Decoding a Decade of Healthcare Investment Trends: Insights into Hospital Innovation and Development

“2017 Future Healthcare Top 100” Forum, themed “The Era of Species Explosion,” was held at the Beijing Marriott Hotel from December 15 to 17, 2017.

Leveraging the release of the “Top 100 Future Healthcare Companies” list and its series of annual awards, this conference brought together the most dynamic healthcare startups, investment and financing institutions, and professional medical organizations from both China and abroad. It also hosted multiple parallel forums focusing on annual hot topics such as intelligent imaging, smart medical devices, maternal and child health, and hospital innovation.

As a partner organization for the “Top 100 Future Healthcare Companies” list and the “2017 Competitiveness Report on the Medical and Health Industry,” Zero2IPO Capital participated in the conference throughout its duration.

At the conference, Yu Jurong, Partner at Zero2IPO Capital, delivered a keynote speech titled “A Decade of Healthcare Investment Data: Perspectives on Innovative Development in Hospitals.” She shared insights on why hospital innovation is crucial, the impact of healthcare investment on hospitals’ innovative development, and future trends in investment in hospital innovation.

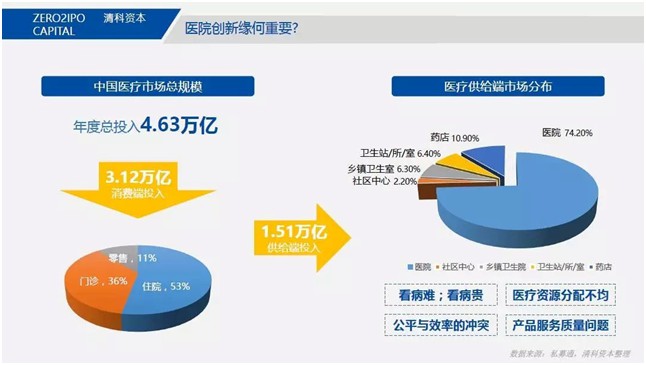

Why Is Hospital Innovation Important?

According to statistical data, the total size of China's healthcare market has reached RMB 4.63 trillion, with a 2:1 ratio between consumer-side and supply-side investments. From the consumer perspective, nearly 90% of diagnosis and treatment activities take place in hospitals; from the supply side, hospitals remain the dominant providers.

Relevant data indicate that 28,000 hospitals handle over 75% of outpatient and inpatient demand. The challenges of “difficult and expensive access to medical care” remain prominent, with persistent issues including uneven distribution of medical resources, conflicts between equity and efficiency, and concerns regarding the quality of products and services. As the core of the healthcare system, hospitals must enhance their management, operational capabilities, and clinical service standards; thus, hospital innovation is imperative.

Does Medical Investment Fuel Innovation and Development in Hospitals?

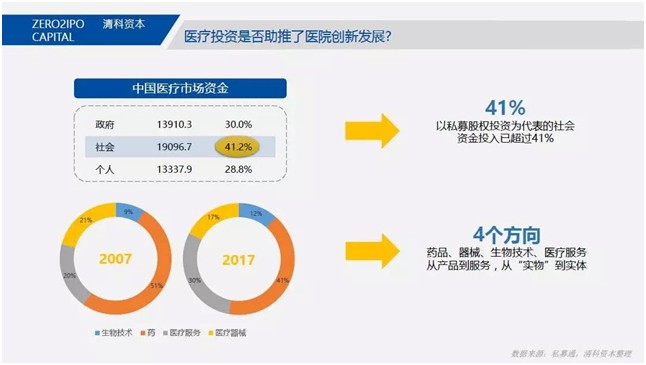

Funding for the healthcare market primarily comes from three sources: government investment, social capital, and individual investment. Among these, social capital, represented by private equity (PE) investment, has accounted for over 41% of healthcare spending, becoming a significant force in healthcare development. (It is worth noting that the healthcare investments mentioned below refer specifically to healthcare private equity investments. Although disclosed investment events constitute a small proportion of total social healthcare investment, they have had a certain impact on promoting healthcare innovation, which may increase as policies are further liberalized.)

Healthcare investment primarily focuses on four key areas: pharmaceuticals, medical devices, biotechnology, and healthcare services.

From 2007 to 2017, the proportional distribution among these four investment categories remained relatively stable. The share of investments in pharmaceuticals and medical devices declined, while that in healthcare services and biotechnology increased. The developmental trend has evolved from initial investments in “tangible” hospital-based products to broader investments in healthcare “entities.” As capital participation in healthcare innovation policies has gradually opened up, investment strategies have shifted from indirect to direct investment. To a certain extent, healthcare investment and hospital innovation mutually influence each other.

