China's Diabetes Drug Market Reaches RMB 47.5 Billion, with Retail Pharmacies Accounting for 23.7% and Foreign-Origin Brands Dominating Top 10

Diabetes is a common endocrine and metabolic disorder, characterized by fundamental pathological features of insufficient insulin secretion or peripheral tissue insensitivity to insulin, leading to a series of metabolic disturbances in carbohydrates, proteins, and fats.

According to data from the International Diabetes Federation (IDF), approximately 415 million people worldwide had diabetes in 2015. China has the largest number of diabetes patients globally, with around 110 million cases, accounting for approximately 10% of the total adult population.

November 14, 2017 marked the 11th United Nations Diabetes Day. Sinohealth CMH, a full-channel market data research institution under Sinohealth Information, has compiled national retail pharmacy market data on diabetes medications and released it on the VCBeat platform (WeChat: vcbeat). This initiative aims to provide market-based insights to help the healthcare industry and the general public better understand the prevalence and treatment landscape of diabetes.

The Market Size of Diabetes Drugs Continues to Expand

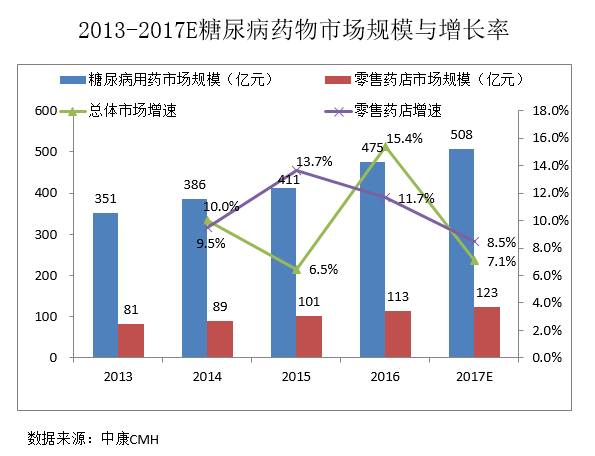

According to data from Zhongkang CMH, the overall market size for diabetes medications reached RMB 47.5 billion in 2016, representing a year-on-year increase of 15.4%. Of this, the market size through the retail pharmacy channel amounted to RMB 11.3 billion, accounting for 23.7% of the total market. This segment grew by 11.7% compared with 2015, a growth rate slightly lower than the overall market’s 15.4%.

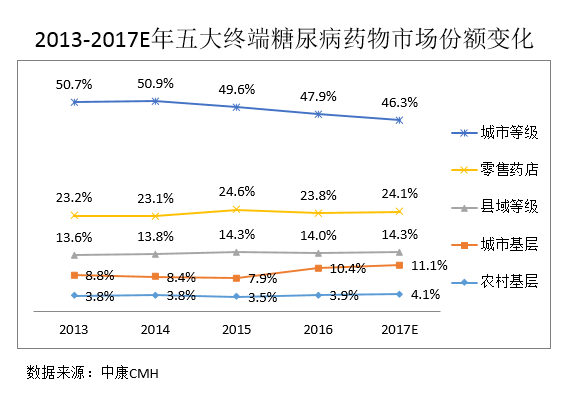

Tier-1/2 city hospitals and county-level hospitals remain the primary markets for diabetes medications, accounting for a combined share of 60.6%. The market share of primary care institutions has increased, benefiting from the comprehensive promotion of tiered diagnosis and treatment. Retail pharmacies account for 24% of the market share. With the gradual implementation of policies such as medical insurance cost containment, which restricts the growth of the hospital market, and the advancement of policies like the separation of prescribing and dispensing and the outflow of prescriptions, the market share of hospital channels has been declining year by year. In 2017, the retail pharmacy segment for diabetes medications is expected to maintain its growth trend, with a projected growth rate higher than that of the overall market.

The prevalence of diabetes in China has been increasing year by year, resulting from the interplay of multiple factors, including genetic predisposition, improved living standards, sedentary lifestyles with insufficient physical activity, and population aging. The rising number of patients, coupled with heightened awareness of self-care, has expanded market demand for antidiabetic medications, leading to a steady upward trend in China’s diabetes drug market in recent years.

Categories and Proportions of Diabetes Medications

Diabetes medications include oral hypoglycemic agents, insulin and its analogs, and other non-insulin hypoglycemic drugs.

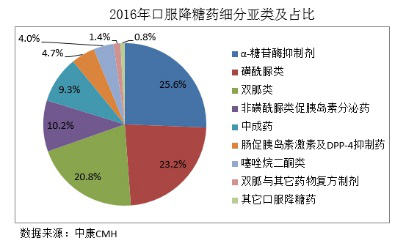

Type 2 diabetes is the most prevalent form, accounting for approximately 90% of cases. Unlike type 1 diabetes, which requires continuous insulin administration, patients with type 2 diabetes primarily manage their blood glucose levels through oral hypoglycemic agents. In 2016, the market size of oral hypoglycemic agents in retail pharmacies reached RMB 7.24 billion, representing 64% of the overall diabetes medication market share and marking a year-on-year growth of 13%.

According to monitoring data from Zhongkang CMH, chemical drugs dominate the oral hypoglycemic agent market, accounting for 89.9% of the share, while traditional Chinese medicine (TCM) proprietary medicines account for 9.3%. In terms of subcategories of oral hypoglycemic agents, α-glucosidase inhibitors held the largest market share in 2016 at 25.6%, followed by sulfonylureas at 23.2% and biguanides at 20.8%.

α-Glucosidase inhibitors lower postprandial blood glucose by delaying the breakdown of sucrose, starch, and maltose into glucose in the small intestine. The main agents include acarbose, voglibose, and miglitol.

