Third-Party Medical Services in China: Socially Operated Healthcare Expands to 10 Categories, with KingMed Diagnostics and Joinn Laboratories Leading as Industry Exemplars Amid Falling Barriers – 2017 Year-End Review

Third-party medical services have emerged as a buzzword in the healthcare sector this year. Competent authorities, including the State Council and the National Health and Family Planning Commission, have issued multiple supportive policies and established detailed industry standards and regulatory frameworks. As policy dividends are gradually realized, there is growing willingness among social capital to enter the market.

KingMed Diagnostics and Joinn Laboratories, after their IPOs, were warmly embraced by the capital market, fully leveraging their “role model” influence to drive the industry toward large-scale and concentrated development;

As the comprehensive reform of public hospitals advances, services such as clinical laboratory testing, pathology, health examinations, and medical imaging will be unbundled, creating more opportunities for third-party medical service providers and driving leapfrog growth in the industry.

VCBeat (WeChat ID: vcbeat) reviewed the policies and market performance related to the third-party medical services industry in 2017, analyzed the key factors for the development of third-party medical services, and looked ahead to future trends.

Policy: Broadening Categories and Refining Standards

An overview of the policies related to third-party medical service institutions throughout the year reveals two core messages: lowering entry barriers and establishing standards.

Lowering entry barriers entails relaxing restrictions on the types, investment entities, and administrative approval processes for third-party medical service institutions. Meanwhile, standards refer to the issuance of basic standards and management specifications for three categories of medical service institutions: hospice care, rehabilitation medicine, and nursing centers.

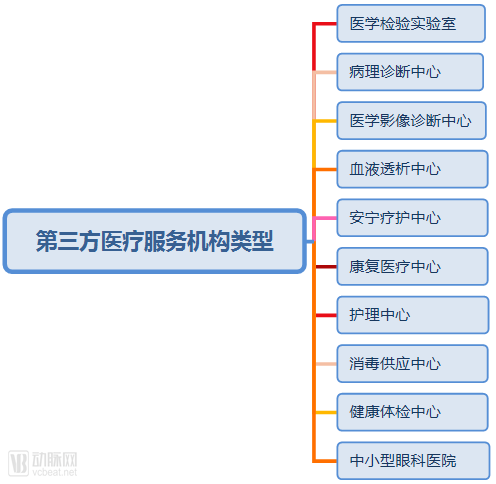

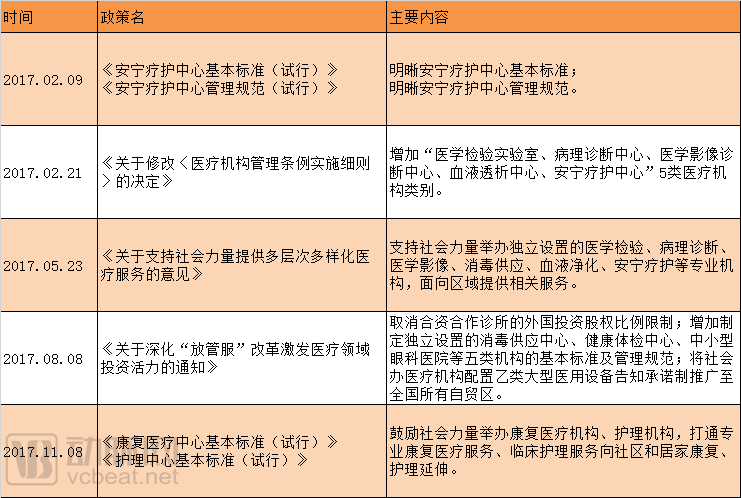

First, let’s discuss the deregulation. On February 21 this year, the National Health and Family Planning Commission issued the “Decision on Amending the Detailed Rules for the Implementation of the Regulations on the Administration of Medical Institutions,” adding five new categories of medical institutions: medical laboratory testing centers, pathology diagnosis centers, medical imaging diagnosis centers, hemodialysis centers, and hospice care centers.

