Medical Health Investment Sees 54.7% CAGR Despite 2017 Dip; Tech-Driven Segments Gain Favor

VCBeat’s 2017 Annual Report, “A Data-Driven Glimpse into Healthcare: 2017 Competitiveness Report on the Medical and Health Industry,” was officially released on December 15 at the Top 100 Future Healthcare Forum.

From 2011 to 2016, internet healthcare passed through several key growth milestones of an emerging industry. These included the disruptive innovation in 2011 when Chunyu Yisheng (Spring Rain Doctor) first launched its mobile consultation services, the industry’s explosive growth during the capital investment boom in 2014, and the subsequent downturn in both the industry and capital markets from 2015 to 2016, driven by the end of the traffic dividend era.

Starting from the field of healthcare industry innovation, VCBeat has analyzed corporate operational data and investment/financing data to innovatively establish a quadrant model that visualizes the operational status of companies in these sectors and maps out the current competitive landscape. With this model, we can more conveniently observe the operational realities of enterprises within specific sub-sectors, making our research findings easier to comprehend. In this report, while interpreting the model, VCBeat also examines the changes and developments in the healthcare sector over the past year from the perspectives of productivity, production relations, and factors of production.

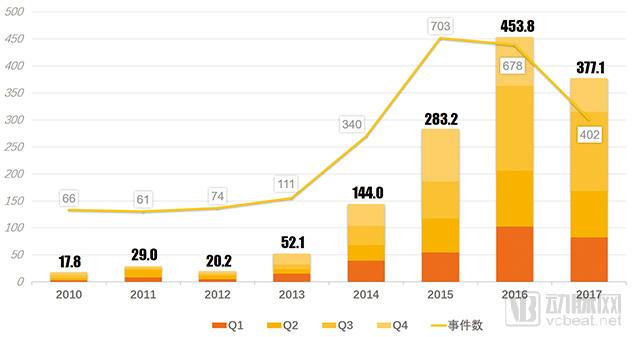

Meanwhile, VCBeat also analyzes the development of startups in the healthcare sector based on investment and financing data. The healthcare sector can be described as the industry with the fastest investment growth. From 2010 to the present, the annual average growth rate of primary market investment in the healthcare sector has reached as high as 54.7%, but this trend changed in 2017.

According to the VCBeat database, as of November 31 this year (the report was completed on December 10, and the full-year 2017 investment and financing data will be released soon), China’s healthcare sector recorded 402 primary-market financing rounds, with a total funding volume of RMB 37.7 billion. This investment scale ranks second only to the TMT sector.

Historical Investment and Financing Data in the Healthcare Sector, Compiled by VCBeat

I. The Industry Gradually Matures, and Investment Becomes More Rational

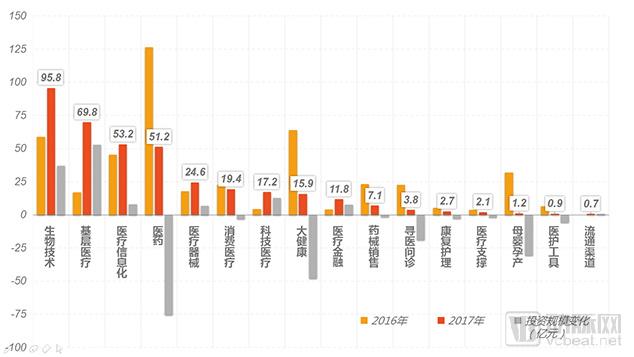

Changes in Investment Scale Across Subsectors of the Healthcare Industry in 2017, Compiled by VCBeat

As of November this year, financing in the healthcare sector has declined by nearly 20%. In fact, multiple sub-sectors have simultaneously shown signs of cooling investment interest.

VCBeat Database categorizes the healthcare industry into 16 major segments. Our analysis of this year’s investment and financing scale reveals that 14 of these sectors have experienced a cooling trend in investment activity, with the pharmaceutical, broader health, and maternal & child care sectors showing the most pronounced declines.

Taking the pharmaceutical sector as an example, the tech boom in recent years made it a favorite among investors. However, with the emergence of technological monopolies, investment driven by technological innovation in this sector has seen its market scale shrink by nearly 60%. This implies that early movers in related industries, leveraging their prior investments, have established formidable technical barriers. Since technology investment is largely a one-time expenditure, once competitive advantages are secured through technological means, the position of these pioneers becomes difficult to challenge. It is predictable that, absent breakthrough advancements in pharmaceutical technology in the future, the cooling trend in market financing will continue to intensify.

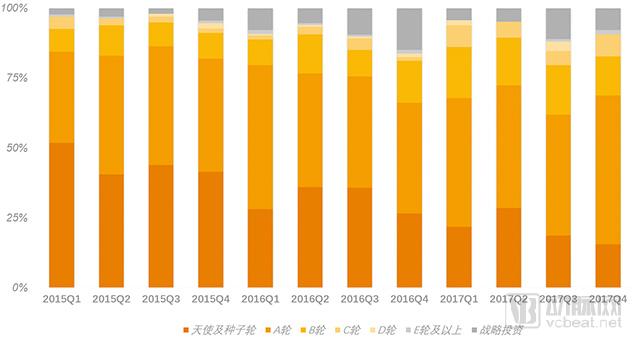

From the perspective of changes in investment rounds, there has been a clear downward trend in early-stage financing dominated by angel and seed rounds from 2015 to the present.

