Private Hospitals in China: Obstetrics Dominates Specialty Segment, Tier-3 Hospitals Account for Only 2%

Foreword

As an important component of China’s healthcare service system, private hospitals have played a significant role in actively promoting the advancement of the country’s healthcare sector. Compared with public hospitals, private hospitals feature more flexible management systems and operational mechanisms. The government implements market-adjusted pricing for private hospitals, allowing them to set prices independently based on market supply and demand as well as service costs, thereby facilitating greater initiative in market competition. In 2017, the “Opinions of the General Office of the State Council on Supporting Social Forces in Providing Diversified Medical Services” highlighted implementation measures such as encouraging the development of general practice services and accelerating the growth of specialized medical services, fully expanding multi-level and diversified medical services, thus providing direction and safeguards for the development of private hospitals.

This paper aims to analyze the development status and challenges of private hospitals by collecting and examining data from recent years on their scale, healthcare workforce, and operational performance, thereby proposing targeted recommendations to promote their healthy and sustainable development.

Indicator Explanation:

① Hospitals: including general hospitals, traditional Chinese medicine (TCM) hospitals, integrated TCM and Western medicine hospitals, ethnic medicine hospitals, specialized hospitals, and various types of nursing homes.

② Private hospitals: Hospitals whose economic ownership type is other than state-owned or collective, including joint ventures, shareholding cooperatives, privately owned, and those with investment from Hong Kong, Macao, Taiwan, or foreign countries.

③ Public Hospitals: Refers to hospitals with state-owned and collective economic types.

In recent years, privately run medical institutions have become a highlight and key focus of China’s healthcare system reform, with the development of private hospitals serving as a crucial measure to implement this initiative. To achieve the Healthy China strategic goal of “shared construction and universal health,” it is essential to accelerate the development of private hospitals, formulate supporting policies, encourage active participation of social capital in their establishment, and address the current lag in their growth. However, due to their late start and weak foundation, private hospitals are characterized by numerous but not strong entities during their development process.

