Data Insights: China's 2017 Future Healthcare 100 List

In December 2016, VCBeat launched the inaugural Future Healthcare Top 100 List (China List/Overseas List) for the global healthcare industry, quantifying its observations, insights, and understanding of innovation and entrepreneurship in the healthcare sector over the preceding three years.

It is our original mission in establishing the “Top 100 Future Healthcare Companies” list to identify Chinese innovative healthcare enterprises that truly represent the future of medicine, and to uncover the core forces driving China’s future healthcare industry.

This ranking, based on VCBeat’s valuation algorithms and database, identifies the top 100 “Future Healthcare” companies among non-listed enterprises (including those listed on the New Third Board) in China’s healthcare sector, ranked in descending order by market valuation and financing stage.

Two months ago, we once again launched the selection campaign for the “2017 Top 100 Future Healthcare Companies of the Year.”

During this period, we collected hundreds of corporate registration entries, obtained dozens of full-year investment datasets for 2017 from industry-focused investment institutions, and integrated over 5,000 records of the latest round of corporate financing data from the VCBeat database, ultimately compiling the “2017 Future Healthcare 100 – China List.”

On the evening of December 15, 2017, at the “2017 Top 100 Future Healthcare Companies” forum themed “The Era of Species Explosion,” VCBeat unveiled the list and presented medals to the listed companies.

This article aims to interpret the “2017 Top 100 Future Healthcare Companies in China” list, providing insights into the development landscape of the healthcare industry in 2017.

Statistical data reveals that the total valuation of companies listed on the “2017 Future Healthcare Top 100 China List” exceeded RMB 320 billion, representing a nearly 30% increase from the total valuation of the 2016 Top 100 list.

The valuation threshold for companies on the list reached RMB 800 million, an increase of RMB 360 million compared to 2016.

The total valuation of the top 10 companies on the list reached RMB 129.963 billion, an increase of RMB 19.563 billion compared to 2016.

As can be seen, the prestige of the 2017 Top 100 list has increased significantly, with both companies that were on the list last year and those newly added this year delivering more impressive performances.

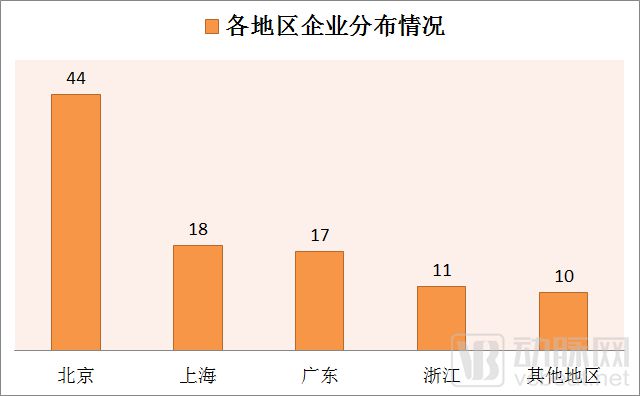

Beijing is the primary hub for listed companies, accounting for nearly half of the total with 44 enterprises. In the 2016 Top 100 list, Beijing-based companies were predominantly service-driven, including eight firms focused on online medical consultation and appointment scheduling. In contrast, the 2017 list shows a marked increase in technology-driven enterprises, with a significant emergence of genomics and medical artificial intelligence companies.

Shanghai, Guangdong, and Zhejiang exhibit a relatively balanced distribution of listed companies, with 18, 17, and 11 enterprises respectively, while other regions have significantly fewer listed entities. Among the 18 companies in Shanghai, there is a substantial proportion of biogenetic firms, attributable to the region’s abundant pool of professional talent. As a frontier province for the internet industry and geographically proximate to Shanghai, Zhejiang is predominantly dominated by internet healthcare and genetic biotechnology enterprises. Guangdong, as a hub for high-tech industries, primarily hosts technology-driven enterprises.

The most active capital behind the listed companies is almost entirely from well-known investment institutions. These prominent firms often invest in high-potential startups, which, after several years of development, typically evolve into industry-renowned enterprises. Many have even become unicorns with exceptionally high valuations.

Among the top 10 most active investment institutions in our statistics, Matrix Partners China invested in the highest number of listed companies, reaching 11. The lowest number was 5 listed companies, with four investment institutions falling into this category: IDG Capital, Zhongwei Fund, Legend Capital, and ZhenFund.

It is worth noting that these figures primarily reflect the cumulative outcomes of years of strategic positioning by these investment institutions, rather than real-time feedback from 2017.

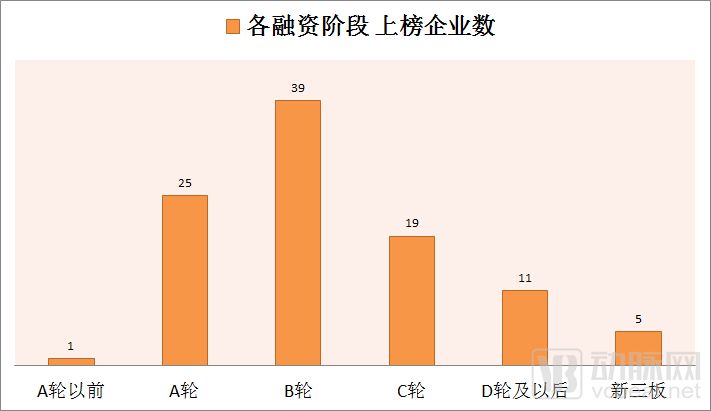

Among the listed companies, those in Series A and Series B financing rounds dominate, totaling 64.

