional medical device companies, establishing a new department in-house to develop AI products is quite complex. Therefore, some of them choose to collaborate with artificial intelligence companies,Integrate the other party's existing artificial intelligence system into one's own devices to achieve intelligent product upgrades.For example, Medtronic and IBM collaborated to launch diabetes monitoring products; Anhan Medical partnered with IBM to explore the application of artificial intelligence in early screening for gastrointestinal diseases.

2. Internet of Medical Things (IoMT)

In recent years, Internet of Things (IoT) technology has provided momentum for the development of the digital healthcare industry. In an era where the internet and smartphones are ubiquitous, people can not only manage their daily lives through apps or cloud-based products but also monitor and manage their health via a range of medical IoT devices.

The Internet of Medical Things (IoMT) is the convergence of medical devices, communications, and information technology. Device-centric, it connects stakeholders in healthcare delivery through networked infrastructure. Patients can leverage extensive health data generated by these devices to manage their medication regimens, dosages, and reminders. Meanwhile, physicians can track and review patients’ health data and medical records via the cloud at any time, thereby reducing follow-up costs. It can be said thatThe Internet of Medical Things is preventing and even participating in medicine, while providing support for evidence-based medicine.

According to statistics, the global market size of connected medical devices has currently reached $9 billion and is growing rapidly at a rate of 16%. It is expected that the market size will exceed $23 billion by 2020.

3. Healthcare Information Technology

Medical devices serve as the primary entry point for collecting patient health data. Consequently, medical device manufacturers that secure these critical access points gain a first-mover advantage.They began to expand into medical informatization, health big data, and chronic disease management platforms to enhance the company's service capabilities.

Meanwhile,"Informatization has gradually played a crucial role in the procurement, maintenance, and asset management of medical devices."Traditional medical device management is an extremely cumbersome undertaking, requiring staff to expend considerable effort in collecting and analyzing data on funding, utilization, maintenance status, and specific details of medical devices. The application of information technology has streamlined the medical device management process, enabling healthcare professionals to quickly and accurately retrieve relevant information and data via computers.

Thus, healthcare informatization has also ushered in development opportunities for third-party service providers dedicated to asset management and equipment maintenance.

4. 3D Printing Technology

With the development and maturation of 3D printing technology, its applications in the medical device sector have garnered widespread attention in recent years. The 3D printing industry for orthopedic devices has seen initial clinical adoption in recent years, exemplified by Stryker’s 3D-printed knee replacements, AK Medical’s 3D-printed hip joints, and Ketai Madi’s 3D-printed critical bone structures.

Another major application area of 3D printing is dentistry. Among the first batch of approved projects under the National Key R&D Program during the 13th Five-Year Plan period is the project led by Peking University School and Hospital of Stomatology, titled “Research on Key Technologies for Additive Manufacturing of Personalized Dental Implants and Maxillofacial and Temporomandibular Joint Prostheses,” which is scheduled to enter clinical trials by the end of this year. Meanwhile, international medical giants such as BEGO and Planmeca have launched 3D printing equipment suitable for dental applications, and systems from 3D Systems and EOS have also been initially introduced into hospitals in China. In October 2017, GE Healthcare opened its first 3D printing laboratory in Uppsala, Sweden, to accelerate the rollout of innovative new products for the healthcare industry.

Beyond orthopedic and dental implant applications, 3D printing has achieved breakthroughs in the fields of cells, living tissues, surgical guides, surgical planning models, and rehabilitation medical devices.Current achievements indicate that patients in urgent need of organ transplants may soon have easy access to livers, hearts, and other organs; this long-awaited technological breakthrough for humanity is no longer out of reach.

5. Sensors + Chips

Industry insiders believe that over the next decade, every subsector—from diagnosis and monitoring to treatment and rehabilitation—will usher in an era of intelligence. Furthermore, driven by advancements in technologies such as sensors and microfluidics, the trend toward miniaturization and intelligentization within the medical device industry is expected to become increasingly prominent.

