2017 Healthcare Industry Annual Report: Decoding 8 Sub-sectors with the Proprietary VB Quadrant Model – A Data-Driven Insight into Medical Innovation

VCBeat’s Eggshell Institute released its 2017 Annual Report, “A Data-Driven Glimpse into Healthcare: 2017 Competitiveness Report on the Medical and Health Industry,” at the Future Healthcare Top 100 Forum on December 15.

From 2011 to 2016, internet healthcare traversed several critical growth milestones characteristic of an emerging industry. These included the disruptive innovation marked by Chunyu Doctor’s launch of mobile consultation services in 2011, the industry’s explosive expansion during the 2014 capital investment boom, and the subsequent downturn in both the sector and capital interest from 2015 to 2016, driven by the exhaustion of traffic dividends.

As 2017 draws to a close, VCBeat’s Eggshell Research Institute has developed a novel quadrant model to visualize the operational status of companies in the field of healthcare industry innovation and to map out the competitive landscape. By analyzing corporate operational data and investment/financing records, this model enables more convenient observation of the current operational state of enterprises within specific sub-sectors, thereby enhancing the accessibility and understanding of our research findings. In this report, alongside an interpretation of the model, the Eggshell Research Institute reviews the changes and developments in the healthcare sector over the past year from the perspectives of productivity, production relations, and factors of production.

We believe that, after five years of fluctuations and adjustments, innovation in the healthcare industry began to gradually enter a phase of rational development starting in 2017, as evidenced by the following key aspects:

1. Enhancement of Productivity: New technologies are generating new productive forces, with big data driving the optimization of hospital management processes and fostering new insights into disease treatment and rehabilitation.

2. Changes in Production Relations: To achieve tiered diagnosis and treatment and address the challenges in primary healthcare, private and public hospitals, as well as public hospitals among themselves, have shifted from competition to collaboration, supplementing primary healthcare resources and establishing medical consortia.

3. Shift in Production Factors: The Brand Effect in Healthcare Is Transitioning from Hospitals to Physicians.

4. Upgrading of Consumer Mindsets: Rising consumer demand is driving the marketization of the healthcare industry, creating greater market opportunities.

This report is based on interview records from senior VCBeat journalists and comprehensive industry data from the VCBeat knowledge base. Combined with VBInsight’s research on benchmark enterprises in the industry and its insights into industry trends, it provides a summary and outlook on China’s healthcare industry across eight sections:

Part I: Pioneering the VB Quadrant Model for the Future Healthcare Industry

Part II: VB Quadrant Model Analysis

Part III: New Technologies Transform Productivity and Upgrade the Healthcare Industry

Part IV Changes in Production Relations: From Competition to Collaboration, A New Landscape of Differentiation for Healthcare Institutions

Part V: Changes in Production Factors: The Brand Effect Is Shifting from Hospitals to Physicians

Part VI The Upgrade of Consumption Concepts: Rising Consumer Demand Drives the Marketization of the Healthcare Industry

Part VII: The Healthcare Industry Enters a New Era of Cross-Industry Competition

Part VIII: Analysis of Investment and Financing in the Healthcare Industry from January to November 2017

Introduction to the VB Quadrant Model

Previously, the primary work of VCBeat’s VBInsight involved providing industry professionals focused on the healthcare sector with research reports covering four key areas: global capital dynamics, emerging technological products and business models, evolution of the industrial ecosystem, and market application trends, analyzed from multiple dimensions including technology, market, capital, and policy.

Now, VCBeat will leverage its proprietary database to develop a big data product focused on investment and financing in the healthcare industry. Additionally, we have created a novel model framework that makes our research findings more accessible and our models easier to implement. In the future, we will provide more industry research insights based on survey data from healthcare companies covered by VCBeat.

At the 3rd Future Healthcare 100 Forum in 2017, VCBeat Research Institute, in collaboration with Zero2IPO Capital, launched the VB Quadrant Model based on the VCBeat database, following multi-dimensional data research on enterprises conducted in the preliminary phase.

Based on the knowledge base of VCBeat, VBInsight has accumulated enterprise and industry data in the healthcare sector. Supported by rigorous analyses from VBInsight and Zero2IPO Capital, we have developed an analytical model that reflects the development status of startups in the medical and health fields, which we call the VB Quadrant. During the model’s development, we extend our gratitude to Zero2IPO Capital for participating as experts in designing the model dimensions, assigning weight scores, and conducting data research.

