Gene Testing in 2017: Sustained Momentum, Emphasis on Indigenous Innovation, and Market Surge Driven by IPOs of Industry Leaders

In the 2016 VCBeat “Future Healthcare 100” rankings, the genetic testing sector made a strong breakthrough, securing two of the top five spots, with BGI Genomics claiming the number one position.

In 2017, two industry leaders went public in succession, positioning the tumor detection sector for rapid growth. Under policy guidance, microbiomics gradually matured, leading to a diversified industry landscape. Meanwhile, with the launch of domestically developed sequencers independently innovated by MGI Tech and Hanhai Gene, the campaign for domestic substitution in the upstream sequencing segment was officially underway.

Next, VCBeat will review and analyze the industry’s financing and investment activities, policies, and key events in 2017, looking back at the eve of these developments to gain insights into the future.

219%! Explosive Growth in Financing Volume

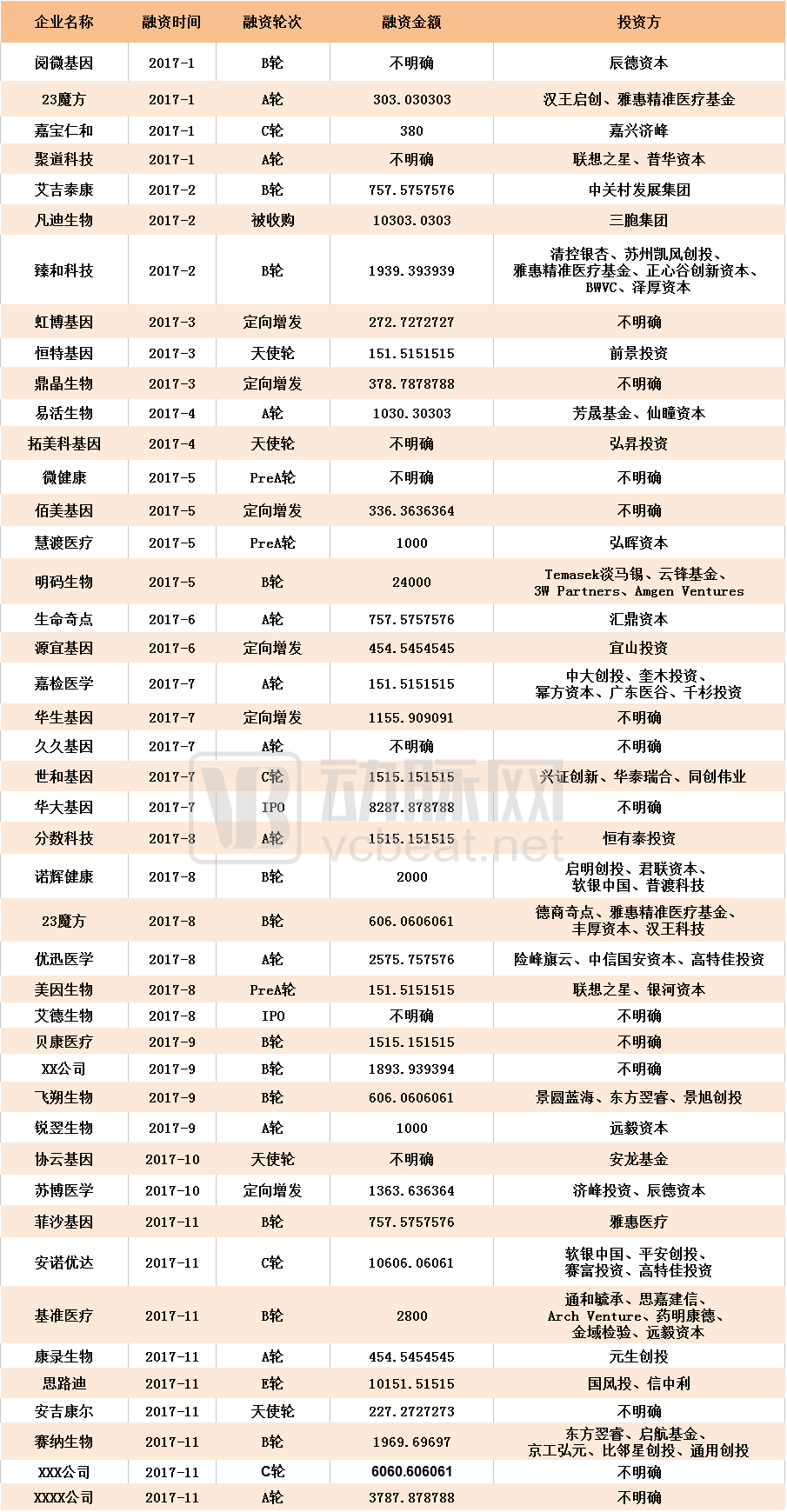

In 2017, although artificial intelligence and CAR-T therapy were dominating the trends, capital investment enthusiasm in the gene sector did not wane but instead increased, with total financing doubling compared to the previous year.

As of the end of November 2017, total financing in China’s genetic testing sector exceeded $1 billion, representing a 219% increase compared with 2016!

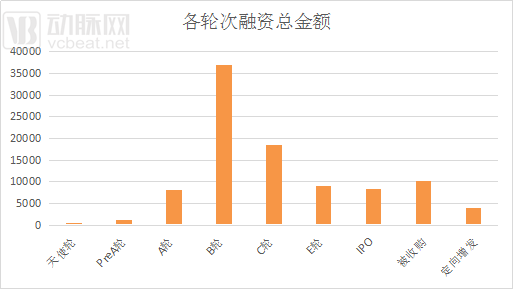

In 2017, corporate financing rounds were concentrated between Series A and Series B, whereas last year they were relatively focused on angel rounds and Series A. This indicates that most companies are gradually maturing after one year of development.

In terms of the distribution of financing amounts, the vast majority of funds flowed to enterprises at Series A and beyond. Only six companies secured angel or Pre-A round financing, accounting for a mere 1.3% of the total financing amount. This indicates that companies established in this later cohort face greater pressure to compete in this red-ocean market.