The National Health and Family Planning Commission stated that the Detailed Rules for the Implementation of the Regulations on the Administration of Medical Institutions, which had been in effect since 1994, no longer met regulatory requirements. Against the backdrop of a new industrial environment and development needs, revisions had long been planned. Since 2016, the Commission had successively issued the basic standards and management norms for medical service institutions mentioned above. The current revision aims to better meet residents’ health needs and stimulate the participation of social forces in the development of the health services industry.

By August 8, the National Health and Family Planning Commission (NHFPC) issued the “Notice on Deepening the ‘Streamline Administration, Delegate Power, Improve Regulation, and Upgrade Services’ Reform to Stimulate Investment Vitality in the Healthcare Sector.” The Notice contains ten specific measures, including: implementing a filing-based system for clinics established within elderly care institutions; formulating standards and management regulations for independently established rehabilitation medical centers, nursing centers, sterile supply centers, health examination centers, and small- to medium-sized ophthalmic hospitals; further enhancing the level of opening-up in the healthcare institution sector; merging the approval for establishment and practice registration into a single license for secondary-level and lower-tier medical institutions; and further simplifying the approval process for the establishment of tertiary hospitals.

At this point, the categories of third-party medical service providers have expanded to 10 types.

Looking back at the rationale behind these policies, three key points emerge: First, demand-driven growth—residents’ healthcare needs have been rising steadily, and the existing medical service system can no longer meet these demands. Second, rigid and insufficient supply from public medical institutions—as the primary providers of medical services, public hospitals are overwhelmed by increasing patient demand, necessitating the involvement of private healthcare providers to help “divert” and alleviate this pressure. Third, industrial development needs—policy often lags behind market trends. The “negative list” approach (i.e., everything not explicitly prohibited is permitted) has spurred the rapid proliferation of third-party medical institutions, particularly third-party clinical laboratories and imaging centers, fostering the emergence of multiple listed companies and industry leaders. The recent policies merely clarify standards further, guiding the sector toward healthy and robust competition.

Regulatory encouragement for third-party medical service providers should be viewed through the lens of “supply-side structural reform.” Indeed, the timing of policy incentives for these providers largely coincides with the implementation timeline of “supply-side structural reform.”

In September 2013, the State Council issued the “Several Opinions on Promoting the Development of the Health Service Industry,” proposing vigorous development of third-party services and guiding the establishment of specialized medical laboratory centers and imaging centers, which subsequently experienced rapid growth.

In September 2015, the State Council issued the "Guiding Opinions on the Construction of a Tiered Diagnosis and Treatment System," proposing to integrate and promote the sharing of regional medical resources. Measures include integrating inspection, laboratory testing, and sterile supply centers of hospitals at secondary level and above, opening them to primary healthcare institutions and chronic disease management facilities, while exploring the establishment of independent regional medical laboratory institutions, pathological diagnosis institutions, medical imaging examination institutions, sterile supply institutions, and blood purification institutions to achieve regional resource sharing.

The aforementioned policies are typical examples of "supply-side adjustments." The public healthcare system is, to a certain extent, monopolistic, and such monopoly inevitably leads to structural rigidity and inefficiency. Introducing private capital will naturally inject fresh vitality into the system, thereby enabling the provision of "multi-tiered and diversified" medical services.

From this perspective, policies encouraging the development of third-party medical service providers will continue, as public healthcare system reforms are not yet complete and the challenges of “difficult and expensive access to medical care” have not been fully resolved. The natural solutions lie in the invisible hand of the market and the sharp sword of supply-side structural reform.

2017 Policies Related to Third-Party Medical Services

Industry: The Power of Role Models

Under the "Medical Services" subsector of Shenwan’s Pharmaceuticals and Biotechnology classification, there are 15 listed companies. Two of them went public this year: KingMed Diagnostics and Joinn Laboratories. Amid the substantial influx of private capital into the healthcare services industry, these two companies have served as exemplary role models.