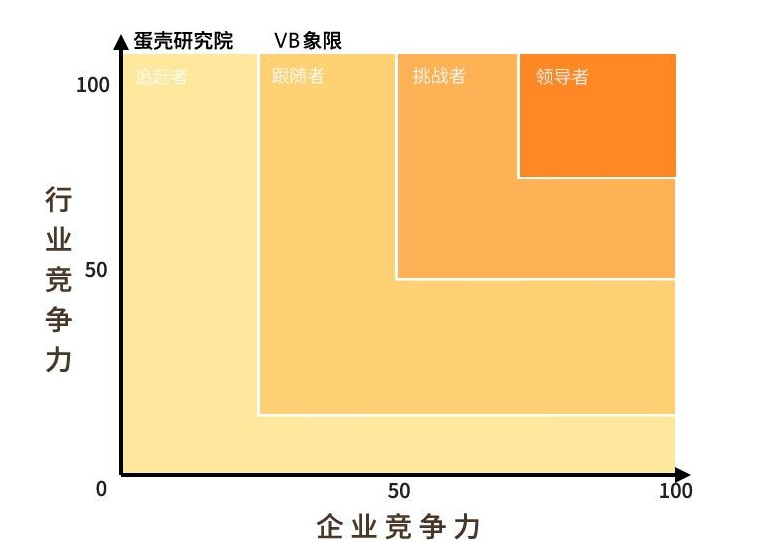

VB Quadrant Model

Leader:The company operates in a niche sector with substantial growth potential, holds a significant market share in its target market, and is recognized as a unicorn within the industry. As a market leader, it sets the pace for other companies in the field in terms of product pricing strategies, new product R&D, distribution channel development, and strategic planning, making it the most likely candidate to achieve an IPO in the near term.

Challenger:These are the most dynamic companies in the market, capable of challenging market leaders and other competitors, with the ambition to seize the position of market leader.

Followers:They follow market leaders and challengers in terms of products, technology, and pricing. Due to certain deficiencies in maturity across markets, products, and technologies, they often secure survival space by serving niche or overlooked market segments. Some companies formulate their corporate strategies by imitating challengers and leaders.

Chasers:Companies in this segment currently have a relatively small scale or operate in markets with limited growth potential. These enterprises are primarily startups. However, their progress over the next one to two years could be the most significant.

Of course, a company’s competitive position is not static; today’s market leader may not necessarily remain the industry frontrunner tomorrow. Therefore, market leaders strive to maintain their leadership, while other competitors race to catch up and improve their standing. It is this intense market competition that drives enterprises in the healthcare sector to compete with one another, thereby promoting the development of both the industry and society. The VB Quadrant Model, developed by VCBeat (VBInsight), objectively measures and evaluates competitive indicators of companies in the healthcare field to determine their competitive positions in the market.

Implementation Methods of the VB Quadrant Model

Step 1: Experts determine the dimensions for indicator scoring. By examining both the industry and enterprise perspectives, we identify the key dimensions that reflect industry and corporate competitiveness, thereby establishing a three-tier indicator model for assessing enterprise competitiveness.

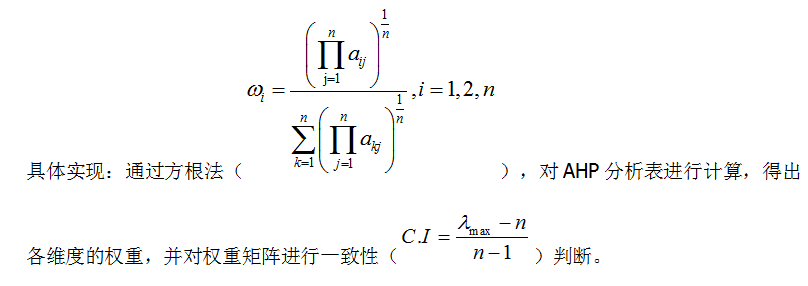

Step 2: Determine the weights of indicators at each level. Experts are invited to employ the Analytic Hierarchy Process (AHP) to evaluate the relative importance of indicators, taking into account the essence of industry competitiveness. The AHP quantifies factors that are difficult to measure directly; combined with expert scoring, the geometric mean method is used to calculate the priority vectors for each dimension, thereby determining the indicator weights. For certain specific indicators, experts directly assign and quantify their weights based on practical considerations.

Step 3: Establish scoring criteria for underlying metrics. Based on the actual conditions of indicators across different dimensions, an expert panel shall define distinct scoring gradients and standards. Metrics for certain dimensions may be updated in real time, reflecting daily updates from the VCBeat database.

Step 4: VCBeat and Zero2IPO Capital collect corporate operational data, input industry and company data into the aforementioned model based on established criteria, automatically calculate weighted scores to derive each company’s overall rating, and finally assess comprehensive competitiveness through quadrant analysis.