Smart medical devices can currently be divided into two main categories: wearable devices and medical robots.VCBeat predicts that wearable devices will become the “smartphones” of the healthcare sector, directly connecting medical device manufacturers with patients, fostering strong user stickiness, and serving as an entry point to the healthcare ecosystem. Meanwhile, medical robots boast even broader development prospects; whether in surgery or rehabilitation therapy, they have already demonstrated performance capabilities far surpassing those of human practitioners.

Business Model Innovation: Companies Are No Longer Pure Equipment Manufacturers

Ultimately, technological innovation aims to better meet customer needs. In the current patient-centered healthcare landscape, companies can no longer prioritize profits alone while neglecting improvements in service quality. This principle also applies to the medical device industry, which is part of the manufacturing sector. Amidst intense competition, enterprises are exploring new business models to find fresh pathways for growth.

From “Equipment Manufacturer” to “Provider of Comprehensive Equipment Solutions”

Companies have evolved from initially manufacturing devices for treating a single disease category, to producing a range of devices for that disease, then investing in other healthcare institutions related to the condition, and finally refining their product portfolios to become comprehensive solution providers for therapeutic equipment targeting that specific disease.

Among them, manufacturers of smart wearable devices stand out the most. They have gradually evolved from being mere device manufacturers in the early days into“Hardware + Software + Cloud Services” Integrated Solution Provider for Smart Wearables. By leveraging self-developed and manufactured smart wearable devices capable of real-time monitoring and transmitting user data to the cloud, and by relying on big data platforms such as mobile health services, companies collect and analyze user data to ultimately provide customers with health management services.

For example, the leading player in China's mobile health sector for diabetes—Mastering Diabetes. This is a diabetes management service connectivity platform developed based on an intelligent data engine, where physicians and medical assistants collaborate to provide patients with personalized, continuous, and integrated diabetes care spanning both in-hospital and out-of-hospital settings.

Zhangkong Diabetes’s three-dimensional management model, centered on a smart engine and integrating “hardware + services + cloud platform,” serves as an industry benchmark. The Zhangkong Diabetes platform leverages devices for complication screening, blood glucose meters, and continuous glucose monitoring systems to collect patients’ test data in real time and upload it to the cloud. By employing big data and artificial intelligence technologies for in-depth data mining and analysis, and integrating these insights with patients’ treatment and monitoring records, the platform generates comprehensive test reports. These reports assist physicians in making accurate clinical decisions and enable the provision of personalized care plans for diabetes and its complications.

From Products to Services: Third-Party Medical Device Services Experience Explosive Growth

Transitioning from products to services is nearly the standard trajectory for development across all industries. Apple’s “product + service” business model offers significant lessons for the future development of various sectors, including the medical device industry. In the future, companies focused solely on the manufacturing and sales of devices will struggle to survive; only those that continuously deliver higher-quality services will be able to sustain growth.

Medical device manufacturers previously relied on the production and sale of medical devices, resulting in a singular business model with limited value-added potential. With the continuous advancement of healthcare system reforms in China, various unreasonable policy restrictions on medical institutions and healthcare services have been gradually lifted.It has become possible for manufacturing enterprises to provide services based on the medical devices they produce, which will effectively enhance the value-added of their business operations and diversify their business lines.For instance, leveraging glucometers to build a chronic disease management platform can provide long-term services to patients; relying on diagnostic equipment to establish independent diagnostic centers and health examination centers can alleviate hospital pressure and improve patients’ medical experience.

Dian Diagnostics is a typical case of service-oriented transformation. Prior to 2008, the company’s primary revenue source was in vitro diagnostic (IVD) products. Over the years, the proportion of revenue from diagnostic services has steadily increased, transforming it into an integrated comprehensive diagnostics company that combines both products and services.

From Traditional Channel Sales to Online Direct Sales: Medical Device Sales Models Seek Breakthroughs

Ultimately, the goal of enterprises in delivering high-quality products and services is to drive sales. The medical device industry has long been characterized by its rigorous and conservative nature. Most companies rely on multi-tiered distributors to sell their products, a model plagued by excessive intermediaries that lead to inefficiencies and inflated sales expenses, significantly squeezing manufacturers’ profit margins. More importantly,The presence of distributors between medical device manufacturers and end users inevitably hinders deeper collaboration with covered hospitals, thereby impeding the development of strong brands and platforms.

