Primary Healthcare in China: Policy-Driven Growth, Over RMB 3.6 Billion in Financing, and High Potential in Family Doctor Contracts and Third-Party Services – 2017 Year-End Review

Niccolò Machiavelli, a scholar of Roman history, once said, “There is no precedent for reform.” The same holds true for reforms in primary healthcare.

Since January 2017, with the introduction of policy mandates such as “accelerating the development of tiered diagnosis and treatment” and “achieving a family doctor contract service coverage rate of over 30%,” we have witnessed the gradual resolution of longstanding issues in primary healthcare, including inadequate fiscal support policies and public distrust in general practitioners. The “inverted pyramid” pattern of healthcare-seeking behavior is expected to be broken.

For primary healthcare, which is fraught with challenges, progress has been made through cautious exploration. However, every area in need of reform signifies greater business opportunities; it is a path strewn with both thorns and flowers.

The primary healthcare institutions referred to here arePrimary Healthcare: The Most Fundamental Level of the Healthcare System. It comprises township health centers, village clinics, private clinics, community health service centers, and community health service stations.

According to the "2016 Health and Family Planning Statistical Yearbook," in 2015, the number of visits to primary healthcare institutions across China reached 4.34 billion, accounting for 56.4% of the total number of medical visits, with an average outpatient cost of 97.7 yuan per visit.

If the proportion of primary care visits to total medical visits reaches 65%, assuming the average cost per outpatient visit remains unchanged at RMB 97.7 (the 2015 level), the annual expenditure for primary care outpatient services will reach RMB 488.7 billion. The figure would be even higher if inpatient costs incurred at primary care institutions are included.

In the grassroots healthcare market, which exceeds RMB 4 trillion, a wide variety of companies have entered the field, centering on scenarios where residents seek medical care at the primary level. Data statistics from VCBeat in February 2017 show that more than 80 companies have already ventured into the grassroots healthcare sector, including portable smart medical hardware, express delivery services for medical test specimens, and private community chain clinics. Among these, the most heavily represented areas are information technology systems, chain clinics, and third-party medical service institutions.

As healthcare reform policies continue to favor primary care institutions, the number of such facilities has been steadily increasing. According to national statistics on medical and health institutions as of the end of June 2017, there were 933,000 primary healthcare institutions across China, including 35,000 community health service centers (stations), 37,000 township health centers, 638,000 village clinics, and 207,000 clinics (infirmary rooms).

Compared with the end of June 2016, the number of community health service centers (stations) and clinics increased, while the number of township health centers and village clinics decreased.

So, what was worth paying attention to in the field of primary healthcare in 2017? What changes occurred?

The state has issued numerous policies for primary healthcare, covering community health service centers, village doctors, traditional Chinese medicine clinics, and family doctors. These entities are positioned to primarily provide basic public health services and basic medical services to residents within the service coverage areas of their respective institutions.

Furthermore, there are policies that indirectly affect primary healthcare. For instance, on January 9, 2017, the State Council issued the Notice on the “13th Five-Year” Plan for Deepening the Reform of the Medical and Healthcare System, which focused on establishing a basic medical and healthcare system suited to China’s national conditions and achieved new breakthroughs in the development of five key systems: tiered diagnosis and treatment, modern hospital management, universal health insurance, drug supply assurance, and comprehensive regulation.

Meanwhile, reforms in related fields will be advanced in a coordinated manner, primarily including: improving and perfecting mechanisms for talent cultivation, utilization, incentive, and evaluation; accelerating the formation of a diversified landscape for healthcare provision; and advancing the development of public health service systems.

The Two Primary Objectives of the “Notice”:

First, by 2017, a relatively systematic policy framework for the basic healthcare system will be fundamentally established. The policy system for tiered diagnosis and treatment will be gradually improved; the construction of modern hospital management systems and comprehensive regulatory systems will be accelerated; the universal medical security system will become more efficient; and policies governing the production, distribution, and use of pharmaceuticals will be further strengthened.

Second, by 2020, establish relatively comprehensive public health service and medical care systems, a relatively sound medical security system, standardized drug supply guarantee and comprehensive regulatory systems, and scientifically grounded management structures and operational mechanisms for healthcare institutions.

This implies that primary healthcare institutions will have the opportunity to access high-quality medical resources. To promote tiered diagnosis and treatment, it is necessary to adjust the allocation of medical resources, devise ways to direct high-quality resources to the primary care level, and enable resource sharing at this level.

Under favorable policy guidance, capital enthusiasm for participating in primary healthcare has reached an unprecedented high.

