Rehabilitation Industry: A Trillion-Yuan Market Only 20% Saturated, Specialty Hospitals Emerge as the Next Investment Hotspot, and Community-Based Rehabilitation Holds Immense Potential [2017 Year-End Review]

In 2017, among the more than 30 niche sectors monitored by VCBeat, the rehabilitation industry did not deliver standout performance. However, after covering numerous startup ventures, this once-overlooked field began to show signs of growth. With the rollout of a series of policies and encouragement for private healthcare provision, many investors extended olive branches to entrepreneurs in this sector through VCBeat.

According to the "Report on Development Prospects and Investment Forecast Analysis of China's Rehabilitation Medical Industry" by Qianzhan Industry Research Institute, the market size of China's rehabilitation medical industry reached approximately RMB 27 billion in 2016. As China continues to deepen healthcare service reforms, improve the three-tier rehabilitation medical system, and further implement medical insurance policies related to rehabilitation services, the rehabilitation medical industry is poised for explosive growth in 2017. It is projected that by 2020, the market size will exceed RMB 70 billion, with a compound annual growth rate (CAGR) of no less than 20%, thereby establishing another trillion-yuan market.

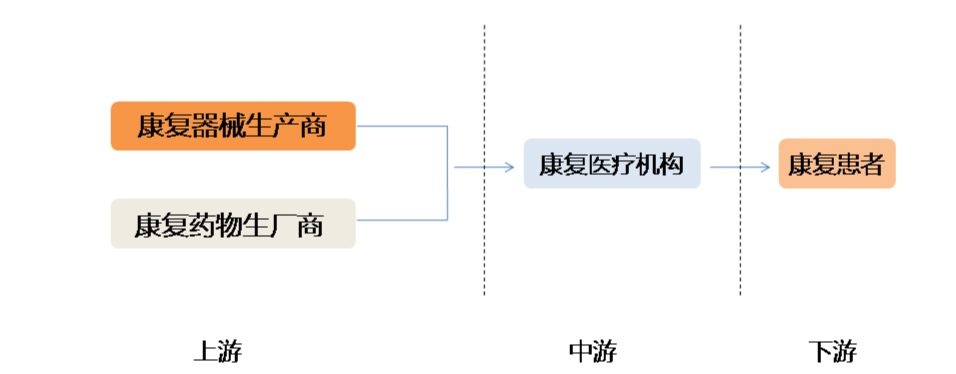

First, let us examine the structure of the industrial chain in the rehabilitation medicine sector:

In the upstream rehabilitation equipment sector, the mid-to-high-end market is monopolized by European and American brands, while domestic manufacturers hold a certain market share only in the low-to-mid-end segment.

Rehabilitation services in the midstream sector remain on the periphery, with no unified industry standards yet established and an industrial landscape still to take shape.

As for the downstream patient side, rehabilitation medicine, as an important component of the modern medical “prevention, clinical treatment, and rehabilitation” trinity, is still in the stage of popularization among institutional users in China, and the rehabilitation market, one of the hospital aftermarkets, has yet to be fully tapped.

Whether driven by national policy or capital investment, a review of the key events and trends in the rehabilitation sector in 2017 reveals that the industry’s trajectory was largely positive. Therefore, VCBeat intends to analyze the 2017 rehabilitation healthcare market from three perspectives: policy, capital, and technology.

Policy Approval Eases, with Private Capital Access Becoming Key

In May 2017, the General Office of the State Council issued the “Opinions on Supporting Social Forces in Providing Multi-level and Diversified Medical Services,” encouraging social forces to delve into specialized medical services and other niche sectors. The policy promotes the accelerated development of a number of competitive branded service providers across various specialties, as well as in rehabilitation, nursing, and health examination services. This signifies renewed national-level support for the establishment of rehabilitation medical institutions, positioning rehabilitation healthcare as the next major opportunity for medical investment.

In May 2017, Zhao Yong, Deputy Director of the General Administration of Sport of China, emphasized that “the integration of sports and medicine is an urgent need for promoting a health revolution and addressing public concerns.” The deep integration of sports and medicine has become a key measure to help the general population avoid illness or reduce its incidence. “Sports-medicine integration” has emerged as a critical pathway and development direction in exercise rehabilitation and rehabilitation medicine.

