Rock Health Releases 2017 Digital Health Funding Report: Record $6B Investment Year and Unveils 2018 Digital Health Top 50

Rock Health recently released its year-end financing report on the digital health industry for 2017. VCBeat (WeChat: vcbeat) promptly translated and compiled the report.

The report pointed out that 2017 was a record-breaking year for the digital health industry, with total venture capital investmentNearly $6 billion, with the number of large deals exceeding $100 million also hitting a record high. Clearly, in the investment sector,The digital health industry has moved beyond its early stage and is advancing into the mid-stage.。

Although investors’ appetite increased significantly in 2017, investment exits remained lackluster., with only 119 acquisitions of digital health companies and no initial public offerings. However, there are more well-capitalized private enterprises than ever before, and investors are eager to seek potential exit opportunities.

Looking back at 2017, the digital health industry has clearly moved beyond the early stage of investment and is advancing toward the mid-stage; we are currently at the tail end of the early phase of digital health.

Over the past seven years, more than $23 billion has flowed into digital health startups.However, in the early stages, investments in 2011 and 2012 accounted for only 5% and 7% of this total, respectively; it was not until 2014 that the sector began to maintain a “steady-state” level of investment.

Between 2014 and 2016, fundraising activities for a large number of enterprises matured. The year 2017 witnessed a surge in mega-deals, as more mature companies began seeking substantial investments. However, it would be overly simplistic to base the 2017 investment levels solely on the projected trajectories of these companies.

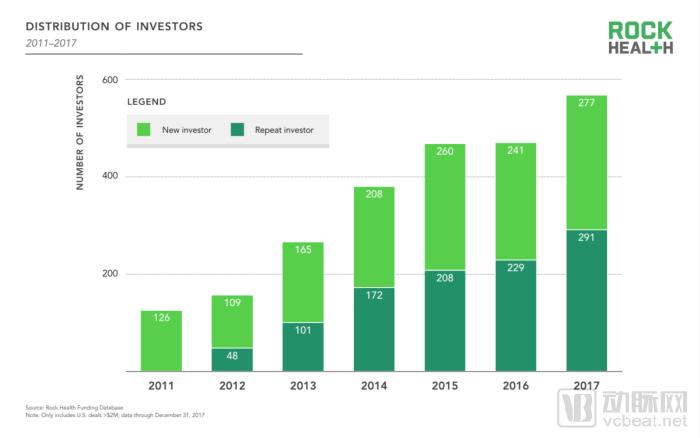

Similarly, not only did the scale and volume of large-scale deals in the later stages reach their peak, but the number of digital health investors engaging in repeat investments also hit a record high.

Despite considerable controversy surrounding policy changes in healthcare reform, digital health financing has still reached record highs, while healthcare policy has played a dominant role amid intense, high-stakes political shifts at the U.S. national level.

Most people may have previously assumed that these challenges would lead to a market crash or a credit crunch, but it has proven otherwise,All of this is attributable to the steadfast investor base in the digital health industry.。

Despite significant achievements, investors and entrepreneurs still face challenges posed by a sluggish initial public offering (IPO) market,No initial public offerings occurred in the digital health industry in 2017.。

The only time the number of companies listed on U.S. stock exchanges was lower than it is now was in the 1960s.

Finally, as public market investors increasingly favor passively managed funds, the number of actively managed funds acting as buyers in future initial public offerings (IPOs) will decline, although their typical size will be larger.

The long-term trends in the U.S. capital markets have posed a barrier to public listings while serving as a source of liquidity for private investors. To date, digital health has been impacted to a similarly significant degree.

Digital health companies that have gone public performed well in 2017, with a 31% increase, outperforming the broader market and surpassing the S&P 500 Index’s 19% gain.

Steadfast investors in the digital health industry firmly believe that there is still ample room in the market for practitioners to deliver better healthcare services to the public.2018 marked the end of the early stage of the digital health industry and the beginning of new challenges.