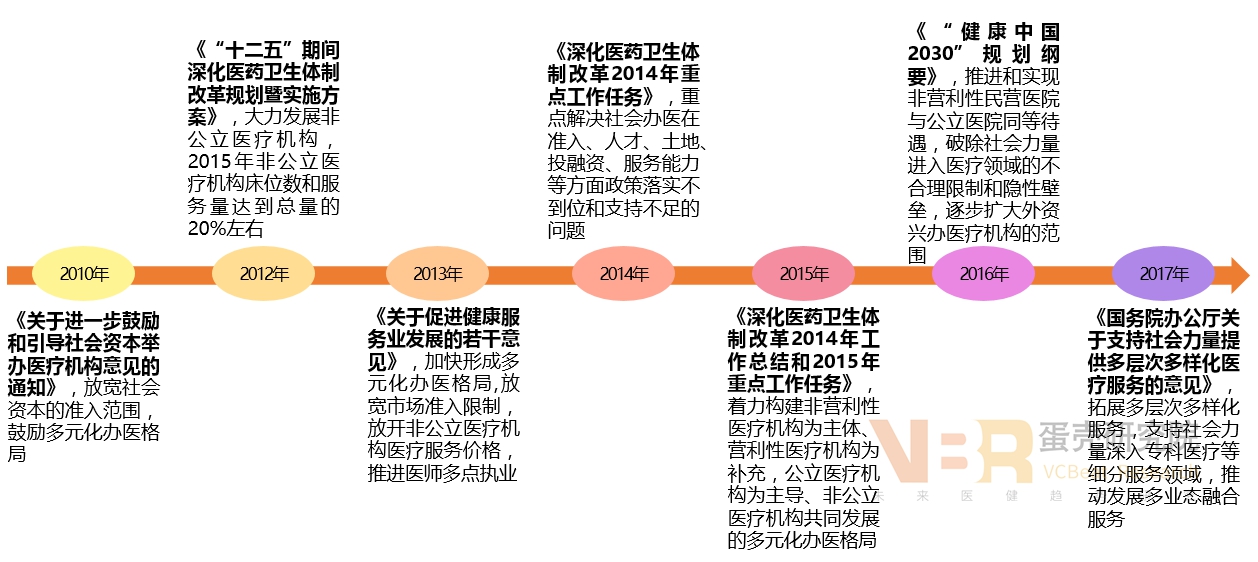

Policy Support: Increasingly Detailed Year by Year with Enhanced Operability

Key Policies for Private Hospitals, 2010–2017

Government support policies for non-public medical institutions have become increasingly operational, extending from strategic planning to specific guidance, thereby propelling the development of private hospitals in China from a phase of slow progress into one of rapid growth. In particular, the promulgation of the Outline of the “Healthy China 2030” Planning Program in 2016 ended the differential treatment between private and public hospitals, removed barriers to social capital participation in healthcare delivery, and accelerated investments by private and foreign capital in the establishment of private hospitals. As a result, the number of private hospitals reached 16,432, exceeding the number of public hospitals by 3,724.

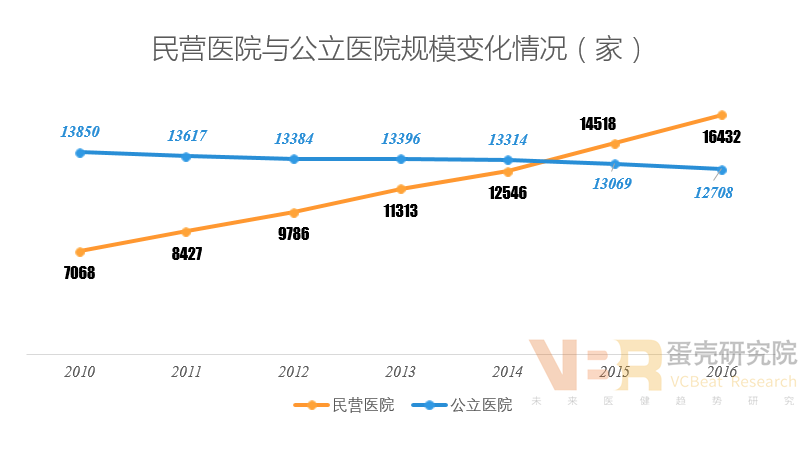

Private Hospitals Enter a Period of Rapid Development, Characterized by Quantity Over Strength

Data source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat

The number of private hospitals is increasing year by year, while the number of public hospitals is decreasing year by year.In 2015, the number of private hospitals surpassed that of public hospitals. This indicates that social capital has actively participated in the development of private hospitals as policy barriers have been gradually lowered.

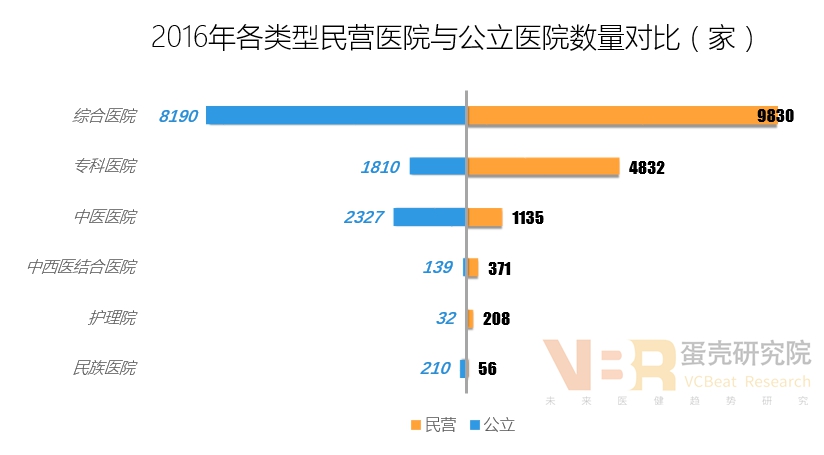

Data Source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat Institute

Private institutions hold a clear advantage in the sectors of general hospitals, specialized hospitals, integrated traditional Chinese and Western medicine hospitals, and nursing homes; whereas public institutions dominate the sectors of traditional Chinese medicine hospitals and ethnic medicine hospitals.