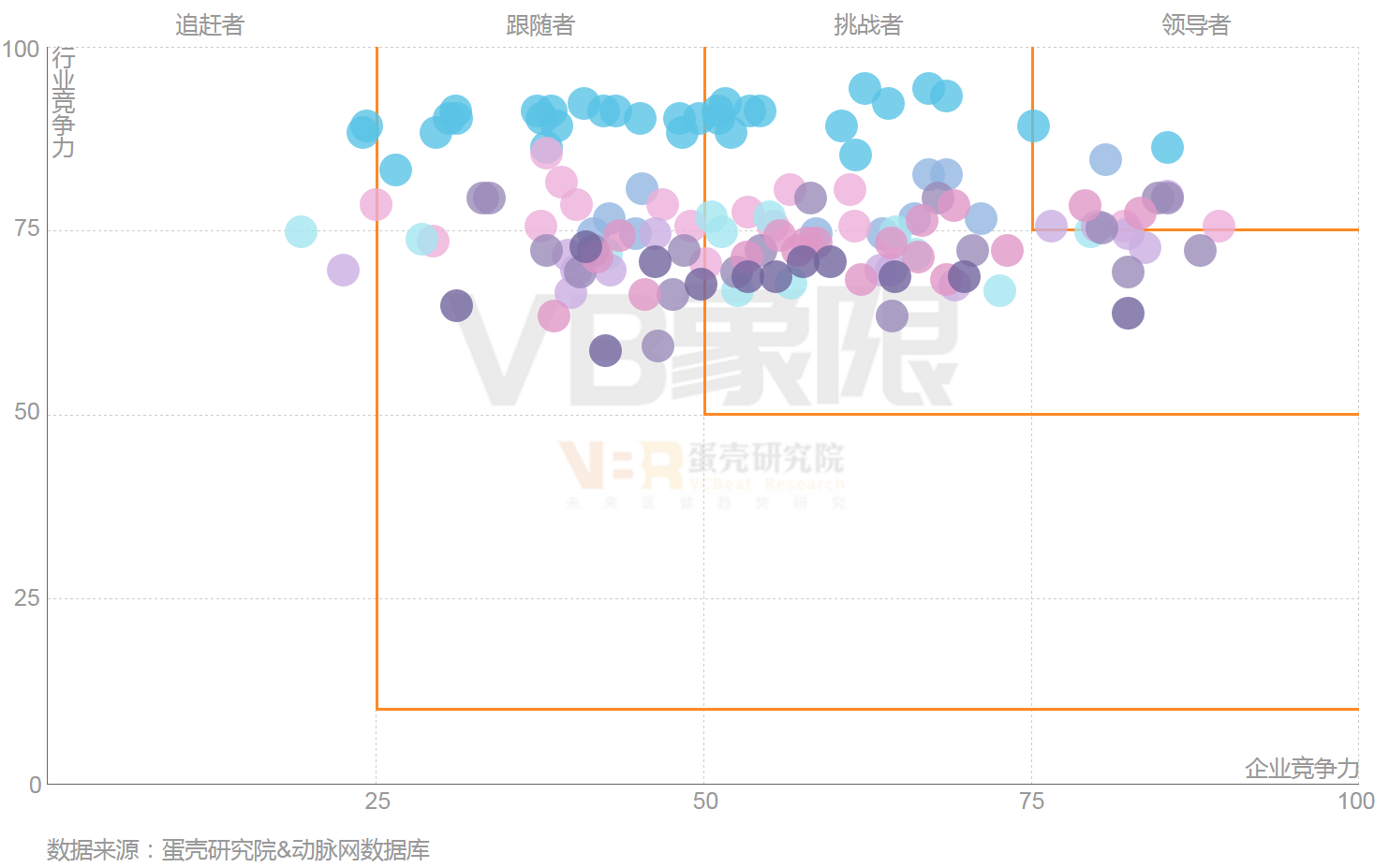

VB Quadrant Model Results

VCBeat, in collaboration with Zero2IPO Capital, conducted surveys and data analysis on hundreds of companies across eight sectors: online medical consultation, healthcare informatics, artificial intelligence, genomics, pharmaceutical e-commerce, clinics, maternal and infant care, and in vitro diagnostics. Through data collection and quantitative analysis, their VB Quadrants were derived.

VB Quadrant Analysis Results

New Technologies Drive New Productive Forces, Upgrading the Healthcare Industry

The development of modern science and technology has reached a critically important stage. The trends of the scientification of technology, the technologization of science, the socialization of science and technology, and the scientification and technologization of society are impacting every sector of the contemporary world in unprecedented ways.

The replication and expression of scientific and technological information systems have had a profoundly far-reaching impact on the politics, economy, culture, and daily life of human society. Much like genes, they determine every aspect of the development of human civilization. Every major breakthrough in science and technology exerts a tremendous influence on the political, economic, and cultural spheres of human society. The scientific and technological revolution plays an extremely important role in transforming the productive forces, relations of production, economic base, and superstructure of human society. Innovation in science and technology has become the fundamental driving force behind the evolutionary development of human civilization.

The economy encompasses processes such as production, exchange, distribution, and consumption, with production at its core. The relationship between science and technology and the economy is, first and foremost, the relationship between science and technology and production. Science and technology differ fundamentally from other tools that regulate the efficiency of production relations; they upgrade or replace existing factors of production by creating new productive forces.

