CVS Health to Acquire Aetna in $69 Billion Deal, Creating Integrated Healthcare Powerhouse

The U.S. healthcare industry has seen its largest deal of the year.

VCBeat (WeChat ID: vcbeat) has learned that U.S. pharmaceutical retail giant CVS recently announced it will acquire health insurer Aetna for $69 billion. This transaction is the largest in the history of the U.S. pharmaceutical retail industry and the largest deal in the global pharmaceutical sector so far this year.

Aetna is a leading commercial insurer in the United States, providing property and casualty insurance, life insurance, health insurance, and other insurance services to governments, businesses, and individuals. It has more than 23 million members in the health insurance sector, with health insurance premium income of $13.469 billion in 2016.

CVS’s acquisition of Aetna has further intensified the oligopolistic landscape in the U.S. pharmaceutical retail and health insurance industries.

How America’s Largest Pharmaceutical Retailer Was Built

The U.S. pharmaceutical retail industry is currently characterized by a duopoly. While CVS trails Walgreens in store count and retail scale, its total revenue exceeds that of Walgreens.

According to CVS’s 2016 annual report, the company operates more than 9,700 pharmacies nationwide in the United States, of which 1,100 are equipped with “MinuteClinic” facilities, and its Pharmacy Benefit Management (PBM) business serves nearly 90 million members.

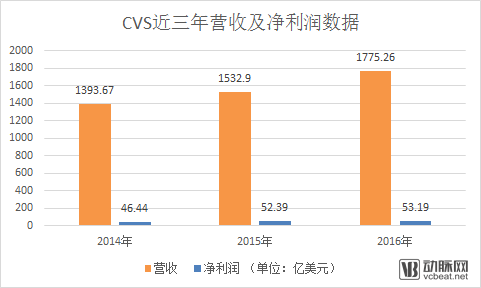

In 2016, CVS reported revenue of $177.526 billion, a 15.8% increase from 2015; net income amounted to $5.319 billion, representing a 1.5% rise compared to 2015.

CVS originated in the 1960s. Its initial business was not pharmaceutical retail; it gradually shifted its focus to pharmaceutical retail after two or three years of operating in the health products sector. By 1970, CVS had opened 100 stores across New England and the Northeastern United States. By 1985, its annual sales surpassed $1 billion.

Since the 1970s, CVS has embarked on cross-industry mergers and acquisitions, initiating its nationwide expansion across China: In 1972, CVS acquired Clinton Drug Discount Store; in 1977, it acquired the Brothers pharmacy chain in New Jersey; in 1990, CVS acquired People’s Pharmacy...

While expanding its scale through a series of acquisitions, CVS also focused on horizontal mergers and acquisitions to broaden its business scope. In 2006, CVS acquired MinuteClinic, establishing a new business model featuring small clinics within pharmacies. In 2007, CVS merged with Caremark, a pharmacy benefit manager (PBM), to strengthen its PBM operations.

CVS’s most recent major acquisition occurred in 2015, when it spent $1.9 billion to acquire more than 1,600 pharmacies and 80 clinics from U.S. retailer Target, thereby becoming the largest pharmaceutical retailer and pharmacy services provider in the United States.

CVS’s revenue is derived from two core business segments: retail pharmacy and pharmaceutical services. The latter refers to comprehensive pharmacy benefit management (PBM) services, including mail-order pharmacy, specialty pharmacy, and infusion services provided by CVS Caremark, as well as health management programs, prescription management, and claims processing. The primary clients for this segment include employers, insurance companies, labor unions, government employee organizations, health plans, managed Medicaid programs, and other sponsors of health benefit plans or individuals.

CVS Caremark manages prescription dispensing for over 75 million members, facilitated through five mail-order pharmacies, specialty pharmacies, long-term care pharmacies, and a nationwide network of more than 68,000 retail pharmacies in China (including 41,000 chain pharmacies and 27,000 independent pharmacies).

