GaoSheng Solely Invests RMB 100 Million in HuanSheng Medical's Series A Funding to Expand Chain Hemodialysis Services

VCBeat (WeChat: vcbeat)It was reported that on January 5, 2018, Beijing Huansheng Medical Investment Co., Ltd. (hereinafter referred to as “Huansheng Medical”) announced the completion of its RMB 100 million Series A financing round, exclusively invested by Goldman Sachs, a globally leading investment bank, with Orient Securities-Citi serving as the exclusive financial advisor.

Previously, investors in Huansheng Medical also included Chongqing Tus-Holdings Yueyao Equity Investment Fund Partnership and Tibet Dashu Hetai Industrial Co., Ltd., among other enterprises.

It is reported that following this round of financing, Huansheng Medical will continue to dedicate itself to hemodialysis medical services, providing convenient healthcare solutions for dialysis patients.

Alongside the announcement of securing financing, Huansheng Medical has clearly outlined the next-phase development goals for Xiaojing Dialysis: it will conduct further exploration in the field of hemodialysis, including expanding the coverage and number of its chain facilities, exploring collaborative and integrated models with internet healthcare platforms and physician groups, improving system infrastructure, and establishing industry standards, thereby further leading industry development.

About Huansheng Medical

Beijing Huansheng Medical Investment Co., Ltd. was formerly the medical division of 3SBio Inc. (1530.HK). Following a spin-off and restructuring in November 2014, it became a wholly domestic-invested medical project investment company primarily engaged in establishing and operating chain hemodialysis centers. Its wholly-owned subsidiaries include Jiangsu Pharmaceutical Technology Co., Ltd., Beijing Huansheng Hospital Management Co., Ltd., and Liaoning Sansheng Technology Co., Ltd.

The company primarily provides customized, safe, and high-quality diagnostic and therapeutic services for patients with kidney disease. Its business strategy focuses on establishing community-based primary care nephrology hospitals and independent hemodialysis centers, dedicated to improving the quality of life and survival for a broad population of patients with end-stage renal disease (ESRD), while striving to deliver the optimal patient experience during treatment.

Xiaojing Dialysis is the flagship brand of Beijing Huansheng Medical Investment Co., Ltd. It is dedicated to providing patients with customized, safe, and high-quality hemodialysis services. On one hand, it ensures patient safety and superior dialysis quality through stringent quality control; on the other hand, it advocates a "patient-centered" service philosophy, delivering targeted and personalized treatment and care to help patients achieve a better quality of life.

As early as 2009, the predecessor of “Xiaojing Dialysis,” known as “Sansheng Kidney Friends Home,” established China’s first grassroots community hemodialysis center in Jinzhou, Liaoning Province, becoming the first pioneer in the domestic hemodialysis industry. In 2012, it became the first partner of U.S.-based DaVita Inc. in China. After six years of strategic preparation and layout, Huansheng Medical was spun off from Sansheng in 2014 to operate independently, rapidly completing the construction of 14 nephrology hospitals and independent hemodialysis centers. According to VCBeat, the predecessor of Xiaojing Dialysis was the medical division of Shenyang Sunshine Guojian Pharmaceutical (formerly known as Shenyang Sansheng Pharmaceutical).

Huansheng Medical’s hemodialysis centers are currently concentrated primarily in second- and third-tier cities across Hebei, Liaoning, Hunan, and Hubei provinces. On one hand, the company operates independent hemodialysis centers equipped with approximately 20 dialysis machines and basic nephrology departments. On the other hand, it has established secondary hospitals that adopt a “specialty-focused, general-care supplementary” model, with nephrology specialty hospitals and hemodialysis centers as their core services.

Chain Hemodialysis Center Policies Have Been Liberalized

The hemodialysis industry features high barriers in equipment and high-end material technologies, with foreign companies holding a dominant position. Consequently, as the National Health and Family Planning Commission (NHFPC) and local health authorities have issued a series of policies encouraging the development of independent hemodialysis centers, hemodialysis services have become a fiercely contested sector for domestic companies. In late December 2016, the NHFPC released the basic standards and management specifications for four types of independently established medical institutions, including hemodialysis centers, encouraging the opening of hemodialysis centers to private capital and promoting their development along chain-based and group-oriented lines.

Under the new standards, hemodialysis centers, as the only type of patient-oriented medical institution among the four independent medical entities, have attracted significant attention from private capital due to their substantial growth potential.

Mr. Cheng Wenwu, General Manager of Huansheng Medical, stated, “The medical services industry differs from other sectors in that it requires practitioners to possess compassion and a sense of responsibility; it is an industry driven by ethical conscience. For patients, dialysis is an essential necessity, and there must be enterprises within the industry willing to shoulder this responsibility. As a pioneer of independent hemodialysis medical services in China, the brand significance of Xiaojing Dialysis lies in delivering more professional and attentive medical care to a broader patient base through branded operations and chain management.”