However, in recent years, with the development of the internet and the rise of e-commerce, medical device manufacturers have begun to make changes. Gradually, we have seen some miniaturized home-use medical devices appear on major e-commerce platforms. In 2017, even large medical device manufacturers expanded their businesses online, engaging inOnline Direct Sales, to address the pain points of traditional sales models, such as complex processes, lengthy timelines, and high costs.

Although this novel sales model for medical devices appears somewhat risky, if successful, it will help increase corporate profit margins, generate greater profits, achieve deep penetration among hospitals and patients, and establish a robust ecosystem.

Medical Devices Become the New Darling of Capital, with Import Substitution Just Around the Corner

Medical devices have long become a strategic focus for numerous companies. In recent years, physicians have increasingly recognized the critical role of medical devices in diagnosis and treatment, while national policies have progressively strengthened support for the sector. As the medical device industry gains greater attention, it has swiftly emerged as a new favorite among investors.

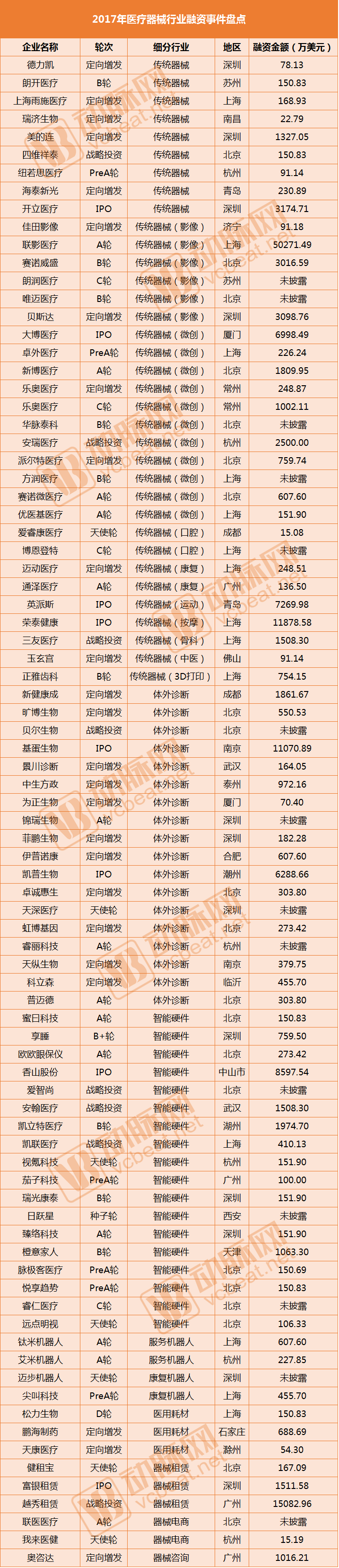

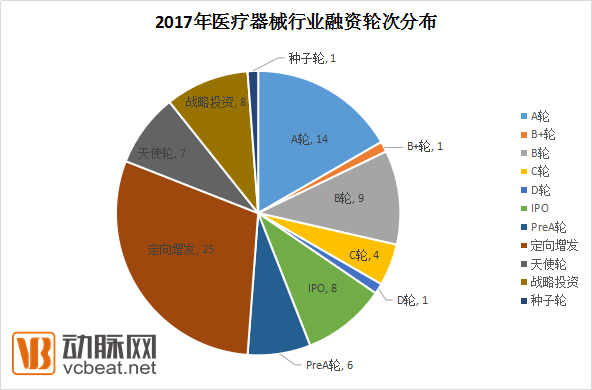

According to incomplete statistics from VCBeat, the medical device industry witnessed a total of 84 financing events (including 8 IPOs) in 2017, with a cumulative amount nearing $1.6 billion (approximately RMB 10 billion). Among these, the four sectors of in vitro diagnostics (IVD), smart hardware, minimally invasive medical devices, and medical imaging equipment demonstrated the most prominent performance. Additionally, medical consumables, medical device e-commerce, and medical device financial leasing also experienced varying degrees of development.