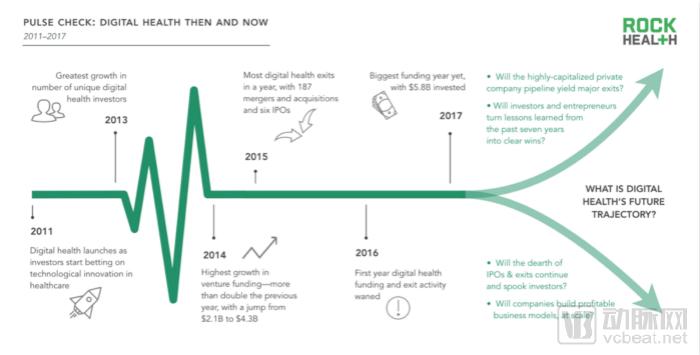

A Brief History of Digital Health

2011: Investors turned their attention to technological innovations in the healthcare industry, and digital health began to develop;

2013: A surge in the number of digital health investors;

2014: Venture capital saw its largest increase, jumping from $2.1 billion to $4.3 billion;

2015: The digital health sector saw the highest number of exit activities in a single year, with a total of 187 M&A transactions and 6 initial public offerings;

2016: The performance of digital health financing and exit activities was first time barely satisfactory;

2017: The year with the highest funding, totaling $5.8 billion;

The Future of Digital Health:

Will Highly Capitalized Enterprises Exit Through an IPO?

Will investors and entrepreneurs learn from the lessons of the past few years and make a comeback?

Will the lack of IPOs and exits persist, and will this deter investors?

Can enterprises establish profitable business models on a large scale?

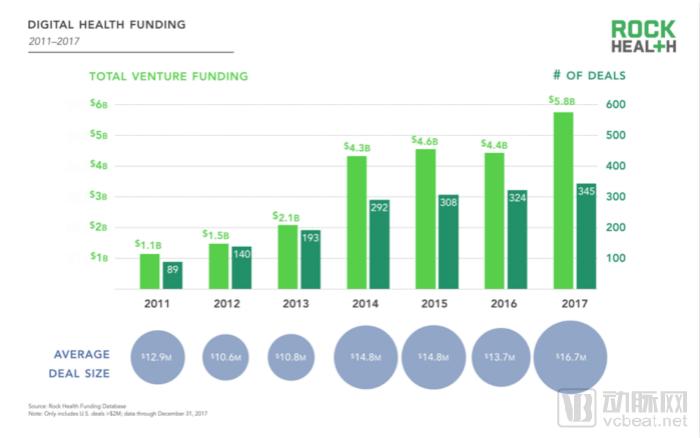

2017, Annual of Digital Health CompaniesFinancing Amount Exceeds $5 Billion for the First Time。

2017 was the year with the highest funding amount in the digital health industry to date,A total of $5.8 billion,The number of completed transactions has grown steadily, albeit modestly.

However, the increase in deal volume alone has not driven a sharp rise in capital inflows. Instead, we are seeing investors in this sector become more comfortable and confident, demonstrating a greater willingness to make larger investments in the digital health industry.

In fact, Outcome Health and Peloton Interactive secured the largest digital health investments on record, at $500 million and $325 million, respectively. Driven by these mega-deals, the average deal size hit a historic high of $16.7 million.

Historical Transaction Trends in the Digital Health Industry

The total funding amount in 2017 also serves as a cautionary tale. Despite strong mid-term momentum, Outcome Health is now facing serious allegations, subpoenas from the Department of Justice, lawsuits from investors, and the need to pay severance compensation to more than one-third of its employees.

But even without Outcome Health’s blockbuster deal, total digital health financing in 2017 would still have set a record by a wide margin, indicating that investor appetite is indeed growing.