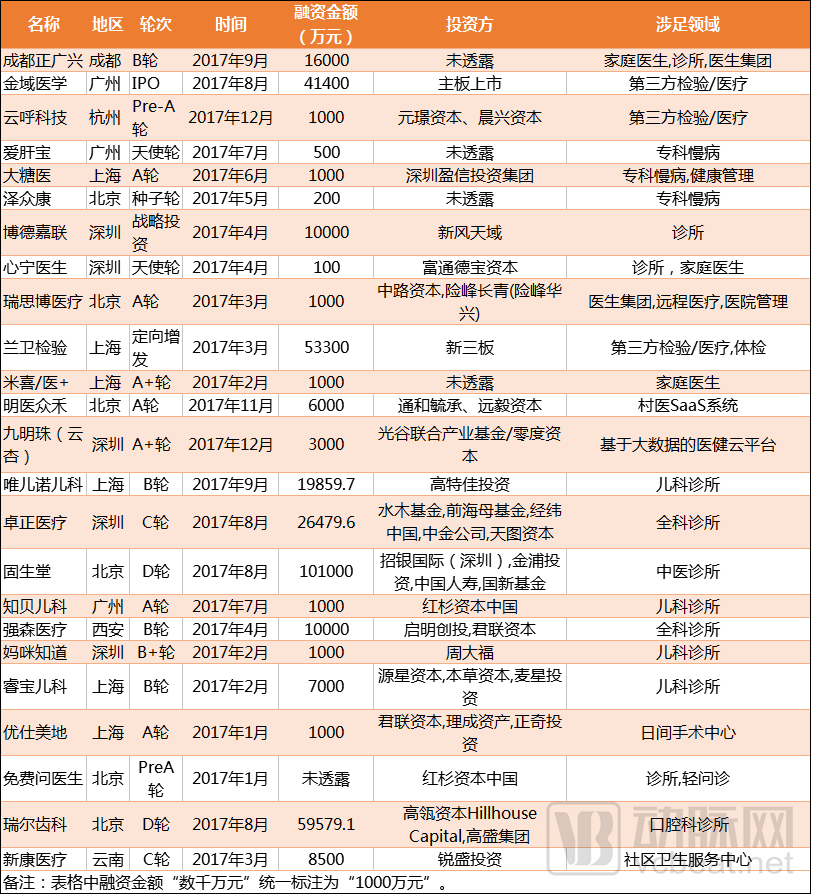

According to incomplete statistics from VCBeat, as of December this year, 24 startups have secured financing, with the total amount exceeding RMB 3.6 billion.

In terms of project financing rounds, there are angel rounds, pre-rounds, Series A, Series B, Series C, New Third Board listings, and IPOs.

Most of them are Series A companies, totaling five: Da Tang Yi, Risebo Medical, Mingyi Zhonghe, Zhibei Pediatrics, and Usmile.

In terms of the sectors involved in the funded enterprises, they include family medicine, chronic disease management, village doctor SaaS systems, community health service centers, and clinics.Among them, 12 clinics have obtainedFinancing, with total funding exceeding RMB 1.3 billion;

There are two listed third-party medical testing companies.KingMed Diagnostics and Lanwei Medical Laboratory;

Three companies are engaged in the informatization of primary healthcare;

Seven enterprises focus on family doctor contract services and chronic disease management centered around community health service centers, while one operates a day surgery center.

"Among the entire list of financings, the largest single round was secured by Gushengtang, a chain of traditional Chinese medicine clinics."

In August 2017, Gushengtang obtainedRMB 1.01 billion Series D Financing(510 million in equity + 500 million in bonds), jointly invested by central state-owned enterprises and domestic financial giants, with its business covering multiple fields such as traditional Chinese medicine (TCM) healthcare, TCM education, and TCM promotion.

Why Has Clinic Project Financing Been So Impressive This Year?

Clinic Project Secures Funding in 2017The period from January to September saw the most financing concentrated in April, August, and September.

This is because on February 28, the National Health and Family Planning Commission issued “Order No. 12 of the National Health and Family Planning Commission of the People’s Republic of China,” which promulgated the Decision of the National Health and Family Planning Commission on Amending the Detailed Rules for the Implementation of the Regulations on the Administration of Medical Institutions (hereinafter referred to as the “Detailed Rules”), effective April 1, 2017.

One provision relaxes the eligibility criteria for applicants seeking to establish medical institutions, permitting currently employed medical personnel to do so. The clause stating that “medical personnel who are currently employed by medical institutions, have resigned due to illness, or are on unpaid leave shall not apply to establish medical institutions” has been deleted.

Following the revisions, the "Implementation Rules" regarding the eligibility of applicants for establishing medical institutions will focus primarily on medical quality and safety, emphasizing the review of applicants’ operational conditions and qualifications. This approach is conducive to fully leveraging physicians’ professional technical expertise and stimulating their enthusiasm for independent entrepreneurial ventures.

