The Tug-of-War Between Profit and Regulation: Pharma Companies Eye China's RMB 130 Billion Primary Care Drug Market, Capped by医保 Reimbursement Limits

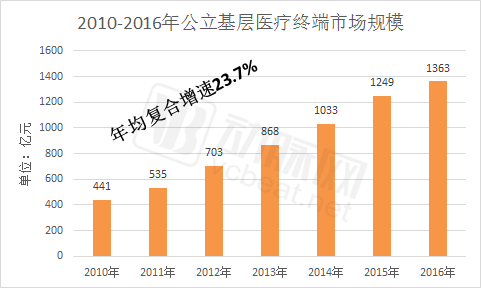

With the implementation of the tiered diagnosis and treatment policy, the primary healthcare market has become a key focus for pharmaceutical companies in recent years and is one of the fastest-growing segments in terms of scale. According to relevant data, the market size of public primary healthcare terminals reached RMB 136.3 billion in 2016, accounting for 9.1% of the total pharmaceutical market (RMB 1,497.5 billion), whereas this figure was only 6.6% in 2011.

The rapid growth of the primary healthcare market is driven by multifaceted factors: first,The Effectiveness of Tiered Diagnosis and Treatment Is Prominent, the increase in patient visits at primary healthcare institutions has driven pharmaceutical sales; secondly, policies such as the “Two-Invoice System” and “Zero Markup” have prompted tertiary public hospitals to open up their pharmacies,Primary Healthcare Institutions Partially Assume the Pharmacy Functions of Tiered Hospitals; thirdly, the policies on medical consortiums and family doctor contract services have enabledEnhanced Service Capacity of Primary Healthcare Institutions and Increased Patient Stickiness, pharmaceutical care services have become an important component.

As primary healthcare experiences a comprehensive rise, pharmaceutical companies and pharmaceutical commercial enterprises are increasingly prioritizing the grassroots market, ramping up their investments through academic promotion, physician education, network development, and patient education.

In the process of pharmaceutical companies and commercial enterprises laying out their strategies for the grassroots market, they have also encountered many problems. For example, there is a lack of appropriate methods, low return on investment, and restrictions on grassroots procurement due to medical insurance limits. Only by solving these problems can pharmaceutical companies and distribution enterprises better lay out their strategies in the grassroots market.

The Market Size of Primary Healthcare Drugs Exceeds 100 Billion Yuan

Primary healthcare institutions refer to community health service centers and stations, township health centers, and village clinics. Characterized by their large numbers and extensive coverage, they serve as the most accessible channel for residents to seek medical care and are known as the "gatekeepers" of public health. These institutions undertake the functions of diagnosis and treatment, rehabilitation, and long-term medication management for residents, playing a foundational role in the healthcare system.

In China, 80% of medical and health resources are concentrated in urban areas, with 80% of those further concentrated in large and medium-sized hospitals, forming an "inverted triangle" resource structure. Meanwhile, the majority of demand for medical and health services lies at the primary care level, forming a "regular triangle" demand structure.The inverted triangle of medical resources and the upright triangle of medical demand have led to difficulties in accessing healthcare, while tiered diagnosis and treatment can effectively address this challenge., while also curbing the overtreatment of minor ailments, and in conjunction with policies such as the separation of prescribing from dispensing, aims to control the unreasonable growth of medical insurance expenditures.

In 2009, China’s “New Healthcare Reform” first introduced the concept of tiered diagnosis and treatment, requiring conditions to be classified by severity and urgency as well as by the complexity of treatment, with medical institutions at different tiers assuming responsibility for treating different categories of diseases. This tiered model, spanning from general practice evaluations to specialty care, aims to achieve initial consultations at primary care facilities, two-way referrals, separate management of acute and chronic conditions, and coordinated care across different levels of the healthcare system, ultimately establishing an ideal pattern in which minor illnesses are managed in the community, serious conditions are treated in hospitals, and rehabilitation is conducted back in the community.

In August 2016, the National Health and Family Planning Commission issued the "Notice on Advancing Pilot Programs for Tiered Diagnosis and Treatment," designating four municipalities directly under the central government and 266 prefecture-level cities to carry out pilot initiatives for tiered diagnosis and treatment.Pilot cities account for 88% of the total number of cities in China.

The notice requires implementing tiered diagnosis and treatment by further enhancing primary care capabilities, advancing family doctor contract services, exploring the establishment of medical consortia, scientifically implementing separate management of acute and chronic conditions, and promoting healthcare informatization to facilitate regional sharing of medical resources.