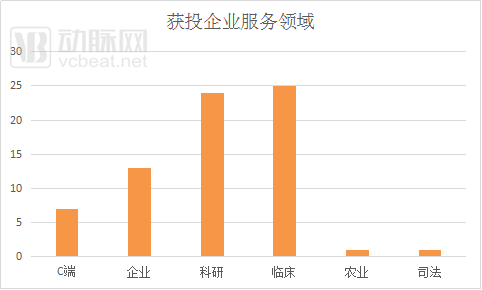

From the perspective of service domains, capital appears to favor enterprises serving the clinical and research sectors.

Technologically, the research and clinical markets are undoubtedly the high ground of this industry, where companies possessing core technologies are not easily replicated by competitors. From a market perspective, the research sector was the earliest to adopt gene technology; as for the clinical market, its scale speaks for itself—just non-invasive prenatal testing (NIPT) has sustained more than 20 companies and spawned one publicly listed entity. With the China Food and Drug Administration (CFDA) beginning to signal the orderly development of the tumor testing market, the clinical testing market is poised to grow several-fold.

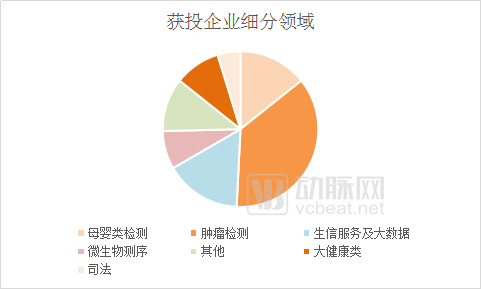

In 2017, the oncology sector emerged as the biggest winner. Among the 44 companies that received investment, 23 were involved in tumor detection-related services (excluding susceptibility gene testing). These companies aggressively attracted 54% of the total funding, amounting to approximately $560 million.

In contrast, only nine companies have secured investment in the maternal and infant testing sector (including NIPT, preconception screening, and newborn screening), a figure that pales in comparison to the number of oncology-focused enterprises. This disparity may be attributed to market maturity. The core of maternal and infant testing lies in Non-Invasive Prenatal Testing (NIPT), and with the implementation of industry regulations, the competitive landscape has largely solidified. These nine companies have raised nearly $300 million in financing, indicating that dominant players have already emerged, making it difficult for startups to challenge or disrupt the status quo.

