In Vitro Diagnostics in 2017: 10 Major M&A Deals, 8 IPOs, with Immunoassay and Molecular Diagnostics Leading Growth – 4 Investment-Worthy Segments Highlighted

As one of the most promising sectors within the medical device industry, in vitro diagnostics (IVD) has long been recognized as the cornerstone of precision medicine.

In 2017, new technologies such as next-generation sequencing (NGS) and microfluidics, emerging models including “Internet Plus,” big data, and health management, as well as new objectives like precision medicine, all opened up new horizons for the in vitro diagnostics (IVD) industry, further expanding its growth potential.

Current Development Status of Major IVD Subsectors in 2017

The in vitro diagnostics (IVD) industry is highly segmented, with significant variations across subsectors in terms of life cycle, market size, growth rate, technological barriers, and marketing channels. While some segments have achieved domestic production, others remain entirely dependent on imported products. So, what is the current development status of the major subsectors within China’s IVD industry?

1. Biochemical diagnostic technologies have matured, and the localization process has been largely completed.

Biochemical diagnostics is one of the earliest-developed subsectors of in vitro diagnostics (IVD) in China; therefore, whether in terms of accumulated technological expertise or the range of product coverage,, major domestic manufacturers of biochemical diagnostic products (including instruments and reagents) have gradually mastered core technologies and basically completed the transition from pure imports to independent research and development.Diagnostic reagents have basically achieved import substitution, with domestic products accounting for 70% of the market share. However, high-end instruments are still dominated by foreign companies, with domestic products holding less than 10% of the market share.

Benefiting from technological advancements and the development of the primary healthcare market, China’s clinical chemistry diagnostics industry has maintained a steady growth trajectory. In 2016, the market size was approximately RMB 6.5 billion, with a compound annual growth rate (CAGR) of 6%–8%. The market is projected to reach RMB 8.56 billion by 2020.

However,In recent years, the biochemical diagnostics industry has shown signs of fatigue, with a significant slowdown in growth rate., hospital service volume has generally remained in sync with outpatient visits. The implementation of tiered diagnosis and treatment has led to a decline in outpatient visits at large hospitals, with a significant decrease in biochemistry diagnostic service volume as patients are diverted to primary care institutions.

2. Rising Market Share of Immunoassays: Chemiluminescence Emerges as a New Growth Driver

Immunodiagnostics has been one of the largest, most rapidly expanding segments within China’s in vitro diagnostics (IVD) industry in recent years, characterized by the greatest number of new product introductions and the highest growth rate, with an annual industry growth rate exceeding 15%. In 2016, the market size for immunodiagnostic products in China was approximately RMB 10.9 billion. According to forecasts by Kalorama & Huidian Research, the market size is projected to surpass RMB 19 billion by 2020.

With the continuous transformation of immunological technologies,Chemiluminescence immunoassay (CLIA) is gradually replacing enzyme-linked immunosorbent assay (ELISA) and has become a new growth driver in immunodiagnostics, owing to its advantages such as high sensitivity, strong specificity, and extended reagent shelf life.However, as chemiluminescent immunoassay diagnostic products operate as closed systems with integrated instruments and reagents, they present high technical barriers. With few domestically developed chemiluminescent products available in China and a predominance of imported alternatives, testing costs remain relatively high.

3. Molecular diagnostics is in its nascent stage, with genetic testing driving accelerated development of the industry in China

As a cutting-edge technology in the life sciences, molecular diagnostics has been widely applied in areas such as prenatal screening, infectious diseases, and oncology. The most well-known genetic sequencing at this stage falls within the scope of molecular diagnostics and is regarded as one of the 12 disruptive technologies that will shape the future economy.

Among numerous applications,Non-Invasive Prenatal Testing (NIPT) is currently the most mature application of gene sequencing and holds the largest market share.The domestic NIPT market is conservatively estimated at RMB 3.5 billion, with an oligopolistic structure dominated by BGI Genomics and Berry Genomics, which together account for more than 90% of the market share in China. Both companies went public this year, listing on the capital market.

