Youjia Health Files for IPO: Leveraging Early Lenovo Star Backing to Capture the Booming Third-Party Health Insurance Services Market

Health Insurance: Benefiting from policy incentives, a more complete insurance industry chain, and heightened public awareness of health coverage, health insurance has become the fastest-growing segment of the insurance industry. According to data from the China Insurance Regulatory Commission (CIRC), the compound annual growth rate (CAGR) of health insurance premiums exceeded 30% starting in 2012. The market size reached RMB 404.2 billion in 2016 and is projected to surpass RMB 420 billion in 2017.

The development of health insurance relies heavily on the robust support of Third-Party Administrators (TPAs). These companies provide health insurers with a wide range of services, including product design, sales support, policyholder management, and data mining. By enhancing the overall health insurance framework, TPAs have laid the foundation for establishing a multi-tiered and comprehensive health insurance system.

Amid the rapid development of health insurance, third-party insurance service companies have emerged in large numbers. Beijing UPlus Health Insurance Technology Co., Ltd. is one of the many newly established third-party insurance service providers.

Recently, VCBeat (WeChat ID: vcbeat) interviewed Wang Yanping, founder of Youjia Health, to hear her detailed views on the health insurance and third-party service markets, as well as Youjia Health’s product and market plans.

Building a Professional Third-Party Service Platform for Health Insurance

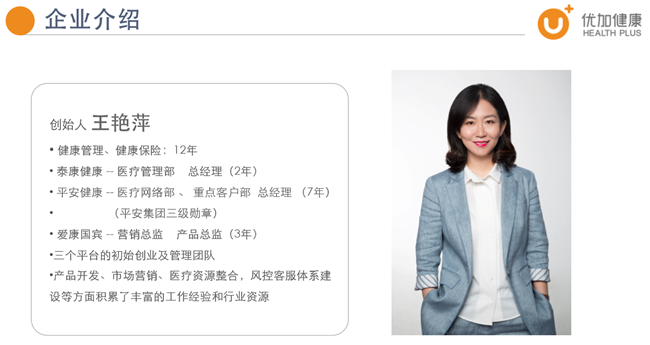

With over a decade of experience in the health insurance industry, Wang Yanping was an early founding team member and part of the preparatory group at iKang Guobin, Ping An Health, and Taikang Health. She has personally witnessed the ten-year early development of health insurance and health management in China. She has previously served as General Manager of the Medical Network Department and Key Accounts Department at Ping An Health, and as General Manager of the Medical Management Department at Taikang Health. Other members of the founding team come from the insurance, healthcare, and internet sectors, bringing extensive management and operational expertise.

In June this year, the founding team was fully assembled. Shortly after its formation, the team secured angel-round investment from Legend Star, a leading domestic healthcare investment firm.

Wang Yanping told VCBeat that UJia Health positions itself as a third-party service platform connecting healthcare providers, insurers, and policyholders, aiming to enhance the service and risk control capabilities of commercial insurance companies, improve the service experience for policyholders, and increase the operational efficiency of medical institutions.

Centered on third-party services, Youjia Health currently operates two core brands. The first is the product brand “Critical Illness Worry-Free,” which recommends appropriate medical institutions to customers through an intelligent triage system prior to medical visits; provides deposit advances, medical record management, and specialized medical treatment recommendations during hospitalization; and offers direct claim settlement services after discharge. Additionally, a dedicated “Medical Consultant” position has been established to provide policyholders with combined online and offline consultation and assistance for medical care. The second brand is the “Medical Insurance Worry-Free” Cross-Industry Salon, an initiative that primarily provides a communication platform for insurance companies and medical institutions to discuss current hot topics in medical insurance, thereby fostering mutual understanding and deepening cooperation between the insurance and healthcare sectors.

According to Wang Yanping, UJia Health has now signed contracts with several well-known Grade 3A hospitals in first-tier cities and established partnerships with multiple insurance institutions, with its business operations having entered a substantive phase.