Conducive to promoting private investment and accelerating the development of privately run healthcare institutions;

It is conducive to further improving the healthcare service system, promoting the formation of a diversified pattern of medical service provision, and better meeting the public’s diverse healthcare needs.

This change means that incumbent medical personnel can apply to establish medical institutions. The state has finally “loosened restrictions” on applications by practicing physicians to set up medical facilities, while also encouraging doctors to start their own businesses and leverage their professional expertise.

As public hospitals gradually transition to a filing-based staffing system, medical professionals are regaining their status as free agents. With the national promotion of multi-site practice, the model of working at a hospital while operating a private clinic is just around the corner.

On April 26, the National Health and Family Planning Commission and the State Administration of Traditional Chinese Medicine jointly promulgated the “Guiding Opinions of the State Council on Accelerating the Advancement of ‘Internet + Government Services’” (hereinafter referred to as the “Opinions”).

The goal isBy June 2018, all provinces had established local electronic registration systems that were interconnected with the national electronic registration system, thereby achieving electronic management of the registration of medical institutions, physicians, and nurses.

By 2020, fully implement electronic registration management.Basically completed the issuance and use of electronic licenses, achieving the goals of convenient and efficient administrative approval services, dynamic and timely interim and ex-post supervision, and universal access to medical resource information services.

The promulgation of this policy will shorten the processing time for practicing licenses for medical institutions, physicians, and nurses; continuously deepen supply-side structural reforms in the healthcare service sector; ensure the solid implementation of initiatives to improve healthcare services; accelerate the formation of a diversified landscape for healthcare provision; and sustainably increase the supply of healthcare resources, thereby continuously unlocking their potential.

Subsequently, on May 4, Premier Li Keqiang presided over an executive meeting of the State Council to determine measures supporting privately run medical institutions and health tourism, thereby meeting the public’s multi-level and diversified health needs.

Concurrently stated: No restrictions shall be imposed on private medical institutions that meet planning conditions and access qualifications, under any pretext! Furthermore, a one-stop acceptance mechanism, parallel approval, and online approval will be implemented for private medical institutions. Chain medical institutions may have their industrial and commercial registration handled uniformly by their headquarters—the era of “one certificate only” has finally arrived. This is also in line with the intensive policy measures introduced in recent years.The highest-level policy among those encouraging private capital to establish medical institutions.

The meeting held that targeting the multi-level and diversified health needs of the public, advancing streamlining of administration and delegation of power in the medical sector while strengthening regulation and optimizing services, and vigorously supporting social forces in providing medical services are important measures to deepen healthcare reform, address shortcomings, and improve people's livelihoods.

At the meeting, three measures were proposed to accelerate the development of privately-run healthcare institutions:

First, encourage non-governmental entities to establish general practice clinics and independently operated specialized institutions such as medical laboratories and rehabilitation and nursing care facilities. Promote cross-provincial and cross-municipal chain operations of capable privately run traditional Chinese medicine (TCM) clinics and outpatient departments. Attract overseas investors to engage in joint ventures and cooperation to establish high-quality medical institutions.

Second, implement a one-stop acceptance system, parallel approval, and online approval for private medical institutions.Chain-operated medical institutions may have their business registration handled centrally by the headquarters.No restrictions shall be imposed, under any circumstances, on privately operated medical institutions that meet planning requirements and access qualifications.The establishment of individual clinics is not subject to planning and layout restrictions.Implement regional registration for physicians to promote orderly mobility and multi-site practice;

Third, efforts should focus on improving the quality of services provided by private medical institutions, while exploring inclusive and effective approaches to prudential regulation.Severely crack down on illegal and irregular activities such as opening practices by renting or lending practice licenses, contracting out departments, false advertising, and illegal medical practice.

The meeting proposed promoting the deep integration of health, tourism, and elderly care, guiding social capital investment, encouraging the development of high-end medical services, traditional Chinese medicine (TCM) healthcare, rehabilitation and convalescence, and leisure and wellness products, and accelerating the cultivation and development of the health tourism market.

It was also clarified at the meeting that"General practice clinics, independently established medical laboratories, and specialized institutions for rehabilitation and nursing care" are key areas for private capital investment., and proposed "promoting the cross-provincial and cross-municipal chain operations of capable private TCM clinics and outpatient departments."

It is worth noting that the meeting proposed focusing on improving the quality of services provided by private medical institutions. Under the premise of relaxing market access requirements, it called for “exploring inclusive and effective prudential regulatory approaches” to address “long-standing issues” such as operating with rented practice licenses or certificates, contracting out clinical departments, false advertising, and illegal medical practice. The meeting also reaffirmed the implementation of one-stop acceptance, parallel approval, and online approval processes for private medical institutions.