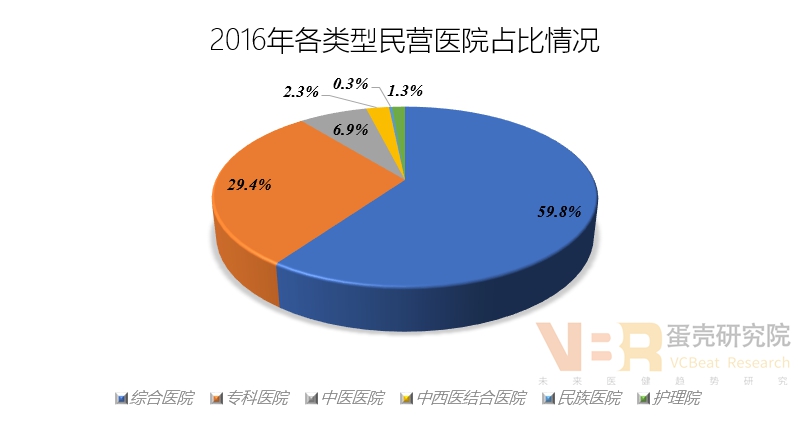

Data source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat Institute

Comprehensive Hospitals Account for the Highest Proportion, as general hospitals offer a wide range of medical services and have diverse revenue sources.

Ethnic Hospitals Account for the Lowest Proportion, as hospitals of this type are primarily located in ethnic minority areas, which are relatively few in China.

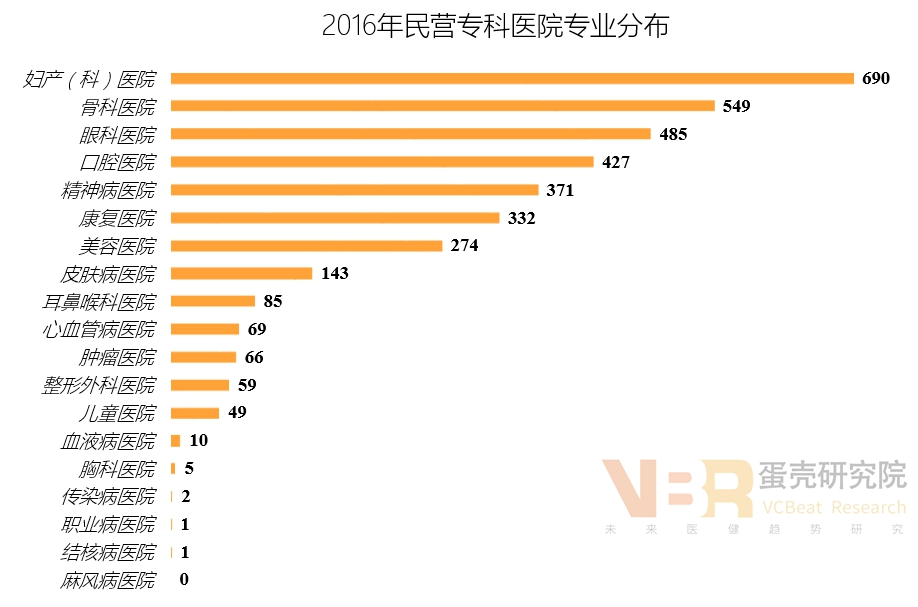

Data source: China Health and Family Planning Statistical Yearbook (2017), compiled by VCBeat

Maternity and Obstetrics Hospitals Are the Most Numerous, as consumption upgrades, residents are willing to spend more to ensure the safety of both mothers and infants.

Low Penetration Rate of Children's Hospitals, with the gradual implementation of the universal two-child policy, the shortage of pediatricians and the lack of specialized pediatric hospitals will become increasingly prominent. In the future, children's hospitals hold immense development potential.

Few hospitals specialize in infectious diseases, leprosy, and the like., this type of hospital is subject to strict policy regulation, serves a specialized patient population, and entails high operational risk.

Data Source: China Health and Family Planning Statistical Yearbook (2017), compiled by VCBeat.

