Three-Year Analysis of Healthcare Industry Funds: Nearly 160 Funds Target Over RMB 240 Billion in Fundraising, with Some Already Deployed

It has become a hot topic in healthcare investment in recent years for listed companies to lead the establishment of industrial funds or participate in their operations.

This approach offers significant advantages. For listed companies, investing through industrial funds can diversify investment risks and mitigate the impact on the performance of the listed entity. Meanwhile, industrial fund investments typically focus on the supply chain surrounding the listed entity, thereby providing a reserve of high-quality resources for the company’s future development.

For the professional asset management firms and government-guided funds involved, this has achieved capital aggregation and a resource leverage effect. Hence, listed companies’ participation in industrial investment funds has gained significant popularity in recent years.

VCBeat (WeChat ID: vcbeat) has compiled data on healthcare industry funds from 2015 to 2017, aiming to analyze the logic and trends of medical investments from perspectives such as participating entities, investment sectors, and investment scale.

Number of Issues Slightly Increases, Proposed Fundraising Amount Rises 70% Year-on-Year

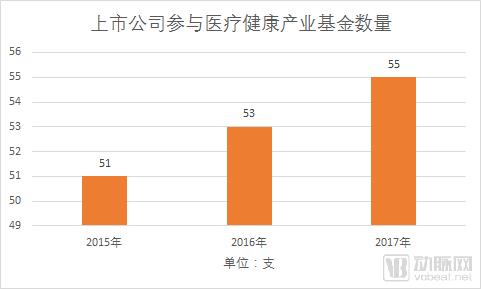

We compiled data on industrial funds for three consecutive years from 2015 to 2017 and found that the number of industrial funds initiated or participated in by listed companies remained relatively stable over this period, while the target fundraising amounts exhibited significant fluctuations.

In 2015, the number of healthcare industry funds involving listed companies was 51; it rose to 53 in the following year and reached 55 in 2017.

The above data indicate that,Listed companies’ enthusiasm for participating in healthcare industry funds has been continuous, becoming an industry “norm.”

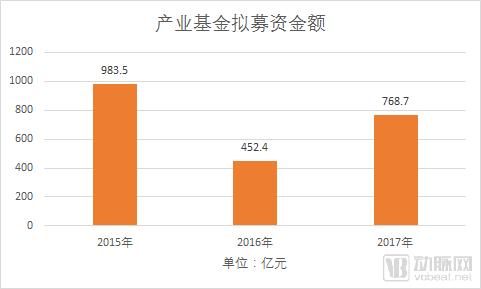

Let’s revisit the data on changes in the target fundraising amount for industrial funds.In 2015, the figure stood at RMB 98.35 billion; it dropped to RMB 45.24 billion the following year, and then rose to RMB 76.87 billion in 2017. The chart exhibits a typical “V”-shaped pattern.

Overall, listed companies initiated or participated in nearly 160 healthcare industry funds between 2015 and 2017, with a proposed fundraising amount exceeding RMB 240 billion.

Generally, the capital raised by industrial funds is not secured in a single lump sum; instead, it is raised in tranches aligned with the project development cycle.

Following the initial fundraising in 2015, the industrial fund began identifying and investing in high-quality targets, with this deployment phase occurring in 2016.

While making co-investments in the inaugural fund, fundraising for a new round of funds was simultaneously underway; the overlap of these two activities led to a reduction in the planned fundraising amount for industrial funds in 2016. By 2017, the fundraising scale began to recover, with the planned fundraising amount projected to decline again in 2018. This pattern reflects the cyclical nature of industrial funds.

