Opportunities in Prescription Diversion: 2018 Market Size to Reach RMB 160 Billion, Retail Pharmacies Benefit, DTP Model Gains Favor

Prescription Outflow: A Buzzword in the Pharmaceutical Retail Sector in Recent Years. Against the backdrop of the broader “separation of prescribing and dispensing,” drug sales are undergoing structural adjustments, with out-of-hospital channels capturing the incremental growth driven by prescription outflow.

In the process of accommodating prescription outflow, pharmaceutical manufacturers, distributors, retail pharmacies, and e-commerce platforms have made proactive efforts, developing various models such as hospital-adjacent pharmacies, Direct-to-Patient (DTP) pharmacies, and new retail.

VCBeat (WeChat ID: vcbeat) has surveyed current cases of outpatient prescription outflow in China, aiming to comprehensively analyze its impact on the industry and future development trends.

Policy: The Separation of Prescribing and Dispensing Is an Irreversible Trend

Due to historical reasons, the revenue of China’s public healthcare system has been heavily reliant on pharmaceutical sales, leading to issues such as a high drug-to-revenue ratio, inflated drug prices, illicit benefit transfers, and bribery in the pharmaceutical sector. Against this backdrop, one of the core tasks of healthcare reform is to abolish the practice of “subsidizing healthcare with drug profits.”

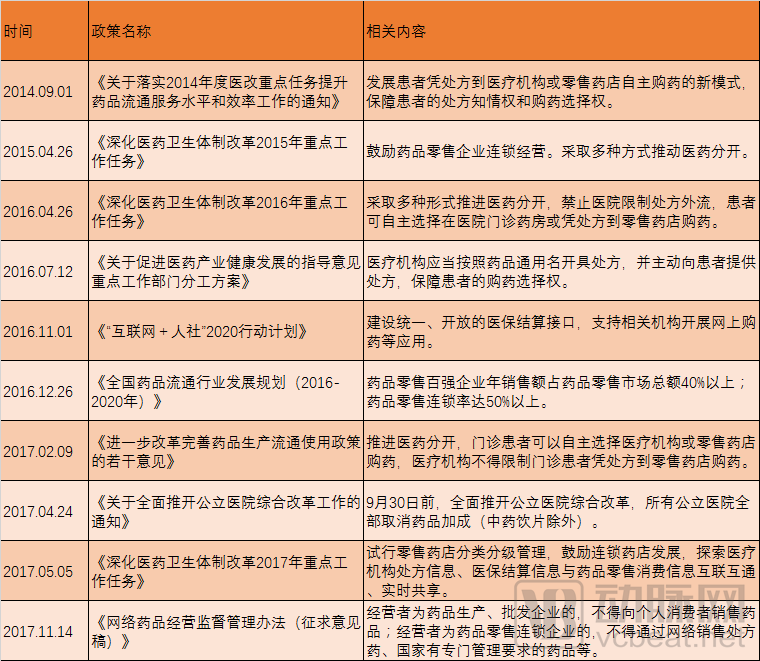

Recent Policies on Prescription Outflow

In 2000, the State Council’s Office for Healthcare Reform issued the “Guiding Opinions on the Reform of the Urban Medical and Health System,” which stipulated that pharmaceutical revenues should be “accounted for separately, managed independently, submitted centrally, and reasonably refunded,” thereby initiating the effort to dismantle the mechanism of subsidizing healthcare with drug profits.

The 2009 “New Healthcare Reform” proposed advancing the separation of pharmaceuticals from medical services and actively exploring various effective approaches to gradually reform the mechanism of subsidizing healthcare with drug revenues. Since then, relevant policies have been continuously advanced, and the “separation of pharmaceuticals from medical services” has been progressively implemented.

The report to the 19th National Congress of the Communist Party of China proposed the comprehensive elimination of the practice of subsidizing healthcare services with drug profits and the improvement of the drug supply and guarantee system. This signifies that the separation of prescribing from dispensing will continue to advance, making adjustments to pharmaceutical retail channels inevitable.