After in-depth analysis by reporters, this wave of capital primarily flowed into niche sectors such as in vitro diagnostics, radiotherapy, medical imaging, ultrasound equipment, medical robots, endoscopic minimally invasive devices, rehabilitation medicine, and home medical devices.Geographically, Beijing, Shanghai, and Guangzhou continue to hold a dominant advantage. Beijing had the highest number of companies securing financing, with 21 firms, followed closely by Shanghai and Shenzhen, with 14 and 12 companies, respectively.

In 2017, the influx of various domestic capital sources reflected the promising prospects of the Chinese medical device industry. According to reporters, diagnostic equipment and consumables such as electrocardiographs, ultrasound diagnostic systems, and coronary stents have gradually initiated or achieved import substitution in clinical settings. The product quality and performance of domestic medical device manufacturers, represented by Lepu Medical, Wandong Medical, Mindray, United Imaging, and Yuwell, have been increasingly recognized by the market. The gap between high-end domestic medical devices and imported brands is narrowing, making the replacement of imports with domestic products imminent.

On September 15, 2017, United Imaging Healthcare successfully completed a Series A financing round of RMB 3.333 billion, setting a record for the largest single private equity financing in China’s medical device industry to date. As a provider of high-end medical equipment and healthcare informatics solutions, United Imaging Healthcare’s successful fundraising not only raised its valuation to RMB 33.333 billion but also highlighted the promise of domestically produced high-end medical equipment.

Furthermore, in terms of financing rounds, there were numerous private placements by listed companies, as well as Series A and pre-Series A projects in 2017. Meanwhile, a total of eight medical device companies completed their initial public offerings (IPOs) in 2017, namely Sonoscape Medical, Double Medical Technology, Impulse Sports, Rongtai Health, Basecare Medical, Hybribio, Xiangshan Shares, and Fuyin Leasing. This indicates that, in addition to capital favoring early-stage medical device projects, the capital market was also quite vibrant this year.

Policy Tailwinds: Broad Prospects for Innovative Medical Devices

Beyond the continuous technological breakthroughs achieved by domestically produced medical devices, another key reason for capital’s strong preference for the medical device industry is the safeguard provided by national policies.

In recent years, to break the monopoly held by foreign companies, the Chinese government has continuously introduced new policies and measures to encourage investment and ensure the healthy development of the medical device industry. VCBeat provides a brief analysis of the top ten medical device-related policies issued in 2017.

From these policies, it is evident that the state primarily focuses on regulation and innovation to encourage the localization of medical devices and achieve standardized development.

First,In terms of regulation, regulatory authorities have continuously issued new regulations aimed at establishing a sound medical device regulatory framework, eliminating non-compliant enterprises and low-quality medical devices; ensuring the high quality and safety of medical devices in China, with industry concentration steadily increasing and long-term trends remaining positive.

Secondly,In terms of innovationA series of policies, centered on the “Opinions on Deepening the Reform of the Review and Approval System to Encourage Innovation in Drugs and Medical Devices” and the “13th Five-Year Plan for Scientific and Technological Innovation in Medical Devices,” focus primarily on high-end imaging equipment, wearable devices, medical robots, and “Internet + Healthcare.” These initiatives aim to encourage the Chinese medical device industry to pursue technological innovation and completely move away from its former position at the bottom of the value chain, which relied on low-end products yielding slim profit margins.

Meanwhile, the state has also established a “green channel” for domestically produced innovative medical devices to streamline procedures and accelerate approval, thereby vigorously promoting R&D innovation in the medical device sector and catching up with international standards.

Driven by favorable policies, the overall revenue and profit growth rates of China’s medical device industry have now ranked first among all its subsectors.According to available data, the medical device industry achieved a revenue growth rate of 13% and a profit growth rate of 32% in 2016. Both metrics ranked first among all sub-sectors. Notably, the profit growth rate was significantly higher than the overall industry average of 15.57%, as well as the 5.34% recorded during the same period the previous year.

