Healthcare Payment Industry 2017 Year-End Review: Over 7,000 Cross-Provincial Designated Medical Institutions Go Live as Ant Financial and Tencent Intensify Market Competition

Before conducting a review of the healthcare payment industry in 2017, we must first ask the following questions:

1. What is the progress in the implementation of the national platform for direct settlement of cross-provincial medical expenses?

2. Regarding Document No. 55 issued by the State Council, what is the current status of its implementation across China?

3. In the Mobile Healthcare Payment Market, Which Is More Dominant: WeChat or Alipay?

4. What business changes occurred in the healthcare payment market in 2017 for publicly listed healthcare IT companies?

These four questions essentially encapsulate all the changes that occurred in the healthcare payment industry in 2017. This article will provide answers to each of them one by one.

Nationwide Direct Settlement for Cross-Provincial Medical Treatment

Direct Settlement for Cross-Regional Medical Care refers to the process whereby basic medical insurance enrollees who have completed the required filing procedures receive treatment at designated medical institutions outside their place of insurance coverage and settle inpatient medical expenses directly. When receiving inpatient care across regions, enrollees are only required to pay the out-of-pocket portion as stipulated by policy, while the remaining costs are covered by the medical insurance administration agency.

National Platform for Direct Settlement of Cross-Provincial Medical ExpensesThe National Platform for Direct Settlement of Cross-Provincial Medical Expenses was developed in accordance with the overall plan of Phase II of the Golden Insurance Project. Leveraging the Golden Insurance Project network and using the Social Security Card as the primary medium, the platform operates on the principles of “applying the medical treatment location’s drug and service catalog while adhering to the insured location’s reimbursement policies” and “real-time transmission of broad categories with post-service transmission of detailed items,” thereby enabling direct settlement of medical expenses for insured individuals receiving care across provincial boundaries.

The system supports cost auditing and regular disbursement for designated medical institutions, primarily managed by the place of treatment, enabling periodic inter-regional settlement and fund transfers; it also facilitates collaborative processing of cross-provincial remote medical care networked settlements, providing convenient and efficient direct settlement services for medical expenses to individuals seeking healthcare across provincial boundaries.

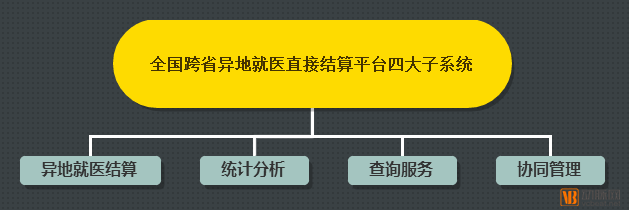

China's National Direct Settlement Platform for Cross-Provincial Medical Care includes the following four major subsystems:

Among these, the Inter-provincial Medical Treatment Settlement System serves as the data exchange hub for cross-provincial medical care, facilitating data exchange across various regions. The Statistical Analysis System functions as the fund clearing center for cross-provincial medical treatment, handling reconciliation, clearing, and monitoring of medical expenses incurred outside the insured’s home region. The Query Service Center and Collaborative Management System act as the data resource center for cross-provincial medical care, responsible for storing enrollees’ out-of-area medical treatment registration information, basic catalog information, information on contracted designated healthcare institutions, and records of medical visits and settlement payments, while also conducting data analysis and application.

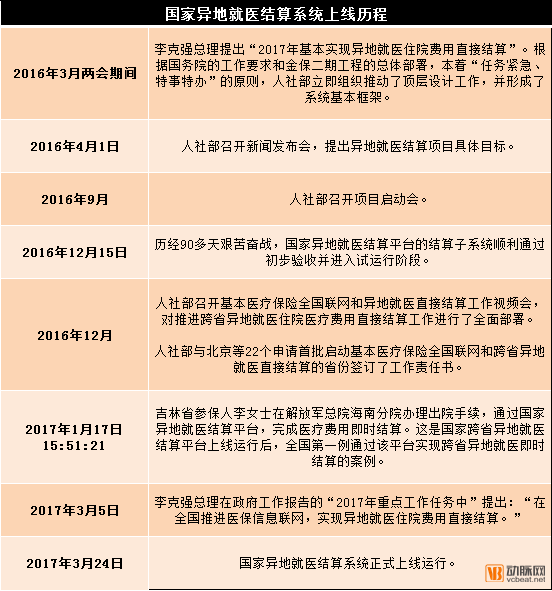

A review of the launch process reveals that within just one year, the national platform for direct settlement of cross-provincial medical expenses went from basic framework to full operational status, underscoring its significant importance.