Currently, the primary policy direction for guiding prescription outflow is toward retail pharmacies. For instance, the 2016 Healthcare Reform Task List stipulated that hospitals are prohibited from restricting prescription outflow, allowing patients to freely choose whether to purchase medications at hospital outpatient pharmacies or at retail pharmacies with a valid prescription.

The list of healthcare reform tasks for this year features slight changes in detail. Pilot programs for the tiered management of retail pharmacies are proposed, with encouragement for the development of chain pharmacies. Efforts will be made to explore the interconnectivity and real-time sharing of prescription information from medical institutions, health insurance settlement data, and drug retail consumption records. This signifies that policies have provided clearer direction on how pharmacies can accommodate the outflow of prescriptions, offering support in terms of prescription sources and health insurance payment mechanisms.

Furthermore, the “Internet + Human Resources and Social Security” policy released at the end of last year stated that the Ministry of Human Resources and Social Security will open up payment and settlement interfaces for social security cards, supporting integration with various social payment channels. A unified and open medical insurance settlement interface will be established to support relevant institutions in developing applications such as online pharmaceutical purchases. This means that pharmaceutical e-commerce has also become one of the alternative channels for prescription outflow.

In addition to the separation of prescribing and dispensing, public hospitals’ strict control over the drug-to-revenue ratio, the zero-markup policy, and distribution channel rectification have also accelerated the outflow of prescriptions from hospitals.

From the data, in 2015, the total revenue of public hospitals in China was 2.08 trillion yuan, with a drug proportion of 36.2%, far higher than that of developed countries. The State Council's Healthcare Reform Office required that by the end of September 2017, all public hospitals nationwide would eliminate drug markups (except for traditional Chinese medicine decoction pieces), and at the same time, the overall drug proportion in public hospitals in the first four batches of 200 pilot cities should be reduced to around 30% before 2017. After strictly controlling the drug proportion, pharmacies will transform from profit centers into cost centers within hospitals, promoting the gradual separation of pharmacies from hospitals.

“Two-Invoice System + VAT Reform + Distribution Rectification”: The pharmaceutical distribution channels have been compressed, making the distribution process more transparent and, to some extent, curbing benefit transfers tied to drug distribution, thereby creating an opportunity for hospitals to take over prescription drug sales.

Furthermore, it is worth noting that fiscal subsidies and adjustments to medical service prices have played a significant role in dismantling the mechanism of subsidizing healthcare providers through drug markups. Fiscal subsidies have alleviated, to some extent, the financial pressure on hospitals following the implementation of zero-markup drug policies, while adjustments to medical service prices have addressed the issue of physicians’ income.

Overall, driven by the comprehensive reform of public hospitals and the rectification of pharmaceutical distribution channels, the separation of prescribing from dispensing has become an inevitable trend. Before supporting policies and solutions are clearly defined, the industry will undergo a gradual process of adaptation and experimentation under policy guidance, paving the way for the full implementation of this separation.

Retail Pharmacies Are the Biggest Beneficiaries of Prescription Outflow

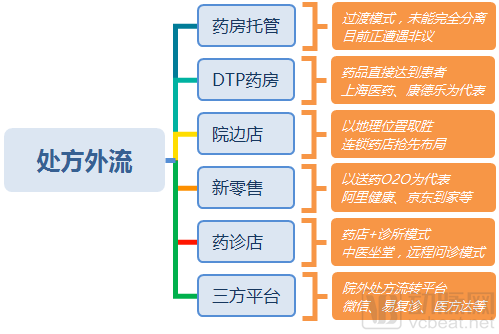

In the process of accommodating the outflow of prescriptions, numerous beneficial initiatives have emerged, including DTP (Direct-to-Patient) pharmacies, pharmacy trusteeship, retail pharmacies located adjacent to hospitals, the “Internet +” new pharmaceutical retail model, pharmacy-clinic collaborations, and off-hospital prescription circulation platforms. Below, we will analyze some typical cases among these initiatives.