In the medical field, enhancing humanity’s understanding of life serves as both the starting point and ultimate goal of scientific and technological advancement, with technological innovation being the most dynamic and proactive factor in productivity. Only through technological innovation can the efficiency of productivity be fully and positively realized.

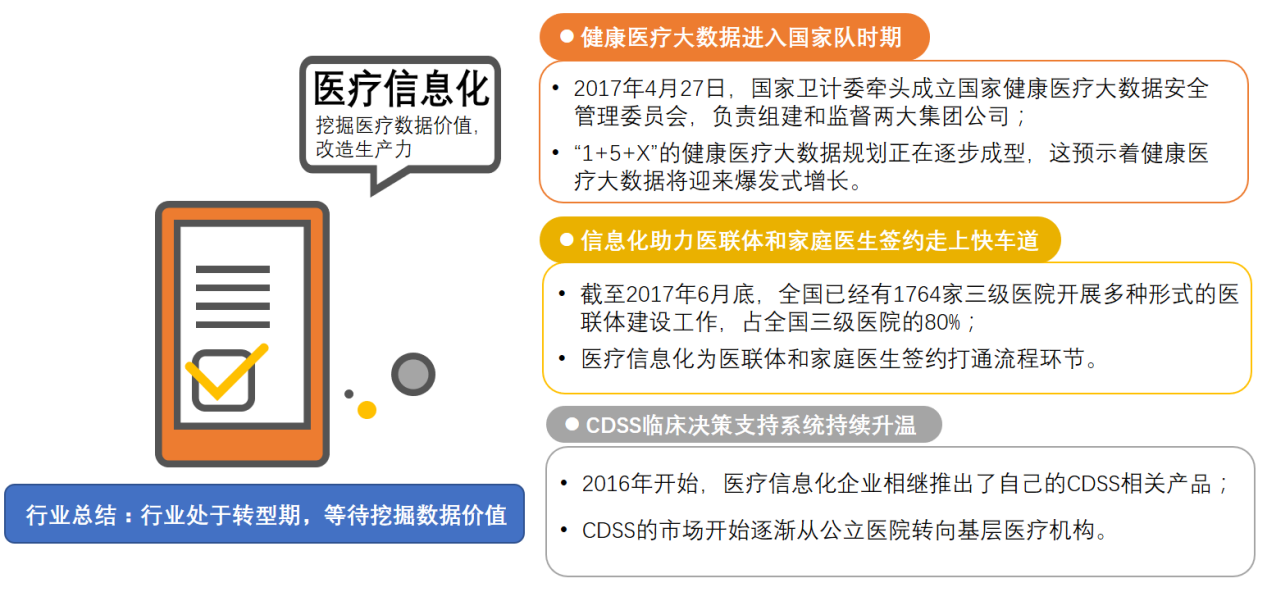

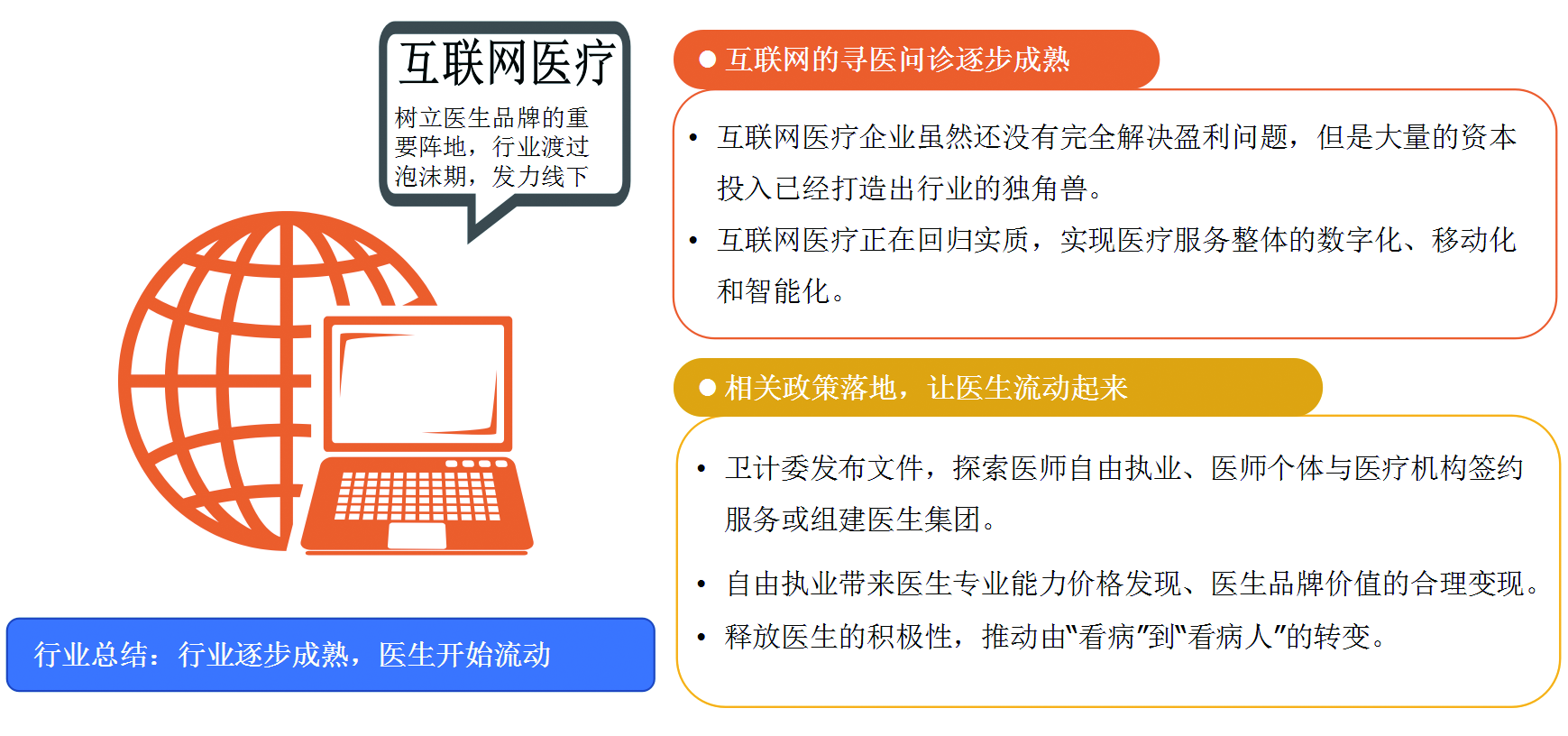

In the Digital Healthcare 1.0 era, internet technologies broke down barriers to medical knowledge, leading to strong capital interest in platforms for sharing medical information and connecting patients with healthcare providers. In the Mobile Healthcare 2.0 era, technological innovations targeting the core of healthcare have become this year’s trend, with the rapid industrialization of genetic testing and artificial intelligence being particularly prominent.

In recent years, the digital health sector has primarily focused on service innovations that disrupt traditional healthcare delivery processes. This year, fields such as artificial intelligence, clinical decision support, medical big data, and genomics have frequently secured substantial funding rounds, signaling the dawn of a healthcare transformation driven by technological innovation. Moving forward, more cutting-edge technologies will be integrated into diagnosis and treatment, bringing about more miracles in saving and improving lives.