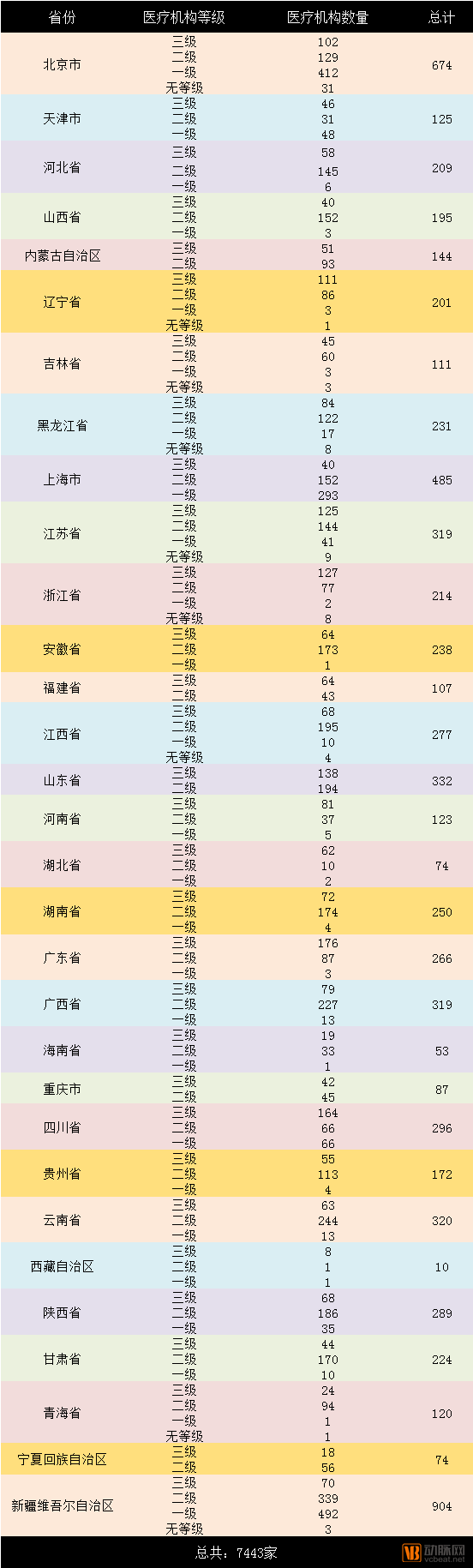

On October 25, 2017, the Ministry of Human Resources and Social Security released the sixth batch of designated medical institutions for cross-provincial basic medical insurance. As of October 15, on the basis that all provincial platforms and all pooling areas across China had achieved connectivity with the National Direct Settlement Platform for Cross-Provincial Medical Care, the number of designated medical institutions for cross-provincial care increased to 7,443. More than 80% of counties and districts now have at least one designated medical institution capable of providing direct settlement services for inpatient medical expenses incurred during cross-provincial medical care.

VCBeat compiled the list and produced the following table:

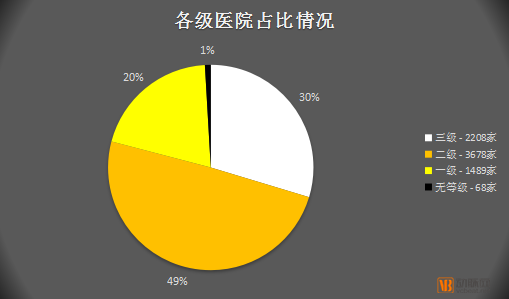

As shown in the table, among the 7,443 designated medical institutions across China providing cross-provincial services, secondary hospitals accounted for 49% (3,678 institutions); tertiary hospitals accounted for 30% (2,208 institutions); primary hospitals accounted for 20% (1,489 institutions); and unclassified hospitals accounted for 1% (68 institutions).