Among them, KingMed Diagnostics’ market capitalization has increased more than fourfold since its IPO, reaching a total of RMB 16.2 billion (as of the close on November 22, same below); Joinn Laboratories’ market capitalization has risen by 367.81% since its IPO, with a total market value of RMB 4.795 billion.

KingMed Diagnostics and Joinn Laboratories have attracted significant capital interest for two primary reasons: first, both companies possess strong core competencies and hold notable market shares in their respective niche sectors; second, investors are optimistic about their growth potential, given the favorable industry landscape and substantial room for expansion.

Let’s first look at KingMed Diagnostics, whose core business comprises third-party medical testing and pathological diagnosis services for various healthcare institutions. Building on this foundation, the company is also expanding into laboratory-related businesses.

The emergence of third-party medical laboratory and pathology diagnostic services stems from the specialized division of labor in healthcare delivery. Relevant institutions have enhanced testing efficiency and quality through scaled operations and specialized division of labor.

In the U.S. market, the third-party medical testing industry emerged during the 1960s–1980s. Against the backdrop of controlling healthcare expenditures, hospitals outsourced a growing number of tests to third-party medical laboratories with lower operating costs. Currently, the U.S. clinical laboratory industry is valued at approximately RMB 75 billion, with independent laboratories accounting for about 35% of the market share. Third-party medical testing institutions in Europe and Japan have also developed robustly, capturing 50% and 67% of their respective market shares.

There is a significant gap between China’s third-party medical testing sector and its counterparts in Europe, the United States, and Japan. The primary reason is that public hospitals dominate the healthcare services market, with most medical testing conducted in-house; thus, the clinical laboratory and pathology departments of public hospitals constitute the main body of the medical testing market.

In terms of scale, the total revenue of domestic third-party medical laboratory testing institutions in 2015 was approximately RMB 10 billion, accounting for about 5% of the medical testing market. According to forecasts by Qianzhan Industry Research Institute, the third-party medical laboratory testing services market is expected to maintain a growth rate of 35%-40% from 2014 to 2020, with its share of the medical testing market reaching around 7%-9%. By 2020, the theoretical market size of third-party medical laboratory testing is projected to exceed RMB 50 billion.

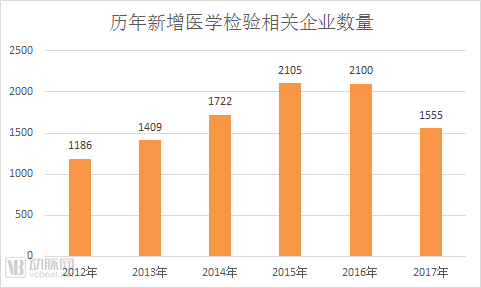

In addition to KingMed Diagnostics’ IPO, corporate registration data also highlights the booming third-party medical testing market. According to business registration records, as of November 22, 2017, a total of 1,555 new companies related to medical testing and nine pathology diagnosis companies were established throughout the year. Dian Diagnostics, KingMed Diagnostics, Zhongke Runda, and Wuhan Landin have all newly established multiple medical testing centers.

Another benchmark in the third-party medical services market is Joinn Laboratories, which primarily engages in preclinical CRO (Contract Research Organization) services for pharmaceutical R&D and manufacturing enterprises. With an annual revenue of approximately RMB 200 million, it ranks among the top tier of China’s CRO industry.

CROs also represent a key subsector of third-party medical services, with a total market size even surpassing that of third-party clinical laboratories. According to statistics from the Southern Institute of the China Food and Drug Administration (CFDA), sales in China’s CRO industry rose from RMB 14 billion in 2011 to RMB 37.9 billion in 2015, achieving a compound annual growth rate (CAGR) of 22.04%, which exceeded the growth rate of the global CRO market during the same period.