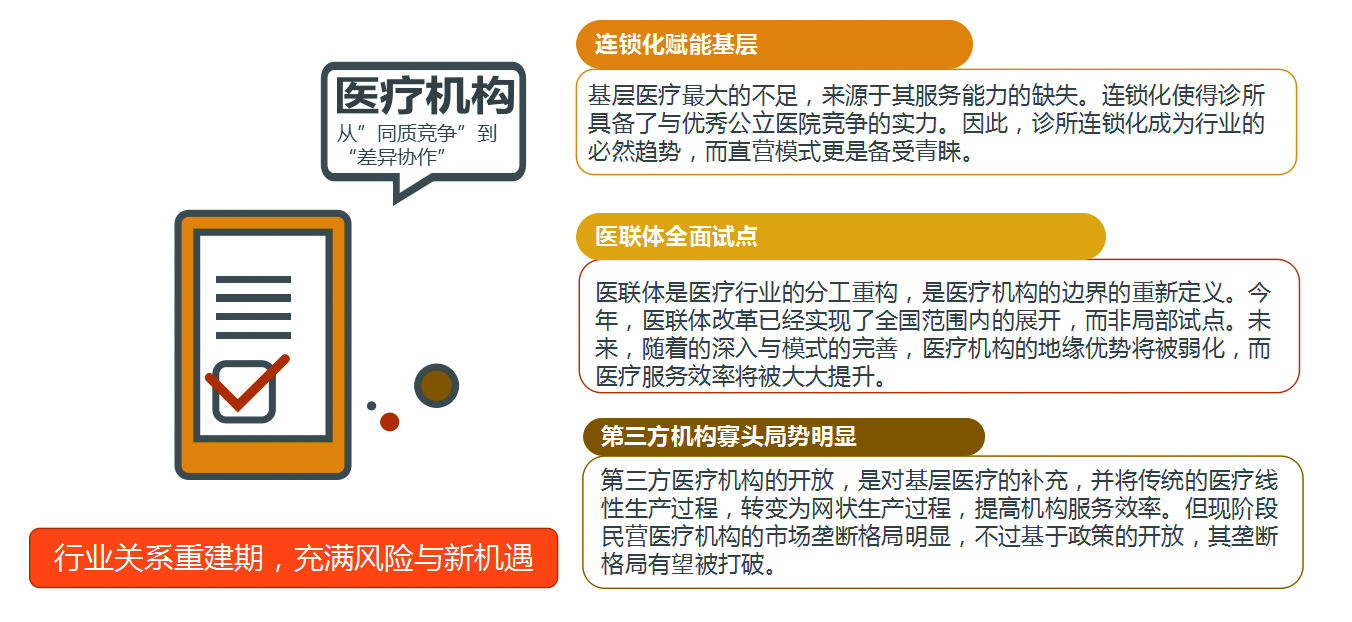

Shifting Production Relations: From Competition to Collaboration—A New Paradigm of Differentiation for Healthcare Institutions

Since the reform and opening-up, multiple industries in China have introduced market competition mechanisms through market-oriented reforms. However, the healthcare industry differs from other sectors. The primary objective of the healthcare industry is not to create commercial value through market competition, but rather to safeguard residents’ health and enhance public well-being. Meanwhile, the healthcare industry plays a pivotal role in improving people’s livelihoods and maintaining national stability and harmony. This implies that China’s healthcare industry must be dominated by public ownership.

The dominance of public ownership does not mean that the healthcare industry is immune to the objective laws of the market economy, especially in today’s context of rapidly growing national demand and increasing levels of domestic marketization and economic freedom. These laws include competition theory. According to this theory, weaker competitors in an industry can only prevail by leveraging first-mover advantages or by creating differentiated value. Meanwhile, participants in industries dominated by public ownership often lack commercial strategic thinking, resulting in a deficiency in competitive strategy.

Individual rational choices often lead to collective irrationality. From the perspective of the competitive landscape in healthcare institutions, such rational decision-making means that medical facilities with vastly unequal competitive strengths offer heavily overlapping services at largely identical prices. This results in highly competitive institutions being overwhelmed with patients, while less competitive ones struggle to attract any.

On the other hand, the Matthew effect has created a vicious cycle in the healthcare industry characterized by “concentration of consumption → enhanced competitiveness of large hospitals → further attraction of consumption → even stronger competitiveness of large hospitals.” For most industries, this is a normal process of market consolidation that enables survival of the fittest among participants and represents an inevitable stage in industrial development. However, as China’s healthcare sector is fundamentally oriented toward safeguarding people’s well-being, the law of the jungle based on survival of the fittest is inherently inapplicable. Consequently, the Matthew effect has instead exacerbated imbalances in medical services across China, reduced overall industry productivity, and perpetuated a vicious cycle where the strong grow stronger while the weak become weaker.

We can posit that the essence of the imbalance in domestic medical resources lies in the homogenized competitive landscape among healthcare institutions. A review of China’s healthcare reform strategies in recent years reveals a consistent underlying logic: assigning distinct service functions to different healthcare institutions to achieve differentiated positioning; enhancing the competitiveness of weaker institutions to drive patient consumption toward primary care levels; and establishing a new production relationship within the healthcare industry characterized by “mutual complementarity and win-win cooperation” among healthcare providers.

Taking the tiered diagnosis and treatment system, a core component of healthcare reforms in recent years, as an example, the term “tiered” itself is imbued with a sense of “differentiation.” It breaks down originally homogeneous services into multiple units, each corresponding to medical service providers with varying levels of competitiveness.

Tiered Diagnosis and Treatment: Starting from the individual’s health needs, this approach triages demands based on severity and urgency (“mild vs. severe” and “non-urgent vs. urgent”) while decomposing the medical care process. By aligning disaggregated patient needs with segmented medical processes, the core functions of healthcare institutions with varying competitive advantages are redefined. This facilitates tiered diagnosis and treatment and establishes a differentiated pattern of industry-wide division of labor and collaboration. In essence, tiered diagnosis and treatment represents a deepening of the division of labor within China’s healthcare sector and a restructuring of its production relations.

Shift in Production Factors: From Hospitals to Physicians, the Brand Effect Is Transferring

Within China’s healthcare system, hospitals are unequivocally the most critical venues for diagnosing and treating diseases, serving as the primary setting for all medical activities. In the process of modernizing hospital management, as hospitals expand and strengthen, only by establishing a strong hospital brand can they continuously enhance their core competitiveness.

Hospitals and physicians are two complementary factors of production in healthcare. In the past, public perception of medical brands was primarily centered on hospitals, specifically public tertiary Grade-A hospitals. A hospital’s brand is closely tied to the technical expertise of its specialties and leading specialists, demonstrated by the ability to diagnose and treat complex conditions that others cannot, thereby earning recognition from peers and society. The brand effect not only attracts patients but also draws in talent and greater resource investment, enabling hospitals to maintain a competitive edge in a fiercely competitive market.