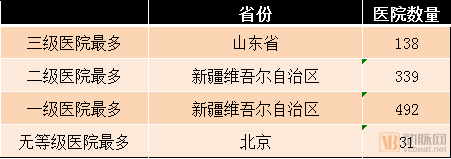

The following are the provinces with the top ten and bottom-ranked hospitals connected to the network:

Among them, Shandong Province has the highest number of tertiary hospitals connected to the network, Xinjiang has the highest number of secondary and primary hospitals connected, and Beijing has the highest number of unclassified hospitals connected.

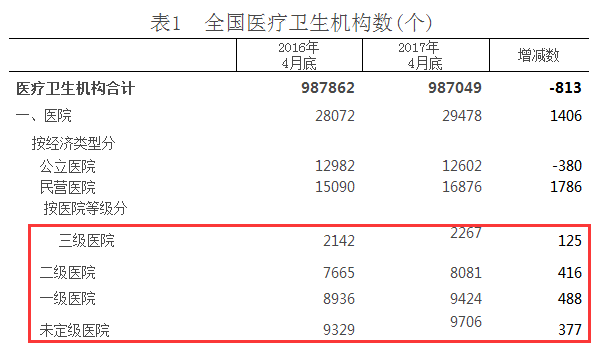

In late April 2017, the Statistical Information Center of the National Health and Family Planning Commission released data on the number of medical and health institutions nationwide. The data showed that China had 2,267 tertiary hospitals, 8,081 secondary hospitals, 9,424 primary hospitals, and 9,706 ungraded hospitals.

By integrating data from the two tables, we can analyze that approximately 97.4% of tertiary designated medical institutions have been connected to the network; approximately 45.5% of secondary hospitals have been connected; approximately 15.8% of primary hospitals have been connected; and only about 0.7% of non-graded hospitals have been connected.

We attribute these results to two factors:

On the one hand, this is due to disparities in informatization capabilities among medical institutions at different levels. Previously, we had discussed in “Medical Big Data: Foundations Remain Lagging; Entry of National Teams and AI Companies in 2017 May Spark a New Round of Fierce Competition》As analyzed in this article, the current level of basic informatization application in China remains relatively low, particularly in hospitals below Tier 3, where there is still a long way to go in terms of informatization construction. The proportion of network connectivity across hospitals at various levels also serves to substantiate this conclusion to some extent.

On the other hand, it is related to patients’ healthcare-seeking needs. At present, although the state vigorously promotes tiered diagnosis and treatment, the siphon effect of Grade A tertiary hospitals makes them still the first choice for patients. Compared with these institutions, secondary hospitals, primary hospitals, and even ungraded hospitals have a much weaker demand for cross-regional direct settlement. Therefore, achieving cross-regional direct settlement in Grade A tertiary hospitals across China has become the core focus currently, and the results have been highly significant.

The Era of Diagnosis-Related Group (DRG) Payment Has Arrived

For a long time, fee-for-service has been the primary model for hospital billing and health insurance reimbursement in China. Currently, fiscal subsidies from governments at all levels account for only 8.22% of the actual operational expenditures of public hospitals at the county level and above. The remaining compensation for these hospitals is primarily derived from their own revenue generated through medical service activities.

Furthermore, public hospitals are subject to strict government-set pricing for medical services, with price levels far below the actual cost of care. These prices fail to reflect the labor value of healthcare professionals and are insufficient to cover the operational costs of hospitals.

Meanwhile, the absence of clear application management mechanisms for pharmaceuticals and medical consumables has led to revenue from these items becoming the primary means of hospital compensation. This is the fundamental reason behind the formation of the “drug-revenue-subsidized healthcare” compensation mechanism.

Under this compensation mechanism, healthcare institutions induce patient consumption through a fee-for-service payment model. The prescription of excessive medications, the misuse of high-value consumables, and the overuse of diagnostic tests have become the most prominent manifestations of profit-driven behaviors in hospitals, with such trends intensifying over time.