China’s molecular diagnostics sector is in its nascent stage, characterized by low market concentration and a relatively small scale. However, it is experiencing remarkable growth, leading the in vitro diagnostics (IVD) industry with a growth rate exceeding 25%. In 2010, the domestic molecular diagnostics market was valued at only RMB 1 billion.Driven by breakthroughs and declining costs in technologies such as gene sequencing, gene chips, and polymerase chain reaction (PCR), along with policy support and capital investment, the overall market has expanded rapidly. The market size exceeded RMB 6 billion in 2016 and is projected to reach RMB 10 billion by 2019.

However, due to the high barriers to instrument and reagent development, high-end products such as gene chips and next-generation sequencing (NGS) remain monopolized by foreign companies. With regulatory policies relaxing the clinical application of NGS and growing market acceptance and recognition of new technologies, next-generation sequencing is poised for rapid growth.

4. POCT: The New Blue Ocean of In Vitro Diagnostics

POCT (Point-of-Care Testing) is now widely used in ICUs, operating rooms, emergency departments, clinics, and patients' homes due to its advantages such as short testing time, ease of operation, and timely and accurate results.

POCT technology pathways are gradually being upgraded, with quantification, miniaturization, and portability emerging as key development trends, leading to extensive clinical applications.In terms of test items, POCT is mainly concentrated in 13 major categories, including blood glucose testing, blood gas and electrolyte analysis, infectious disease testing, rapid diagnosis of cardiac markers, and drug abuse screening. Among these, the blood glucose segment has the largest market size, while the cardiovascular segment is experiencing the fastest growth rate.

In recent years, point-of-care testing (POCT) has become one of the fastest-growing segments within the in vitro diagnostics (IVD) industry. China’s POCT sector has maintained an annual growth rate of 20%–30%, surpassing the approximately 8% growth rate observed in the international market. The domestic POCT market size approached RMB 3.5 billion in 2013 and exceeded RMB 6 billion in 2016, reflecting rapid development. It is projected to approach RMB 10 billion by 2018.

Four Key Factors Driving Trends in In Vitro Diagnostics

Driver 1: Policy Changes Reshape Industry Competition Landscape

Over the past three years, the intensive rollout of industry policies has become a primary driver stimulating sector-wide transformation, with varying degrees of policy impact felt across research and development, clinical trials, regulatory registration, and distribution. Under the influence of these policies, the competitive landscape of the in vitro diagnostics (IVD) industry is expected to be optimized. The Matthew effect will be amplified by external factors, enabling leading enterprises to strengthen their dominant positions.

Tiered Diagnosis and Treatment Policy Drives Channel Penetration into Primary Care

Since the tiered diagnosis and treatment system was explicitly proposed at the Two Sessions in 2015, pilot programs were launched in 100 public hospitals that same year. During the Two Sessions in 2016 and 2017, the state successively set targets for pilot prefecture-level cities to cover 70% and 85% of such cities, respectively. Driven by these policy initiatives, the tiered diagnosis and treatment system has begun to demonstrate significant effects.

The goal of the tiered diagnosis and treatment policy is to gradually divert patient flow from tertiary hospitals to primary care institutions and private hospitals, thereby alleviating the immense pressure on large public hospitals. It is projected that 20–30% of patients will receive diagnosis and treatment at community outpatient clinics and private hospitals in the future. This shift is expected to drive procurement demand for in vitro diagnostic (IVD) products by clinical laboratories in secondary and tertiary hospitals, despite the anticipated significant growth in the overall patient population.

In other words, the implementation of the tiered diagnosis and treatment policy has, on one hand, increased the patient volume at primary care hospitals and, on the other, gradually heightened the demand for basic laboratory testing equipment.