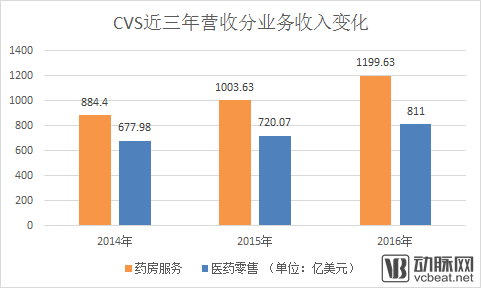

As the data shows, CVS’s pharmacy services revenue exceeded that of its pharmaceutical retail business. In 2016, pharmacy services revenue approached $120 billion, while pharmaceutical retail business revenue stood at $81.1 billion.

Why Did CVS Favor Aetna?

Aetna is one of the world’s oldest health insurance companies. In 1850, it established an Annuity department and launched its life insurance business; in 1853, this department was spun off to form Aetna Life Insurance Company. In the United States, the company ranks among the leaders in medical, dental, prescription drug, life, and group disability insurance.

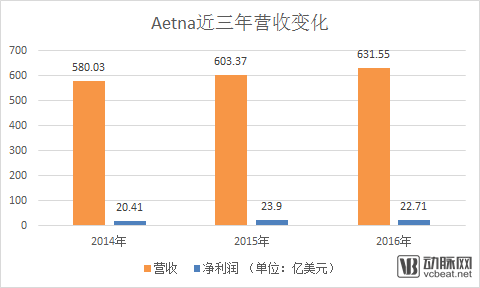

According to Aetna’s 2016 annual report, its revenue for 2016 was $63.155 billion, a 5% increase from 2015; net income was $2.271 billion, a 5% decrease from the previous year. The same report indicated that Aetna had 23.11 million health insurance members.

CVS’s acquisition of Aetna is driven by multiple factors. One key reason is their long-standing partnership; the two companies signed a contract in 2010 under which CVS provided pharmacy benefit management (PBM) services to Aetna, although this agreement was set to expire at the end of 2019. Earlier this year, executives from both CVS and Aetna stated that they were working on mutually beneficial modifications to the contract.

Second, the U.S. e-commerce giant announced earlier this year its entry into the pharmaceutical retail sector, sending shockwaves through the industry. According to reports, Amazon has obtained regulatory licenses for pharmaceutical wholesale in 12 U.S. states and will fully launch its pharmaceutical distribution operations.

Third, competition between Walgreens and CVS remains intense, with CVS seeking to expand its operational scale to widen the gap with Walgreens. In fact, as CVS continued its acquisition spree, Walgreens also seized the opportunity to expand both domestically in the United States and overseas. Its expansion efforts included merging with Alliance Boots, Europe’s largest healthcare products distributor, and pursuing the acquisition of Rite Aid, the third-largest pharmacy retailer in the United States.

Just before CVS confirmed its acquisition of Aetna, Walgreens Boots Alliance (formed by the merger of Walgreens and Alliance Boots) announced a strategic investment of $2.767 billion in China National Pharmaceutical Group’s retail pharmacy chain, Guoda Drugstore, acquiring a 40% equity stake.

Fourth, the management teams of CVS and Aetna believed that their merger would generate business synergies, reduce operational costs, and enhance the performance of both parties. According to foreign media reports, the two companies had previously engaged in “secret negotiations for several months.”

Prior to the news of its commitment to CVS, Aetna had been involved in multiple “rumored deals.” Last year, after being blocked by regulators, Aetna was forced to abandon its $37 billion acquisition agreement with rival Humana, which argued that the deal would harm competition and consumers.

Under the agreement reached between CVS and Aetna, CVS will pay Aetna shareholders $207 per share to acquire their shares, comprising $145 in cash and $62 in CVS stock. Including Aetna’s debt, the total value of the transaction amounts to $77 billion.

Following CVS’s acquisition of Aetna, a comprehensive healthcare service ecosystem encompassing “PBM + pharmaceutical retail + health insurance + medical services” will be established. Aetna’s 23 million members will serve as a “traffic source” for CVS, while Aetna will benefit from more refined pharmacy benefit management and cost-containment measures provided by CVS. More importantly, the combination of the two entities will form a powerful bargaining alliance, strengthening their negotiating leverage against pharmaceutical companies and healthcare providers, thereby helping to further reduce operational costs.