These three policies significantly boosted the development of clinics. At that time, Johnson Medical had just secured RMB 100 million in financing; for Johnson Medical, which was expanding its footprint across China, this policy support came at a most opportune moment.

Its CEO, He Haiyang, told VCBeat:“We are a chain enterprise and encountered two issues during our expansion. First, previously, general practitioner (GP) family doctor responsibility-based chain clinics were ineligible for registration; with the current recognition of ‘general practice,’ such operations are now fully compliant and lawful. Second, it was not possible to obtain unified business registration approval through the headquarters; each new clinic required separate business registration procedures, posing significant challenges in financial auditing, tax compliance, and management. Now, group-level unified business registration is available, greatly facilitating operations and reducing barriers caused by cross-management.””

At that time, Zhao Qiang, CEO of Zhibei Pediatrics, was deeply troubled as he was applying for a second clinic.He had previously opened a pediatric clinic at Aoyuan City World in Zhongcun Street, Panyu District, Guangzhou. Opening another new clinic locally would require reapplying for the license and resubmitting physicians’ practice qualification certificates, making the approval process overly complex. Without unified management during the application process, efficiency is significantly reduced.“With the policy now in place, I hope local governments will implement it soon to streamline many procedures. Once centralized processing is established at headquarters, the efficiency of clinic approval will improve significantly.” The clinic is currently planning to open in January.

Driven by these factors, private clinics have demonstrated even greater vitality. Relevant policies have become clearer and more open; capital has grown more rational; and the industry has entered a phase of restructuring.

Looking ahead, several trends regarding clinics are becoming increasingly evident:

1. Chain or Group Operations. From a market perspective, independent clinics are increasingly losing their voice. The development of standardized chain operations is the only viable path for primary care. In the future, several large healthcare groups will inevitably emerge in this sector, gradually growing into the industry's leading enterprises;

2. Greater convenience. In the primary healthcare sector, convenience and speed are irreplaceable values; there is no ultimate convenience, only greater convenience. All innovations aimed at enhancing convenience, whether online or offline, deserve encouragement.

3. Payment Reform and Insurization. Driven by heightened health awareness and consumption upgrades, medical payment models are bound to undergo transformation. The traditional volume-based, price-oriented fee-for-service model will inevitably evolve into a value-oriented, bundled payment system under accountable care, with the integration of primary healthcare and insurance emerging as a major trend.

4. Shared clinics are emerging. The term “shared clinics” here refers to multi-site practice platforms for physicians, such as the one built by Xingren Doctor. According to Martin, CEO of Xingren Doctor,After opening its first clinic in Shenyang, it successively recruited partners across 33 major cities throughout China, aiming to replicate the Almond Clinic model.

Since September 2016,Xingren Doctor has launched a recruitment campaign for Xingren Clinic partners across core cities in China,Establishment of a Co-Construction Fund for Outpatient Clinic Development; Physicians Contributed to the Co-Construction Pool, with Monthly Contributions Surpassing RMB 40 Million in the Launch Month. Doctors Actively Supported the Development of Xingren Outpatient Clinics and Showed Strong Interest in the Innovative “Outpatient Clinic Partner” Model.

The vigorous development of clinics has also driven the growth of enterprises that serve them, such asCompanies in the fields of healthcare informatization, village doctor SaaS systems, and telemedicine have also performed exceptionally well.

December 15, 2017,Jiumingzhu & Yunxing HealthAnnounces the Successful Completion of a RMB 30 Million Series A+ Financing Round。Jiumingzhu is a seasoned health and medical informatics enterprise in China, with “Yunxing Health” serving as its smart healthcare platform.

Jiumingzhu was founded and established by the Sanjiu Enterprise Group in 1999., it has evolved from a Health Information Technology (HIT) company into a technology-driven enterprise comprehensively expanding into the “Internet + Healthcare” sector, and has now become a well-known domestic provider of an integrated cloud service platform for internet-based healthcare tailored to small, micro, and medium-sized medical institutions.

Since merely focusing on the informatization of primary healthcare institutions cannot truly address their multidimensional needs, establishing a new ecosystem within small, micro, and medium-sized medical institutions is essential to provide tangible support for the development of private hospitals and primary healthcare facilities.

Yunxing has two product lines: one is Cloud HIS, which serves both clinics and provides “group management” for physician groups; the other is Cloud Referral.

Taking Cloud HIS as an example, it alleviates users’ apprehension toward information technology software by offering an intuitive interface that facilitates a smooth transition from paper-based to electronic prescribing. Meanwhile, Yunxing has successively launched WeChat Mini Programs such as Yunxing Scan and Yunxing Mini Clinic, addressing the need for mobile workflows among healthcare professionals.

