Is Healthcare Cloud Failing Due to Local Incompatibility or Misdiagnosed Core Issues?

In November 2017, the authoritative research firm IDC released its findings on the market share of China’s public cloud IaaS sector for the first half of 2017. The data showed that Alibaba Cloud’s market share increased by 7 percentage points from the end of 2016, reaching 47.6%. During the same period, the market shares of the second- through fifth-ranked cloud service providers were 9.6%, 6.5%, 6%, and 5.5%, respectively.

Among them, Alibaba Cloud generated $500 million in IaaS revenue in the first half of 2017, capturing a 47.6% share of the Chinese market; Tencent Cloud ranked second with revenue of approximately $100 million and a 9.6% market share; Kingsoft Cloud came in third with $68.39 million in revenue and a 6.5% share; China Telecom placed fourth with $62.54 million in revenue and a 6% share; and UCloud ranked fifth with $57.74 million in revenue and a 5.5% market share.

Zhang Shu, an analyst at IDC China, stated, "The rapid development of China's public cloud IaaS market is driven by the swift upgrading of infrastructure by enterprise users amid the wave of digital transformation. As provincial and municipal governments roll out specific action plans in response to national cloud computing policies and advance related demonstration projects, the demonstrative and catalytic effects across industries will propel the rapid growth of China's public cloud market."

The booming public cloud market has naturally drawn VCBeat’s attention to the healthcare sector. In China, uneven distribution of medical resources, low utilization rates, and the existence of resource silos persist. The only way to optimize resource allocation is to achieve “regional collaborative healthcare,” for which cloud infrastructure serves as the most fundamental informational safeguard. From both technical and business perspectives, the cloud service model is the optimal platform for supporting the healthcare informatization industry.

Compared with the high-profile presence of cloud computing in government affairs and industry, medical cloud seems somewhat subdued. Is this due to systemic or mechanistic issues? What are the underlying reasons? With these questions in mind, VCBeat conducted an investigative analysis.

Background of the Emergence of Medical Cloud

From an architectural perspective, cloud computing comprises three service models: IaaS (Infrastructure as a Service), PaaS (Platform as a Service), and SaaS (Software as a Service).

IaaS primarily leverages virtualization technology to provide customers with infrastructure resources, including computing, storage, and networking. PaaS typically offers developers a development platform and provides the corresponding runtime environment for SaaS-layer applications, specifically encompassing services such as data analytics, speech recognition, image recognition, and advertising. SaaS is mainly oriented toward end-user groups, including enterprises and individuals, delivering specific software application services.

Cloud computing is akin to a utility service, such as gas, water, or electricity. It often remains distant from the actual needs of specific industries, thus requiring collaboration with IT companies across various sectors to achieve practical implementation. The United States boasts a more advanced information technology industry than China, particularly in vertical sectors such as industrial manufacturing and healthcare. The IT capabilities of industry giants like Microsoft, IBM, Adobe, and Oracle are by no means inferior to those of cloud computing enterprises such as Amazon, Google, and Facebook.

When public cloud IaaS and PaaS replace traditional IT architectures, IT companies assume the role of SaaS-level service developers; if both parties possess strong technical capabilities, seamless integration can be achieved.

China’s government cloud, healthcare cloud, and other industry-specific clouds are essentially solution-oriented offerings and do not operate at the same level as public clouds. Due to the limited capabilities of domestic vertical-industry IT firms, they lack the capacity to interface directly with cloud computing providers. Consequently, cloud computing companies have been compelled to launch corresponding industry cloud products to accommodate IT solutions across various sectors.

It is precisely due to differences in foundational IT capabilities that industry clouds (government clouds, industrial clouds, and healthcare clouds) became the biggest watershed between China’s and the United States’ cloud computing industries in 2017.

From the perspective of the hierarchy of healthcare information technology, cloud computing resides at the lowest level, namely the infrastructure layer; big data sits above it, with artificial intelligence positioned at the top. Therefore, structurally, cloud computing companies provide big data services, upon which artificial intelligence is built.