Proportion of Investment Rounds from Q1 2015 to Q4 2017, compiled by VCBeat.

Investment Scale and Number of Investment Events in Various Sub-sectors of the Healthcare Industry in 2017, Compiled by VCBeat

In 2015, angel and seed-stage financing deals accounted for up to 50% of all investment transactions during that period. Currently, however, these early-stage rounds represent only about 15%. In contrast, the more mature Series A round has gradually become the primary stage for investment activity. This shift indicates that the healthcare industry has experienced significant growth driven by investment capital; many sectors now boast sufficiently strong companies, reducing investors’ need to devote substantial resources to nurturing new ventures.

II. Technology-Driven Sectors Are More Popular Than Consumer-Driven Sectors

In terms of investment interest across specialized sectors, areas with certain technical barriers, such as medical devices and biotechnology, have attracted relatively high levels of investment. In contrast, sectors driven by service model innovation, such as maternal and infant care and online medical consultation, have seen declining investment interest. Taking online medical consultation as an example, there were 46 financing deals in 2016, whereas only seven investment transactions occurred through November 30, 2017.

In the field of service innovation, compared to the technology sector, industries are more mature, product homogenization among enterprises is severe, entry barriers are low, and products can be easily replicated. Companies can achieve rapid growth through capital injection; however, once industry giants emerge, the homogenized products and services make it difficult for smaller players to survive. After two years of development, consumer-driven service sectors may have already established a certain degree of monopoly. If new companies in these sectors fail to break through, the cooling trend in the capital market is likely to continue.

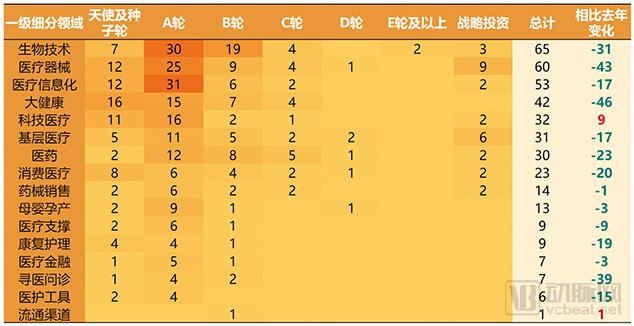

Biotechnology and Medical Devices Sectors Record the Highest Number of Transactions

Distribution of Investment Rounds by Sub-sector in 2017, Compiled by VBInsight

Among the 15 investment subsectors, biotechnology and medical devices recorded the highest number of transactions, accounting for more than 30% of total financing events. Primary healthcare and pharmaceuticals were the most sought-after sectors, exhibiting the fastest growth; meanwhile, investment enthusiasm in healthcare informatization declined most rapidly.

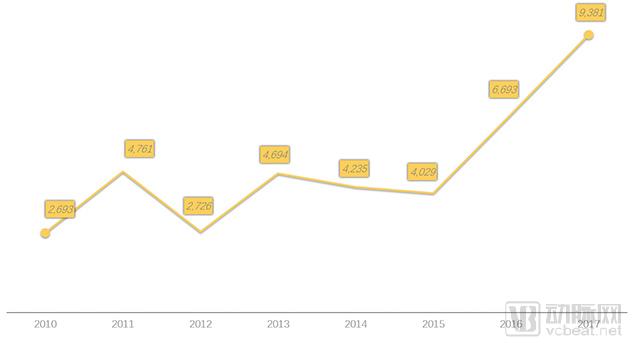

Significant Increase in Average Investment Amount and Rising Investment Concentration

Changes in Single-Transaction Financing Amounts from 2010 to 2017, Compiled by VCBeat

Although both the number of investment deals and the total investment amount in China’s healthcare sector declined this year, the upward trend in average deal size remained unchanged.

Compared with 2015, the average amount per investment this year is close to RMB 93.81 million, more than double that of 2015. The rise in average investment size indicates an overall increase in industry maturity. Capital market investment strategies have shifted from a previous “spray-and-pray” approach to a current focus on concentrating resources on high-potential projects.

On the other hand, the frequent emergence of large-scale investments is also a characteristic of the capital market in the healthcare sector this year.

2017 Top 10 Investments (the last two tied for 10th place)

United Imaging Healthcare Secures RMB 3.333 Billion in Series A Financing, Marking the Largest Primary Market Funding Round in China’s Healthcare Sector to Date. Benefiting from Policy Liberalization, More Than Four Companies in the Grassroots Healthcare Segment Were Listed, with Financing Scale Reaching a Historic High for the Sector.

For more detailed analytical reports, please scan the QR code below to purchase, or become a VCBeat member.

Scan the QR code above to purchase the full report for 499.

Scan the QR code below to become an official VCBeat member and gain free access to all reports from VCBeat Eggshell Research Institute!