Value-added services such as cloud-based prescription review and electronic signatures, built on the cloud HIS system, address users’ needs for rational drug use and paperless office operations, respectively.In just six months, Yunxing has accumulated 5,000 users.

Yunxing’s flagship product is Yun Referral. Built upon its cloud-based Hospital Information System (HIS), it provides professional solutions for bidirectional diagnosis and treatment among hospitals, small and micro medical institutions, and physicians. This system effectively enhances the efficiency of information management in the referral process for medical institutions at all levels and primary care physicians, thereby tangibly increasing patient visits to hospitals.

Unlike traditional paper-based referrals, “Cloud Referral” centers on the “tiered diagnosis and treatment” model. Leveraging the Hospital Information System (HIS) and the Free Doctor APP as intermediaries, it effectively integrates resources among large hospitals, private specialized hospitals, primary healthcare institutions, and patients according to the varying needs of medical institutions. This approach addresses resource asymmetries among these four parties and provides an actionable solution for implementing tiered diagnosis and treatment as well as two-way referrals.

Since its establishment, the platform has established cooperation intentions with more than 30 hospitals across China and has signed contracts with ten medical institutions.

Among them, the cloud referral platform of Guangdong Minsheng Medical Group went online in May 2017, with its monthly referral volume exceeding RMB 1 million by August. The number of “village doctors” served through its Ziyu Doctor APP has reached over 2,400, resulting in significant improvements in both brand awareness and economic benefits.

If the development of Jiumingzhu Yunxing represents a microcosm of the evolution of domestic primary healthcare platforms, then Mingyi Zhonghe’s positioning for the development path of rural clinics is even more specialized.

Due to the vast distances and scattered distribution of rural clinics, the cost of team expansion is prohibitively high. Consequently, few are willing to invest substantial time, effort, human resources, material assets, and financial capital into developing the rural market. As a result, the focus of most grassroots healthcare entrepreneurs currently remains concentrated on urban areas.

In the rural grassroots healthcare market, Mingyi Zhonghe’s development path is worth referencing.

The rural primary healthcare regions selected by its founder, Jiang Qiang, include Shandong, Henan, Hebei, and Guangdong.He conducted thorough research and, based on a comprehensive evaluation of local grassroots population size, density, economic conditions, and other dimensions, ultimately concluded that the optimal grassroots healthcare market for incubating the project must be characterized by a large population and a scarcity of high-quality medical resources.

By precisely targeting this segment, Mingyi Zhonghe has already covered nearly 30,000 clinics. The company aims to capture at least one-third of the market share in this sector in the future, which translates to serving 100,000 clinics.

In 2017, Jiang Qiang accomplished two major milestones: first, he secured RMB 60 million in Series A financing; second, he completed the development of the “Yidebang” Clinic Ecosystem Service Cloud SaaS platform, conducted field research on frontline data, and promoted its business model.

Meanwhile, it has refined the mapping of platform users’ medication purchasing needs and transaction behavior patterns, streamlining processes across drug distributors, manufacturers, GSP-compliant warehousing and logistics providers, clinics, and service-oriented sales representatives within the cloud pharmacy model. Currently, Mingyi Zhonghe has completed its pilot deployment, and partners across various sectors have endorsed its proposed model for restructuring pharmaceutical supply chains in primary healthcare.

Telemedicine Empowers Primary Care: How Heart Doctor International Does It!

On December 8, Jiao Yahui, Deputy Director of the Bureau of Medical Administration and Hospital Management under the National Health and Family Planning Commission, stated at a regular press conference: “To enhance the homogenization and accessibility of healthcare services,”China has extended telemedicine coverage to 13,000 medical institutions and all nationally designated poverty-stricken counties. In 2017, more than 60 million teleconsultations and remote diagnostic services—including pathology, imaging, and electrocardiography—were conducted, and prescription extensions were implemented for eligible patients with chronic diseases within medical consortia.

Among the enterprises assisting hospitals in establishing telemedicine systems, Xinyi International’s development is particularly representative. By empowering healthcare institutions across three dimensions—resources, technology, and services—Xinyi International enables medical consortia to achieve seamless vertical integration and effective two-way patient referrals, thereby unlocking the full value of these collaborative networks.

Resources—Dual-engine drive by expert and disciplinary resources. XinYi has built China’s largest multi-tier medical collaboration platform, integrating high-quality medical resources from over 50 national-level hospitals, more than 160 regional leading hospitals, dozens of specialty-leading hospitals, and overseas partner hospitals. It provides medical collaboration services to nearly 4,000 county-level public hospitals and township health centers. Meanwhile, it offers targeted support to grassroots institutions in co-developing branded specialties, helping them attract and retain patients.