From the perspective of implementation outcomes, tiered diagnosis and treatment has demonstrated a significant effect in diverting patient flow. Taking Beijing as an example, data from the Beijing Municipal Health and Family Planning Commission shows that, compared with the same period in 2016, outpatient and emergency visits at tertiary and secondary hospitals decreased by 11.5% and 3.9%, respectively, while those at primary hospitals and grassroots medical and health institutions increased by 14.7%. The volume of diagnoses and treatments at some community health service centers in urban areas rose by more than 20%. Common and routine diseases have been gradually diverted to grassroots institutions, alleviating the overcrowding at large hospitals.

The increase in patient visits has directly led to changes in drug sales. According to data from Menet,Since 2010, the market size of pharmaceuticals at primary-level public medical terminals has grown at an average annual rate of 23.7%, reaching RMB 136.3 billion in 2016, accounting for approximately 9.1% of the total sales across China’s three major pharmaceutical market segments.

Domestic and Foreign Pharmaceutical Companies Each Excel in Their Own Right

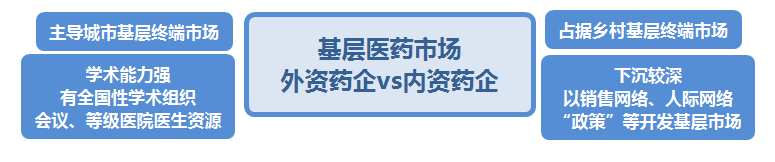

In terms of market share, foreign-funded pharmaceutical companies and domestic pharmaceutical companies each have their own advantages in the urban primary healthcare market and township health centers.The former dominates cities, while the latter entrenches itself in rural areas.

Bayer Healthcare, Pfizer, Novo Nordisk, and Sanofi ranked as the top four pharmaceutical companies in urban community healthcare medication, while Novartis ranked ninth. Together, these foreign pharmaceutical companies accounted for 12.94% of the market share in urban community healthcare medication terminals. In contrast, all of the top ten pharmaceutical companies in the township health center medication market were domestic enterprises, collectively holding a 13.67% market share.

The differing performance of domestic and foreign pharmaceutical companies in the primary healthcare market is closely tied to their respective strategies in this sector.

Industry insiders told VCBeat that foreign pharmaceutical companies possess strong academic capabilities, enabling them to leverage mainstream industry associations and organizations, combined with resources from tertiary hospitals, to provide primary care institutions and physicians with academic capacity building, departmental development, and treatment guidelines, thereby achieving radiation and coverage at the grassroots level. In contrast, domestic pharmaceutical companies, especially smaller manufacturers, place greater emphasis on “policy” and rely on regional sales networks and interpersonal relationships.

According to their observations, both domestic and foreign pharmaceutical companies are currently increasing their investment in the primary healthcare market, with common practices including expanding sales networks, academic promotion, and patient education.

“Fragmented, small-scale, and dispersed operations characterize the primary healthcare market. Under the tiered diagnosis and treatment policy, the primary care sector is poised for sustained growth in the future. To maintain existing market share and capture new segments, concerted efforts must be directed toward developing the primary care market—a strategy equally applicable to both foreign and domestic enterprises.”

An industry insider stated that their company began developing the grassroots market early, proposing a strategy to penetrate grassroots levels around 2011, and has since established a nationwide sales network across China.

In his view, pharmaceutical companies must go through two phases to develop the primary care market: the first phase involves early-stage development, including tendering and bidding, establishing marketing networks, and ensuring distribution coverage; the second phase focuses on refined terminal management, physician education, and patient education.

“You must first win the tendering and bidding process before entering the primary healthcare market. Then, you need to have a clear understanding of the specific conditions at the grassroots level, such as medication usage patterns at each terminal point and physicians’ prescribing habits. For patients requiring long-term medication or those with chronic diseases, brand building can be achieved through free clinic services and promotional discounts.”

Pharmaceutical companies, in the process of developing the primary care market,A more effective approach lies in aligning with and adapting to the developmental needs of primary healthcare.

“Grassroots healthcare institutions seek to enhance their diagnostic and treatment capabilities to retain patients. Pharmaceutical companies entering this sector should leverage this characteristic by providing tailored services. For patients with chronic conditions requiring long-term care, key considerations include medication efficacy, cost, and side effects. Although prescribing authority rests with physicians, brand communication directed at patients remains a viable strategy.”

Overall, both foreign and domestic pharmaceutical companies are still in a state of continuous adjustment in their development of the primary healthcare market. Unlike the tiered public hospital market, which has established systems and proven strategies, the vast primary healthcare market provides fertile ground for experimenting with more effective operational models.