Analysis of 2017 Healthcare Industry Fund Data

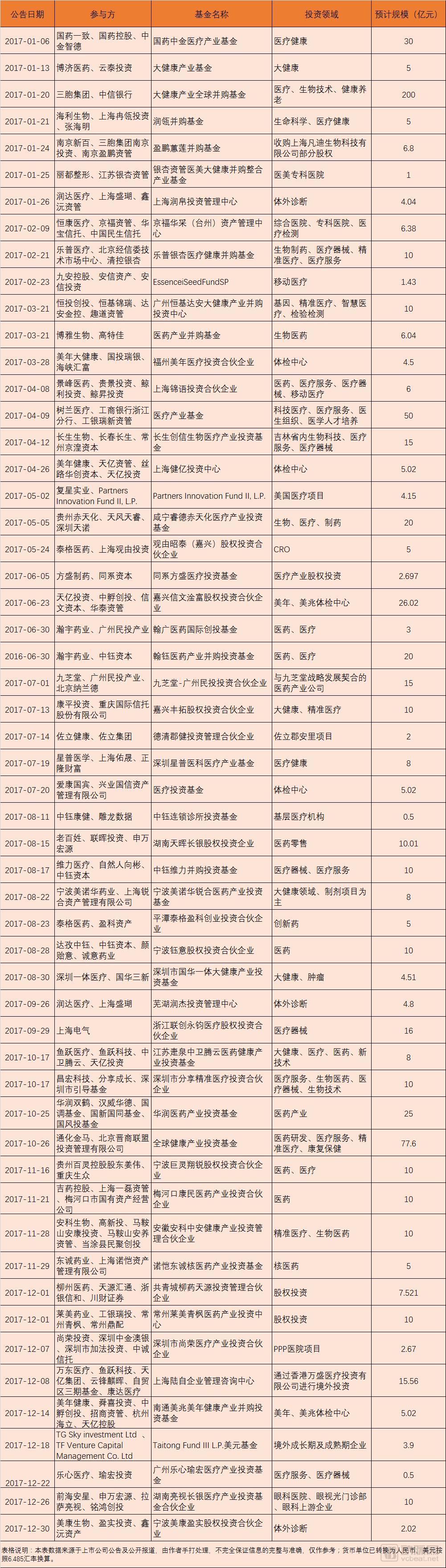

By reviewing announcements and public information from relevant listed companies, VCBeat has compiled data on healthcare industry funds in 2017, as shown in the attached table:

Before delving into the 2017 industrial fund data, let us first review the overview of industrial funds. In a broad sense, a fund refers to a pool of capital aggregated for a specific purpose. A healthcare industry fund is a specialized asset management entity established exclusively to capitalize on investment opportunities within the healthcare sector.

The typical structure of an industrial fund involves the establishment of an independent limited liability company by relevant entities to serve as the fund management company, followed by the formation of a limited partnership. The limited liability company acts as the general partner (GP) of the partnership, while other participating entities contribute capital as limited partners (LPs). In terms of participants, government bodies, corporate legal entities, securities firms, and others can serve as primary sponsors or managers.

The operational process of a fund is generally divided into three phases: early, middle, and late. The early phase involves the convening of managers and investors, capital contribution, and determination of the management structure. The middle phase covers project sourcing, investment decision-making, and portfolio management. The late phase focuses on exit and realization of returns, typically through initial public offerings (IPOs), mergers and acquisitions (M&A), or share buybacks.

Of course, during the fund’s operation, there are also issues related to finance, legal affairs, due diligence, and so on, which will not be elaborated here.

Below, we focus on analyzing the relevant situation of healthcare industry funds in 2017. First and foremost,Who is the initiator?issues. Based on our analysis, the following scenarios are generally observed:

Wholly Owned by Listed Companies.Publicly listed companies establish fund management firms and inject their own idle funds into the fund pool. Generally, such funds are not large in scale, and the projects they invest in are directly related to the core business of the initiating entity. For example, Zuoli Health, a wholly-owned subsidiary of the publicly listed company Zuoli Pharmaceutical, jointly established a health industry M&A fund with its affiliate, Zuoli Group. The purpose was to meet the development needs of its Jun’anli project.

Joint Venture System.Specifically, professional asset management institutions, listed companies, and their controlled subsidiaries jointly establish joint ventures, which then initiate fund-raising plans; both the asset management institutions and the listed companies subscribe to a certain portion of the shares. The collaborations between Lidu Plastic Surgery, Lepu Medical, and Yinxing Asset Management, as well as between HanYu Pharmaceutical, Weili Medical, and Zhongyu Capital, fall into this category.