Technology—Integration Services for IT and Clinical Technologies. Leveraging extensive customer research and business practice, Mindray International has proposed a product service system for tiered diagnosis and treatment known as the “Five Platforms, One Center.” Additionally, it supports informatization at the primary care level through technologies such as cloud imaging, rapid intraoperative remote pathology services, and regional imaging center services, thereby promoting interoperability of patient data. Meanwhile, it strengthens the practical skills of primary care physicians through multidisciplinary, clinically oriented practical training.

Services—Diversified Operational Service Models for Comprehensive Efficiency Enhancement. Leveraging its operational and disciplinary service advantages, Xinyi helps primary healthcare institutions effectively utilize remote education to achieve a closed loop of academic capability, enhance county-level medical capacity through comprehensive discipline planning, develop multi-modal remote services online, and advance grassroots talent capacity building through offline advanced training. By vertically integrating these efforts, Xinyi elevates the service capabilities of primary healthcare, enabling hospitals within medical consortia not only to be “connected” but also to be “activated.”

Taking the areas served by XinYi International in Shaanxi Province as an example, it has built and operated more than 20 regional and specialized medical consortium projects centered around major hospitals such as Shaanxi Provincial Tumor Hospital, Xi’an Honghui Hospital, Ankang Traditional Chinese Medicine Hospital, and Xijing Hospital. This has established a “comprehensive and far-reaching” telemedicine collaboration network in Shaanxi Province, effectively alleviating the difficulty of accessing medical care for residents in remote areas.

Currently, there are 50 national key counties for poverty alleviation in Shaanxi Province. Winning Health has supported the development of local grassroots healthcare infrastructure, helping over 90% of these key counties achieve coverage by telemedicine service networks.

At the end of 2016, Ankang City in Shaanxi Province included remote consultation services in the reimbursement scope of the New Rural Cooperative Medical Scheme (NRCMS), clearly specifying the pricing and subsidy amounts. With a minimum out-of-pocket cost of RMB 20, patients could access remote consultations provided by tertiary hospitals across China.

Ankang has established a telemedicine service model characterized by “government leadership, hospital implementation, and third-party services,” directly channeling high-quality medical resources from large hospitals to county-level hospitals and township health centers. As of October 30, 2017, the Ankang Mindray International Telemedicine Platform had completed 6,263 remote consultations.

Xinyi International’s initiatives in Guizhou Province also offer valuable lessons. As one of the first provinces designated for national telemedicine policy pilots, Guizhou has comprehensively achieved full coverage of telemedicine services across four tiers: provincial, municipal, county, and township levels. Leveraging this digital infrastructure, the “meridians” facilitating the smooth flow of high-quality medical resources are gradually being unblocked, fostering closer collaboration between large hospitals and primary care institutions, and enabling a growing number of patients to benefit from these advancements.

Guizhou Province has established a telemedicine network covering 199 public hospitals at the provincial, municipal, and county levels, and formed a professional technical team of 5,241 telemedicine specialists. Tertiary Grade A hospitals have adopted measures such as zoned responsibility, paired assistance, and the formation of medical consortia. Since June 2016, Guizhou has conducted over 20,000 remote consultations, a figure 80 times the cumulative total of all previous years.

A large number of patients have been “retained” at the primary care level. Last year, medical institutions at the county level and below provided 135 million outpatient visits and inpatient services, a year-on-year increase of 7.1%. Leveraging telemedicine information systems led by provincial flagship hospitals, more than 150 training sessions were conducted for medical institutions across the province, training over 23,000 participants.

Across China, Medlinker covers a remote collaboration system for medical consortia spanning 31 provinces and over 4,300 hospitals, serving more than 120 medical consortia at various levels and types. By integrating multi-tier high-quality medical resources, advanced information technology, and professional operational services, it helps medical institutions, experts, and physicians at all levels enhance their capacity and efficiency in patient care, promotes the optimized allocation of medical resources, and facilitates the implementation of tiered diagnosis and treatment.

“Transforming the service model of primary healthcare, implementing family doctor contract services, and strengthening the functions of the primary healthcare service network are important tasks in deepening the reform of the medical and health care system, as well as a crucial approach to better safeguarding the health of the people under the new circumstances.” This statement comes from the “Guiding Opinions on Promoting Family Doctor Contract Services” (hereinafter referred to as the “Opinions”), formulated last year by the State Council’s Office of Healthcare Reform, the National Health and Family Planning Commission, the National Development and Reform Commission, the Ministry of Civil Affairs, the Ministry of Finance, the Ministry of Human Resources and Social Security, and the State Administration of Traditional Chinese Medicine. The “Opinions” have been reviewed and approved by the Central Leading Group for Comprehensive Deepening of Reforms.