Eight Major Trends in the Future Medical Device Industry: Six Core Sectors Poised for Breakout Growth

Based on an analysis of the current state of China’s medical device industry in 2017, VCBeat identifies eight major future trends driven by the convergence of technology and services.

1. The market for the medical device industry will continue to expand.With the rapid development of China’s economy and society, the total annual sales of medical devices in China are projected to exceed RMB 700 billion by 2020, and the growth rate of China’s medical device industry is expected to remain at an average annual increase of more than 10% over the next decade.

2. China's mid- to low-end medical device market will expand rapidly.Currently, the level of medical equipment provision in China's primary healthcare institutions is relatively low, with a significant gap; there is an urgent need for "upgrading and replacement" and "filling the gap."During the 13th Five-Year Plan period, healthcare reform prioritized the implementation of a tiered diagnosis and treatment system. Enhancing equipment allocation in primary healthcare institutions became a key task in 2017, driving rapid growth in the market for low- to mid-end medical devices.

3. Domestically developed, independently innovated medical devices will continue to emerge.With advancements in science and technology, particularly the implementation of national policies encouraging the research, development, and production of innovative medical devices, as well as the pull from growing healthcare demands, independently innovated medical devices in China will emerge at an accelerated pace. The market share of domestically produced high-end medical devices will gradually increase, and the dominant position of multinational companies in the domestic high-end medical device market will be progressively broken. Domestic medical device products will break through from the low-to-mid-end market to the high-end market. Meanwhile, technological upgrades will also drive the consumption upgrade of high-value consumables in medical institutions.

4. Imports and exports of medical devices will continue to increase.Based on the trends in China's medical device imports and exports, the total trade volume is expected to increase further. Imports of medical devices will continue to grow steadily, remaining dominated by high-end imaging products. Meanwhile, export value will continue to rise, with an increasing share attributed to high-end medical devices, leading to a gradual improvement in the product mix of exported medical devices.

5. Mergers and acquisitions, as well as restructuring, in the medical device industry will accelerate.In China, both horizontal and vertical integration through mergers, alliances, and restructurings will emerge among medical device companies. Production will increasingly concentrate in large-scale medical device enterprises, while small and medium-sized enterprises (SMEs) will either focus their efforts on the research and development of specific devices or certain device components, or be acquired and restructured by larger medical device manufacturers.It is predicted that in the next 5–10 years, China’s “aircraft carrier” of the medical device industry will most likely emerge from the Pearl River Delta, the Yangtze River Delta, or the Bohai Rim region.

6. Home-use medical devices will flourish.Amid the trend toward miniaturization and intelligence in medical devices, there is a growing movement to downsize large hospital equipment and imbue traditionally “dumb” devices with smart capabilities for home use. As a result, China’s medical device sector is witnessing the emergence of a new growth opportunity:Smart Home Medical DevicesAccording to statistics from relevant institutions, China's home medical device market will reach RMB 61 billion in 2017.

7. Third-party services based on medical devices will accelerate their rise.A series of policy documents have clarified that medical imaging, laboratory testing, blood purification, and pathology centers can operate as independent medical institutions. It is foreseeable that emerging intensive service models based on medical devices—such as third-party diagnostics, examinations, pathology, logistics, sterilization, maintenance, and equipment bundling—will accelerate in the future.

8. The six core sectors hold immense potential for development and may see major breakthroughs in the future. These six sectors are IVD (including POCT), high-value consumables, medical robots, home medical devices, 3D-printed medical devices, and medical imaging centers.

If you are interested in “Intelligent Medical Equipment (Devices),” you are welcome to register for the event to be held in Beijing from December 15 to 17.“2017 Future Healthcare Top 100” Forum, VCBeat and Zhizhong jointly create“Parallel Forum on Intelligent Medical Devices (Equipment)”, inviting renowned industry experts and multiple corporate executives to discuss “New Trends in the Development of the Medical Device Industry—Policy, Regulatory, and Channel Changes”. Long-press the image below to scan the QR code and register.