Higher Registration Thresholds, Intensifying Matthew Effect in the Industry

2014 marked a regulatory watershed for the in vitro diagnostics (IVD) industry. Prior to 2014, the sector experienced unregulated growth, characterized by high product gross margins, low barriers to entry, and a substantial increase in the number of manufacturers. Beginning in 2014, regulatory authorities, including the China Food and Drug Administration (CFDA), intensively rolled out a series of policies to strengthen oversight and standardization across market access, manufacturing, and distribution channels.

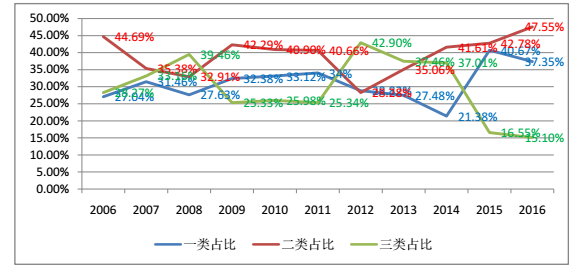

Trend Chart of the Proportion of Class I, II, and III Products in the Total Number of Marketed Products (Data Source: 2016 Annual Statistical Report on Food and Drug Supervision, Hongta Securities)

The increasing difficulty of obtaining registration certificates has led to most industry growth being driven by Class I and II medical devices with relatively low technical barriers, while the number of Class III device registrations has declined sharply. In the future, against the backdrop of encouraged innovation and stricter regulation, manufacturers of low-technology products will face significant challenges in securing regulatory approvals. Conversely, the market for Class III devices is expected to grow, and the Matthew effect within the in vitro diagnostics (IVD) industry will gradually intensify.

Medical Insurance Cost Control + Import Substitution: Accelerating the Process of Localization

In addition to the heightened registration barriers affecting the competitive landscape of the entire in vitro diagnostics (IVD) sector, the “import substitution” policies introduced by the state over the years to support domestic brands are also catalyzing industry transformation.

Especially against the broader industry backdrop of reduced testing prices and tightened health insurance cost controls, in vitro diagnostics (IVD) are billed on a per-test basis, turning diagnostic instruments and consumables into cost centers. This has enabled domestic brands with greater price advantages to gradually enter the procurement lists of tertiary hospitals, making import substitution merely a matter of time.

Driver 2: Capital Invigorates the Industry; Mergers and Acquisitions Drive Structural Optimization and Marketing Channel Integration