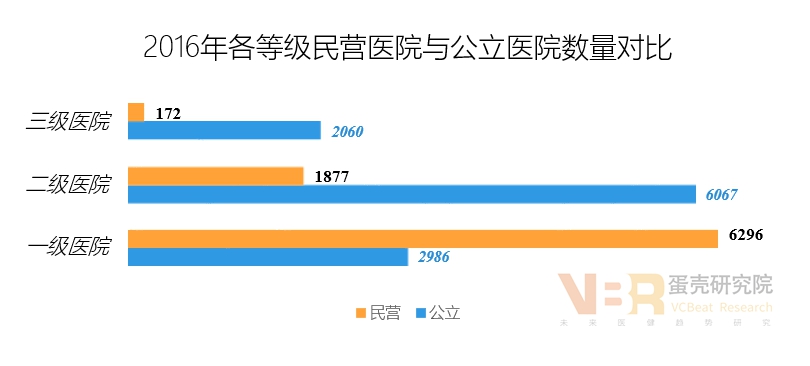

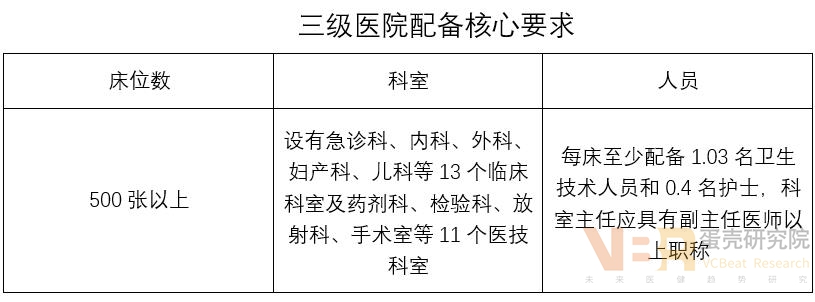

Data Source: "Measures for the Graded Management of Hospitals"

The number of private hospitals at the primary level is the highest and exceeds that of public hospitals at the same level; however, there are relatively few private hospitals at the secondary and tertiary levels compared to publicThere are significant disparities among hospitals.Among private hospitals, tertiary hospitals account for only 2%.This indicates that private hospitals lag behind public hospitals in terms of bed capacity, departmental configuration, and staffing. To achieve substantial growth, private hospitals must significantly enhance their comprehensive service capabilities.

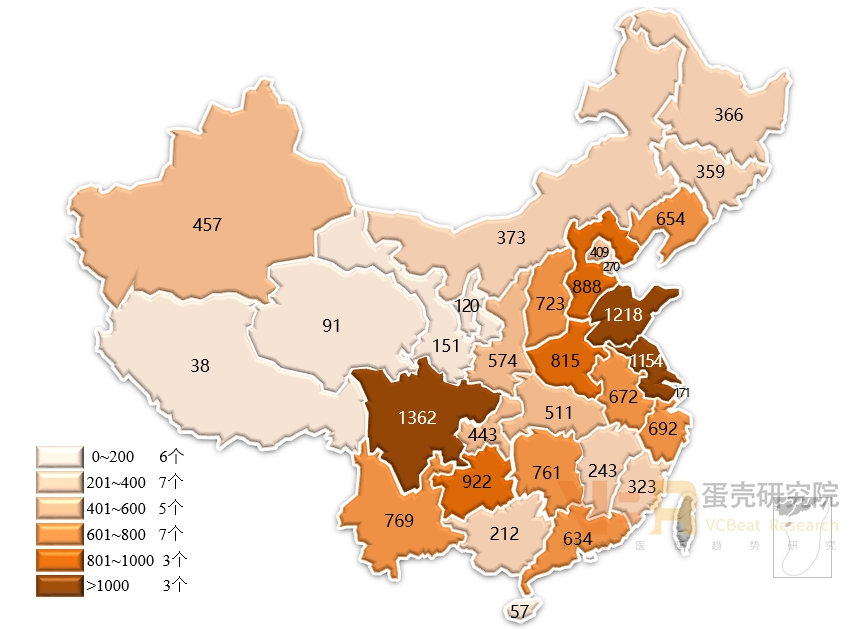

Number of Private Hospitals by Province (Municipality) in 2016

Data Source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat

Only 3 Provinces Exceed 1,000: Sichuan, Shandong, and Jiangsu each have more than 1,000 private hospitals; these provinces have large populations and substantial demand.