Partnership Structure.This business model is characterized by multiple listed companies, asset management firms, banks, and government entities serving as investors in the fund, with structural tranching among these investors into senior, mezzanine, and junior/equity tranches. Collaborations involving Changhong Technology with the Shenzhen Government Guidance Fund and Fenxiang Chengzhang, as well as those involving China Resources Double-Crane Pharmaceutical, Hanwei Huade, Guotiao Fund, Guoxin Guotong Fund, and China Venture Capital Fund Corporation, fall under this category.

Both the joint venture company structure and the partnership structure are established through limited liability companies or partnerships, respectively. The key differences lie in the composition of general partners and the decision-making mechanisms within partnerships. The joint venture company model involves fewer participating entities, whereas the partnership model is more suitable for multi-party participation, particularly in funds involving government guidance funds, featuring more standardized organizational structures, capital contribution methods, and decision-making processes.

In addition, there are other models, such as capital contributors entrusting professional asset management firms to manage the fund, or conglomerates establishing asset management subsidiaries to centrally oversee the group’s investment activities.

In terms of organizational structure, there are more funds established as limited partnerships. In 2017, the number of such funds was 32, followed by 11 joint venture companies, 6 wholly-owned subsidiaries of listed companies, and 6 other types.

Although collectively referred to as healthcare industry funds, there are certain differences in their specific investment directions.Generally, foundations involving listed companies focus on areas related to the core business of the listed company., for example, Meinian Onehealth raised multiple funds to support the construction of Meinian and Meizhao health examination centers.

Projects involving government-guided funds are often aligned with the local pharmaceutical industry’s development needs., for example, the Shenzhen Government Guidance Fund targets the precision medicine sector, while Anhui Ma’anshan Anyang Asset Management and Dangtu County Minjuchuang focus on the elderly care and biopharmaceutical sectors.

In addition, our comparison of healthcare fund data from 2015 to 2017 reveals that,Government-guided funds, or the “national team,” are increasingly participating in healthcare and medical funds.In 2015, only two or three funds had participation from government guidance funds; by 2017, approximately ten funds were associated with government guidance funds. This indicatesThe government is transforming its fiscal investment approach, expanding from the previous model of providing land and policy incentives to deep financial participation, with growing recognition of industrial funds.Government participation in industrial funds enables the steering of investment directions and the planned stimulation of regional economic development; this approach is also applicable beyond the healthcare sector.

In terms of the initial fund size, the range of RMB 500 million to RMB 2 billion is the most suitable scale for industry funds. At this scale, funds can participate in angel investments in start-ups as well as strategic and financial investments, thereby achieving broad coverage.

The largest industrial fund disclosed in 2017 was the Big Health Industry Fund, a collaboration between Sanpower Group and China CITIC Bank, with a target fundraising amount of RMB 20 billion, primarily investing in healthcare, biotechnology, and elderly care. The Sinopharm Zhongjin Medical Industry Fund, involving Sinopharm Accord, Sinopharm Holdings, and CICC Zhide, had a proposed fundraising scale of RMB 3 billion. The Jiaxing Xinwen Ganfu Equity Investment Partnership, involving Tianyi Investment, Zhongfu Venture Capital, Xinwen Capital, and Huatai Asset Management, had a proposed fundraising scale of RMB 2.602 billion. The Hanyu Pharmaceutical Industry M&A Investment Fund, involving Hybio Pharmaceutical and Zhongyu Capital, had a target fundraising amount of RMB 2 billion, also ranking among the top in terms of proposed fundraising scale.

Here, we also need to highlight several “star” enterprises that have actively participated in healthcare industry funds and developed highly mature investment models. Typical representatives include GTJA Investment, Tianyi Investment, Zhongyu Capital, and Jinpu Investment.

Another direction is funds specifically targeting overseas projects, such as the U.S. healthcare project fund participated in by Fosun Industrial and Partners Innovation Fund II, L.P., and the offshore growth- and mature-stage enterprise project funds participated in by Tigermed’s subsidiaries, TG Sky Investment Ltd. and TF Venture Capital Management Co., Ltd.

Detailed data on the projects invested in by the 2017 healthcare fund are not yet available; however, VCBeat has learned that some projects had identified target companies at the initiation stage, while others have completed project screening and investment approval processes.