A Decade of Healthcare Investment: Entering a Phase of Rational Growth

Over the past decade, annual investment in the healthcare sector grew nearly ninefold, from $500 million to $4.4 billion;

The number of investment cases increased from 82 to over 580, representing a more than sevenfold growth;

The number of participating investment institutions grew from 69 to 413, representing a more than sixfold increase;

The amount of a single investment has doubled, rising from $6.5 million to $7.5 million.

Notably, there were nine financing deals exceeding $100 million in 2017, which raised the average investment amount per deal; for the remaining healthcare projects, the average financing ranged from RMB 20 million to RMB 30 million.

Healthcare Investment: Three Stages Over a Decade—Exploration, Acceleration, and Return to Rationality

In 2007, Chen Zhu was appointed Minister of Health; Legend Capital invested in its first healthcare project, Pharmaron; SAIF Partners recruited clinical physicians from Peking Union Medical College Hospital; and IDG assembled professionals specializing in immunology and pharmacology.

Qiming Venture Partners, Morningside Venture Capital, Eli Lilly and Company, Sequoia Capital, China Everbright Group, CDH Investments, Matrix Partners China, Fidelity Asia, Oriental Fortune Capital, Shenzhen Capital Group, JD Capital, Cowin Capital Group, Fortune Capital, and GTJA Capital, among other renowned institutions, also began venturing into healthcare investments. In the subsequent years, they strengthened their healthcare investment teams, thereby ushering in a new era of healthcare investing.

At this stage, investments remain primarily focused on pharmaceuticals, medical devices, and related products.

The first batch of outstanding CRO companies has gained capital recognition, with increased investment in informatization directly related to hospital innovation, while independent medical service institutions, represented by health check-up centers, have begun to emerge.

Representative CROs include WuXi AppTec, Tigermed, and Pharmaron.

Representative companies in the informatization sector include Jiahe Technology, Tianjian, and Lanweitong.

Representative healthcare service providers include physical examination institutions such as iKang Guobin, Ciming, and Meinian Onehealth.

Primarily driven by the dual forces of policy and technology. Policy-driven growth stems from healthcare reform entering its second development phase, which encourages capital investment in private healthcare and reforms in public healthcare. Technology-driven growth arises from the dividends of mobile internet development and the rapid advancement of biotechnologies, represented by biologics and sequencing.

Medical investment blossomed during this phase, with internet healthcare shining brightly, while sequencing, diagnostics, and biopharmaceuticals began to emerge and grow rapidly. A surge of new investment firms entered the healthcare sector, ushering in a new dawn for this previously understated industry.

The first wave of major healthcare investors began to fragment and upgrade, with a new cohort of healthcare funds—represented by Honghui Capital and Jifeng Capital—being established, becoming more active and diversified.

Representative internet healthcare platforms during this phase include Chunyu Doctor, Haodf Online, DXY, and WeDoctor.

Representative companies in the biotechnology sector include Berry Genomics and Annoroad, among others;

Representative biopharmaceutical companies include Beta Pharma and Innovent, among others;

Medical service representatives include Wuhan Asia Heart Hospital, Hanxi Medical, Kyoto Children's Hospital, and Ear Era.

Investment amounts have not declined, but the pace of project investment has slowed. The internet healthcare sector has cooled rapidly, while practitioners in specialty and primary care have gained recognition. Investment themes continue to follow the precision medicine trend, with medical AI emerging as a new hotspot.

Primary care initiatives such as Mingyi Zhonghe and Xinkang Medical;

The precision medicine sector is beginning to diverge, with a pronounced "winner-takes-all" effect among sequencing companies, while product-focused firms are seeking the next major direction beyond NIPT. Representative companies include Annoroad Gene Technology, Burning Rock Biotech, Geneseeq Technology, Subo Medical, and ClearMed.

Representative medical AI projects include Infervision and LinkDoc Technology.

For more project information, please refer to the “2017 Future Healthcare 100” list released by VCBeat.

Major healthcare investment institutions are encouraging medical teams to raise funds independently, providing professional teams with greater room for development. New specialized healthcare investment firms have become more active, contributing fresh momentum to the healthcare market. These include Yahui Precision Medicine Fund, Chende Capital, Mifang Capital, Tonghe Yucheng, Yuanyi Capital, Boxing Capital (formerly Qingkong Yinxiang), Anlong Fund, and Fenxiang Investment.

Listed companies, government-guided funds, securities firms, banks, state-owned capital, and real estate entities have deepened their penetration into the market as off-exchange investors. By participating as limited partners (LPs), investing through funds of funds (FOFs), or making direct investments, they have provided a substantial capital pool for the healthcare sector, driving its rapid development.

A Decade of Change in Healthcare Investment: Perspectives from M&A and IPOs

Mergers and acquisitions (M&A) have been the fastest-growing sector over the past decade. The annual M&A transaction value increased 400-fold, rising from RMB 140 million to RMB 56 billion. The number of M&A deals grew 46-fold, from 5 to 228 transactions. The average deal size increased from RMB 28 million to RMB 246 million. By industry segment, M&A activity was distributed as follows: pharmaceuticals > medical devices > healthcare services > biotechnology. M&A activities are expected to continue expanding in the future.