Coastal provinces demonstrate a significant numerical advantage: The high level of economic development in coastal regions has created a favorable economic environment for the establishment of private hospitals.

Low Number of Provinces in Northwest China: The sparse population and lagging economic development in Northwest China have constrained the growth of private hospitals.

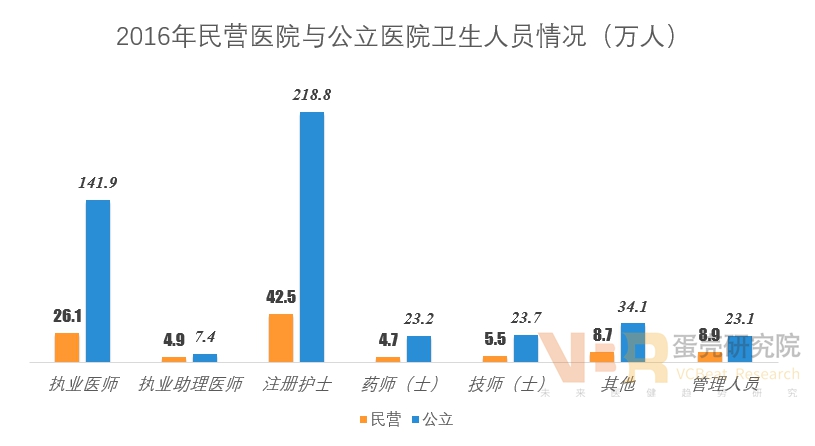

Service Capacity Continues to Strengthen, While Talent Becomes a Development Bottleneck

Data Source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat.

There is a significant gap in healthcare personnel between private and public hospitals., particularly due to the scarcity of licensed physicians and registered nurses, the shortage of medical professionals has become a hindrance to development.

Data source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat Research Institute

Data source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat Institute

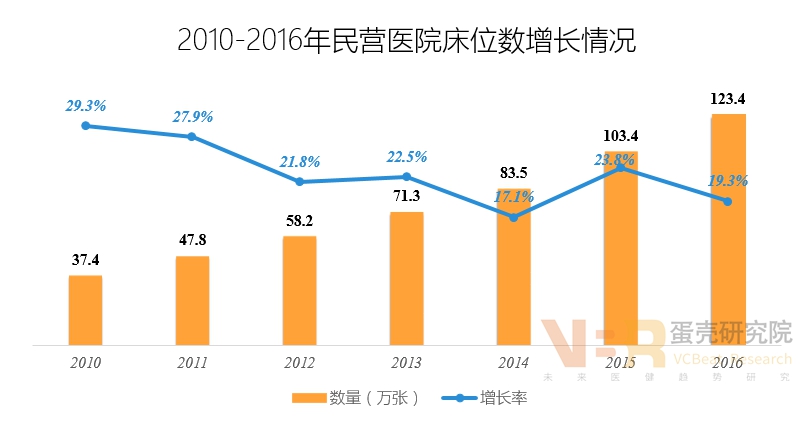

Total Volume Increasing with a High Growth Rate: The number of beds in private hospitals continues to grow, with an annual growth rate of approximately 20% in recent years, indicating an increase in the number of private hospitals as well as an expansion in their scale.

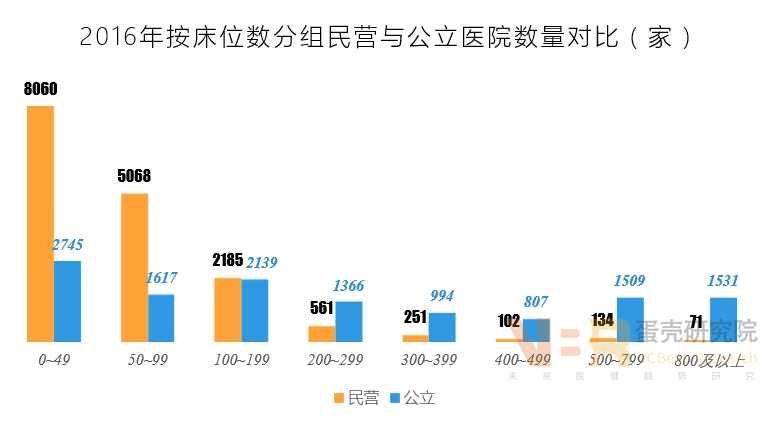

The greater the number of beds, the larger the gap.: Most private hospitals have fewer than 200 beds, and the numerical advantage of public hospitals becomes more pronounced as bed count increases, indicating that private hospitals generally have weaker patient intake capacity.