In August 2017, Jiao Yahui, Deputy Director of the Bureau of Medical Administration and Hospital Management under the National Health and Family Planning Commission (NHFPC), announced at a routine press conference held by the NHFPC that five additional categories of independent medical institutions would be introduced. Alongside nursing centers, sterile supply centers, small and medium-sized ophthalmic hospitals, and health examination centers, rehabilitation medical centers were also included in this expansion.

In August 2017, the National Health and Family Planning Commission issued the “Notice on Deepening the Reform of ‘Streamlining Administration, Delegating Power, and Improving Services’ to Stimulate Investment Vitality in the Medical Field” (Guo Wei Fa Zhi Fa [2017] No. 43), which called for encouraging social forces to establish rehabilitation medical institutions and nursing institutions, thereby bridging the “last mile” in extending professional rehabilitation medical services and clinical nursing services to community-based and home-based rehabilitation and care.

In November 2017, the National Health and Family Planning Commission organized the formulation of the Basic Standards for Rehabilitation Medical Centers (Trial) and the Basic Standards for Nursing Centers (Trial), along with their respective management specifications. The release of these “dual-center” standards explicitly encourages the group-based and chain-operation models for rehabilitation medical centers and nursing centers, aiming to establish standardized management and service models. Furthermore, priority in establishment approval will be granted to applications for group-based or chain-operated rehabilitation medical centers and nursing centers.

The trend toward chain-based and group-oriented development is attracting well-capitalized consortia to enter the market. For companies that have already established a presence in rehabilitation hospitals, rehabilitation services target not only the nearly 130 million people in China with rehabilitation needs but also the home-based elderly care population, which accounts for 90% of the 230 million individuals requiring eldercare. Encouraging private sector participation in the development of rehabilitation medical centers is expected to bring sustainable vitality to community-based rehabilitation through replicable operational models.

As early as June last year, nine departments, including the Beijing Municipal Development and Reform Commission, jointly issued the “Guiding Opinions on Strengthening the Construction of Beijing’s Rehabilitation Medical Service System” (hereinafter referred to as the “Guiding Opinions”), launching the first batch of public medical institutions to transform into rehabilitation facilities, including six institutions such as the Zhanlanlu Hospital in Xicheng District. The policy specifies that certain public hospitals in Beijing will transition into rehabilitation hospitals, and some therapeutic beds in these hospitals will be converted into rehabilitation beds.

In early 2017, Beijing launched the second batch of six public hospitals transitioning into rehabilitation institutions. It has been reported that by 2018, Beijing will initiate the third batch of public hospital transformations. Once the full list of 18 public hospitals across all three batches is announced, each district in Beijing will have one to two public rehabilitation hospitals.

Policy guidance has created a strategic window of opportunity for the rehabilitation sector. For enterprises that have already established integrated medical and elderly care models, this represents an opportunity to extend and expand their business models, while companies that were previously on the sidelines are rapidly entering the rehabilitation field.

Capital in the Rehabilitation Market Mostly Holds Cash and Adopts a Wait-and-See Approach

2017 Financing Events in the Rehabilitation Sector

In 2017, a total of 12 financing deals were completed in the rehabilitation sector. According to publicly disclosed data, the total amount was approximately USD 194 million (equivalent to RMB 1.286 billion). Notably, RMB 1 billion of this sum was contributed by Gulian Medical. The remaining RMB 286 million in financing was shared among 11 companies.

Among the aforementioned financing events, ten companies were at stages prior to Series A, primarily concentrated in the angel and Series A rounds. Of these, enterprises in the upstream segment of the industry chain—specifically those focused on rehabilitation equipment and intelligent hardware—and those in the midstream segment providing rehabilitation services each accounted for half of the list. Overall, this indicates that capital remains relatively cautious about investing in immature business models within the rehabilitation sector, and the market has not yet exhibited a trend of explosive growth.

The development of enterprises in this sector is not yet mature. On one hand, the weak foundation of China’s rehabilitation market has kept most capital in a wait-and-see mode; on the other hand, apart from privately initiated establishments, most specialized rehabilitation hospitals are transformed from public hospitals, into which private capital cannot be injected.