It is difficult to predict the impact Outcome Health will have on the industry, but investor scrutiny is likely to increase. This development is welcome, yet the pace of financing in 2018 may slow down due to the absence of another $500 million deal.

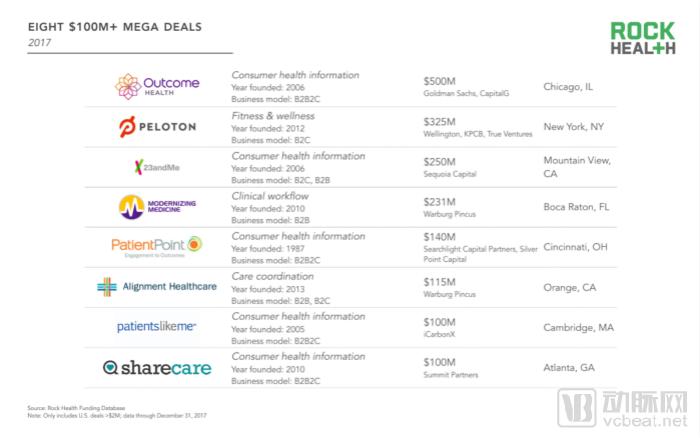

Following a record-breaking seven mega-deals exceeding $100 million each in the first half of 2017, only 23andMe closed a transaction worth over $100 million in the second half of the year.

Overall, the eight major deals in 2017 accounted for 31% of the total digital health financing for the year.These major transactions were completed by digital health companies across the United States, with only two of them headquartered in California.Several companies are relatively mature and experienced,The average age of the companies is 11 years.

Although the first half of 2017 saw a record seven major deals, there was only one major deal in the second half: 23andMe’s $250 million transaction (the company’s second major deal, bringing its total funding to $423 million since 2011).

23andMe’s genetic testing kits were among the top five best-selling products on Amazon during Black Friday 2017, with many consumers readily embracing the company’s promotional pricing. As this period coincided with the holiday gift-giving season, the U.S. Federal Trade Commission (FTC) advised consumers to consider the privacy implications of at-home DNA testing kits.