Data source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat Research Institute

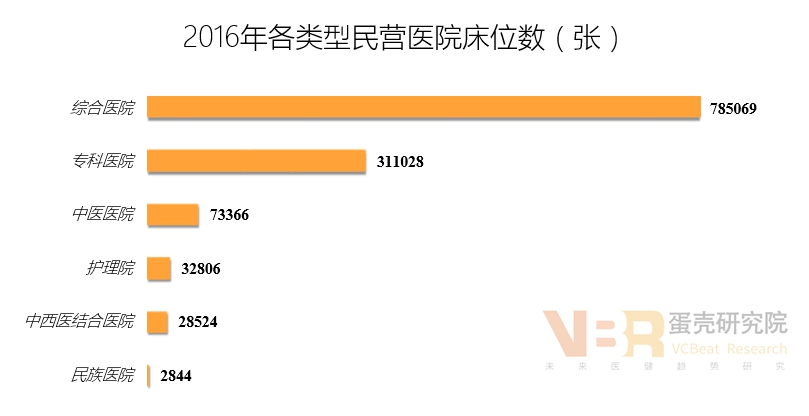

Comprehensive private hospitals have the largest number of beds, far exceeding those of other types of hospitals., primarily because general hospitals receive the highest patient volume and have substantial demand for beds.

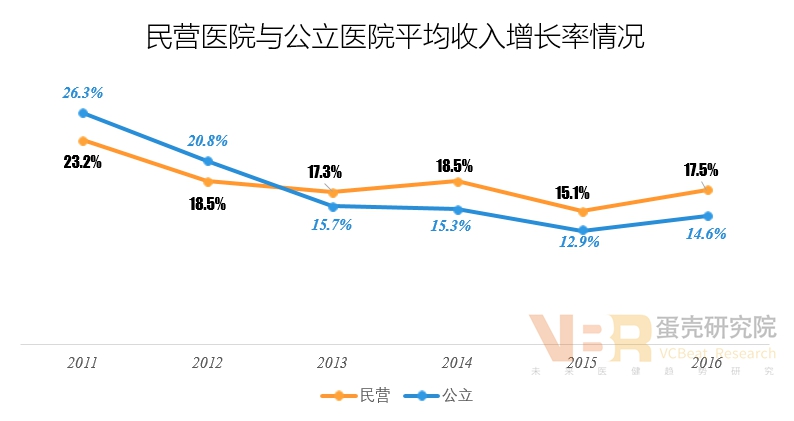

Income Levels Gradually Rise, While Operational Risks Warrant Attention

Data source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat

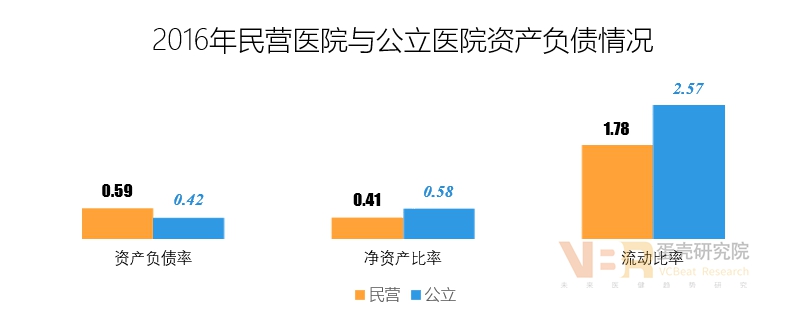

Compared with public hospitals, private hospitals have a higher asset-liability ratio, resulting in weaker debt-servicing capacity.This is primarily because private hospitals receive far less fiscal funding support than public hospitals, necessitating large-scale bank loans and social borrowing to meet their financing needs. This has led to high debt levels in private hospitals, underscoring the need for strengthened fiscal support and optimized financing structures to mitigate debt risks.