While outstanding physicians serve as vital ambassadors in the process of hospital brand building, cultivating star specialists lays the foundation for a hospital’s brand. Previously, hospitals were the sole destination and platform for renowned physicians. However, with the development of private hospitals, physician groups, private clinics, and internet-based platforms, doctors now have greater opportunities for professional growth and access to diverse platforms.

In the past, it was difficult for physicians’ personal brands to break away from the overarching reputation of their hospitals. In the internet era, a physician seeking to build their own brand must focus on three key areas: specialty discipline branding, personal service branding, and social influence.

Physicians such as Zhang Qiang, Yu Ying, and Cui Yutao have cultivated personal brands on internet platforms that rival even those of hospitals. By providing medical science popularization and engaging with patients online, they have attracted substantial followings. Leveraging their strong personal brands, these “internet-famous doctors” are able to draw sufficient patient volumes regardless of whether they practice within physician groups, private hospitals, or self-operated clinics.

The brand effect in healthcare is gradually shifting from hospitals to individual physicians, with non-public medical institutions—including private hospitals, internet hospitals, shared hospitals, and clinics—emerging as alternative venues for physicians’ clinical practice.

Upgrading Consumption Concepts: Rising Consumer Demand Drives Marketization of the Healthcare Industry

The Debate on the Marketization of China's Healthcare Industry Has Always Existed.

Proponents of healthcare marketization argue that by drawing on market-oriented healthcare systems, exemplified by the United States, China can enhance the overall quality of its medical products and services, thereby optimizing the allocation of healthcare resources. In contrast, opponents of healthcare marketization contend that the government has long served as the central director of healthcare resource distribution in China, enabling resources to reach patients in need at a lower cost. They maintain that the public-welfare nature should be the primary attribute of healthcare, which currently best demonstrates the superiority of China’s healthcare system.

The debate continues, yet subtle shifts are already emerging in the market—various signs indicate that the marketization of China’s healthcare industry is no longer an optional choice, but an inevitable outcome driven by pressing demands.

First, for government departments, warnings of depleted medical insurance accounts have already emerged in many regions, making “cost containment” a Damocles’ sword hanging over the heads of healthcare-related authorities. Leveraging market-based mechanisms to encourage social capital and resources to enter the healthcare sector will undoubtedly significantly alleviate the fiscal pressures faced by the government.

An examination of the annual health yearbook published by the National Health and Family Planning Commission clearly reveals the growing strength of private capital. By the end of 2015, the number of private medical institutions had surpassed that of public ones, and this trend of “private sector expansion amid public sector contraction” continues to persist.

Meanwhile, China’s expanding middle class and the widely discussed phenomenon of “consumption upgrading” across various industries are profoundly reshaping the country’s healthcare sector. The strong investor enthusiasm for consumer-oriented medical services—such as dentistry, ophthalmology, and medical aesthetics—in the capital markets is a microcosm of this broader trend.

China’s tiered diagnosis and treatment system can be described as both a government-led initiative and an objective trend of the times. China’s healthcare industry also appears to have reached a similar tipping point: allowing patients with specific needs to pay out-of-pocket for high-quality medical resources, while the government ensures coverage for the public’s basic healthcare needs.

Whether in basic primary care or in highly specialized oncology; whether in the towering metropolises of Beijing, Shanghai, Guangzhou, and Shenzhen, or in third- and fourth-tier cities still undergoing gradual development, marketization in the healthcare industry is no longer confined to specific regions or services. It is a pervasive trend spreading across the entire sector.

VCBeat Research selected the two sectors where demand-driven marketization of the healthcare industry is most prominent—the maternal and infant care sector and the pharmaceutical distribution sector. By examining their development and evolution in 2017 through the lenses of free choice of resources and free choice of capital, we jointly explore the direction of marketization in China’s healthcare industry.

The Healthcare Industry Enters a New Era of Cross-Industry Competition

In 2017, the healthcare industry continued to capitalize on emerging opportunities, attracting many companies whose core businesses lay elsewhere to make strategic moves. Meanwhile, enterprises already deeply entrenched in the healthcare sector began extending their reach into various niche segments, pursuing diversified business models.

How will these forces drive the process of healthcare system reform in China? How will they impact the development of China’s healthcare industry? And how will they reshape the competitive landscape of China’s healthcare sector? In this report, we provide a detailed analysis of real estate developers, insurance companies, and internet giants entering the healthcare field, as well as the emerging trend of cross-industry competition driven by online healthcare providers establishing offline clinics.

Internet Giants' Moves in the Healthcare Sector in 2017

Analysis of Investment and Financing in the Healthcare Industry from January to November 2017

The healthcare sector is arguably the fastest-growing area for investment. From 2010 to the present, the annual compound growth rate of primary market investment in the healthcare sector has reached as high as 54.7%.