In addition, more than 71 investment firms participated in investments in the genetic testing industry this year, including overseas early-stage venture capital firms such as Arch Venture Partners and Temasek. Among domestic institutions, Yahui Medical, Chende Capital, Dongfang Yirui, GTJA Capital, Legend Star, and Yuanyi Capital were the most active.

Continued Favorable Policy Winds

The industry's development is inseparable from policy support. Continuing the trend of last year, the state has also issued multiple policies this year to promote industrial growth.

Broadly speaking, this year’s policies can be categorized into two directions: one is to encourage frontier innovation, and the other is to regulate and implement genetic testing.

Accelerating the innovation and development of biotechnology has been a central theme in science and technology in recent years, with genetic testing constituting a critical component thereof.

In May 2017, the Ministry of Science and Technology issued the Notice on Printing and Distributing the “13th Five-Year” Special Plan for Biotechnology Innovation. The document identified breakthroughs in several key frontier technologies as the next priority tasks, including the development of next-generation gene sequencing technologies, novel gene manipulation technologies, and microbiomics.

Abstract of the “13th Five-Year” Special Plan for Biotechnology Innovation:

Development of Next-Generation Gene Sequencing Technology, emphasize the application of single-molecule technologies and the analysis and interpretation of sequencing data; develop technologies for single-cell isolation, genome amplification, transcriptome amplification, and single-cell genomic analysis; advance single-molecule detection of biomacromolecules, fluorescence in situ hybridization (FISH), and noise reduction techniques; develop protein sequencing technologies, novel mass spectrometry, and microfluidic chips; and advance precise measurement technologies for genes and proteins, promoting the development of bioassay techniques toward miniaturization, trace-level detection, single-molecule resolution, and high-throughput capabilities.

Development of Novel Precise or Quantitative Gene Editing Technologies, eukaryotic cell gene (genome) editing technology, a novel microbial gene recombination technology with significant application value in industrial production and environmental protection, promotes the integration of various gene (genome) editing methods, emphasizes the efficiency and throughput of genetic manipulation, improves ease of operation, reduces off-target effects, and expands the scope of applications.

ResearcherThe Relationship Between the Human Microbiome and Population HealthIdentify key microbiome traits and gene clusters to conduct human nutrition-related microbiome research and develop associated products; conduct research on plant symbiotic, rhizosphere, and soil microbiomes to develop agricultural and environmental microbial agents; carry out research on probiotics and gut microbiomes in poultry, livestock, and aquatic economic animals for product development; investigate industrial, environmental, and marine microbiomes along with functional regulation technologies and products. Develop high-throughput, high-precision computational methods and bioinformatics techniques for microbiome data processing, establish relevant data centers and technical platforms, and perform large-scale integration and mining of microbiome data.

In June, another “13th Five-Year Plan” was released. The Ministry of Science and Technology, the National Health and Family Planning Commission, the General Administration of Sport, the China Food and Drug Administration, the State Administration of Traditional Chinese Medicine, and the Logistics Support Department of the Central Military Commission jointly issued the “Special Plan for Scientific and Technological Innovation in Health and Wellness during the 13th Five-Year Plan Period.” The plan once again emphasized innovation in frontier technologies.Priority deployment of biotechnologies including gene sequencing, gene editing, immunotherapy, and cell therapy., and enhance the level of originality in frontier areas of medicine.

In addition to prioritizing breakthroughs in next-generation gene sequencing technologies, omics research and big data integration analysis are also on the agenda, aiming to establish a multi-level precision medicine knowledge base system and a national biomedical big data sharing platform.

In terms of implementation,In January 2017, the National Development and Reform Commission officially issued the “13th Five-Year Plan for the Development of the Biotechnology Industry,” which set a target to cover more than 50% of the newborn population with genetic testing capabilities. The plan emphasized building an integrated biological information database across different data layers, based on individual genomic information combined with related internal environmental data such as proteomics and metabolomics.

Guided by the “Plan,” localities swiftly followed suit with corresponding guidance documents.