The "Dual Rise" of Industrial Investment

Driven by policy, market dynamics, capital, technology, and consumer trends, the landscape of the broader health industry is undergoing dramatic changes. To seize investment opportunities in this sector, it is essential to have a clear insight into industrial trends.

From the perspective of healthcare reform, cost containment by medical insurance will continue to drive payment system reforms centered on payers, strictly controlling the proportion of drug costs and limiting reimbursement for auxiliary drugs and injectables. Tiered diagnosis and treatment will be gradually implemented, with deepened adoption of the family doctor contract system and expanded pilots of specialized medical consortia. Secondary price negotiations will become normalized, while Group Purchasing Organizations (GPO) and cross-regional centralized procurement will emerge as trends. The two-invoice system and zero-markup policy will be further advanced, a registration system for pharmaceutical representatives will be established, and the practice of subsidizing healthcare with drug profits will be comprehensively abolished.

From the perspective of market structure, entry barriers in the pharmaceutical manufacturing industry have risen, leading to the accelerated elimination of smaller pharmaceutical companies and a rebound in industrial growth. The pharmaceutical distribution sector is undergoing rapid consolidation, with further increases in market concentration; regional distributors are accelerating their transformation, while third-party logistics providers are entering the market as disruptive forces. The chain pharmacy rate continues to rise, and new trends in prescription outflow from hospitals are fostering novel models such as Pharmacy Benefit Management (PBM) for retail pharmacies. Third-party medical imaging and laboratory testing services are gaining momentum and evolving toward group-based operations. Meanwhile, the growing value of physicians’ individual brands is driving the development of private medical institutions.

Furthermore, technologies such as big data and artificial intelligence will accelerate industrial restructuring. This is evident in the rollout of the “Digital China” strategy, the establishment of AI national teams—such as the intelligent platforms of Baidu, Tencent, and iFlytek—and the vigorous development of health and medical big data.

Therefore, when making industrial investments, greater emphasis must be placed on “integration of industry and finance,” which is also the reason for the proliferation of healthcare industry funds.

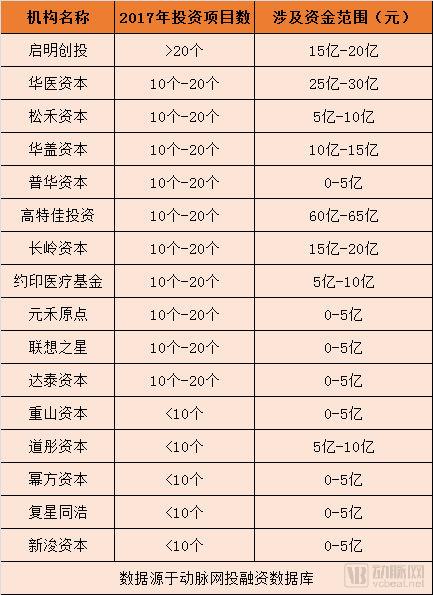

In addition to healthcare industry funds, specialized investment firms are also a significant force in healthcare sector investments.

VCBeat also compiled statistics on relevant data of investment institutions in the healthcare sector in 2017, with the general overview as follows:

For capital, this is the best of times; for startups and innovative enterprises, it is equally the best of times. Industrial transformation requires the support of capital, while capital needs high-quality targets to anchor its investment tracks. The interplay between the two drives the continuous advancement of the healthcare industry.

Further Reading

A Comprehensive Analysis of 108 Health Industry Funds from Listed Companies, with a Total Scale of RMB 168.2 Billion

http://vcbeat.top/OTRhMDJkNDQyMDZhM2VmNzJlNDc4MTY5N2ZmY2ZkYmM=

Fivefold Growth in Five Years: Total Scale Reaches 180 Billion, A Detailed Analysis of the Pharmaceutical Industry’s Stunning M&A Data

http://vcbeat.top/MGY5MmFkZjVmMzEzNDc2ZjFhNjkzNDNiMmRhNDJjNjU=

Pharmaceutical Industry: Multiple Major Policies Implemented in 2017, Robust Industrial Growth, and Investment and M&A Focused on Value Discovery [2017 Year-End Review]

http://vcbeat.top/ZWEzOWYxYjgyYTA1MWViMzMyMzcwYjYzNjA3M2QyNjI=