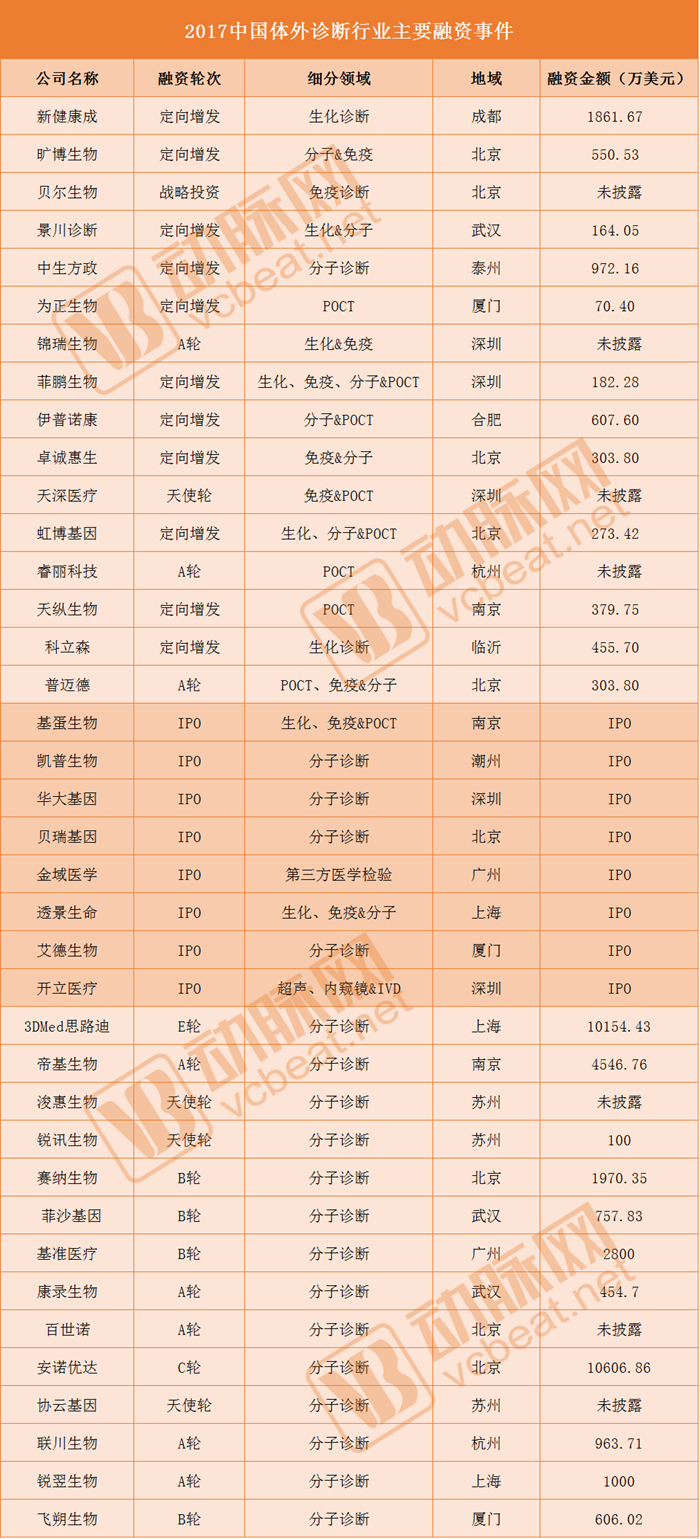

In addition to imaging equipment and medical consumables, in vitro diagnostics (IVD) has consistently remained a hot spot for investment within the medical device industry. According to incomplete statistics from VCBeat, there were 38 financing and investment events in China’s IVD industry in 2017, with a cumulative amount exceeding USD 400 million; among these, the molecular diagnostics sector (particularly gene sequencing) attracted the most funding. This year, the number of IVD companies going public has also increased rapidly, with seven companies listing (HybriMed, Tumor Genomics, BGI, Getein, KingMed, AmoyDx, and Sonoscape) and one completing a back-door listing (Berry Genomics). To date, the roster of listed IVD companies in China has expanded to 21.

Looking at the development history of the IVD industry abroad, as the domestic IVD market experiences rapid growth and intensifying competition, the industry’s growth rate is bound to decline. Once each niche sector reaches its peak, relying solely on organic growth will yield very limited speed; therefore, injecting competitive advantages through industrial M&A will inevitably become the primary approach.

Corporate mergers and acquisitions (M&A) are primarily categorized into technology-and-product-driven M&A and market-share-driven M&A. The former aims to shorten product development cycles, thereby reducing R&D risks, and to rapidly launch new products to capture market share by leveraging the target’s innovative technological advantages combined with the acquirer’s mature industrialization capabilities. The latter seeks to increase market share and optimize the competitive landscape, with acquisition targets consisting mainly of competitors.