The two companies stated that cost synergies would reach $750 million in the second full fiscal year following the completion of the transaction (if the transaction is completed in the second half of 2018, the second full fiscal year will be 2020). They expect this to increase adjusted earnings per share by 1% to 5%.

Morgan Stanley’s analysts also believe that the transaction will “diversify CVS’s profit sources and lay the foundation for a new healthcare retail model.”

Of course, this transaction will also undergo an antitrust review by the U.S. Department of Commerce to ensure that the alliance does not harm the interests of the industry and consumers.

Insight: China’s Pharmaceutical Retail Sector Should Accelerate Consolidation

As a long-standing benchmark for China’s pharmaceutical retail industry, CVS’s continuous mergers and acquisitions have offered valuable insights to the sector, including horizontal expansion to diversify business models and vertical expansion to achieve economies of scale.

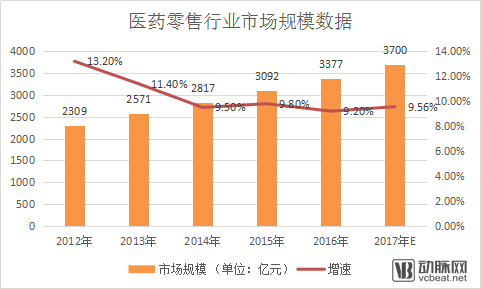

Currently, the issue of insufficient scale in China’s pharmaceutical retail industry persists. According to data from the Ministry of Commerce, in 2016, the top 100 pharmaceutical retail enterprises by sales operated a total of 54,300 stores, accounting for 12.2% of the national store count; their combined sales revenue reached RMB 107 billion, representing 29.1% of the total retail market; and the market share of the top three retail enterprises was merely 6.7%. In contrast, the top three enterprises in the United States accounted for more than 80% of the total market share. This indicates that there is still significant room for improvement in China’s chain store penetration rate and market concentration.

It is worth noting that the density of retail pharmacies in China is already very high. Based on 2016 data, with a population of 1.375 billion and 446,000 pharmacies, the ratio was approximately 3,082 people per pharmacy, whereas the “saturation standard” in developed countries is 2,500 people per pharmacy. This implies that, assuming no significant changes in population size, opening new stores will not be the primary mode of entry into the pharmaceutical retail sector in the future.

Recent policies have facilitated the increase in industry concentration. For instance, the “13th Five-Year Plan for the Development of the Pharmaceutical Circulation Industry (2016–2020)” stipulated that the chain pharmacy rate should exceed 50% by 2020. Meanwhile, increasingly stringent regulatory and industrial environments have made independent pharmacies and small-scale chains more willing to align with industry giants, with franchising or being acquired emerging as highly cost-effective solutions. These factors will collectively contribute to higher industry concentration.

From an industry practice perspective, there are currently four listed companies in the pharmaceutical retail sector: Yixintang, Laobaixing, Yifeng Pharmacy, and Dashenlin. The revenue and profit levels of Yixintang, Laobaixing, and Dashenlin are relatively close, with Yifeng Pharmacy ranking slightly behind. In terms of expansion strategies, all adopt a combination of organic and inorganic growth, though each has its own primary focus and regional differences.

Yixintang has deeply cultivated the Yunnan market while focusing on Sichuan and Chongqing; Laobaixing is prioritizing expansion in the Central-South region; Yifeng excels in refined management; and Dashenlin, having recently gone public, will leverage its IPO advantages to intensify its market presence. In the future, these four listed companies will continue to dominate their respective regions, leading to a fragmented landscape across China.

In addition to listed companies, industrial capital and non-listed enterprises have also been active in investment and M&A. Gansu Zhongyou, Shaanxi Huakang, and Quanyi Health have all undergone large-scale regional expansion in recent years and are poised to emerge as regional industry leaders.

Overall, pharmaceutical retail is a low-frequency, high-unit-price industry. Benefiting from the development of the broader health industry and opportunities arising from healthcare system reforms, its market size continues to expand. Driven by policy and capital, the pharmaceutical retail sector is actively addressing issues such as fragmentation, disorder, low market concentration, and limited professionalism through mergers and acquisitions. The industry is currently undergoing a period of rapid transformation, presenting significant opportunities.