Companies prior to Series A financing have largely faded from the Top 100 rankings due to their early stage and low valuations. As the industry continues to advance, it is unlikely that future early-stage companies will have significant opportunities to make the list.

Among them,AThe participating enterprises include25Home.ACompanies at this funding stage are still in their early development phase; making the list indicates that they have identified a viable business model, thereby securing substantial investment.

From a business sector perspective, technology-driven enterprises represented by genetics, biopharmaceuticals, artificial intelligence, and medical devices accounted for more than half of the share. This aligns closely with the overall trend in 2017 that “high technological barriers equate to high financing amounts.”

It is worth noting that United Imaging Healthcare, which tops the list, was also at the Series A stage. In September 2017, the company secured RMB 3.333 billion in Series A financing, marking the largest single private equity investment in China’s medical device industry and emerging as the biggest dark horse on this year’s list. With the further advancement of import substitution for medical devices and the intelligent upgrading of imaging equipment driven by the deep integration of medical imaging and artificial intelligence, we highly anticipate United Imaging Healthcare’s future performance.

Most service-driven companies listed in Series A financing adopt a B2C business model, such as pharmaceutical e-commerce and consumer healthcare. In contrast, for service-oriented enterprises with a B2B business model, the viability of their model typically becomes evident only after Series B; valuations at the Series A stage are generally modest.

BNumber of companies from this round that made the list reached39Home, is the category with the highest proportion of companies on the list. ByBAt this funding round stage, the company’s business model has been preliminarily validated, and its operational capabilities have become largely stable; valuations for companies at this stage typically experience exponential growth.

Among the sectors listed, medical artificial intelligence has seen the most significant growth in valuation. Infervision, TomoDeep, and Huiyi Huiying all reached Series B financing in 2017, with each securing over RMB 100 million. Compared to 2016, their valuations increased substantially.

Genetics companies emerged as the strongest cohort among Series B enterprises, with nine firms at this stage. Novogene and BGI Genomics ranked in the top 10, with valuations of RMB 10 billion and RMB 8 billion, respectively.

CCompanies at the Series B round and later stages undoubtedly constitute the group with the highest valuation share on the list, with a total valuation exceeding1200billion yuan, ranking among the top10of5Chair.

Companies at this stage are primarily aiming for an initial public offering (IPO). Most have been established for over five years, with many exceeding ten years. Relatively speaking, their core businesses are not in emerging sectors; rather, they feature mature business models that have achieved substantial revenue or even reached break-even. Dominant players include medical informatics companies and comprehensive platforms that originated from online physician consultation services.

Based on the statistics in the table above, we arrive at the following results: there are 51 service-driven enterprises with a total valuation of RMB 170.88 billion, and 49 technology-driven enterprises with a total valuation of RMB 149.253 billion. [There is an overlap between the two types of enterprises (the total number of enterprises counted in the table exceeds 100), so the classification is primarily based on their focus in business models.]

An analysis of the sectors represented by the listed companies largely aligns with the current industrial landscape of healthcare innovation and entrepreneurship in the primary market: although service-driven enterprises command higher overall valuations—with comprehensive platforms offering medical consultation services still boasting the highest total valuation of RMB 72.88 billion—technology-driven enterprises, represented by innovative medical devices, genomics, and artificial intelligence, experienced more rapid growth in 2017.

Based on this data, the following trends can be identified:

1. Comprehensive platforms offering medical consultation and diagnosis services dominate the rankings, primarily driven by leading players such as WeDoctor, Ping An Good Doctor, Haodf Online, and Chunyu Doctor. The combined valuation of these four platforms reaches RMB 55.3 billion. Resources in this sector are increasingly concentrating among top-tier platforms, further squeezing the development space for small and medium-sized enterprises;

2. If BGI Genomics and Berry Genomics had not gone public in succession in 2017, the genomics sector would have topped the list in both the number of companies and total valuation. The performance of genomics companies in 2017 was remarkable, with firms such as Annoroad Gene Technology, Personal Biotechnology, and 3D Medicines securing substantial financing and essentially reaching the IPO stage. Import substitution for gene sequencers has also been gradually achieved this year, with domestically developed third-generation sequencers being introduced one after another, all of which point to a promising outlook for the genomics industry. If we are to predict the most valuable sector in future healthcare, the genomics industry is the most likely candidate.

3. Compared with the previous year, AI companies made remarkable progress on the 2017 list, with six companies included and a total valuation exceeding RMB 15 billion. The listed companies are all star players in the field of medical AI, having secured substantial financing and reached Series B stage. However, beneath the surface prosperity, a more sober perspective on medical AI is warranted. It is undeniable that AI algorithm models have matured and clinical practice has yielded favorable feedback; nevertheless, policy guidance, as well as compliance, legality, and standardization of data, remain constraints impeding further industry development. Moreover, although industry leaders have reached Series B, the sector as a whole still lacks mature monetization models. These are the challenges that medical AI companies will need to confront in 2018.

4. Amid the trend of import substitution for medical devices, United Imaging Healthcare has emerged as the most prominent dark horse in the innovative medical device sector, topping the rankings with a valuation of RMB 33.333 billion. This year, other high-quality companies in this field, including Anhan Medical, Sinovision, and Langrun Medical, have also secured substantial financing rounds. It is evident that, driven by the rapid development of artificial intelligence, imaging equipment closely integrated with AI is attracting increasing capital attention, indicating significant potential for the intelligent transformation of medical devices.