The primary objective of this Opinion is to launch family doctor contract services in 200 pilot cities for comprehensive public hospital reform by 2016, while encouraging other eligible regions to actively carry out pilot programs. Breakthroughs should be prioritized in areas such as service delivery models, content, payment and fee collection, performance evaluation, and incentive mechanisms. Priority coverage should be given to the elderly, pregnant and postpartum women, children, persons with disabilities, as well as patients with chronic diseases such as hypertension, diabetes, and tuberculosis, and those with severe mental disorders.

By 2017, the coverage rate of family doctor contract services exceeded 30%, and the coverage rate for key populations exceeded 60%.By 2020, efforts will be made to expand contracted services to the entire population, establish long-term and stable contractual service relationships, and basically achieve full coverage of the family doctor contracted service system.

Across China, the implementation of family doctor enrollment varies by region. In some areas, medical staff from community health service centers provide home-based family doctor services; in others, local governments outsource public health services to qualified enterprises through public-private partnership (PPP) models.

At the Xinqiao Central Health Center in Youxian District, Mianyang City, Sichuan Province, medical staff proactively provide door-to-door family doctor services, achieving a contract signing rate of over 90%.Five-member family doctor teams provide each contracted household with a small card printed with the team’s name, phone number, and photo. Residents can contact their family doctors at any time to address health concerns and seek answers to their questions. The teams also regularly disseminate health education materials and facilitate referrals to higher-level hospitals for serious conditions, thereby ensuring that minor illnesses are treated within the township and major diseases are managed within the county.

Xinqiao Town, Youxian District, is a national “Grade A Class I” rural central health center. It covers an area of 13 mu, with a total building area of 4,500 square meters. The facility has more than 20 clinical and medical technology departments, 60 hospital beds, a service radius of nearly 15 kilometers, directly serving a population of 21,000 and reaching a broader population of nearly 70,000. It handles over 50,000 outpatient visits and more than 5,000 inpatient admissions annually, with total annual business revenue approaching RMB 8 million.

In advancing the development of the “PPP” model for family doctor contracting, Xinkang Medical’s approach exhibits distinct characteristics.Their CEO, Yang Sa, believes that their approach targets two key areas: first, how to attract patients; and second, how to retain high-quality physicians, thereby integrating the two.

Xinkang Medical has established extensive connections with patients by centering its approach on accompanying them throughout their entire life cycle. Substantial value can only be realized through comprehensive data collection, continuous interaction, and ongoing optimization.

Through four years of exploration, Xinkang has established standards for the construction, service processes, management, performance evaluation, operations, and informatization of primary community healthcare institutions. The entire process is assessable, supervisable, and replicable, paving the way for chain-based operations and group-level management.

In 2017, Xinkang began piloting a model of comprehensive co-management and co-construction of grassroots healthcare systems with local governments on a county-by-county basis. Within a single county jurisdiction, there are nearly one hundred community health service centers and community health stations combined. This structure positions Xinkang for more rapid expansion of its clinic network in the future. Yang Sa expects the number of Xinkang Community Hospitals to surpass 1,000 within two years.

As the service capabilities of primary healthcare institutions improve, a chain reaction will be triggered. The increase in patient visits, growth in end-user demand for pharmaceuticals, and expanded service volume for third-party medical testing platforms will drive performance improvements in the pharmaceutical and medical testing industries.

In terms of scale, the total revenue of domestic third-party medical testing institutions in China was approximately RMB 10 billion in 2015, accounting for about 5% of the medical testing market. According to forecasts by Qianzhan Industry Research Institute, the third-party medical testing services market is expected to maintain a growth rate of 35%-40% from 2014 to 2020, capturing around 7%-9% of the medical testing market share. By 2020, the theoretical market size of third-party medical testing is projected to exceed RMB 50 billion.

According to business registration data, as of November 22, 2017, a total of 1,555 new companies related to medical laboratory testing and nine pathology diagnosis companies were established throughout the year. Dian Diagnostics, KingMed Diagnostics, Zhongke Runda, and Wuhan Landing all newly established multiple medical laboratory testing centers.

In the third-party medical testing platform services sector, two companies have gone public this year: KingMed Diagnostics and Lanwei Inspection. As of the market close on December 14, KingMed Diagnostics had a market capitalization of RMB 13.6 billion, while Lanwei Inspection’s market capitalization stood at RMB 2.982 billion.

KingMed Diagnostics and Lanwei Clinical Laboratory have been highly sought after by investors, primarily for two reasons: first, both companies boast strong fundamentals, ample cash flow, and a certain market share in their respective niche segments; second, investors are optimistic about their growth potential, given the significant promise of their sectors and substantial room for expansion.