According to Sun Weifeng, Industry Director at the Mobile Information Research Center, partnering with healthcare system integrators is the primary strategy for deploying medical clouds. Integration with hospitals’ underlying systems represents the most critical and challenging link in the entire hospital cloud industry chain. Both internet companies and traditional IT vendors have made collaboration with healthcare system integrators their entry point, leveraging this partnership as a breakthrough to penetrate the underlying systems of the healthcare industry.

In this context, competition in the cloud computing market for the healthcare industry will ultimately evolve into a contest of strength and resources among these partners. Competition in the healthcare cloud market will no longer be characterized by individual efforts, but rather by team-based strategies formed through alliances.

The Biggest Challenges of Medical Cloud: Poor Informatization Level and Difficulties in Ensuring Data Security

From a purely demand-side perspective, and setting aside patient privacy concerns, healthcare and cloud computing are highly compatible. Tiered diagnosis and treatment has been the central theme of China’s national healthcare policy in recent years. This approach is driving a shift from hospital-centric business models to regionally centralized, intensive care models. Within this system, the focus is transitioning from disease-centered care to health management-centered care. Meanwhile, as healthcare institutions grow in scale, the trend toward platformization places higher demands on technology.

Furthermore, in the broader context of separating pharmaceutical prescribing from dispensing, controlling overall costs has become a core task for hospital administrators. Hospital information systems generally do not require substantial computational power; some hospitals’ needs are limited to website hosting or using cloud services merely as data storage tools. Cloud computing providers can fully leverage this cost perspective to deploy low-cost, high-performance cloud services in hospitals.

However, unlike sectors such as government affairs and industry, the unique characteristics of healthcare have made the implementation of cloud computing fraught with challenges.

Cloud computing companies aim to integrate data from various hospital information systems and store it on cloud platforms, but this initiative faces significant challenges. The prevailing industry consensus is that hospital data is highly sensitive and requires stringent confidentiality, particularly regarding patient privacy. Hospitals impose rigorous requirements on system real-time performance, stability, and the security of medical data.

Article 5 of the Cybersecurity Law of the People's Republic of China clearly stipulates:The State shall take measures to monitor, prevent, and handle cybersecurity risks and threats originating from within and outside the People’s Republic of China, protect critical information infrastructure against attacks, intrusions, interference, and destruction, punish cyber illegal and criminal activities in accordance with the law, and safeguard cyberspace security and order.。

Driven by the imperative to safeguard national medical data, hospital information management departments place significant emphasis on the background of cloud computing providers, adopting a more conservative stance toward cloud products offered by foreign enterprises such as AWS and Microsoft. Consequently, in terms of cloud product selection, companies like Alibaba Cloud, China Telecom Cloud, and Kingsoft Cloud have relatively greater opportunities.

Furthermore, physicians place great importance on medical data, particularly for research purposes, and are generally reluctant to store such information on cloud platforms. Currently, the healthcare content that hospitals migrate to the cloud mainly comprises non-core systems, such as office automation and health examination systems. However, hospitals remain hesitant and conservative about migrating core clinical systems, such as Electronic Medical Records (EMR), Hospital Information Systems (HIS), and Laboratory Information Systems (LIS), to the cloud.

Hospital physicians also face a dilemma: on one hand, they are only willing to upload partially de-identified imaging archive files to the cloud, leveraging private cloud services for storage, intelligent image interpretation, and computer-aided diagnosis; on the other hand, they hope to access data from other hospitals and physicians through public cloud platforms.

Therefore, at present, private clouds and hybrid clouds remain relatively long-term, phased solutions for medical clouds. However, from the perspective of future development, public clouds will become the mainstream. At this stage, however, hybrid clouds offer more promising prospects for implementation.

Given that domestic healthcare informatization initiatives have primarily focused on hospitals at the secondary level and above, primary care institutions generally exhibit weak informatization capabilities. Therefore, the implementation of cloud computing requires a gradual rollout facilitated by the development of medical consortia and family doctor contract platforms.