These mechanisms and tendencies have led to increased sales volumes of pharmaceuticals and medical consumables, as well as higher utilization rates of diagnostic and laboratory tests, driving a rapid surge in healthcare expenditures. This has placed an unsustainable burden on medical insurance funds and increasingly weighed down patients with out-of-pocket medical costs. Implementing diagnosis-related group (DRG)-based payment is one effective approach to addressing these issues.

The series of policies promulgated in 2017 also indicates that China has entered the era of diagnosis-related group (DRG) payment. Among them, Document No. 55 issued by the General Office of the State Council in June was the most influential.

In accordance with the requirements of the “Opinions,” starting from 2017, budget management of medical insurance funds was further strengthened, and a diversified, composite medical insurance payment system dominated by diagnosis-related group (DRG)-based payments was comprehensively implemented. Localities were required to select a certain number of disease conditions for implementation of case-based payment, while the national government selected certain regions to pilot payment based on Diagnosis-Related Groups (DRGs). Localities were encouraged to improve various other payment methods, such as capitation and per-diem payments. By 2020, reforms in medical insurance payment methods covered all medical institutions and medical services nationwide; a diversified, composite medical insurance payment system adapted to different diseases and service characteristics was widely implemented across China, and the proportion of fee-for-service payments decreased significantly.

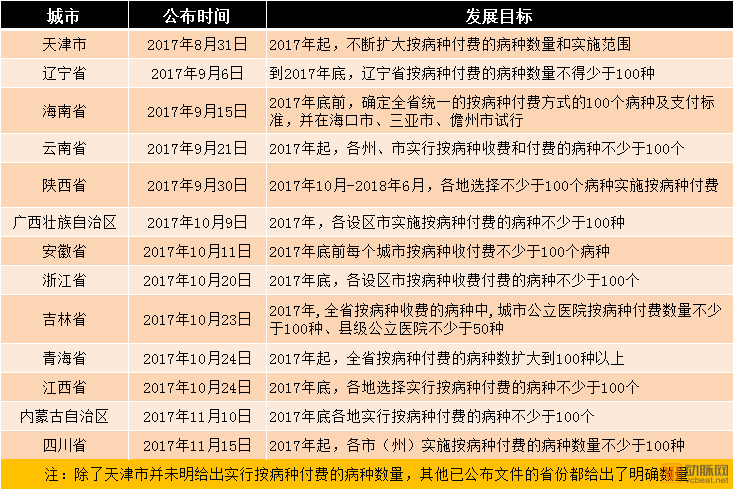

In the aforementioned objectives, the “Opinions” did not impose mandatory quotas on the number of diseases covered under diagnosis-related group (DRG) payment. Following the release of the “Opinions,” provinces and municipalities across China subsequently issued their own implementation plans in line with its guiding principles. In this regard, VCBeat has compiled the DRG payment implementation targets outlined in the development goals of various regions:

It is evident that Tianjin Municipality has been the quickest to follow up with policies, although it did not explicitly specify target figures. Liaoning Province was the first to clearly define the number of disease categories subject to diagnosis-related group (DRG) payment, and subsequent provinces that followed suit have all set their targets at more than 100 categories.

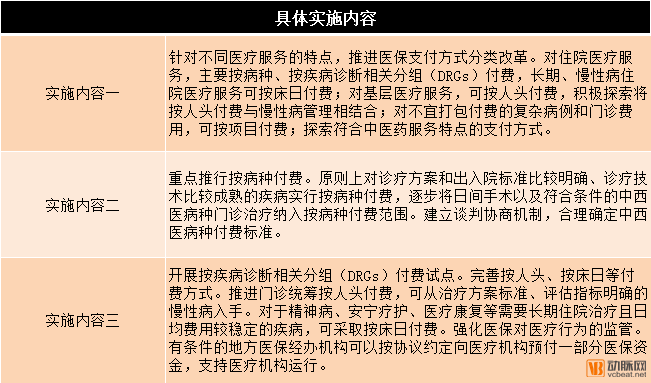

To achieve this goal, reforms to health insurance payment methods have been initiated primarily in the following areas.