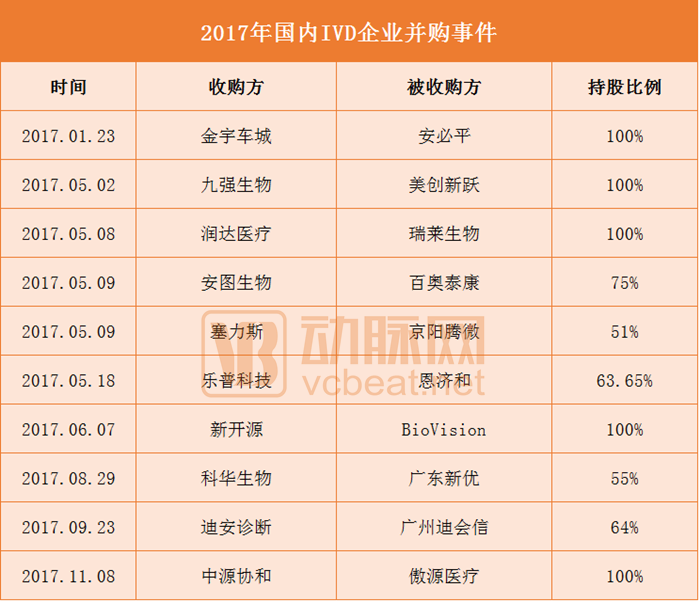

Compared with foreign markets, China’s domestic IVD industry remains in its growth phase, characterized by high growth rates, low entry barriers, and intensifying competition. With the acceleration of A-share initial public offerings (IPOs), listed in vitro diagnostic (IVD) companies are no longer scarce. Those with capital advantages are actively seeking to acquire high-quality products to strategically expand and diversify their product portfolios. Since 2016, M&A activities in China’s IVD sector have occurred frequently, with 22 deals completed in the previous year alone. Although the pace of M&A slowed in 2017, there were still at least 10 transactions, involving well-known enterprises such as Runda Medical and Dian Diagnostics.

Driver 3: Technological Upgrading Is the Intrinsic Driving Force Behind the Rise of Domestic IVD Enterprises

For years, China’s vast primary healthcare market has provided a solid foundation for the growth and expansion of domestic IVD companies, enabling them to accumulate various technological capabilities. Meanwhile, with the public listings of leading IVD enterprises, capital inflows into the industry have been rapidly replenished, significantly boosting R&D investment. The accumulation of technology and capital has gradually made it possible for technological upgrades to transition from quantitative changes to qualitative leaps.

For example, in the field of immunodiagnostics, domestically produced chemiluminescence assays have achieved breakthroughs in niche segments such as infectious diseases, opening the door to import substitution. With the market launch of new domestic mass spectrometry-based detection technologies, China is also poised to break the import monopoly in the microbiology sector. Recently, Autobio Diagnostics rapidly launched two flagship products: the Autolas A-1, a fully automated laboratory assembly line system, and the Auto fms1000, a microbial mass spectrometry identification system. This achievement exemplifies the perfect synergy between the company’s technological accumulation and support from the capital market.

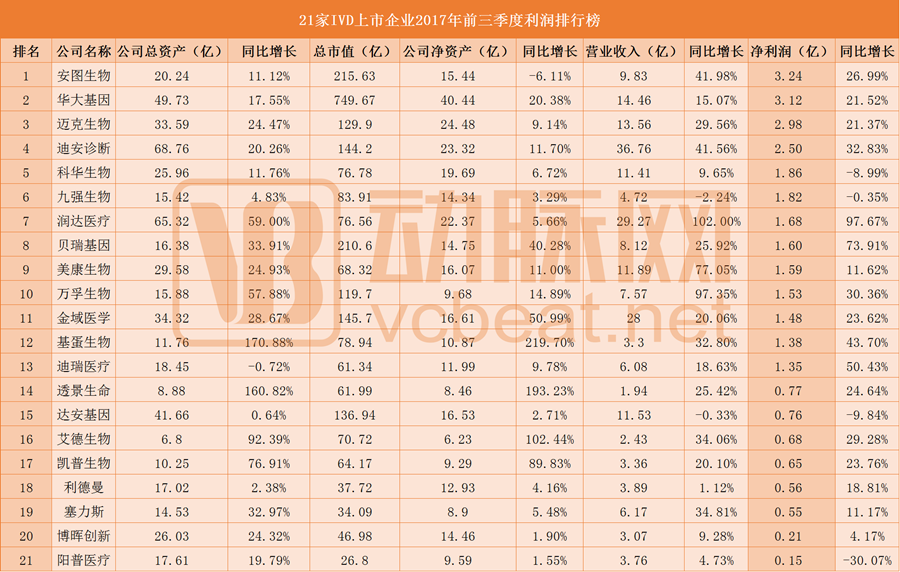

Technological upgrades are driving rapid industry development, and the revenues of domestic IVD companies are also substantial.