Medical Insurance Caps Are the Biggest Obstacle to Growth in the Primary Care Market

When asked about the challenges encountered in expanding into the primary care market, the aforementioned industry insider told VCBeat that medical insurance reimbursement caps have imposed a ceiling on growth in this sector, becoming the biggest obstacle for pharmaceutical companies seeking to expand their presence in the primary care market.

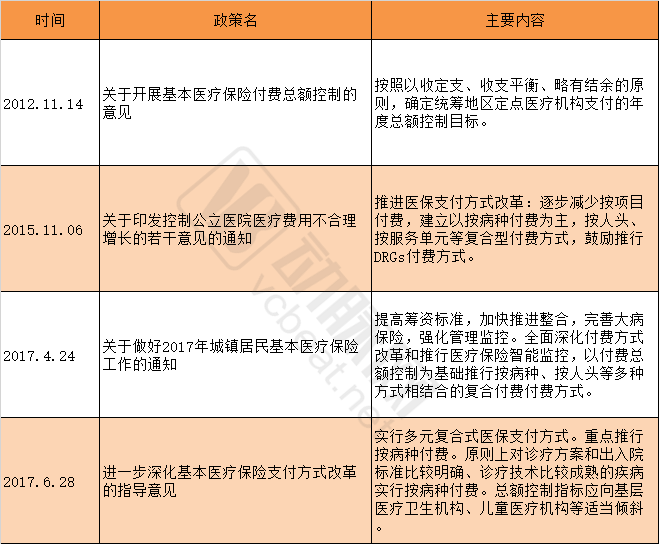

The “medical insurance cap” he mentioned refers to the global budget control for medical insurance, which was first introduced in the 2012 document *Opinions on Implementing Global Budget Control for Basic Medical Insurance Payments* issued by the Ministry of Human Resources and Social Security. The document stated that “the principle of determining expenditures based on revenues, maintaining a balance between revenues and expenditures, and achieving a slight surplus should be followed.”Determine the annual global budget cap for payments to designated medical institutions within the pooling area.

In terms of specific implementation, there are two common approaches to global budget control: one is the “direct allocation method,” which decomposes the overall medical insurance fund budget for a given pooling area into quotas assigned to each designated medical institution, including primary care facilities; the other is the “point-based method,” which adopts diagnosis-related group (DRG) point-value payment, assigning predetermined points to each disease category based on its treatment complexity and resource consumption. Currently, the direct allocation method is predominantly implemented across China.

According to the aforementioned industry insiders, in the process of implementing tiered diagnosis and treatment, the "medical insurance payment caps" for primary healthcare institutions have not been raised. This has led to a peculiar situation,By September and October each year, primary healthcare institutions are unable to prescribe medications, as their medical insurance quotas are nearly exhausted and drug procurement volumes have declined.

“This is, in essence, a systemic contradiction: the medical insurance reimbursement caps for primary healthcare institutions have not increased in tandem with the rise in patient visits, resulting in significant lag. This creates considerable uncertainty for pharmaceutical companies strategizing their entry into the primary care market, as the overall market size remains limited; consequently, they must carefully evaluate multiple factors when making investment decisions.”

On a physician community platform, this scenario has also sparked discussion. A primary care physician stated that his grassroots hospital had exhausted its annual medical insurance budget quota within the first three quarters, leaving it under immense pressure for the remaining months of the year.

“Medical insurance is a key payer in healthcare. Without reimbursement, residents are less likely to seek care at primary medical institutions, and previously established patient relationships may be lost.”

Another noteworthy point is that the reimbursement rate at primary healthcare institutions is higher than that at tiered hospitals. This means that under the “patient diversion” effect of the tiered diagnosis and treatment system, primary healthcare institutions deplete their medical insurance quotas more rapidly, and the constraints imposed by medical insurance will intensify as the tiered diagnosis and treatment system is further implemented.

Recent Policies on Medical Insurance Cost Control

Certainly, regulatory authorities have also taken note of this situation and are making concerted efforts to address it. For instance, the “Guiding Opinions on Further Deepening the Reform of Basic Medical Insurance Payment Methods,” issued by the General Office of the State Council in June 2017, pointed out that (medical insurance) “The total expenditure control targets should be appropriately tilted toward primary healthcare institutions, pediatric medical institutions, and similar facilities.”. Meanwhile, regions with the necessary conditions should actively explore integrating the point-based method with global budget management and diagnosis-related group (DRG) payment systems, gradually replacing institution-specific global budget caps with regional (or scope-defined) global controls on medical insurance funds. This will undoubtedly play a significant role in alleviating the reimbursement pressure on primary healthcare institutions, indicating a larger market share for the grassroots pharmaceutical and medical sector.