On January 16, the official website of the Hainan Provincial People’s Government released the “Opinions of the General Office of the Hainan Provincial People’s Government on Supporting the Application of Gene Testing Technology,” which put forward 12 recommendations covering areas such as the establishment of a testing institution system, improvement of payment mechanisms, industrialization, and talent development. Meanwhile, Hainan Province also proposed to increase support for key projects, including financing support and external cooperation.

In May, the Zhejiang Provincial Price Bureau, the Health and Family Planning Commission, and the Human Resources and Social Security Department jointly issued a notice in accordance with the "Notice of the National Development and Reform Commission on Issues Concerning Accelerating the Acceptance and Review of New Medical Service Price Items," establishing pricing standards for multiple molecular diagnostic products.

In addition to these two regions, multiple provinces—including Hunan, Guizhou, Henan, and Guangdong—have successively introduced corresponding supportive policies since 2015.

On October 10, the General Office of the National Development and Reform Commission (NDRC) issued a reply concerning the construction plans for the second batch of demonstration centers for genetic testing technology applications. The General Office of the NDRC granted preliminary approval to the construction plans submitted by the development and reform commissions of Hebei, Liaoning, Jiangxi, Chongqing, Hainan, and Qinghai provinces (municipality), as well as those of Dalian and Xiamen.

The reply letter requires all provinces and municipalities to actively study and implement measures supporting the application of genetic testing technologies, strengthen coordination among various functional departments, improve the management systems and mechanisms of demonstration centers, and promote relevant entities to carry out innovations in technology, products, services, and business models.Promoting the Popularization of Genetic Testing Technology for Public Benefit。

From Made in China to Created in China

In 2017, the upstream market for gene sequencing saw substantial gains, with a total of three independently developed and innovative gene sequencers launched.

On July 31, 2017, Hanhai Gene officially launched its independently developed third-generation sequencer, GenoCare. This instrument is currently the only third-generation gene sequencer worldwide approved for clinical applications. The company stated that its technology has reached a world-leading level. Once the product is mass-produced and commercialized, the cost of whole-genome sequencing will drop sharply from $1,000 for second-generation sequencing to $100, and the sequencing turnaround time will be significantly reduced—from one week for second-generation sequencing to just one day.

On October 27, 2017, MGI Tech unveiled two high-throughput sequencers—the MGISEQ-2000 and the MGISEQ-200—at the 12th International Conference on Genomics (ICG), hosted by BGI. The MGISEQ-2000 is built upon the dual-chip independent operation platform of the BGISEQ-500, with the addition of two chips of different specifications to offer users more diverse options. A single run can generate up to 600 Gb of output data. Under full load in PE100 read length mode, it takes less than 48 hours to complete a run, achieving an annual throughput equivalent to the whole-genome sequencing data of more than 1,000 individuals.

The MGISEQ-200 retains the convenience and flexibility of the BGISEQ-50. Operating at full capacity in PE100 read-length mode, it generates 60 G of output data in less than 48 hours, enabling rapid testing of an average of 24 tumor samples per day.

Annuoda has achieved a comprehensive industrial layout across the upstream, midstream, and downstream sectors through its partnership with Illumina. On March 21, 2017, which coincided with World Down Syndrome Day (Trisomy 21 Day), Annuoda held a new product launch event in Beijing, officially unveiling the NextSeq 550AR, a new desktop high-throughput gene sequencer that had recently received registration certification from the China Food and Drug Administration (CFDA), along with a fetal chromosome aneuploidy (T21, T18, T13) detection kit based on reversible terminator sequencing technology.

To date, 12 sequencer models have been launched in the Chinese market. Coupled with domestic companies specializing in gene capture and CTC (circulating tumor cell) capture, such as AgiTech and Zhongke Natai, as well as downstream service providers like Judao Technology, China’s gene sequencing industry has initially formed an independently innovative industrial chain.

Agitron, a Chinese manufacturer dedicated to gene capture, completed its Series B financing round of RMB 50 million in February, with Zhongguancun Development Group as the investor. Domestic companies such as Sina Biology and Feishuo Biology have also secured funding in succession. Compared to the heavy investments in mid-stream sequencing enterprises over the past two years, this slight shift in capital direction reflects investors’ recognition of independent innovation enterprises and highlights the future trend of autonomous innovation within the industry.