In fact, to ensure the effective implementation of the pilot program, the National Health and Family Planning Commission has formulated the C-DRG payment and charging standards and established a nationwide cost monitoring platform.

The full name of C-DRG is the "National Standard for Diagnosis-Related Group (DRG)-Based Payment and Charging." It is a DRG-based payment and charging system with Chinese characteristics, developed over ten years by a national large-scale research task force established by the Health Development Research Center (hereinafter referred to as the "Research Center") under the commission of the Department of Finance of the National Health and Family Planning Commission.

C-DRG is not a simple grouping or service, but rather a comprehensive system. This system consists of one standardized framework, three foundational tools, one cost platform, and a set of principles for payment policies, collectively referred to as the “1311” system.

In June 2017, public hospitals in three cities—Shenzhen in Guangdong Province, Karamay in the Xinjiang Uygur Autonomous Region, and Sanming in Fujian Province—as well as three provincial- or municipal-level hospitals, namely the Affiliated Union Hospital of Fujian Medical University, Fuzhou First Hospital, and Xiamen First Hospital, announced the simultaneous launch of DRG pilots. Particularly following the issuance of Document No. 55, C-DRG is poised to expand nationwide.

A Duopoly in the Mobile Healthcare Payment Market

Alipay has long adhered to the philosophy of consolidating all industry chains involved in healthcare onto a single platform with minimal steps. Internally, this driving force is referred to as “Techfin,” whose core lies in opening up infrastructure to partners and customers across the entire ecosystem, leveraging data as the foundation and technology as the means to enhance efficiency and reduce costs for the industry.

Throughout 2017, Ant Financial has transformed its capabilities in payment, security, data, as well as its proprietary credit, financial services, and anti-fraud systems into infrastructure, making them available to its healthcare ecosystem partners.

After binding and generating an electronic social security card via Alipay, users in many cities can seek medical treatment at hospitals and pharmacies without carrying a physical card, conveniently completing payments for both medical insurance-covered and out-of-pocket expenses through their mobile phones. Meanwhile, some cities have introduced specialized features. In Hangzhou, the family mutual aid function for medical insurance accounts allows users to share their medical insurance balance with family members and relatives, while the medical insurance consumption alert feature pushes every medical insurance transaction record to users via Alipay statements, ensuring transparent spending. In Wuhan, the electronic social security card for university students eliminates the need for incoming freshmen to apply for a physical social security card.

Leveraging the ecosystem capabilities and traffic entry points provided by Ant Financial, a range of deep-vertical applications across various industries have emerged, fostering a symbiotic and mutually prosperous industrial model between enterprises and Ant Financial. It is foreseeable that more healthcare service providers will rely on the “Future Hospital” platform to penetrate into various niche segments of the medical industry.

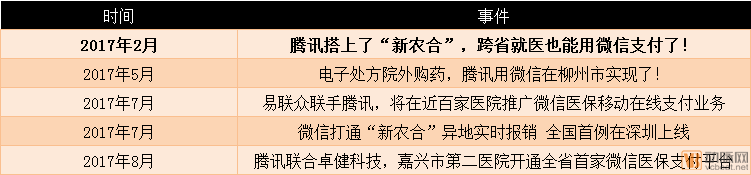

Compared with Ant Financial’s ecosystem development, Tencent’s medical payment initiatives in 2017 focused more on cross-province medical treatment and payments under the New Rural Cooperative Medical Scheme.

2017 Tencent-Related Medical Payment Incidents (Reported by VCBeat):

To date, residents of cities such as Shenzhen, Wuhan, Xiamen, Chengdu, Zhengzhou, Shantou, Yan’an, Kaifeng, Jiaxing, and Tongchuan have been among the first to enjoy the convenience of WeChat medical payments. Some cities that initially launched WeChat medical insurance payment services are continuing to upgrade their systems; for instance, residents of Zhengzhou can now experience the “card binding without prior authorization” service in advance. Residents of Gansu Province, Shaanxi Province (excluding Yan’an City), and Ningbo City can already link their medical insurance cards to WeChat to check their balances without requiring a password.