The Head Effect in Cloud Computing Is Prominent, but Concentration in Medical SaaS Remains Insufficient

In fact, in addition to the internal hospital issues mentioned earlier, the difficulty in implementing cloud computing in the healthcare industry is also attributable to the low level of consolidation within the health informatics sector.

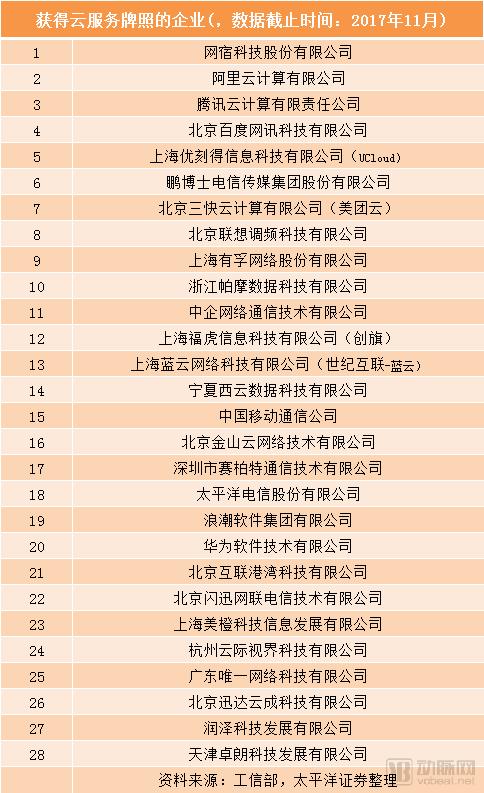

At the “Trusted Cloud” Conference held on July 25, 2017, Zhang Jianhua, Director of the Market Division of the Information and Communications Administration Bureau under the Ministry of Industry and Information Technology, provided a clear answer regarding the issue of cloud service licenses.

As cloud services have been incorporated as a new service model into the revised Catalogue of Telecommunications Business Categories, enterprises that originally held an Internet Data Center (IDC) license and are de facto engaged in cloud services or Content Delivery Network (CDN) services are required to submit a written commitment to meet the corresponding operational licensing requirements and obtain the relevant business licenses by the end of the year.

If the commitment is not fulfilled as scheduled, the corresponding business operations shall be prohibited starting from April 1, 2017. For those that have made commitments, enterprises failing to obtain the required licenses by the end of the year in accordance with the committed timeline shall be prohibited from conducting the corresponding business operations starting from January 1, 2018. According to Zhang Jian, there are currently 1,272 enterprises in China holding IDC (Internet Data Center) licenses, 12 enterprises with cloud service licensing qualifications, and 267 enterprises have committed to obtaining the necessary licenses by the end of the year.

Due to the presence of economies of scale, the public cloud sector exhibits a pronounced Matthew effect, where “the strong grow stronger.” The primary reasons are:

1. Hardware costs decrease on a per-unit basis as scale increases: As hardware scale expands, companies’ bargaining power strengthens, resulting in lower unit costs at larger scales.

2. The larger the platform scale, the richer its products and services, and the stronger its appeal to the industry.

Currently, the top three public cloud providers in China are Alibaba Cloud, Tencent Cloud, and Kingsoft Cloud. Alibaba’s 2017 financial report showed that Alibaba Cloud’s revenue grew by 120.7%, reaching RMB 6.663 billion, compared to just RMB 1.271 billion in 2015. With strong momentum, Alibaba Cloud entered the “Visionaries” quadrant upon its first inclusion in the Gartner Magic Quadrant in 2017.

On January 4, 2018, Kingsoft Cloud announced that it had secured an additional $220 million in funding, following its $300 million Series D round. This brought the total amount raised in its Series D financing to $520 million, setting a new record for fundraising in China’s cloud industry. With this investment, Kingsoft Cloud’s post-money valuation reached $2.12 billion, once again breaking the record for the highest valuation of an independent cloud service provider in China.