The Booming Development of Health Insurance Brings Market Opportunities

As a senior expert in the health insurance industry, Wang Yanping’s decision to launch her venture by focusing on third-party services is closely tied to her optimism regarding the growth potential of both health insurance and third-party insurance services.

She stated that after more than a decade of development, China's health insurance industry has reached an explosive growth phase, with an urgent demand for third-party services.

From the perspective of key milestones in the development of health insurance, the timeline can be broadly divided into three phases. The first phase spanned from 2005 to 2014, a nascent period for the industry, during which PICC Health, Ping An Health, Harmony Health, and Kunlun Health were established successively; for a long time, these remained the only four specialized health insurance companies in the market. After 2014, the number of health insurance companies began to expand, with Taiping Allianz, Fosun United, and Ruihua Health receiving regulatory approval in turn, prompting broader industry participation in the health insurance sector. The year 2017 can be regarded as the “new inaugural year” for health insurance development, marked by a significant upturn in performance: all four major players reported notable year-on-year growth, with three of them doubling their figures compared to the previous year.

“As health insurance gradually enters the public eye, the performance of specialized health insurance companies is improving, with previous losses beginning to narrow. Meanwhile, the number of health insurance companies is expanding; according to incomplete statistics, more than 50 health insurance companies are currently awaiting license approvals, including internet giants such as Tencent, Baidu, Alibaba, and JD.com, which are also accelerating their entry into the insurance sector.”

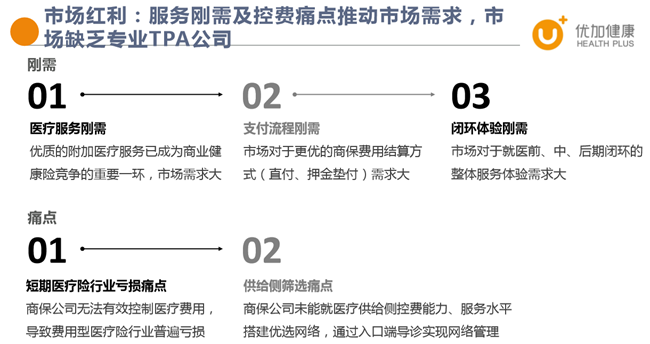

While the health insurance industry is expanding rapidly, it still has significant room for improvement. Currently, the market is dominated by life insurance companies, with long-term critical illness insurance accounting for the largest share. Medical insurance is experiencing rapid growth, whereas long-term care insurance and disability insurance represent only a small fraction of the market. Moreover, total health insurance premium income constitutes merely a minor proportion of life insurers’ overall revenue. Under these circumstances, life insurance companies tend to allocate internal resources unevenly and lack specialized medical and healthcare talent, hindering their ability to achieve professionalized operations.

Furthermore, due to the high risk of adverse selection in individual health insurance and the dominance of social security as the primary payer, commercial insurance companies have limited bargaining power over healthcare providers. Consequently, the two parties are not yet closely collaborating, which prevents insurers from effectively and reasonably controlling medical practices and costs.

It is precisely under these circumstances that third-party insurance service companies find opportunities to exert their influence. Acting as independent intermediaries, they facilitate collaboration between healthcare institutions and insurers, establish preferred provider networks, and leverage technological solutions and data mining to optimize health insurance processes, thereby controlling medical cost expenditures.

Wang Yanping also told VCBeat that domestic health insurance companies lack professional management capabilities and are often hesitant to expand their business scope. Introducing third-party services will effectively enhance their risk control capabilities and service levels, thereby improving the effective supply of health insurance products.

Furthermore, it is a major trend for health insurance companies to outsource management services.

“To provide effective management and services, companies must establish corresponding platforms and invest substantial resources, while smaller-scale firms or insurers whose core business is not health insurance often face the challenge of excessively high operating costs.”