According to the VCBeat database, as of November 30 this year, there have been 402 primary market financing deals in China’s healthcare sector, with a total financing volume reaching RMB 37.7 billion. This investment scale is second only to that of the TMT sector.

As of November this year, financing in the healthcare sector has declined by nearly 20%. In fact, multiple sub-sectors have simultaneously shown signs of cooling investment interest.

The VCBeat database categorizes the healthcare industry into 16 major segments. Our analysis of this year’s investment and financing scale reveals that 14 of these sectors have experienced a cooling trend in investment activity, with the pharmaceutical, general health, and maternal and child health sectors showing the most pronounced declines.

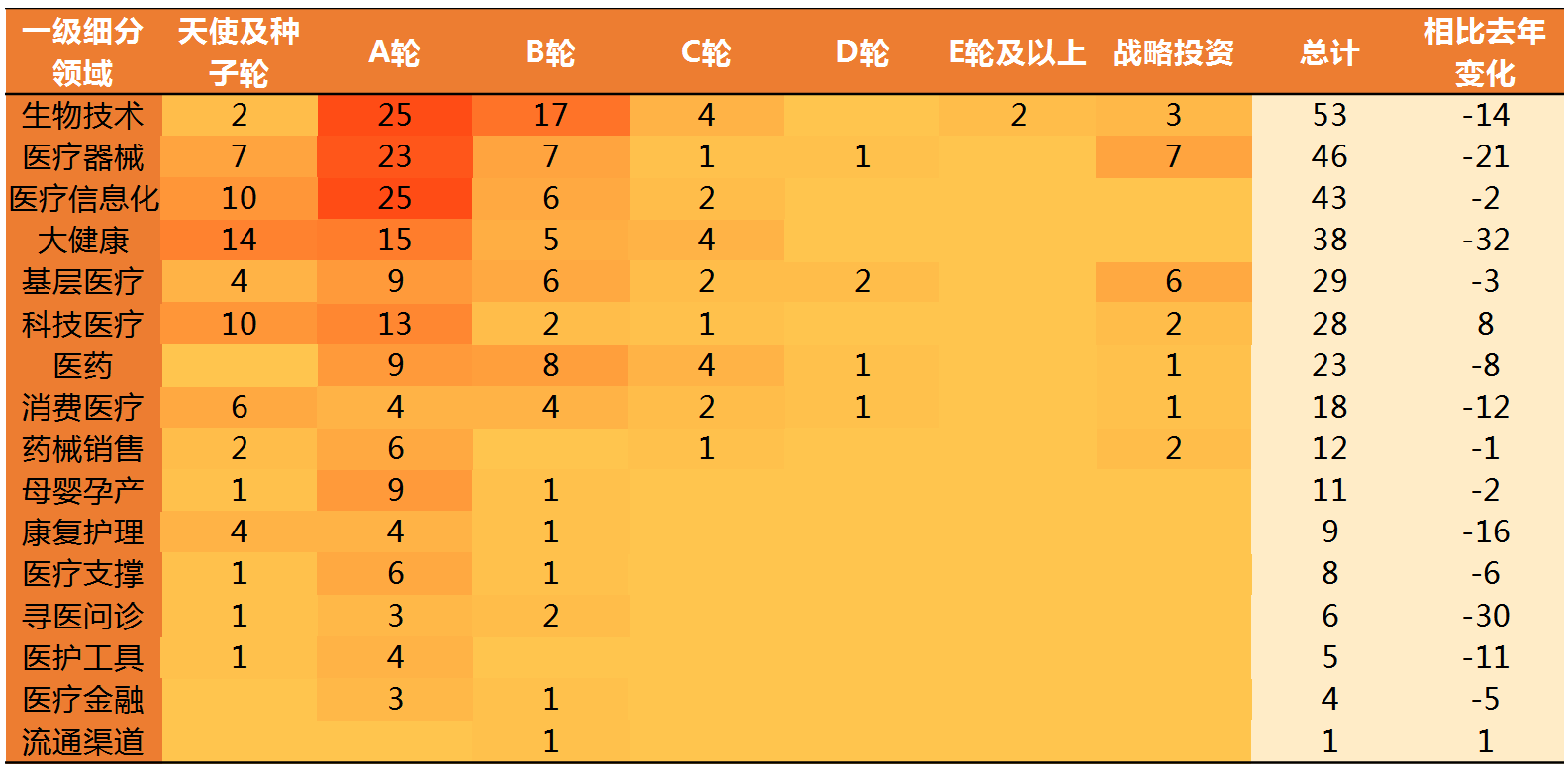

Distribution of Investment Rounds by Sub-sector in 2017

How to Obtain the Full Report:Scan the QR code below to become an official member of VCBeat and receive the complete electronic version of “A Data-Driven Glimpse into Healthcare: 2017 Competitiveness Report on the Medical and Health Industry.”