Compared with public clouds, the implementation of traditional healthcare informatization is hospital-centric and relatively fragmented. Each hospital must invest substantial human, material, and financial resources, resulting in limited economies of scale. The domestic traditional healthcare informatization sector is led by more than ten listed companies, including Donghua Software, Winning Health, Neusoft Group, and Wanda Information. After nearly two decades of development, the market landscape has largely stabilized, without forming a true Matthew effect, and industry concentration remains low.

After years of development, traditional hospital information systems have reached a critical juncture for upgrading and replacement, with healthcare institutions demonstrating a strong willingness to modernize. New-generation SaaS products characterized by integration, unification, intelligence, and enhanced interconnectivity are poised to become the focal point of hospital informatization upgrades, giving rise to a number of emerging health IT enterprises. Furthermore, changes in operational models driven by medical consortia and family doctor contracting programs have created significant market opportunities for these new types of informatization companies.

These new information technology enterprises have emerged in large numbers. Due to the internet-based nature of SaaS products, industry consolidation is inevitable once they reach a certain scale, a trend already evident in the cloud PACS sector.

According to a cloud PACS practitioner, China’s medical PACS industry will undergo a major reshuffle in the coming years. The number of PACS vendors is expected to plummet from over 300 currently to fewer than 20. These remaining 20 companies will include not only the fortunate incumbents that survive but also newly established, well-capitalized players.

The reasons are multifaceted, with the most direct one being internetization. Internetization has transformed PACS projects from small-scale, workshop-style operations into large-scale, coordinated efforts akin to group army campaigns. This shift inevitably raises corporate demands for capabilities in capital, technology, talent, market expansion, and management. With the development of third-party medical imaging centers, cloud PACS vendors are poised to welcome a new wave of growth. This reshuffling transformation will rapidly increase industry concentration among top players.

Similar to Heyun PACS, VCBeat anticipates that the medical SaaS sector—encompassing platforms such as medical consortiums and family doctor contracting services—will undergo significant industry consolidation. The leading companies that emerge will become the preferred partners for top-tier cloud computing providers, potentially ushering in a true boom period for medical cloud services.

Four Major Pathways for Cloud Computing to Enter the Healthcare Sector at the Current Stage

An examination of cloud computing companies’ strategic presence in the healthcare sector reveals that cloud infrastructure enables the integration of diverse application products tailored to meet varying medical needs. Whether it is Alibaba Cloud’s ET Medical Brain Open Platform or Kingsoft Cloud’s Tiered Diagnosis and Treatment Assistance Management Platform, both represent applications deployed across different scenarios based on cloud computing. As many industry insiders have noted, “The cloud is the soil.” If cloud computing is viewed as fertile land, then virtually anything can grow upon it.

According to VCBeat’s observations, medical cloud computing is poised to achieve breakthroughs first in the following four healthcare sectors:

From raw files generated by gene sequencing to processed files, the entire workflow is fully standardized; however, the biggest challenge lies in time, specifically analysis speed.

Taking the analysis of whole-genome sequencing data for a single individual as an example, standalone computing requires 5 to 8 days. By leveraging the distributed processing capabilities of cloud computing, the computation time is reduced to just 3 hours, representing more than a 50-fold improvement in speed. For the analysis of whole-exome sequencing data from 1,000 individuals, the processing time has been reduced from 100 days to approximately 22 hours. However, deploying large-scale distributed computing clusters on-premises places excessive pressure on enterprises, with prohibitive costs making it unaffordable for many companies.

Domestic genomics companies now generate tens of petabytes (PB) of sequencing data annually. This massive volume places severe strain on corporate data centers, forcing continuous investment in infrastructure expansion and driving up costs.

By adopting solutions provided by cloud computing companies, costs can be effectively controlled. For cloud-based services tailored to gene sequencing, cloud providers typically charge genetic enterprises a fee that is significantly lower than the cost of building and maintaining an in-house infrastructure.

According to Gu Fei, a precision medicine scientist at Alibaba Cloud, Alibaba Cloud’s pricing models include pay-per-compute and subscription-based options (monthly or annual).