Clinical Testing Boom: Future Explorations in Microbiomics

As mentioned earlier, tumor detection companies are the biggest winners this year. In September 2016, the China Food and Drug Administration (CFDA) accepted the application for approval of Burning Rock Biotech’s tumor detection kit, signaling that a storm was brewing in the field of tumor detection.

Annuoda’s latest funding round marks the largest publicly disclosed investment in this sector this year. One investor revealed to VCBeat that, following this round, Annuoda’s overall valuation has reached RMB 4 billion.

In addition, multiple cancer liquid biopsy companies, including New Horizon Health, Genetron Health, Huidu Medical, and Youxun Medicine, have successively secured financing. Among them, Huidu Medical’s Pre-A round reached the tens of millions of U.S. dollars, while the financing amounts for the other companies were all in the range of hundreds of millions of RMB.

From both market and technological barrier perspectives, the oncology sector is an undisputed high-valuation domain.

Exploring Microbiomics

Since the completion of the Human Genome Project in 2003, many scientists have recognized that deciphering the human genome alone does not fully unlock the key to understanding human disease and health, as humanity remains largely ignorant of the vast number of microbial communities that coexist symbiotically within the human body.

In late 2007, the U.S. National Institutes of Health (NIH) announced an investment of $115 million to officially launch the “Human Microbiome Project,” which had been in development for two years. Led by the United States, the project involved participation from more than a dozen countries, including several European Union member states, Japan, and China.

Furthermore, the United States launched the National Microbiome Initiative in May 2016; in August of the same year, the United Kingdom established the world’s largest cloud computing platform for microbial genomics. The European Union also initiated the “Human Gut Metagenomics Project.”

China’s 13th Five-Year Plan designated microbiomics as a key area for breakthroughs, drawing increasing attention from industry stakeholders. In October 2017, the “China Gut Metagenomics Project” was officially launched. The project is being implemented by RayBiotech and BGI Research, with the first phase expected to conduct metagenome-wide association studies on approximately one hundred gut microbiota-related conditions. In September 2017, the company secured $10 million in Series A financing from Yuanyi Capital.

Other microbial sequencing companies that secured financing this year include Xieyun Genomics and Wei Jiankang, which are at the angel round and Pre-A round, respectively. Although the funding amounts in this niche sector are not particularly high, the fact that companies specializing in microbial sequencing have gained capital recognition indicates, to some extent, their future potential.

Compared to tumor detection, the field of microbiology is like a gold mine waiting to be excavated.

General Health Testing: Implementation Still Requires Exploration

Compared to other sectors, the barriers to entry for testing in the broader health and consumer goods industries are relatively lower. While this sector boasts the largest number of enterprises, only a handful have successfully secured financing.

This year, a total of five companies in this sector secured financing, with the total amount falling short of $30 million. Notably, 23andMe’s Series A round was announced in January, but it was highly likely completed last year. Excluding this round, the total financing in this niche segment amounts to only $23 million. For context, a single company in the field of tumor liquid biopsy may secure funding exceeding this entire figure.

The CFDA has not yet issued corresponding regulatory guidelines for the general health and consumer genetic testing sectors; coupled with low technical barriers, this area has become a popular direction for establishing many enterprises.

The quality of companies in this field varies widely, with no shortage of amateur players who lack any real understanding of the technology or the industry. The current state of the digital health sector is characterized by a large number of tech-focused firms but relatively few securing investment.

In May 2017, VCBeat published an article addressing the current issues surrounding this category of products. Compared with clinical diagnostics, these tests target a more diverse population. As costs decline, technologies advance, and user awareness improves, this market is poised for gradual expansion. Although some products are used very infrequently, their broad target audience, coupled with favorable trends in cost, technological capability, and consumer purchasing power, is driving healthy market development.

The problem, however, is that most current products have yet to identify a truly suitable implementation model. Taking health management products as an example, consumers expect testing to provide helpful guidance for their health management. Yet the subsequent series of reports—which merely highlight high-risk factors and offer dietary recommendations—fail to create a robust industry closed loop or deliver substantial benefits to consumers. Moreover, many products still fall short of consumer expectations.