Eight Deals Exceeding $100 Million

1、Outcome Health

Company Sector: Consumer Health Information

Year Founded: 2006

Business Model: B2B2C

Financing Amount: $500 million

Investors: Goldman Sachs Group, CapitalG

Company Address: Illinois

2、PELOTON

Company Sector: Fitness and Wellness

Year Established: 2012

Business Model: B2C

Financing Amount: $325 million

Investors: Wellington, KPCB, True Ventures

Company Address: New York

3、23andMe

Company Sector: Consumer Health Information

Year Established: 2006

Business Model: B2C, B2B

Financing Amount: $250 million

Investor: Sequoia Capital

Company Address: Mountain View, California

4、MODERNIZING MEDICINE

Company Sector: Clinical Workflow

Year Founded: 2010

Business Model: B2B

Financing Amount: $231 million

Investor: Warburg Pincus

Company Address: Florida

5、PatientPoint

Company Sector: Consumer Health Information

Year Established: 1987

Business Model: B2B2C

Financing Amount: $140 million

Investors: Searchlight Capital Partners, Silver Point Capital

Company Address: Cincinnati, Ohio

6、Alignment Healthcare

Company Sector: Care Coordination

Year Founded: 2013

Business Model: B2B, B2C

Financing Amount: $115 million

Investor: Warburg Pincus

Company Address: Orange, California

7、patientslikeme

Company Sector: Consumer Health Information

Year Founded: 2005

Business Model: B2B2C

Financing Amount: $100 million

Investor: iCarbonX

Company Address: Cambridge, Massachusetts

8、sharecare

Company Sector: Consumer Health Information

Year Founded: 2010

Business Model: B2B2C

Financing Amount: $100 million

Investor: Summit Investment

Company Address: Atlanta, Georgia

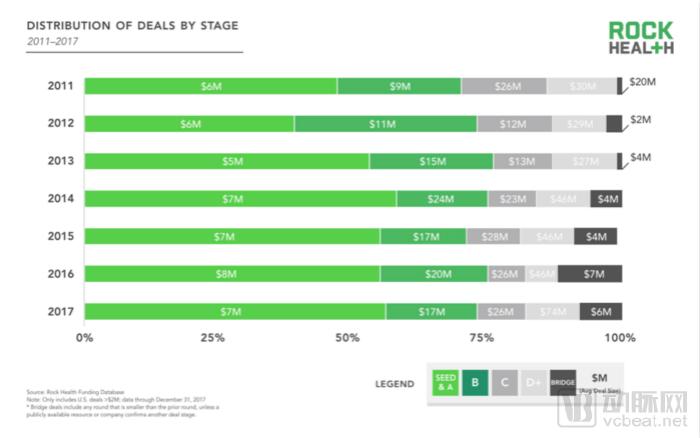

Driven by large-scale transactions,The average deal size for Series D+ financing rounds in 2017 increased by 60%.

From the overall distribution of financing stages in 2017, seed funding and Series A financing in the previous years still accounted for a share of the total transaction volume. However,The average deal size for Series D+ financing rounds surged, with a 60% increase per transaction to reach $74 million.

Excluding Outcome Health, the average Series D+ funding round size still saw substantial growth, reaching $60 million.This indicates that investors are willing to complete large transactions with companies that have a strong track record.。

Distribution Chart of Transaction Stages

withCompanies offering consumer health information as their primary value proposition dominated the 2017 funding market., the following are the 6 sectors with the most funding。

Note: A single enterprise may fall under multiple value proposition categories; therefore, the sum of financing amounts across all categories does not equal the total financing amount.

1. Consumer Health Information

Content: Helping consumers better understand their health, common medical care concepts, and the healthcare system.

Total Transaction Value: $1.6 billion (including $500 million for Outcome Health)

Number of Transactions: 41

2. Clinical Decision Support and Precision Medicine

Content: Providing real-time information and alerts to healthcare providers to assist them in making patient care decisions or adjusting the management and treatment of patients' conditions.

Total Transaction Value: $811 million (Outcome Health accounts for $500 million)

Number of Transactions: 19

3. Fitness and Health

Content: Maintain and promote users' personal health, including fitness, nutrition, and sleep

Total transaction value: $752 million (Pelton accounts for $325 million)

Number of Transactions: 32

4. Disease Surveillance

Content: Monitoring Specific Clinical Symptoms

Total Transaction Value: $517 million (LIVONGO accounts for $52.5 million)

Number of Transactions: 39

5. Disease Diagnosis

Content: Diagnosis of Specific Clinical Symptoms

Total transaction value: $493 million (Heatflow accounts for $90 million)

Number of Transactions: 35

6. Non-clinical Workflows

Content: Administration and management of non-clinical operations (e.g., scheduling, bookkeeping, etc.)

Total Transaction Value: $482 million

Number of Transactions: 54

In 2017, consumer health information was the sector most favored by investors, accounting for five of the eight major deals. Although Outcome Health belonged to the largest deal category,Consumer Health Information Tops the Charts Regardless。

Other corporate transactions that share this value proposition include: PatientPoint, which uses tablets and screen-based media to enhance communication between patients and healthcare providers; 23andMe, which offers genetic health risk testing for individuals; and ShareCare, which uses surveys to assess health status and provides solutions based on symptoms.

Although these companies adopt different communication models, they all aim to deliver information to consumers, helping them manage their personal health while navigating the complex healthcare system.

Tech giants also believe the time is ripe for innovation in this field. Amazon is exploring the use of Alexa’s voice technology to provide health information for common conditions, while Apple is working to make the all-knowing iPhone the centerpiece of patients’ health records.

Enterprises whose primary value proposition is providing clinical decision support and precision medicine raised a total of $811 million in financing in 2017, accounting for half of the total amount raised by consumer health information companies ($1.6 billion).