DTP (Direct to Patient) refers to the model where pharmaceutical products are delivered directly to patients. Typically, pharmaceutical manufacturers authorize pharmacies to act as direct distributors, thereby eliminating intermediaries. After obtaining a prescription from a hospital, patients can purchase medications at these pharmacies and receive professional guidance on their use. The DTP model relies on deep integration between pharmacy and pharmaceutical company resources. Its product portfolio primarily consists of high-margin specialized drugs and novel specialty medicines, most of which are paid out-of-pocket.

Currently, the DTP pharmacies performing well in China include Shanghai Pharmaceuticals, Guoda Drugstore, Cardinal Health, and Laobaixing Pharmacy.

Shanghai Pharmaceuticals operates more than 40 DTP (Direct-to-Patient) pharmacies in East and North China. On November 15, Shanghai Pharmaceuticals announced that it expects to acquire Cardinal Health’s China business for $557 million, with its DTP pharmacies representing a key asset. Cardinal Health currently operates 30 DTP pharmacies in China, each generating annual sales of RMB 20 million—40 times that of an average retail pharmacy—with total annual revenue ranging from RMB 600 million to RMB 700 million. Following the acquisition of Cardinal Health’s China operations, Shanghai Pharmaceuticals will become the company with the largest number of DTP pharmacies and the most extensive DTP network coverage in China, positioning it for significant future growth.

Pharmacy Trusteeship refers to a drug operation model in which medical institutions, through contractual arrangements and without changing the ownership of the pharmacy or altering state preferential policies for non-profit medical institutions, entrust the sales of pharmaceuticals to qualified pharmaceutical enterprises with strong operational and management capabilities and the ability to bear corresponding risks. These enterprises engage in compensated operation and management, thereby clarifying the rights and obligations between the owners and operators of hospital pharmacies.

Currently, pharmacy trusteeship enterprises in China are predominantly hospital-led, with pharmaceutical distribution companies serving as the primary operators. Notable examples include the collaboration between Shunde Hospital of Jinan University and Guangzhou Pharmaceutical Holdings, as well as partnerships between multiple hospitals in Wuhan and companies such as Sinopharm Holding and Jinma.

Due to the failure to fully sever the financial ties between hospitals and outsourced pharmacies, coupled with issues such as exorbitant management fees, the outsourced pharmacy model is currently in an awkward predicament, facing sustained criticism within the industry.

Strictly speaking, pharmacy stores adjacent to hospitals are not a formal channel for accommodating the outflow of prescriptions. However, against the backdrop of prescription outflow, these stores are poised to reap the initial benefits due to their geographical proximity to hospitals. Consequently, developing such pharmacies has become a popular investment direction under the trend of prescription outflow.

“Internet +” New Pharmaceutical Retail primarily refers to the pharmaceutical O2O (Online-to-Offline) model, including platforms such as the AliHealth O2O Alliance, JD Daojia, Haoyaoshi, Dingdang Kuaiyao, and Kuaifang Songyao. Some fresh food delivery platforms are also entering the pharmaceutical and healthcare market, becoming significant participants. The new pharmaceutical retail model meets patients’ demands for convenient medication purchases and home delivery services; however, current product categories remain largely concentrated on over-the-counter (OTC) drugs and health products, with prescription sources constituting a major limiting factor.

The “pharmacy + clinic” model refers to the establishment of clinics within pharmacies to provide basic medical services and prescription refills for chronic diseases. The “TCM consultation in-store + pharmacy” model is a typical example, as Traditional Chinese Medicine (TCM) enjoys broad public support and serves as a significant driver of customer traffic. With the rise of internet healthcare, the “remote consultation + pharmacy” model has emerged, including initiatives such as Micro-Pharmacy Clinics and Micro-Consultations. This model leverages medical resources efficiently to offer residents lightweight consultations and electronic prescriptions, and is currently being implemented across various regions.