Data source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat

Data source: China Health and Family Planning Statistical Yearbook (2017), compiled by VCBeat

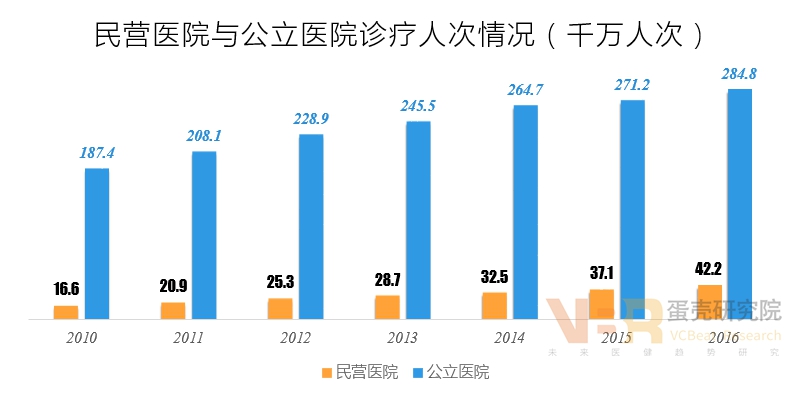

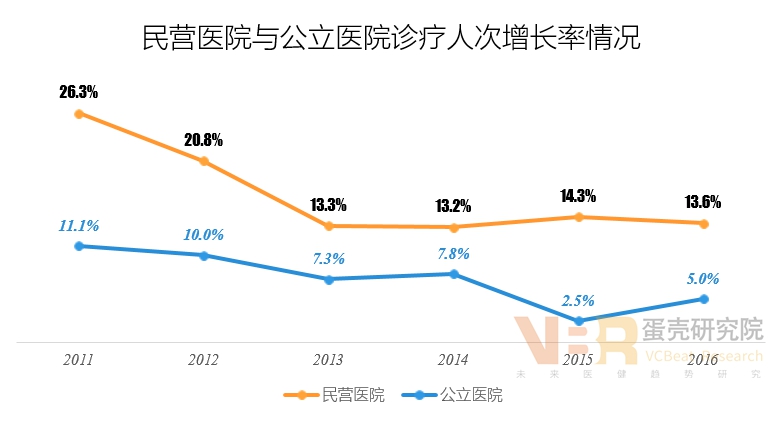

In terms of patient visits, there is a significant gap compared to public hospitals, but the growth rate is higher than that of public hospitals.Due to the absolute advantages of public hospitals in terms of bed capacity, medical personnel, and equipment, their overall strength in medical services is robust, enabling them to accommodate more patients; consequently, the number of patient visits far exceeds that of private hospitals. However, with the development of private hospitals, whose numbers have surpassed those of public hospitals and whose coverage has become more extensive, coupled with continuous improvements in medical talent and facilities/equipment, the number of patient visits in private hospitals has grown rapidly, with a growth rate significantly higher than that of public hospitals.