Source: China IVD Network

As of October 31, 21 A-share listed in vitro diagnostics (IVD) medical device companies have successively released their financial reports for the first three quarters. Data from these reports indicate that the average year-on-year revenue growth rate for these 21 listed IVD enterprises reached 30.41%. The performance shows highly encouraging growth compared to the same period last year, with some companies even achieving substantial increases. Notably, Sonoscape Medical, although engaged in IVD business, derives its primary revenue from ultrasound diagnostic systems and was therefore excluded from this statistical analysis.

Driver 4: Aging Population, Urbanization, and Heightened Health Awareness Drive Growing Market Demand

The size of the clinical laboratory market is directly correlated with hospital patient volumes; aging drives increased healthcare demand, thereby leading to a rise in testing volume. According to the World Health Organization’s inaugural Global Report on Ageing and Health, released in 2015, China’s elderly population is projected to grow from 194 million to 483 million between 2012 and 2050, with the aging rate increasing from 14.3% to 34.1%.

On the other hand, healthcare institutions are concentrated in urban areas, where population agglomeration facilitates easier access to medical services. The rising level of urbanization has also driven an increase in healthcare demand and a growth in diagnostic testing needs. The proportion of China’s urban population to its total population has risen from 26.41% in 1990 to 57.35%, and is expected to exceed 80% in the future.

Third, as living standards and incomes rise, individuals are paying increasing attention to their own health. According to data from statistical yearbooks over the years, per capita household expenditure on healthcare and medical services among urban residents in China increased from RMB 528 in 2004 to RMB 1,305.6 in 2014, while that among rural residents rose from RMB 131 to RMB 753.9 during the same period. The continuous growth in per capita income will drive a corresponding increase in per capita healthcare spending, thereby fueling rapid growth in demand for the in vitro diagnostics (IVD) market.

Future Development Trends of China's IVD Industry

1. Extending to the grassroots level: Metrological traceability drives significant industry growth

In the context of tiered diagnosis and treatment, the volume of laboratory tests is shifting toward primary care hospitals, while the test portfolio in tertiary hospitals is transitioning from routine testing to specialized testing. Meanwhile, as referral needs across medical institutions at all levels increase, mutual recognition of regional laboratory results is becoming a developmental trend, raising the standards for laboratory capabilities at the primary care level. To achieve mutual recognition of test results among hospitals, it is essential to ensure the temporal and spatial comparability of these results, and metrological traceability serves as an effective pathway to establishing standardized laboratory medicine.

Traceability of measurement values in the field of in vitro diagnostics is defined as the process of comparing the test results of in vitro diagnostic systems with a continuous chain of comparisons. Through continuous calibration, this process links the test results of different combined diagnostic systems to international standards (reference materials and reference methods), thereby enhancing metrological accuracy and achieving mutual recognition of test results across different medical institutions.

2. In the distribution sector, the bundled business model is expected to be rolled out nationwide

Policies such as tiered diagnosis and treatment, zero markup on drugs, and Diagnosis-Related Group (DRG)-based medical insurance reimbursement have prompted hospitals to prioritize cost control. Consequently, a series of new models have emerged in the distribution sector, with the “bundling model” being the most representative. The bundling model refers to optimizing product portfolios (primarily by offering high cost-performance combinations), enhancing pre-sales, during-sales, and after-sales services, and improving the operational efficiency of clinical laboratories, all without compromising testing quality. Driven by hospitals’ profitability needs and the imperative for cost control in clinical laboratories, the “bundled business model” is poised for widespread adoption across China.

3. Tiered Diagnosis and Treatment: A New Dawn for Third-Party Independent Laboratories

Tiered diagnosis and treatment has increased the volume of laboratory tests at hospitals below the tertiary level, while hardware deficiencies have driven a divergence in the penetration rates of third-party independent clinical laboratories (ICLs) across different hospitals. Currently, the market size of third-party independent clinical laboratories in China stands at RMB 7.5 billion (compared to approximately USD 30 billion in ICL revenue in the United States in 2015). Although the compound annual growth rate (CAGR) over the past five years has exceeded 50%, ICLs account for only 4% of the total medical diagnostics market share.