In 2017, the number of IPOs reached a new high of 52, with total funds raised exceeding RMB 27 billion, representing a more than fourfold increase. In terms of industry distribution, pharmaceuticals remained the most represented sector, while biotechnology demonstrated strong performance this year. The majority of IPOs were still listed domestically in China.

Recently, the Hong Kong Stock Exchange announced that it would accept listing applications from biotechnology companies that are not yet profitable or have no revenue, which is a significant positive development for IPOs in Hong Kong.

How to View Hospitals’ Innovative Direct Investments?

Hospital innovation should be analyzed from both internal and external perspectives. Internally, there are two primary directions: enhancing management and operations, and improving clinical diagnosis and treatment capabilities. Specifically, operational efficiency should be boosted through informatization and diversified payment models, while clinical care should be elevated by strengthening both hardware infrastructure and soft power.

The development of management informatization has gone through three stages:

- A management system centered on personnel, finances, and materials;

Second, an electronic medical record system based on clinical care pathways;

Third, specialty-specific diagnosis and treatment systems based on big data and AI technologies are developing rapidly.

In recent years, at least 20 healthcare investments have been directed to this sector annually, with a trend toward increasing capital allocation.

The primary benefit of payment diversification lies in optimizing cost structures. Public health insurance is gradually transitioning into a phase of cost containment through Diagnosis-Related Groups (DRGs) for single diseases. Meanwhile, the development of commercial health insurance is being intensified, and medical investment interest in health insurance innovation continues to rise, with projects such as Shuidi Huzhu and Xiao Yusan receiving sustained funding.

In terms of hardware upgrades for clinical diagnosis and treatment, the trend toward miniaturization and intelligence of medical devices is evident, with investment cases growing at an annual rate of 5–10%. Meanwhile, service upgrades are even more critical for in-hospital innovation, characterized by finer specialization, enhanced service awareness, and the rise of physician and nursing groups. However, the number of investments in physician groups has declined over the past two years, while investments in in-hospital specialty operations combined with out-of-hospital implementation services have recently shown an upward trend.

Innovation beyond hospital walls, ranging from telemedicine to medical consortia, has fostered tighter horizontal and vertical inter-hospital connections, creating feasible conditions for the implementation of policies supporting independent third-party services. From an investment perspective, projects in telemedicine, internet-based healthcare, and third-party service centers have secured capital support, whereas investment in medical consortia remains relatively cautious due to their non-profit nature.

Future Visions on Innovative Investment Opportunities in Hospitals?

Drawing on the development trajectory of the healthcare industry abroad and trends in consumption upgrading, hospital innovation is likely to undergo a shift from being hospital-centric, to physician-centric, and ultimately to patient-centric. This transition will further optimize the allocation of medical resources, accelerate the development of primary care, and drive hospital innovation through the combined forces of technological advancement and humanistic care.

We are optimistic about opportunities in sectors driven by the dual forces of policy and technology. From a policy perspective, we favor opportunities in primary care and specialized medical services. The downward referral of patients from urban hospitals is driving increased demand for diagnosis and treatment at the primary care level. We maintain a long-term positive outlook on primary healthcare services, which will develop through a hybrid model combining online IT solutions with offline services.

The vigorous implementation of the “Two-Invoice System” and the “Zero Markup” policy has promoted the integration and upgrading of circulation markets for pharmaceuticals, diagnostic devices, and other medical products. Meanwhile, the development of specialized services—represented by cardiology and cerebrovascular care, ophthalmology, dentistry, nephrology, and audiology—as well as third-party laboratory testing platforms, is becoming a powerful support in the development of primary healthcare.

From a technical perspective, we are optimistic about the development of biotechnology and AI-driven medical big data. We maintain long-term focus on high-quality enterprises in fields such as precision diagnosis and treatment, medical intelligence, and big data. Simultaneously, we place particular emphasis on nursing and psychological care sectors that are resistant to AI displacement. Although personalized specialty service management faces significant operational challenges and offers limited short-term returns—making it prone to being overlooked by investment institutions—teams with accumulated experience and long-term strategic preparation in this domain deserve close attention.

Finally, we extend our gratitude to VCBeat for the invitation and for providing this platform, and to the Zero2IPO Private Equity Database for its data support. Covering the two broad themes of healthcare innovation and healthcare investment, this presentation offers a representative overview; any omissions or inaccuracies are inevitable, and we sincerely invite industry professionals to bear with us and offer corrections. Moving forward, Zero2IPO Capital will continue to collaborate with VCBeat in conducting research and analysis, providing detailed breakdowns of data and information across healthcare subsectors for shared insight.