The Market Urgently Awaiting Expansion

Due to the lack of accurate statistical data on patients with end-stage renal disease (ESRD) in China, estimates can only be derived from literature. Currently, all domestic market research reports on hemodialysis services are based on data extrapolated from the article “Epidemiology of Chronic Kidney Disease in China” published by scholars such as Zhang Luxia and Wang Haiyan in The Lancet in 2012. These projections estimate that the number of ESRD patients in China approached 2 million in 2014 and will reach 3.15 million by 2030.

VCBeat Research Institute released in April 2017"Private Independent Hemodialysis Center Industry Report" (Click to access the report), data in the report show that, based on the assumption that 2 million ESRD patients receive hemodialysis treatment at a 100% penetration rate and an annual treatment cost of RMB 75,000 per patient, the theoretical market size for hemodialysis is RMB 150 billion.

However, due to factors such as insufficient household payment capacity and gaps in health insurance coverage, China’s average dialysis treatment rate remains below 20%, significantly lower than that of other countries and regions. The global average dialysis treatment rate is 37%, while in developed countries and regions such as Europe and the United States, the rate reaches 90%.

With the improvement in residents' purchasing power and the expansion of medical insurance coverage, China's hemodialysis treatment rate has increased significantly, and the number of patients undergoing hemodialysis is rising rapidly, indicating substantial growth potential. According to statistics from CNRDS, China's hemodialysis market reached RMB 33.5 billion in 2016 and is expected to exceed RMB 35 billion in 2017.

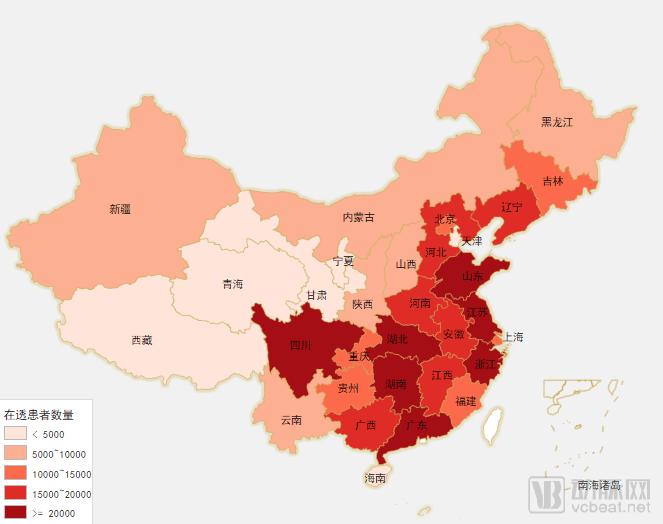

Distribution of Hemodialysis Patients Across China, Data Source: CNRDS

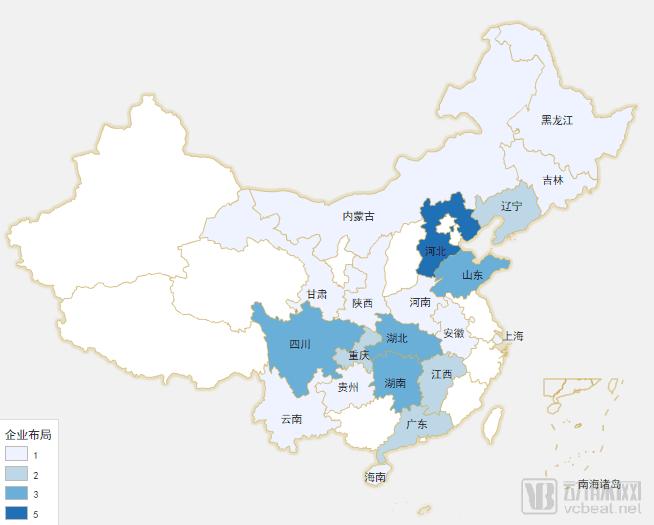

Hemodialysis service providers have already established their presence; data collected by VCBeat Research Institute

According to a research report by Orient Securities, there are currently 3,637 hemodialysis centers in China, predominantly concentrated in large public hospitals, which hold an absolute monopoly. With the expansion of coverage for critical illness insurance, the number of end-stage renal disease (ESRD) patients undergoing hemodialysis is expected to increase significantly. The existing 3,000-plus hemodialysis centers are severely insufficient to meet the needs of China’s vast patient population; it is estimated that China requires approximately 30,000 such centers. This substantial gap cannot be filled solely by the continued expansion of hemodialysis services in public hospitals. Consequently, the remaining significant market space will be captured by private institutions, a sector that remains largely undeveloped and ripe for exploration.