On August 9, 2017, New Frontier Health Group announced an additional strategic investment of RMB 1 billion to support the expansion of Guilian Healthcare’s post-acute care service platform. In September 2017, Chengdu Guilian Rehabilitation Hospital commenced trial operations. With a registered capital of RMB 100 million, a floor area of approximately 13,000 square meters, and a planned capacity of 218 beds, it is set to become the largest international specialized rehabilitation hospital in Southwest China. Guilian Healthcare’s substantial financing round emerged as a major event in the rehabilitation sector that year, with specialized rehabilitation hospitals becoming a widely favored market entry model.

Capital Influx into the Rehabilitation Medical Sector

As early as May 2017, Taikang Insurance Group announced that Beijing Taikang Yanyuan Rehabilitation Hospital had introduced the U.S. GRS rehabilitation model. Liu Tingjun, Vice President of Taikang Insurance Group and CEO of Taikang Community, stated in a media interview, “Rehabilitation hospitals represent excellent investment opportunities.”

Social Capital Favors Specialized Rehabilitation Hospitals for Three Reasons:

First, the “barrier to entry” for rehabilitation medicine is relatively low, as evidenced by its lower dependence on physicians and large-scale medical equipment, smaller capital investment required for individual hospitals, and lower medical risks, making it suitable for private capital investment.

Second, if rehabilitation medical services can accommodate patients in the post-acute phase after hospital discharge, they can effectively alleviate the persistent challenges of difficult and costly access to care within the public healthcare system, thereby creating a win-win model.

Third, many public secondary hospitals are seeking transformation. Following the implementation of the zero-markup policy on pharmaceuticals under the new healthcare reform, secondary hospitals—where pharmaceutical sales previously accounted for 70%–80% of revenue—are now struggling to survive in a precarious position and need to identify new revenue streams. Although the average daily treatment cost in rehabilitation medicine is lower than that in general hospitals, its longer rehabilitation cycles and relatively low capital investment enable it to achieve net profit margins of approximately 15%–20%.

In October 2017, Samsung Medical (601567.SH) announced that its subsidiary, Ningbo Mingzhou Hospital Co., Ltd. (“Mingzhou Hospital”), planned to acquire 100% equity interest in Zhejiang Mingzhou Rehabilitation Hospital Co., Ltd. (“Mingzhou Rehabilitation Hospital”) for RMB 320 million in cash. Following the acquisition, Mingzhou Hospital will hold 100% of the equity in Mingzhou Rehabilitation Hospital. In the first half of the year, Mingzhou Rehabilitation Hospital reported operating revenue of RMB 45.58 million and net profit of RMB 6.23 million.

In July 2017, Shanghai Yongci Rehabilitation Hospital officially opened, marking the formal operation of Haier’s first project in its strategic layout for the big health industry. According to Hu Zhouqing, head of a micro-enterprise (internal venture division) under Haier’s Health and Elderly Care Platform, who disclosed information in a media interview, Haier’s medical business aims to build China’s largest rehabilitation platform integrating online and offline services, targeting 10,000 beds and RMB 2.5 billion in revenue by 2020.

Notably, in April 2016, real estate giant Vanke also announced its entry into the rehabilitation healthcare sector, launching its first medical project in Guangzhou—Vanke Rehabilitation Hospital. Located in the core area of Smart City in Tianhe District, Guangzhou, the hospital occupies a land area of 6,000 square meters, with a total operational floor space of 15,000 square meters, and was built to meet the standards for a Tier-II hospital. At the time, in an effort to attract medical talent, Vanke spared no expense, offering annual salaries ranging from RMB 300,000 to RMB 1.2 million for positions such as hospital director, chief of surgery, chief of internal medicine, and rehabilitation physicians.

According to incomplete statistics from VCBeat, 14 listed companies are involved in the rehabilitation sector.

Statistics on Listed Companies Entering the Rehabilitation Sector

Social capital invests in rehabilitation medical services through flexible and diverse approaches, primarily including the establishment of new facilities, acquisitions, and entrusted management of rehabilitation hospitals. Among these, cooperation between social capital and public hospitals to jointly establish rehabilitation hospitals has become a mainstream win-win model. The investment required for social capital to enter into such partnerships with public hospitals is lower than the cost of building new comprehensive hospitals, shortens the payback period, and offers a high cost-effectiveness ratio.

At the national level, there is encouragement for social capital to invest in healthcare. Considering private capital’s preference for addressing gaps in the medical system and its advantage in establishing specialized hospitals, the rehabilitation medicine sector is poised to experience a surge in investment.