Most domestic companies engaged in CRO services are either publicly listed or subsidiaries of listed companies, including WuXi AppTec (which is applying for a main board listing), ChemPartner under Quantum Hi-Tech, Tigermed, Boji Medicine, Shanghai New Summit under Asia-Pacific Pharmaceutical, and Huawei Medicine under Baihuacun.

According to the Southern Institute’s forecast, sales in China’s CRO market will reach RMB 46.2 billion in 2016, with a compound annual growth rate (CAGR) of 20.79% over the next five years, bringing the market size to RMB 97.5 billion by 2020.

Medical imaging diagnostic centers have also been a key focus for private capital, with companies such as GE China and C-MER Healthcare, Yimai Yangguang, Guangyu Group and Shanghai Shizheng, Glory Medical and Shanghai United Imaging Healthcare, Meinian Onehealth and Siemens, and Alibaba Health and Wanli Cloud having engaged in operational practices for many years.

In addition to establishing medical imaging diagnostic centers independently or through partnerships, providing technical services to public hospitals has also emerged as a major trend, encompassing medical imaging systems and AI-powered medical imaging solutions. AI-powered medical imaging applications are flourishing across the board. According to statistics from VCBeat, throughout 2017, companies such as Huiyi Huiying, Yitu Technology, Deepwise Medical, Tisu Technology, TomoDeep, Yasen Technology, and AliHealth launched or implemented AI-powered medical imaging products in hospitals, covering areas including lung cancer, optometry and ophthalmology, and diabetic retinopathy.

Independent hemodialysis centers also witnessed leapfrog development in 2017, driven by the “Basic Standards and Management Specifications for Hemodialysis Centers” released at the end of the previous year. This specification clearly outlined the establishment conditions, diagnostic and therapeutic services, departmental structure, staffing requirements, and equipment standards for hemodialysis centers, thereby further clarifying the regulatory framework for such facilities.

According to data from VCBeat·VCBeat Research Institute, there are currently approximately 4,000 registered hemodialysis centers in China. Around 20 companies and institutions are piloting independent or chain-based hemodialysis services, including Dakang Medical, Aishen Medical, Shengrenkang Group, Aucland, Shanwaishan, and Xinhua Medical. In 2016, China’s hemodialysis market reached RMB 33.5 billion, and it is projected to exceed RMB 35 billion in 2017. Within the hemodialysis industry chain, there are also development opportunities in management software (including hemodialysis management systems, peritoneal dialysis management systems, consumables and equipment management, and patient management) as well as chronic disease management.

In addition to the aforementioned categories, the current industrial landscape for hospice care centers, rehabilitation medical centers, nursing centers, and sterile supply centers remains relatively unclear, with development being rather fragmented. Driven by policy incentives, scaled and standardized operations will become a key focus.

Trend: Third-Party Services Poised for Leapfrog Growth

Currently, China’s healthcare services are dominated by public hospitals, which hold an absolute advantage over private medical institutions in terms of number, patient visits, and revenue. Meanwhile, public hospitals tend to be “large and comprehensive,” possessing near-monopolistic advantages in departments, equipment, and talent, thereby hindering the development of private medical institutions to some extent.

Comprehensive reforms of public hospitals have been implemented for many years, with key tasks including the separation of pharmaceutical sales from medical services, controlling the growth of medical expenses, regulating the consumption of medical supplies, and implementing diagnosis-related group (DRG) payment systems. Public hospitals will achieve these objectives through measures such as outpatient prescription outflow, outsourcing of laboratory and diagnostic tests, and stricter cost-control mechanisms. Given the dominant position of public hospitals in the healthcare system, the outsourcing of pharmaceuticals, laboratory tests, and other services will create significant opportunities for private medical institutions specializing in laboratory diagnostics, pathology, and medical imaging.

The comprehensive reform of public hospitals is expected to be completed in the near future, signaling that private medical institutions may experience leapfrog development as they absorb the patient volume shifted from public hospitals due to these reforms. This constitutes the overarching theme for the growth of private healthcare providers, although opportunities may vary across different market segments.