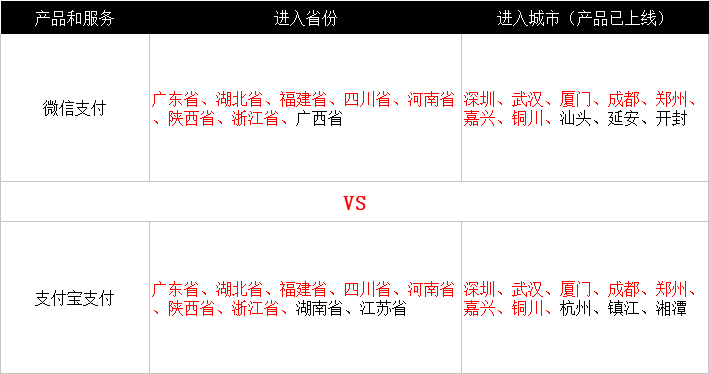

Based on the rapid expansion of WeChat and Alipay in mobile healthcare payments in 2017, VCBeat conducted a comparative analysis of the two platforms from the perspectives of market presence and capabilities:

Markets Already Implemented

(Red indicates shared items)

(Data source: Public information from Tencent and Ant Financial; as of November 2017)

Market data indicates a high degree of overlap between the two parties in terms of provinces and cities where their solutions have been implemented, with overall progress being virtually neck-and-neck.

Comparison of Capabilities and Functions

(Check “√” for present, “\” for absent)

A comparison of their core capabilities and primary functional services reveals that Alipay holds a slight edge in core capabilities, while WeChat has a slight advantage in features and services. Overall, the two are evenly matched.

Diverse Development Paths for Listed Healthcare IT Companies

Jiuyuan Yinhai is the leading enterprise in informatization for the human resources and social security sector, a strategic partner of the Ministry of Human Resources and Social Security (MOHRSS) in industry informatization development, and the primary developer of Versions 1, 2, and 3 of the MOHRSS’s core platform for social insurance management information systems. The company has participated in the top-level design and standard-setting of the Golden Insurance Project. It has exclusively undertaken the construction of national-level information platforms, including the National Platform for Cross-Regional Medical Expense Settlement, the National Public Service Platform for Human Resources and Social Security for Urban and Rural Residents, the National Actuarial Platform for Pension and Medical Insurance, the MOHRSS Macro Decision Support System, and the MOHRSS Information System for Pension Insurance of Government Agencies and Public Institutions.

In 2016, Jiuyuan Yinhai undertook the construction of the National Platform for Cross-Regional Medical Expense Settlement. As of July 31, 2017, it had facilitated the integration of all provinces across China (covering 393 prefecture-level cities and 5,102 hospitals), ensuring the stable operation of the national cross-regional medical expense settlement services.

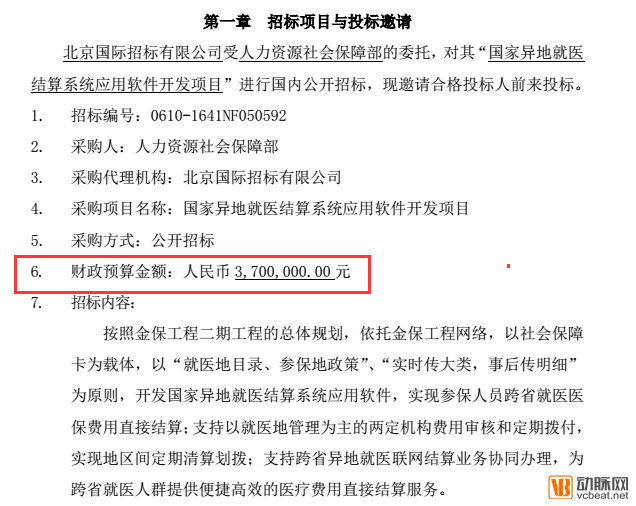

Based on the tender documents for this project, the contract value is RMB 3.7 million, which is not a significant amount.