Furthermore, in the current primary healthcare market, it is more difficult for traditional Chinese medicine (TCM) to expand its market share than Western medicine. Primary care physicians rely heavily on clinical guidelines during treatment; however, many of these guidelines are dominated by Western pharmaceuticals, with fewer proprietary Chinese medicines included. In light of medication safety and standardized diagnosis and treatment, many physicians are reluctant to prescribe unfamiliar drugs.

“Of course, it should be noted that there are certain differences in indications between traditional Chinese medicine (TCM) proprietary medicines and Western drugs. TCM proprietary medicines have a broader range of indications, which is also a factor considered when clinical guidelines include them.” He stated that greater investment should be made in scientific research on TCM proprietary medicines, adhering to the principles of evidence-based medicine and relying on clinical data.

Meanwhile, significant restrictions remain on medication use at the primary care level. For instance, many provinces and municipalities require that drug procurement by primary healthcare institutions comply with the National Essential Medicines List (NEML), with mandated proportions typically ranging between 70% and 80%. This leaves little room for flexibility, making it challenging for manufacturers whose products are not included in the NEML to penetrate the primary care market.

Multiple Players Positioning to Capture Market Share

It benefits from the tiered diagnosis and treatment system, yet faces constraints from medical insurance cost containment, tender-based price negotiations, and the National Essential Medicines List. The grassroots pharmaceutical market is actually “The Game Between Interests and Standardization”。

“A series of policies in the essential medicine market will effectively lead to a reshuffling of product portfolios. In the future, only drugs with proven therapeutic efficacy and established clinical pathways will stand out. Product quality is paramount, while marketing plays a secondary role; marketing is merely a tool.”

Of course, as a supplementary approach, pharmaceutical companies have continuously innovated their grassroots marketing strategies by integrating them with popular internet products and platforms such as physician communities and clinical decision-support tools. A typical example of this trend is digital marketing.

The concept of digital marketing in the pharmaceutical industry refers to pharmaceutical companies establishing direct connections with frontline physicians and patients, either through self-built platforms or in collaboration with third-party platforms, to achieve marketing objectives.

Currently, major pharmaceutical companies primarily leverage digital tools to serve two key groups: physicians and patients. From the perspective of serving physicians, these tools mainly supplement the traditional pharmaceutical sales representative visit model. By capitalizing on their cost-effectiveness and diversity, digital tools help establish more effective information communication platforms between pharmaceutical companies and physicians. Additionally, pharmaceutical companies can utilize digital tools to aggregate professional knowledge and resources, thereby building centers of academic excellence.

In addition to fostering better interactions with physicians, another objective of digital marketing is to serve patients. For instance, leveraging internet-based tools to manage patient adherence after a physician has prescribed medication holds significant value for doctors, patients, and pharmaceutical companies alike.

Currently, pharmaceutical companies such as AstraZeneca, Pfizer, Sanofi, and Novo Nordisk are all exploring digital marketing, partnering with platforms including DXY, WeDoctor, and Xingshulin.

Besides pharmaceutical companies, pharmaceutical commerce enterprises and social logistics providers are also gearing up in the grassroots market.

Under the “Two-Invoice System,” small pharmaceutical distributors face pressure of being phased out and have begun to actively expand into grassroots markets., leveraging its advantage in penetrating the grassroots level to undertake the “dirty” and “arduous” tasks that large enterprises are unwilling to perform, thereby finding its own positioning amidst the policy-driven reshaping of the industry landscape.

Additionally,As the state relaxes qualification approval for third-party pharmaceutical logistics enterprises, a number of social logistics companies are accelerating their entry into the pharmaceutical logistics sector.For instance, China Post’s subsidiaries have launched distribution services for essential medicines in regions such as Fuzhou, Putian, Sanming, and Quanzhou. Meanwhile, companies like SF Express and JD.com have established pharmaceutical logistics platforms to integrate industry resources, making high-profile entries into the pharmaceutical logistics sector. The “last mile” of drug delivery to primary healthcare markets is particularly competitive.

Overall, under policy guidance, primary healthcare is poised to seize significant historical opportunities. From the “dual-track” system featuring parallel public and private sectors, to a surge in patient visits, and its evolving role as the “gatekeeper” of residents’ health, the rapid development of primary healthcare institutions is creating expanded business opportunities for pharmaceutical companies, pharmaceutical commerce enterprises, and third-party service providers. The value of primary healthcare is gaining increasing recognition.