First, clarify the key development factors of the healthcare industry, including policy, funding, technology, and demand.

From a policy perspective, the emphasis is undoubtedly on encouragement. However, it is crucial to note whether the monopoly of public hospitals has been broken, as this is the key to the development of private medical institutions. Based on currently implemented policies, regulators have merely clarified ten categories of private medical institutions, effectively informing social capital where opportunities lie. At the implementation level, however, obstacles such as approval processes, equipment procurement, and talent acquisition still stand in the way of social investment.

It should be noted that such barriers are gradually being dismantled. For instance, in terms of approval processes, the document on deepening the “decentralization, control, and service” reform proposes merging the two certificates for establishment approval and practice registration into one. This undoubtedly streamlines the approval process, shortens approval time, and facilitates rapid expansion. Regarding equipment, regulators previously imposed strict controls on procurement; public hospitals could purchase equipment with fiscal subsidies, while private hospitals faced numerous restrictions. If fiscal support for public hospitals is reduced or restrictions on private medical institutions are eased, private healthcare providers will naturally benefit significantly. As for talent, public hospitals have traditionally attracted professionals through implicit benefits, including established staffing quotas (bianzhi), comprehensive compensation packages, and research infrastructure. However, if physicians are allowed to move freely between institutions, and private medical organizations simultaneously offer incentives such as equity stakes and partnership models, their appeal to talent will be substantially enhanced.

Funding is not the key constraint on the development of private medical institutions. In addition to industrial capital and listed companies, we are also seeing venture capital (VC) and private equity (PE) firms entering the private healthcare sector. The presence of such capital can be observed behind many physician groups, hospital management companies, and “internet-famous physicians.” Capital is flowing into the healthcare sector in a manner reminiscent of its entry into the internet industry—a phenomenon unprecedented in the past.

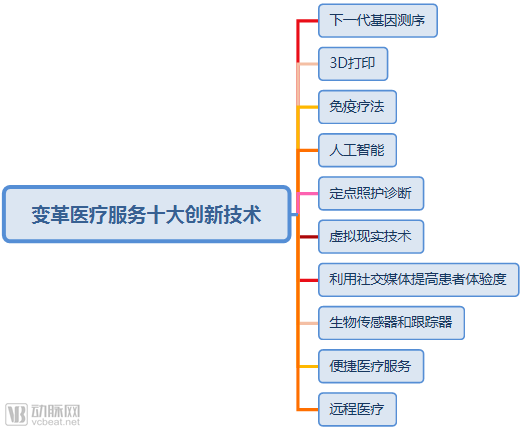

From a technological perspective, new technologies will become a key driver for the development of private medical institutions. According to Deloitte’s “2017 Healthcare Industry Outlook” report, next-generation sequencing (NGS), 3D printing, immunotherapy, artificial intelligence, biosensors and trackers, telemedicine, and other technologies will improve healthcare outcomes and reduce medical costs. Such innovative technologies will also nurture third-party healthcare service providers that possess more flexible organizational mechanisms.

On the demand side, key considerations center on the target populations within niche segments of third-party medical services. For instance, as population aging intensifies, the number of individuals requiring palliative care naturally increases (representing an incremental market). However, it is important to note the gap between those with such needs and those who actually utilize these services. Whether palliative care will experience explosive growth depends on actual willingness to accept such care, as well as market education efforts undertaken by relevant institutions.

Another key factor is the ability to pay corresponding to demand. Given the current strain on public medical insurance funds, developing commercial health insurance has become a critical direction. Collaboration between third-party medical service providers and commercial health insurers will also be an important approach for implementation.

In addition to the ten clearly defined categories of third-party medical service providers, the advancement of comprehensive reforms in public hospitals will lead to the unbundling of more operational functions. This creates development opportunities in areas such as facility management, pharmaceutical services, equipment maintenance, and medical waste disposal, thereby enabling social capital to engage more actively and across a broader range of entry points.