Over the past two years,Investment in disease monitoring, treatment, and diagnosis has increased as investors seek solutions that deliver tangible clinical outcomes.(The increase is 60-115%).

There are more repeat investors in the digital health industry than ever before.

Additional Signs Indicate the Digital Health Industry Has Entered Its “Mid-Stage” for the First Time: In 2017, more than half of digital health investors were repeat investors who had participated in at least two digital health deals since 2011. These transactions included new investments as well as follow-on investments that doubled down on previous commitments.

Investor Distribution

Overall, there were more independent investors in 2017 than in previous years, and the digital health sector received for the first time in its historyFinancing from over 500 independent investors.

New investors account for 49% of this group, and whether they will continue to invest in this sector remains to be seen. If investors fail to see monetization, meaningful outcomes, and notable exit results, their interest could wane rapidly.

Vijay Lathi, General Partner at New Leaf Venture Partners, expects that the momentum and investment in the digital health sector will continue, stating, “The overarching goals of improving healthcare quality, enhancing efficiency, and reducing costs constitute an undeniable value proposition for the healthcare industry today.。”

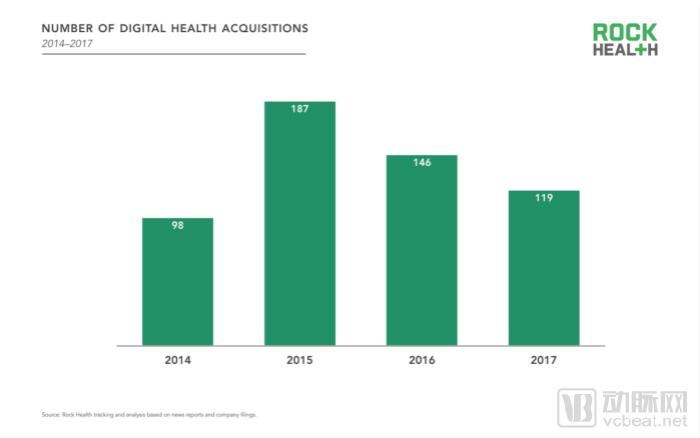

Despite experiencing a record-breaking year,In 2017, the volume of M&A transactions dropped sharply to 119 deals.。

This marks the second consecutive year of decline in public M&A transaction volume. In 2017, the number of digital health M&A deals decreased by 18% compared with 2016 and by 36% compared with 2015, when M&A activity peaked.

Leah Sparks, Co-Founder and CEO of Wildflower Health, stated, “Large enterprises will wake up to the reality that they must acquire innovation, as it cannot be generated solely in-house.” However, protracted sales cycles may mean that few companies currently achieve sufficient scale for large enterprises to derive value through acquisitions.

Since 2015, companies focused on enhancing electronic health record (EHR) functionalities and improving clinical workflows have been the most likely acquisition targets. It has been four years since the EHR system certification rules took effect; to maintain Medicare and Medicaid reimbursement rates, hospitals must demonstrate to the government and the public the value of adopting EHRs.

Number of Digital Health Acquisitions

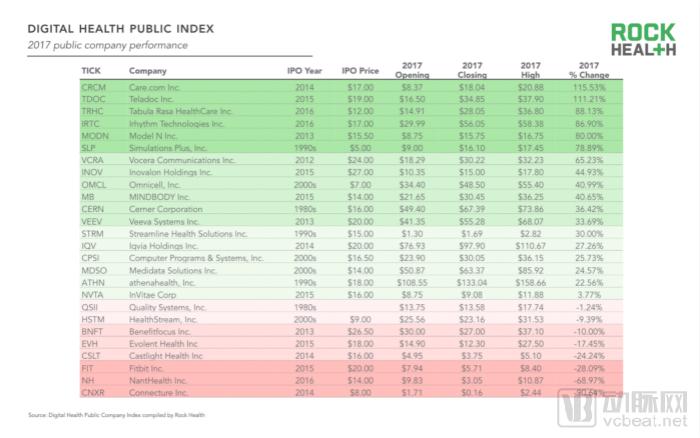

Surprisingly,In 2017, no digital health companies raised capital in the public markets.。

Although the number of initial public offerings (IPOs) in the digital health sector rose in 2014 and 2015, it came to a complete halt in 2017; since iRhythm’s listing in October 2016, no digital health company has entered the public market.