Source: Bidding Documents for the Application Software Development Project of the National Cross-Regional Medical Expense Settlement System, Issue 0810

Furthermore, the company has also undertaken the construction of multiple national-level projects, including the National Public Service Platform for Human Resources and Social Security for Urban and Rural Residents, the National Actuarial Platform for Pension and Medical Insurance, the Ministry of Civil Affairs’ National Household Economic Status Verification System, and the “Internet+” Social Security Convenience Service Platform.

In 2017, Jiuyuan Yinhai’s revenue increased by 20.12% year-on-year. According to the semi-annual report, the primary driver was growth in software and system integration income. VCBeat believes that although the implementation of the National Platform for Cross-Provincial Medical Expense Settlement, for which the company serves as a key contractor, has not significantly impacted its revenue, this national-level project is expected to bolster the company’s overall performance.

In the field of medical insurance management, Neusoft Group has signed contracts with multiple cities, including Changzhou, Qinhuangdao, Shijiazhuang, and Changchun.

The company has undertaken medical insurance cost-control initiatives, including the Xining Medical Insurance Monitoring system and the Baoshan Urban-Rural Integration project. It has signed contracts for medical insurance settlement projects with companies such as Guoyuan Agricultural Insurance, Yunnan Hongxiang, and Chengdu Lianhe. Furthermore, it collaborates with insurers—including PICC, China Life, Taikang Insurance, Sunshine Insurance, and China Continent Insurance—to integrate medical insurance and commercial insurance systems for synchronized settlement.

In addition, Neusoft Group has undertaken the construction of cross-provincial medical expense settlement platforms in 12 provinces, providing platform access services to more than 150 prefecture-level cities.

On July 20, 2017, the Company entered into a strategic cooperation agreement with Shenzhen Tencent Computer Systems Co., Ltd. to promote WeChat’s mobile online payment services for medical insurance across China, deepen collaboration on the “Internet + Ecosystem Hospital” initiative, and explore innovations in medical artificial intelligence. Both parties will actively contribute to building Internet-based payment systems for the human resources and social security, healthcare, and medical insurance sectors.

Leveraging Tencent’s WeChat and QQ ecosystems, payment capabilities, extensive data foundation, and mature cloud computing services, along with Yilianzhong’s leading industry products and technological strengths in human resources and social security, healthcare, payments, social security cards, and self-service terminals, as well as its rich industry resources, both parties will fully integrate their respective advantages. With “Internet + Human Resources and Social Security,” “Internet + Healthcare,” and “Internet + Industry Payments” solutions as key points of integration, and aiming to jointly build a leading Internet-plus industry system, the two parties will engage in comprehensive, in-depth strategic cooperation.

On November 10, Haihong Holdings released a detailed report on changes in equity interests. The equity structure of Zhonghaiheng, the controlling shareholder of Haihong Holdings, has undergone changes. China National Cultural Industry Investment Fund will inject RMB 500 million in capital to become the controlling shareholder of Zhonghaiheng, thereby becoming the indirect controlling shareholder of the listed company. The actual controller of the listed company has changed to China Reform Holdings Corporation.

Data shows that the primary client of Haihong Holdings is the Basic Medical Insurance Fund, which is currently the largest medical insurance fund in China, featuring the most comprehensive coverage of disease types, the most complex demographic structure, the widest regional span, and the most extensive data on pharmaceuticals, medical consumables, medical devices, medical service items, and diagnosis and treatment information.

For China Reform Holdings Corporation (CRHC), acquiring controlling interest in a listed company with a market capitalization of RMB 24.4 billion for just RMB 500 million was not a high price to pay. By positioning itself at the core of medical insurance payments, Haihong Holding serves as a pivotal hub connecting medical insurance, healthcare services, and pharmaceuticals. CRHC can leverage Haihong Holding’s existing technical capabilities and market share to further enhance its medical insurance services.

VCBeat’s analysis suggests that although Haihong Holdings has vigorously promoted its PBM business over the past two years, the results have been less than ideal. With the national government strongly advocating for diagnosis-related group (DRG)-based payment, Haihong Holdings, now a state-owned enterprise, may leverage its existing PBM operations to naturally expand into DRG-related initiatives.