In China’s independent clinical laboratory (ICL) market, Dian Diagnostics, KingMed Diagnostics, Adicon Clinical Laboratories, and Gaoxin Da’an collectively hold over 70% of the market share. Among these, Dian Diagnostics and KingMed Diagnostics hold a distinct advantage in terms of the number of laboratories, each having operated more than 30 testing facilities by 2016, primarily concentrated in first-tier cities or provincial capitals. However, with the deepening implementation of tiered diagnosis and treatment, expanding services to grassroots levels will become a key strategic direction for the future development of ICLs.

4. Four Major Sub-sectors Continue to Shine

Expansion of biochemical diagnostics into overseas markets and the adoption of closed-system products driven by a “instrument-led reagent” model have emerged as two major trends. Over the next three years, immunodiagnostics will benefit from the replacement of traditional methodologies and channel penetration into lower-tier markets, with chemiluminescence immunoassay (CLIA) becoming the absolute mainstream technology in the immunodiagnostics sector. In the molecular diagnostics industry, gene sequencing services are becoming a highly contested strategic battleground, while tumor gene sequencing applications are acting as a catalyst for the “Matthew effect” within the industry. In the point-of-care testing (POCT) sector, technological advancements are driving product iteration and upgrades, ushering niche segments into a period of rapid growth.

5. Polarized Development of In Vitro Diagnostic Technologies

Currently, hospital demand for in vitro diagnostic (IVD) products is showing a polarized trend. High-end hospitals require testing products with high throughput, high efficiency, and high sensitivity, while primary care hospitals need products with moderate speed, affordable pricing, and stable performance. In response to this demand, IVD products in the Chinese market will also develop along two polarized directions: integrated immunochemistry automation lines and point-of-care testing (POCT).

6. The technological gap between domestic and international markets is narrowing, with domestic brands gradually replacing imported ones

In recent years, China’s in vitro diagnostics (IVD) industry has experienced rapid development, with a swift expansion in the variety of testing products. The technological gap between domestic and international players is narrowing. Overall, domestically produced products have captured 44% of the market share; however, development remains uneven across specific product categories. In the field of biochemical diagnostics, Chinese companies have nearly reached parity with their foreign counterparts, and most mid- to low-end products have already replaced imports.

What Are the Remaining Growth Drivers in the IVD Industry?

Having analyzed the current development status, driving forces, and trends of China’s in vitro diagnostics (IVD) industry, what are the future growth points for the IVD sector, and which areas warrant investment?

Currently, “import substitution” in the mid-to-low-end market has been completed, turning it into a red ocean and making it less than ideal as an entry point for startups. Entrepreneurs may consider exploring investment opportunities in the following areas.

1. Diagnostic Instruments.The barriers to instrument R&D are high, and instrument sales drive reagent sales, particularly for instruments with closed reagent systems in the fields of immunology and molecular diagnostics.

2. Niche segments with high barriers to entry.In the fields of chemiluminescence and molecular diagnostics, products feature high technological content, making it difficult for competitors to replicate companies established in these sectors. Moreover, import substitution in these two areas is just beginning, with growth rates exceeding the industry average. Entrepreneurs with strong R&D and manufacturing capabilities, coupled with robust market distribution channels, can still capture a significant share of this “import substitution” opportunity.

3. Comprehensive category coverage.The primary point of use for IVD products in hospitals is the clinical laboratory. Companies that can expand their product portfolios through mergers and acquisitions or organic growth can leverage their existing distribution channels to promote new products, thereby creating new profit growth drivers.

4. High-end markets and certain emerging technology sectors.High-throughput gene sequencing for clinical applications and innovative point-of-care testing (POCT)—particularly projects that undergo initial validation overseas before entering mass production in China—are becoming popular entry points for IVD entrepreneurs.