The out-of-hospital prescription circulation platform is a new model that has emerged in recent years. It operates by having third-party companies build platforms that provide information technology, patient management, and data management services to medical institutions and pharmacies. Currently, companies such as WeChat, Yi Fuzhen, and Yifangda are undertaking such projects in China, with pilot regions including Guangdong, Harbin, and Guangxi.

Overall, retail pharmacies, particularly chain retail pharmacies, are the primary beneficiaries of prescription outflow. This is because: first, retail pharmacies possess a strong operational foundation, enabling them to systematically meet patient demand for medications and pharmaceutical care services; second, the high coverage rate of retail pharmacies in China positions them as the preferred choice for residents purchasing medicines; and third, supported by digital tools and prescription circulation platforms, the competitiveness of retail pharmacies is strengthening, allowing them to provide residents with more diversified and precise medical, pharmaceutical, and health management services.

With a steady customer flow, pharmacies can leverage this advantage to sell health products, including dietary supplements, cosmeceuticals, and smart medical devices. Overall, retail pharmacies are poised to benefit from incremental growth driven by the outflow of prescription drugs from hospitals and diversified business operations. Meanwhile, the number of retail pharmacies in China has approached saturation. Driven by policy and capital, the sector will undergo structural adjustments, accelerating the process of survival of the fittest, with asset securitization emerging as a key direction.

It should also be noted that China is currently promoting tiered diagnosis and treatment systems and the development of medical consortia. The service capabilities of primary healthcare institutions are improving, while restrictions on medication at the primary care level have been relaxed. This means that primary healthcare institutions will divert a portion of patients and prescription demand from large hospitals, representing a significant channel for the outflow of prescriptions.

Outlook: The scale of prescription outflow will reach 160 billion yuan in 2018

From a global perspective, the separation of prescribing and dispensing is an inevitable trend. The United States has implemented a relatively thorough separation, with approximately 60–70% of pharmaceuticals sold through non-hospital channels (such as retail pharmacies and PBM mail-order services). Japan has practiced this separation for over 40 years, and currently, around 70% of prescription drugs are dispensed through out-of-hospital channels. The experiences of the United States and Japan provide valuable references for estimating the scale of prescription outflow in China.

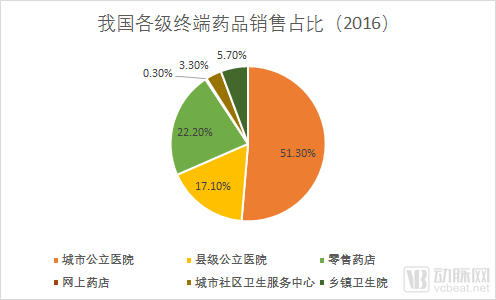

Currently, China’s pharmaceutical market is dominated by urban public hospitals and county-level public hospitals, with retail pharmacies serving as a supplementary channel and other channels accounting for a relatively small share. According to data from Menet, the size of China’s pharmaceutical market in 2016 was approximately RMB 1.5 trillion, representing a year-on-year growth of 8.3%. The hospital channel accounted for a combined 77.4% of the market, while the pharmacy channel comprised only 22.2%, and online pharmacies represented merely 0.3% of the pharmaceutical market.

If the pharmaceutical market maintains a growth rate of approximately 8–9%, its size is projected to reach RMB 1.76 trillion by 2018. If around 30% of pharmaceutical products are sold through out-of-hospital channels, this would imply that the out-of-hospital channel will amount to approximately RMB 530 billion. After accounting for the natural growth of the out-of-hospital channel, the scale of prescription outflow is estimated at around RMB 130 billion.

Certainly, the scale of prescription outflow can also be calculated based on the reduction in the drug revenue share of hospitals. According to the National Health and Family Planning Commission’s Statistical Yearbook, the total revenue of public hospitals in 2015 was RMB 2.0843 trillion, with a drug revenue share of 36.2%. Assuming public hospital revenue maintains an average annual growth rate of 8–9%, the total revenue in 2018 would reach approximately RMB 2.66 trillion. With the drug revenue share remaining unchanged, drug revenue would amount to RMB 962.9 billion. However, if the drug revenue share is controlled at 30%, prescriptions worth approximately RMB 165 billion would flow out of hospitals.