Data Source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat Institute

Data source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat

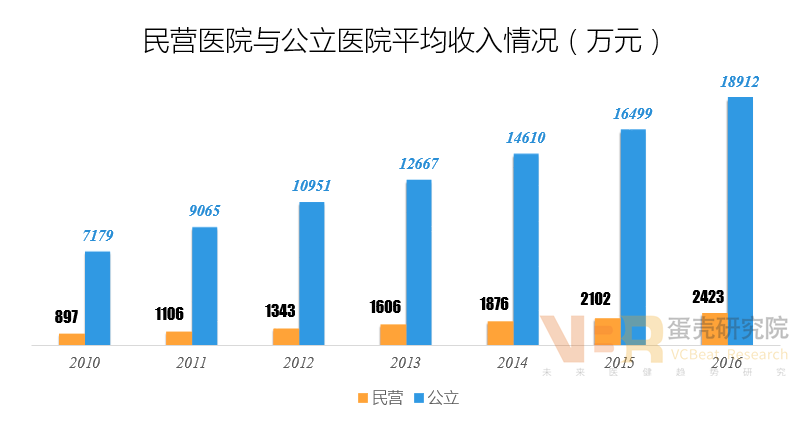

There is a gap in average income between private hospitals and public hospitals.Hospital revenue is directly proportional to the number of patient visits. Public hospitals handle an average of 8.7 times as many patient visits as private hospitals, resulting in a substantial revenue gap between the two. However, since 2013, the average revenue growth rate of private hospitals has exceeded that of public hospitals, primarily driven by a faster increase in patient visits at private hospitals, which has accelerated their revenue growth.

Data Source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat

Data Source: China Health and Family Planning Statistical Yearbook (2017Year), compiled by VCBeat

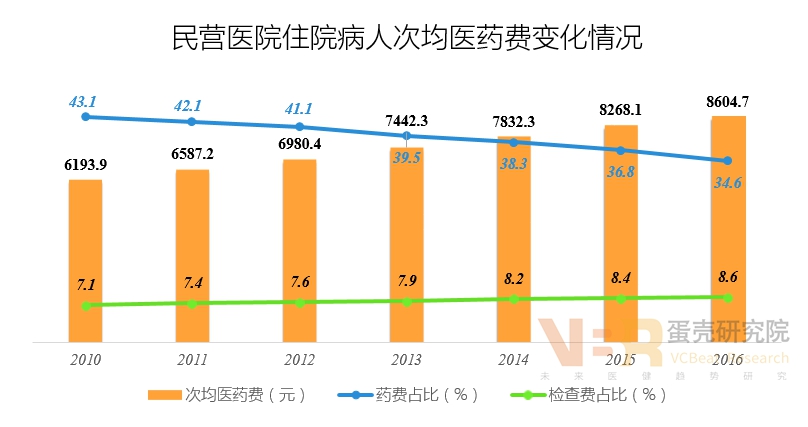

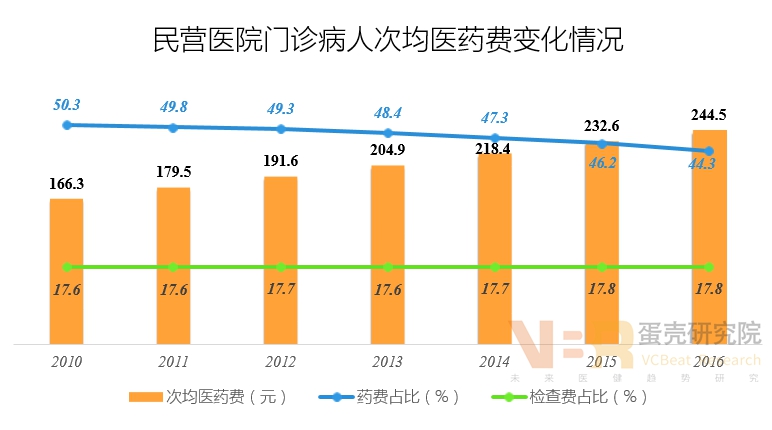

The Average Medical Cost Per Patient Has Increased Year by Year: indicating that household medical consumption expenditure is continuously expanding, and the number of patients seeking medical care is also increasing.

The proportion of drug costs has decreased year by year, while the proportion of examination fees has increased year by year.: This is primarily attributable to the growing demand for medical and healthcare services among residents, who are willing to allocate more funds toward diagnostic examinations to maintain their health.

The proportion of examination fees is lower than that of medication fees.: This indicates that hospital revenue is primarily derived from pharmaceuticals, which has become a major driver of persistently high drug prices. In the future, greater efforts should be made to control the proportion of pharmaceutical revenue.

Overall, private hospitals in China have achieved rapid development in recent years, with continuously rising revenue levels and gradually enhanced service capabilities. However, significant gaps remain compared to public hospitals in terms of infrastructure and service quality. The key factors constraining the development of private hospitals are talent acquisition and medical quality. In the future, private hospitals need to integrate resources, innovate their operational models, and strengthen collaborations with medical schools to overcome bottlenecks and achieve healthy, sustainable growth.