Third-party service providers can offer specialized medical and health services to small and medium-sized insurance companies, helping them reduce investments in manpower, equipment, medical network expansion, and information systems, thereby improving operational efficiency and service quality.

High-Growth Momentum to Continue

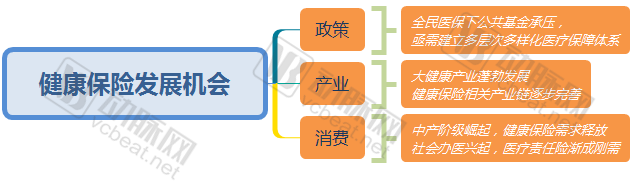

Wang Yanping believes that the expansion of the health insurance market size is mainly driven by two factors: first, policy incentives, including measures to encourage the development of commercial health insurance, pilot programs for tax-advantaged individual health insurance, coordination between commercial health insurance and basic medical insurance, and adherence to the principle that “insurance should prioritize protection”; second, enhanced market innovation capabilities, exemplified by the surge in mid-tier medical insurance products such as “Million-Yuan Medical Insurance,” which has stimulated demand for commercial health insurance among middle-income groups. Additionally, new marketing approaches, such as online promotion and digital underwriting, have improved the accessibility of health insurance.

Driven by policy guidance and proactive initiatives at the industry level, the health insurance market is poised for explosive growth. According to securities research reports, the scale of China’s commercial health insurance will increase to RMB 500–700 billion within five years, becoming one of the three major business segments alongside property and casualty insurance and life insurance.

Wang Yanping stated that, in terms of functional positioning, commercial health insurance should serve as a supplement to universal health coverage, providing policyholders with additional protection beyond basic medical insurance.

“Public health insurance is characterized by ‘broad coverage but a low benefit level.’ As residents’ incomes rise and awareness of health protection strengthens, basic medical insurance can no longer meet the insurance and healthcare service needs of middle- and high-income groups. Commercial health insurance effectively aligns with this shift in demand.”

The Rise of the Middle Class Has Activated the Incremental Market for Commercial Health Insurance. According to McKinsey’s forecast, by 2022, 76% of Chinese urban households will reach middle-class income levels. Among the consumption preferences of the middle class, spending related to “health status” has received significant attention.

From a developmental perspective, policies also encourage collaboration between health insurers, medical institutions, and health management companies, which undoubtedly brings policy “dividends” to third-party management and service providers like UJIA Health.

As mentioned in the “Administrative Measures for Health Insurance (Draft for Comments)” released on November 15, health insurance products should be integrated with health services to provide health risk assessment and intervention, as well as services such as disease prevention, health examinations, health consultations, health maintenance, chronic disease management, and wellness care, thereby reducing health risks and minimizing disease-related losses.

Meanwhile, insurance companies offering medical insurance should strengthen collaboration with healthcare service providers and health management service organizations, actively engage in overseeing healthcare delivery, monitor the authenticity and legality of medical practices, and provide recommendations on the reasonableness and necessity of medical expenditure. This helps alleviate information asymmetry between patients and healthcare providers, as well as reduce doctor-patient disputes.

The revised “Measures for the Administration of Health Insurance” has sent a positive signal from regulators to promote the development of health insurance. The integration of health insurance with health management and medical services aligns with the needs of commercial health insurance development and enriches its connotation.

“High-quality medical services have become a critical component in the competition among commercial health insurers, driven by substantial market demand; third-party service providers also have significant opportunities to optimize policyholders’ consultation and payment processes.” In Wang Yanping’s view, the development of third-party insurance service companies will be propelled by these rigid demands.

Favorable market trends, combined with a precise entry point, have given Wang Yanping full confidence in the development of UPlus Health. She stated that UPlus Health will continue to expand access to high-quality medical resources, identify the needs of insurance institutions and healthcare providers, and develop specialized insurance products and health management standards, thereby truly benefiting patients, healthcare providers, and insurers alike, and growing together with the health insurance industry.