These companies have engaged in significant cross-industry initiatives and explorations within the health checkup and insurance sectors. If a viable implementation model can be identified to enhance consumer demand and willingness to pay, this is believed to represent a substantial market opportunity.

Ancestry-based products have achieved relatively successful commercial implementation, with two companies in this sector demonstrating strong growth momentum. 23Mofang has raised nearly RMB 80 million in total financing. Although WeGene has not disclosed its funding details, its development trajectory suggests that its cumulative fundraising is likely comparable. Both companies clearly position themselves in the realm of consumer-oriented, entertainment-focused genetic testing, placing less emphasis on disease diagnosis and more on helping individuals gain deeper self-understanding through their genetic information.

The two companies offer similar products, operate under comparable business models, and their pricing moves in near lockstep. Interestingly, both have independently and repeatedly slashed prices.

Following its funding round, 23Mofang swiftly reduced the price of its comprehensive genetic testing package (ancestry + genetic health) from RMB 999 to RMB 499, with WeGene quickly following suit the next day. The two companies also offered nearly synchronized discounts during major shopping festivals, ultimately maintaining their prices at the same level.

These two companies are direct competitors; if one lowers its prices, the other is bound to follow suit. Therefore, when 23mofang initially decided to cut prices, its consideration was certainly not about how many customers it could poach from competitors through price reductions. The drop from 999 yuan to 499 yuan also reignited purchase desire among many potential customers who had previously been on the sidelines.

In a subsequent interview, Zhou Kun responded that the price of 499 yuan still allows profits to be kept within a reasonable range, avoiding a cash-burn situation. Therefore, the deeper rationale behind this price war is to initiate unilateral price cuts that compel competitors to follow suit, thereby driving down overall market prices and unlocking a larger market.

As Zhou Kun stated in his response to 21st Century Business Herald, “Price reductions are beneficial for both users and the industry.” Moreover, when the market scale reaches a certain magnitude, there is even the possibility that they may turn around and demand price cuts from upstream enterprises.

Artificial Intelligence Brings New Perspectives to Genomic Big Data

Bioinformatics and big data have perfectly exemplified what constitutes a "small but beautiful" niche in the downstream sector. The decline in sequencing costs inevitably places pressure on data processing capabilities, while simultaneously expanding the market. However, there has not been a significant influx of large enterprises into this field, which may be partly attributable to entry barriers. More likely, however, this is due to the inherent nature of the sector: bioinformatics services function more as tools, and thus do not require the large-scale sales or marketing teams typical of product-driven businesses.

Furthermore, product-market fit is crucial, as inferior products are quickly eliminated. Consequently, companies in this sector have secured relatively strong financing.

AlphaGo’s consecutive victories over Lee Sedol and Ke Jie set off a global wave of artificial intelligence. In the healthcare sector, AI is also making inroads through intelligent imaging, intelligent diagnosis, and data mining.

In the field of genomics, AI- and big data-driven products are also emerging as a growing trend.

In fact, as early as several years ago, many downstream data service providers were already attempting to leverage artificial intelligence for prospective research aimed at accelerating data analysis and interpretation. There is no doubt that AI excels in processing sequential data; however, the associations between genes and diseases are far more complex than the rules of Go.

Under current conditions, leveraging artificial intelligence for data analysis and processing, or even relatively straightforward interpretation, is indeed a promising approach; however, when it comes to diseases involving complex associations, more time and data are required to refine the models.

Leading Companies Go Public, Tencent Enters the Fray

2017 marked the inaugural year for initial public offerings (IPOs) in the next-generation sequencing (NGS) industry, with two leading companies, BGI Genomics and Berry Genomics, going public in succession. Notably, BGI Genomics saw its market capitalization surpass RMB 100 billion within just a few months.

Beyond new entrants, companies in other sectors of the secondary market are also strategically positioning themselves through capital maneuvers such as investments and acquisitions.

In February 2017, Sanpower Group announced the acquisition of Vandy Diagnostics for RMB 680 million, setting a record for M&A transactions in China’s NGS industry. In November, KingMed Diagnostics participated in the Series B financing round of Basecare Medical, two months after its initial public offering.