Rehabilitation Aids and Home Medical Devices Emerge as Blue Ocean Markets

The inaugural “Blue Book on the Development of China’s Medical Device Industry,” released in October 2017, highlighted the future prospects of the home medical device sector as a blue-ocean market.

The Blue Book points out that major home medical device products include: diagnostic and monitoring instruments represented by blood pressure monitors, blood glucose meters, and stethoscopes; therapeutic devices represented by home personal hemodialysis machines; and rehabilitation equipment represented by medical beds and intelligent workstations designed to improve patients' quality of life.

October 2017 marked the first anniversary of the State Council’s official release of the “Several Opinions on Accelerating the Development of the Rehabilitation Assistive Devices Industry” (hereinafter referred to as the “Opinions”). In late October 2016, the State Council officially issued the “Opinions,” which stated that by 2020, the scale of the rehabilitation assistive devices industry was to exceed RMB 700 billion.

On the first anniversary of the issuance of the Opinion, Fan Yubo, Director of the National Research Center for Rehabilitation Technical Aids under the Ministry of Civil Affairs, stated in an interview with media outlets that the rehabilitation assistive device industry is plagued by issues such as a shortage of talent, low-end products, and insufficient subsidies from social security and medical insurance, all of which require urgent resolution.

The research and development of rehabilitation assistive devices in China has long remained at a relatively low level, with most products characterized by low technological content, limited variety, and basic functionality. In stark contrast, sales of well-known international brands have continued to rise in the domestic market, even monopolizing certain segments of the rehabilitation equipment sector, such as the hearing aid and prosthetic limb markets.

Rehabilitation robots are an important branch of medical robots. Their research and development involve many fields, including rehabilitation medicine, biomechanics, mechanics, electronics, materials science, computer science, and robotics. Currently, rehabilitation robots have been widely used in rehabilitation nursing, prosthetics, and rehabilitation treatment.

In VCBeat’s previously published article, “Medical Robots: Annual Financing Reaches RMB 1.5 Billion; Surgical, Service, and Rehabilitation Robots Steadily Develop, with ‘Commercialization’ Becoming the Key Word [2017 Year-End Review],” it was noted that the healthy development of rehabilitation robots is primarily reflected in the influx of capital.

There have been three financing events in the field of rehabilitation robotics this year, namely:

In May 2017, Ruihan Medical announced that it had secured RMB 8 million in angel-round financing, led by Shanghai Zhonghe Venture Capital, with participation from Shanghai Qingrui Investment Center.

In April 2017, Jianjiao Technology secured RMB 30 million in Pre-A series financing from Bojiang Capital, marking the largest funding round in China’s rehabilitation robotics (exoskeleton robotics) sector.

In April 2017, MaiBu Robotics secured angel-round funding, the amount of which was not disclosed; the investors were Lenovo Capital and Taiyou Fund.

Domestic rehabilitation assistive devices are relatively low-end, with high-end products relying primarily on imports. However, imported products are prohibitively expensive; a full set of imported prosthetic limbs costs RMB 400,000, a price that is difficult for ordinary families to afford.

Taking Israel’s ReWalk and Japan’s Cyberdyne as examples, the average price of a single robot ranges from RMB 600,000 to RMB 1 million, with some comparable products reaching as high as RMB 2.5 million; consequently, they are often made available to users only through leasing arrangements.

In contrast to the high prices of foreign exoskeleton robots, Li Muran, CTO of Jianjiao Technology, once stated that Jianjiao’s exoskeleton products would be priced at only tens of thousands of RMB in the future, a revelation that shocked industry insiders.

In August 2017, Han Bicheng, founder of BrainCo and a Ph.D. from the Harvard Center for Brain Science, brought his team’s “Mind-Controlled Prosthetic Arm” to the stage of Hunan TV’s I Am the Future, enabling Ni Min, an armless disabled athlete, to regain arm movement and sparking widespread interest in “brain control” technology.

In September 2017, the brain-controlled lower-limb exoskeleton rehabilitation robot, developed by Professor Xu Guanghua’s team at Xi’an Jiaotong University, made its debut at the finals of the 2017 Silk Road Robot Innovation Competition. By using a helmet to detect the patient’s neural signals, the system transmits these signals to the exoskeleton rehabilitation robot. The robot then executes movements based on the patient’s intent, enabling standing and walking to achieve rehabilitation training and gait correction, while also adapting to various terrain conditions. This marks the first brain-controlled lower-limb exoskeleton rehabilitation robot in China operated by thought control.