In terms of storage, Alibaba Cloud Object Storage Service (OSS) offers three tiers: Standard, Infrequent Access, and Archive. Standard storage provides rapid real-time access, while Archive storage requires a restoration time of less than one minute for data retrieval. Data that does not require frequent access is better suited for Infrequent Access or Archive storage, which are also more cost-effective.

For instance, when certain genetic companies need to conduct research and analysis on genomic data, they frequently access the data, necessitating the use of standard storage. In contrast, for historical data, such as user sequencing data from several years ago, low-frequency or archival storage is typically employed.

Take the collaboration between PKU Healthcare IT and Kingsoft Cloud as an example. Peking University People's Hospital deployed its CDR (Clinical Data Repository) data center to the cloud.

The Zhiyi Cloud solution is a new-generation model based on the “public cloud + private cloud” architecture, primarily comprising three components: lightweight private cloud, dedicated cloud, and public cloud.

By implementing a lightweight private cloud solution, hospital information systems are integrated and data is standardized, thereby minimizing the hospital’s investment in hardware and software. Through a dedicated cloud solution within the public cloud infrastructure, hospitals are provided with exclusive hardware and software environments that deliver secure, stable, and rapid application services, freeing hospital IT staff from endless operational and maintenance tasks. Finally, by leveraging the public cloud, broader medical informatics services spanning multiple healthcare institutions are enabled to serve society as a whole.

According to the project leader, by leveraging the infinitely scalable nature of cloud computing resources, hospitals can enjoy superior healthcare IT services at a lower cost.

Community 580 is an information technology product under New Orange Technology, designed for family doctor contract services.

The services of Community 580 are collectively referred to as the “Capability Cloud.” Community 580 leverages Alibaba Cloud servers to deploy its products in the cloud, utilizing Alibaba Cloud’s stable computing capabilities to ensure reliable business operations.

In addition to information technology services, the “Capability Cloud” also integrates a range of medical services, including intelligent diagnosis, pharmaceutical delivery, and laboratory testing. Once these third-party services are integrated into the Community 580 platform, they can rapidly empower community health service centers and family doctors. Furthermore, various medical data from healthcare institutions can be quickly made available to physicians and residents through integration with the Community 580 platform, thereby generating substantial value.

For most community health service centers, building their own systems to integrate various services is often hindered by insufficient funding and maintenance capabilities. Through the “Capability Cloud” platform of Community 580, community hospitals can be equipped with services such as patient enrollment, health management, medication delivery, and remote diagnosis and treatment within just one to two weeks. This tightly connects patients, medical data, healthcare services, and the Internet of Things (IoT).

The 2017 Tianchi Medical Competition, a highly popular event, was a contest that integrated the three core elements of artificial intelligence: data, algorithms, and computing power. In this competition, the Alibaba Cloud platform effectively combined these three components.

The platform features a three-tier architecture comprising the infrastructure layer, the Apsara distributed cloud operating system layer, and the cloud and big data layer. The cloud and big data layer is built upon Alibaba Cloud’s self-developed cloud computing products (ECS, NAS, SLB, VPC) and big data products (ODPS, PAI). Alibaba Cloud has essentially created a stage where participants can fully showcase their talents in medical imaging algorithms, allowing data to soar through the cloud.

To address security concerns, the Alibaba Cloud team has developed a dedicated data security “cage.” Through filtering and containment within this “cage,” sensitive information in imaging data is removed, ensuring that such data is not leaked.

In this competition, 90% to even 95% of the teams utilized 3D solutions. Alibaba Cloud’s Apsara PAI, leveraging its robust linear scalability, provides specialized solutions for 3D workloads. Competing teams can process more than 32 volumetric images of size 128x128x128 or larger at high speed in each iteration, thereby enhancing the accuracy and effectiveness of nodule detection.

1. Shanxi Securities: In-Depth Analysis of the Cloud Computing Industry—Openness and Aggregation, Focusing on New Momentum in the “Cloud”

2. Pacific Securities: Gradual Volume Expansion Across the Cloud Industry Chain, with Resonant Development in Technology and Market

3. Zhongtai Securities: The Cloud Computing Revolution, Path Becoming Clear