In addition, startups like KuaiYiJian are also drawing significant attention. By integrating mobile internet with professional pharmaceutical cold-chain logistics, KuaiYiJian provides medical testing capabilities to rural grassroots clinics. It enters the primary healthcare market through the underserved niche of routine blood tests, establishing efficient sales channels and logistics networks, and bridging upstream high-quality medical resources with village-level healthcare markets through both online and offline pathways.

As of December 2017, KuaiYiJian had signed contracts with over 10,000 clinics, processed more than 2 million test items, and generated nearly RMB 50 million in revenue.

The rapid development of primary healthcare institutions has also driven growth in sectors such as POCT and rehabilitation equipment, primary care informatics, third-party services, telemedicine, and pharmaceutical e-commerce.

According to the "Report on the Development Prospects and Investment Forecast of China's Rehabilitation Medical Industry" by Qianzhan Industry Research Institute, the market size of China's rehabilitation medical industry reached approximately RMB 27 billion in 2016.

As China continues to intensify reforms in healthcare services, accompanied by the improvement of the three-tier rehabilitation medical system and the further implementation of health insurance policies related to rehabilitation care, the rehabilitation medical industry is poised for explosive growth. In 2017, the sector is expected to enter a rapid expansion phase. It is projected that by 2020, the market size of China’s rehabilitation medical industry will exceed RMB 70 billion, with a compound annual growth rate (CAGR) of no less than 20%, thereby creating another trillion-yuan market.

One approach for companies entering the primary healthcare sector is to align with healthcare reform policies. Although many enterprises have already established a presence across various segments, effectively occupying these market niches, they must still identify viable monetization pathways; otherwise, they risk remaining merely a fleeting trend.

Regarding profitability, Jin Qilin, Director of the Shanghai Yangpu District Health Bureau, pointed out in a media interview that primary public health products are not profitable. “However, there must be profitable areas, namely leveraging public health services to attract this group of people to purchase another profitable product. For example, drugs currently have considerable profit margins; private hospitals even have greater room for drug discounts than public hospitals. But as reforms deepen further and drug prices are suppressed, this source of profit will no longer be available.” Jin Qilin stated that operating in this manner would be unsustainable in the long run.

So, apart from pharmaceuticals, what are the other revenue models? We have drawn reference from the model of ViAid.

“In the design of our group’s overall model, the future revenue ratio is approximately 1:2:3. Traditional medical diagnosis and treatment revenue accounts for only about 15%, value-added or light medical services contribute 35%, and 50% of revenue comes from the extension of medical products, such as medical finance and insurance,” Gao Ping, General Manager of Wei Ai Kang Medical Group, told VCBeat. “The purpose of designing this model is to reduce reliance on revenue from medical diagnosis and treatment, ensuring government satisfaction, tangible benefits for the public, and profitability for the entire project, making it implementable and sustainable.”

Weiai Kang’s business model is divided into two segments: online and offline. The online segment, centered on family physicians, not only provides community hospitals with a steady and controllable patient flow but also operates as an independent revenue-generating unit. Through family physicians, it delivers front-end health management services to consumers, as well as back-end rehabilitation and wellness care within the broader health sector.

Wei Ai Kang positions its family doctor contracting service as the core customer acquisition system and a key component of proactive health management services. Building upon this foundation and centered on the medical and healthcare needs of the “five-member family,” Wei Ai Kang has developed a series of specialized family health protection products. These initiatives not only increase interaction frequency and enhance patient satisfaction but also achieve innovative outcomes in pre-emptive marketing, patient traffic diversion to hospital campuses, and self-generated revenue.

Offline operations primarily focus on community hospitals, aiming to create the “Home Inn” of the healthcare industry. This is achieved by leveraging brand strength and standardized management systems to replicate projects through models such as entrusted operation, third-party construction with self-operation, and investment and M&A.

“Since our first campus began its soft launch in June this year, daily outpatient visits have averaged around 120. While there is room for growth, exceeding 200 patient visits per day would compromise the service quality of a single-site campus and negatively impact patient experience. Therefore, the triage and referral role of our family doctors becomes particularly crucial at this stage; they strategically stagger patient flows to the campus based on the urgency and severity of each case,” said Gao Ping.

WeAiKang aspires to become the Alibaba of the healthcare sector, onboarding numerous B-side enterprises and devising differentiated profit-sharing structures tailored to the unique characteristics of each industry.Open the Weiai Kang platform to high-quality enterprises capable of providing services, deliver enhanced value experiences to the public, and enable individuals to access comprehensive healthcare services across their entire lifecycle on the platform.

From this perspective, the market potential in every segment of primary healthcare is immense. We look forward to seeing more enterprises enter the primary healthcare sector next year and establish their own viable monetization pathways.