Acarbose has maintained a dominant position in the oral antidiabetic drug category at retail pharmacies for many years. According to CMH monitoring data, the market size of alpha-glucosidase inhibitors in retail pharmacies reached RMB 1.9 billion in 2016, with acarbose accounting for as high as 90%, while voglibose accounted for only 7%. Bayer (Glucobay, with a 73% share) is the leading manufacturer in the acarbose market, followed by Huadong Medicine (Carboplus) and Luye Baoguang (Beixi).

Sulfonylureas lower blood glucose levels by stimulating insulin secretion from pancreatic beta cells, thereby increasing endogenous insulin levels.

Sulfonylureas constitute the second-largest subclass of oral hypoglycemic agents. In 2016, the market size for sulfonylureas in retail pharmacies reached RMB 1.68 billion. This subclass comprises a wide variety of products; among them, gliclazide, glimepiride, glipizide, and gliquidone each achieved annual sales exceeding RMB 100 million in retail pharmacies in 2016, collectively accounting for 99% of the total market share. Glimepiride, a third-generation long-acting sulfonylurea antidiabetic agent, demonstrates improved safety and efficacy, and its market share is rising rapidly.

Biguanides are the first-line glucose-lowering agents for children and patients with type 2 diabetes who are overweight or obese; in addition to lowering blood glucose, they also confer cardiovascular protective benefits. The primary agent in this class is metformin.

In 2016, sales of metformin products at the retail pharmacy terminal reached RMB 1.5 billion, representing a year-on-year increase of 13%. There are numerous manufacturers of this product, with the top five manufacturers accounting for a combined market share of 62% in 2016, indicating a high level of manufacturer concentration. Among them, Bristol-Myers Squibb held the largest market share, exceeding 40%, followed by Guizhou Tian’an and Hengrui Medicine.

In addition, DPP-4 inhibitors achieved a growth rate of 39% in 2016, making them one of the fastest-growing categories, with the retail pharmacy market size reaching RMB 300 million. Currently, all five DPP-4 inhibitors marketed in China are exclusive products; agents such as sitagliptin and saxagliptin have been included in the 2017 National Reimbursement Drug List (NRDL) for the treatment of type 2 diabetes. It is anticipated that their inclusion in the NRDL will drive substantial growth for this category. Merck’s exclusive product, sitagliptin (Januvia), demonstrated the strongest market performance, accounting for 64% of the DPP-4 inhibitor market share in retail pharmacies in 2016. Following its launch, the fixed-dose combination product Janumet (sitagliptin/metformin) has also shown a consistent year-on-year increase in its market share within the combination drug segment.

Competitive Landscape of Oral Hypoglycemic Agents

Top 10 Best-Selling Oral Hypoglycemic Agents

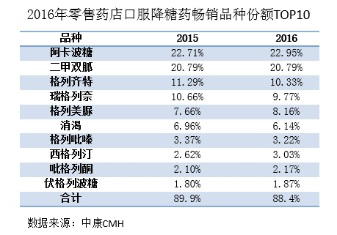

According to monitoring data from Sinocom CMH, the top 10 best-selling products in retail pharmacies accounted for 88.4% of the market share in 2016, indicating a high level of market concentration. All of the top 10 products were single-ingredient formulations, whereas combination formulations, which are relatively more efficient and convenient, have significant growth potential in retail pharmacies.

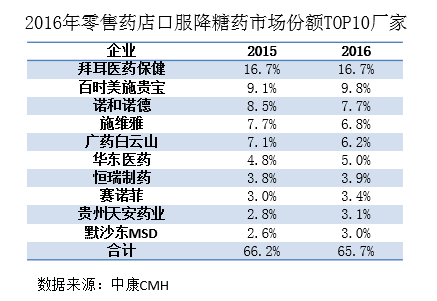

Top 10 Manufacturers by Market Share in Oral Hypoglycemic Agents

According to monitoring data from Zhongkang CMH, domestic and foreign enterprises each hold half of the market for oral hypoglycemic agents in the retail pharmacy channel. In 2016, foreign enterprises had a slight edge, capturing 51% of the market share, while domestic enterprises accounted for 49%.

Among the top 10 manufacturers by market share, domestic companies lag slightly behind foreign companies. According to monitoring data from Zhongkang CMH, in 2016, the combined market share of the top 10 manufacturers of oral hypoglycemic agents in retail pharmacies was 65.7%, indicating a high level of market concentration. Of these, six were foreign companies with a combined share of 47.5%, while four were domestic companies with a combined share of 18.2%. In the diabetes market, domestic companies account for half of the total market share, thanks to the large number of manufacturers, each holding a relatively small share, whereas the situation for foreign companies is the opposite.

Performance of the Top 10 Brands in the Oral Hypoglycemic Drug Market Share

In 2016, the top 10 brands of oral hypoglycemic agents in retail pharmacies accounted for 59% of the market share. Among them, there were 7 foreign brands with a combined market share of 46%, occupying a relatively advantageous position; domestic brands were relatively weak, with only 3 brands and a combined market share of 13%.

The top-performing brand is Bayer’s Glucobay, which has ranked first among oral hypoglycemic agents for consecutive years. It is followed by Bristol-Myers Squibb’s Glucophage and Novo Nordisk’s Novonorm. Guangzhou Pharmaceutical Holdings’ Xiaoke Wan is the only traditional Chinese medicine product in the TOP 10 and the domestically produced hypoglycemic agent with the largest share in retail pharmacies. Other domestic hypoglycemic brands include Huadong Medicine’s Acarbose (Kaboping) and Guizhou Tian’an’s Fulaidi.