The above calculations indicate that,By 2018, the outflow of prescriptions will bring an incremental growth of over RMB 130 billion or RMB 165 billion to the out-of-hospital market. Out of prudence, if the target value is adjusted downward, the scale of prescription outflow in 2018 will still reach at least RMB 100 billion.

The above analysis examines the incremental growth that prescription outflow may bring to the out-of-hospital market. In practical implementation, however, prescription outflow must overcome a series of barriers, including issues related to prescription sources, patient willingness, medical insurance integration, service capacity, and information management.

Despite the implementation of policies aimed at separating medical services from pharmaceutical sales, hospital and physician revenues remain heavily dependent on drug sales. Issues such as overprescribing, the use of high-priced medications, and pharmaceutical bribery continue to persist despite repeated prohibitions. The objective of “separating medical services from pharmaceutical sales” is to exclude drug revenue from healthcare institutions’ income streams, sever direct financial ties among drug bidding and procurement processes, healthcare institutions, medical staff, pharmaceutical companies, and distributors, and establish a system in which clinical diagnosis and treatment operate independently from medication dispensing.

As market liberalization advances, a patient-centered, value-oriented healthcare service system is beginning to take shape. Driven by this trend, pharmaceutical retail is also transitioning toward service-oriented models, with increasingly diversified business operations expanding from mere product sales to basic medical services and health management. Retail pharmacies and similar entities should provide pharmaceutical care services that surpass those offered by medical institutions, including more comprehensive medication counseling, delivery services, and promotional activities, thereby gradually guiding patient preferences.

As a key payer, medical insurance has played a leveraged role in the process of prescription outflow. Currently, there is significant pressure on medical insurance funding and payments, making cost containment a long-term priority. Prescription outflow should align with the direction of medical insurance cost control, leveraging socialized approaches to reduce drug costs.

Furthermore, the outflow of prescriptions will test the service capabilities and information management capabilities of relevant stakeholders. For retail pharmacies, the number of licensed pharmacists and their service levels largely represent their capacity to handle prescribed medications. The management of prescription and patient information also poses a challenge for enterprises with weak informatization capabilities.

Amid the trend of prescription outflow, investment opportunities will emerge in enhancing the informatization level of pharmacies, mergers and acquisitions among regional retail pharmacies, new pharmaceutical retail models, and B2B pharmaceutical e-commerce.

Take a Long-Term View. We believe that the outflow of prescriptions from hospitals is an irreversible trend, with new specialty drugs and long-term medications for chronic diseases being the first to shift away from medical institutions; retail pharmacies located near hospitals and Direct-to-Patient (DTP) pharmacies will be the primary beneficiaries. In accommodating this prescription outflow, stakeholders should optimize their operational structures and enhance service capabilities to adapt to medical insurance cost-containment measures and patient needs. The outflow of prescriptions will cultivate a new blue ocean in pharmaceutical retail.

We extend our gratitude to Qin Gang, General Manager of Qianfang Baiji, and Zhang Ying, Investment Director at GF Xinde, for their support in shaping the concept and drafting of this article.

References:

20170619-Orient Securities-In-depth Report on the Pharmaceutical and Biological Industry: Prescription Outflow Drives Incremental Growth in Pharmacies, While Regulatory Upgrades and Asset Securitization Spur Consolidation of Existing Assets

20170625-China Merchants Securities-Pharmaceuticals and Biotechnology: Special Report on Retail Chain Pharmacies-Prescription Outflow Gradually Materializing, OTC Drugs to Raise Prices and Offer Discounts

20170713-Guosen Securities-Special Research on Chain Retail Pharmacies (Part I): Riding the Spring Breeze of Healthcare Reform, Welcoming the Outflow of Prescriptions

Analysis of the Prescription Outflow Trend: Market Size May Reach RMB 800 Billion by 2020

An In-Depth Analysis of the Wuzhou Model: Perhaps the Best Template for Separating Prescribing from Dispensing in China