Most of these listed companies originated in traditional or heavy industries and began expanding into high-tech sectors after going public, with gene sequencing and precision medicine becoming popular choices for many enterprises.

After Alibaba, Tencent Quietly Enters the Fray

In recent years, the three tech giants—Baidu, Alibaba, and Tencent (collectively known as BAT)—have invested significant efforts in the healthcare sector. However, within the genomics industry, aside from frequent collaborations between Alibaba Cloud (under Alibaba Group) and this sector, Tencent and Baidu have remained relatively quiet.

This year, Tencent has also begun to take action.

In 2017, Grail, a cancer early screening company that had been established for just over a year, secured $900 million in Series B financing. Among the investors in this round of sky-high financing was the Chinese investor Tencent.

In June 2017, the Intel BioIT Forum was held in Beijing. In addition to Alibaba Cloud, a regular attendee, Tencent Cloud also made a surprise appearance. Reportedly, this marked Tencent Cloud’s first public exposition of its perspectives and plans for the life sciences sector. However, at that time, Tencent Cloud had not yet undertaken any substantial initiatives.

Four months later, Tencent Cloud reappeared at the 4th National Functional Genomics Summit in China. At the conference, Tencent Cloud announced its strategic partnership with Biomarker Technologies and officially launched its biological genomics solutions, opening up its IT capabilities such as cloud computing, storage, and artificial intelligence to support the development of the biological genomics industry.

Company A and Company T have successively entered the market, while Company B has yet to make any moves; we shall see what happens next year.

Future Trends

Clear Industry Specialization

From last year’s perspective, the enterprises capable of entering the upstream market were basically industry giants. After years of cultivation in the midstream and downstream sectors, they had accumulated sufficient talent and resources to begin penetrating the upstream segment, thereby completing their full industrial ecosystem chain.

Among the companies listed in recent years, aside from Annoroad Gene Technology, Hanhai Genomics and Sinocelltech are more akin to “small but beautiful” enterprises. These companies have not been established for very long and operate on a relatively small scale; however, their founders hail from top-tier international institutions and possess world-leading technologies.

On the one hand, midstream enterprises are overly saturated, prompting them to venture into blue-ocean markets. On the other hand, this trend is also a result of macroeconomic policies in recent years that have encouraged independent innovation and original drug development.

In the future, as these domestically produced products mature, a wave of import substitution may sweep through the industry. Moreover, due to the price advantage of domestic products, there may be an overall price reduction for market-oriented products.

Meanwhile, as domestic industry players increasingly pursue self-reliance and enhance their technological capabilities, the division of labor within the sector is becoming increasingly pronounced. In the future, companies may no longer aim to control every link in the value chain; instead, they will leverage their own strengths while integrating those of others to jointly build an ecosystem.

Multi-Omics Data-Assisted Clinical Diagnosis

Whether from a policy perspective or an enterprise perspective, the integration of gene sequencing into clinical practice has long become an irreversible trend.

With the rise of cutting-edge technologies such as molecular diagnostics, proteomics testing, and medical imaging, our understanding of diseases has become more multidimensional. However, these technologies currently operate largely in isolation; integrating multi-dimensional data can provide a clearer and more comprehensive understanding of diseases.

With the advent of artificial intelligence and machine learning, the integration of such data has become more accessible. Consequently, the future trend is not for genomic sequencing to operate in isolation within clinical practice, but rather to integrate with other omics data to quantify and elucidate diseases, thereby enabling more precise clinical diagnosis and treatment.

In 2016, while the gene testing industry gained momentum, it also faced ongoing controversies: “capital frenzy,” “precision medicine bubble,” and a lack of upstream productivity. In 2017, sustained capital interest, along with policy support and recognition, favorably demonstrated the industry’s strength and potential. The launch of three independently developed sequencers further signified a breakthrough in China’s upstream sequencing sector. Amidst both skepticism and encouragement, the industry continued to flourish. Bubbles may exist in any industry, but they are not entirely detrimental; after the tide recedes, the bubbles will burst, yet the pearls will remain.