Currently, the biggest challenge facing R&D in the field of rehabilitation robotics is how to translate scientific achievements out of the laboratory, enabling robotic technologies to enter the market and achieve industrialization.

“Small but Beautiful” Community Rehabilitation Holds Great Promise

According to international data, the per capita cost of institutional rehabilitation is $100, covering only 20% of individuals requiring rehabilitation. In contrast, community-based rehabilitation services cost just $9 per capita yet cover 80% of this population. Among patients discharged after the acute phase, 15%–30% are transferred to nursing homes, while 35%–60% return home. Thus, the vast majority of patients either return home or are transferred to nursing homes following the acute phase.

Therefore, vigorously developing community-based rehabilitation services can effectively meet patients’ needs for long-term rehabilitative medical care.

Currently, community-based rehabilitation services in China are primarily delivered by community health service centers. Given their strong public-service orientation, these centers often fall short in terms of professional expertise and staffing levels.

As rehabilitation medicine has been elevated to a national strategic priority, private capital has increasingly turned its attention to community-based rehabilitation. The typical pathway involves first establishing specialized rehabilitation institutions, which are generally positioned in the mid-to-high-end segment and serve a relatively narrow population. After gaining a foothold in specialized rehabilitation, these providers then expand into community-based services. According to VCBeat, most enterprises currently offering community rehabilitation services are still in the pilot phase.

Among the companies covered by VCBeat, Wangnian Yuedong relies on communities to establish daytime rehabilitation training centers, complemented by rehabilitation clinics that provide geriatric rehabilitation services. Currently, it has established five such training and rehabilitation centers in Shanghai.

Meanwhile, Jijin Wanmei, another chain rehabilitation provider, launched a pilot operation of its community-based rehabilitation center in September 2017, focusing primarily on musculoskeletal rehabilitation. Unlike rehabilitation centers located in office buildings or commercial districts, community-based facilities require lower initial investment; a storefront of approximately 150 square meters is sufficient for daily operations. These centers are typically staffed with four to five therapists and one specialist, and can meet operational requirements by serving an average of more than 20 patients per day.

According to Feng Feng, co-founder of Ji Jin Perfect, VCBeat learned that three main groups dominate rehabilitation training at community-based rehabilitation institutions: office workers suffering from cervical and lumbar discomfort; postpartum mothers focusing on pelvic floor function and body shape recovery; and individuals with sports injuries, who often engage in long-term, continuous rehabilitation to expedite their return to athletic activities and improve their quality of life.

Following the release of the Basic Standards (Trial) for Rehabilitation Medical Centers, the Basic Standards (Trial) for Nursing Centers, and their respective management specifications by the National Health and Family Planning Commission in November 2017, diverse service models—including home-based rehabilitation—have gained national recognition. Extending rehabilitation services to the “last mile” of community and home care presents new opportunities and challenges for the rehabilitation medical sector.

In rehabilitation models that cover the most basic units, such as community-based and home-based rehabilitation, the importance of nursing care is self-evident. As the development of nursing care is more mature and standardized than that of rehabilitation, with relatively well-established industry-standard protocols, rehabilitation services should also formulate strict procedures and mechanisms to mitigate risks, thereby taking solid steps in advancing their practice systems.

Among the 12 industries with broad prospects mentioned in the 2017 Government Work Report, rehabilitation, nursing, medical care, and healthcare were explicitly highlighted, signaling that the rehabilitation industry is poised to enter a period of comprehensive, high-speed growth.

Driven by technological innovation in the healthcare sector, supply-side reforms in medical services are gaining strong momentum. The model of medical service is accelerating its transformation from “disease-centered care” to “health-centered care.” Meanwhile, the strategic focus of medical device technology development is gradually expanding beyond in-hospital diagnosis and treatment to encompass pre-hospital home health management, inter-hospital resource sharing, and post-hospital continuous rehabilitation services.

Reviewing previous policies, national initiatives such as tiered diagnosis and treatment and medical insurance have significantly strengthened support for rehabilitative medicine. Therefore, driven by the combined forces of policy, capital, and technology in China, the multi-hundred-billion-yuan market for the rehabilitative medicine industry is poised for takeoff. In 2017, the rehabilitation industry stood on the eve of an explosive growth phase.