Notably, despite the absence of initial public offerings (IPOs), 2017 remains the year with the highest number of large-scale transactions to date. Driven by a greater volume and larger scale of pre-IPO investments, investors will face considerable exit pressure in the upcoming 12 to 24 months.

Among digital health companies that have gone public in the past few years, each company waited an average of ten years and raised an average of $136 million before entering the public market.A few private companies (such as 23andMe, PatientPoint, and ZocDoc) meet both benchmarks and have all completed major transactions since 2011.

Despite the absence of new market entrants, the index of publicly listed digital health companies performed well in 2017.

In 2017, the index of publicly listed digital health companies surpassed the S&P 500 Index in the public markets.

2017 was a banner year for the stock market, with the S&P 500 Index rising by 19%. Despite political uncertainty, the economy continued to thrive. Although healthcare reform remained in a state of flux, the Digital Health Public Company Index outperformed the S&P 500, surging by 31%.The biggest market winners in 2017 were Care.com and Teladoc.

The stock prices of these two companies more than doubled in 2017.

Overall, 18 of the 26 listed digital health companies saw their stock prices rise in 2017. Notably, the number of digital health companies included in the index decreased from 27 to 26 in 2017 due to KKR’s acquisition of WebMD.

Although 2017 was an unequivocally optimistic year for the index of publicly listed digital health companies, some digital health firms still experienced precipitous declines in their stock prices. As of the report’s release date, Connecture and NantHealth had each lost more than half of their stock value in 2017.

Digital Healthcare Listed Company Index

Beyond financing and investment trends, which leading companies, investors, products, and employers stand out in the digital health sector? Rock Health has released its 2018 Top 50 Digital Health Companies list, from which VCBeat (WeChat ID: vcbeat) has selected and highlighted several notable representatives.

Best Startup

Cityblock Health is committed to fundamentally improving the health of urban communities by delivering high-value, readily accessible, and personalized healthcare services to eligible Medicaid and Medicare members.

They aim to fully integrate primary care, behavioral health, and social services into a comprehensive care model, thereby strengthening the relationship between patients and care teams, all supported by their proprietary technology.

Best Digital Health Employer

In the United States, 150 million people obtain health insurance through their employers. Collective Health offers employer-sponsored medical insurance solutions that bypass intermediaries, enabling employers to provide cloud-based, “à la carte” medical insurance benefits at more affordable prices for their employees.

Collective Health helps enterprises maximize returns on their healthcare investments while providing better care for their employees. The team is committed to fostering a diverse and inclusive culture, enabling employees to advance their careers in a health- and wellness-oriented environment, and offering benefits such as flexible work schedules and generous family leave.

Fastest-Growing Enterprises

Grand Rounds is a U.S.-based physician referral service provider that aims to reduce patients’ financial burden and improve treatment outcomes by optimizing patient–physician matching.

The company provides employees and their families with the technology, information, and support needed to help them decide whether to undergo treatment and where to receive it. Since 2015, Grand Rounds has expanded its presence on both the East and West Coasts of the United States, quadrupling its customer base to serve more than three million users.

Annual Invention

U.S. drone startup Zipline has been dedicated to designing drones that deliver vaccines, medications, and blood products on demand to healthcare workers in remote areas.

Zipline is addressing the needs of over 2 billion people who lack adequate access to essential medical products due to challenging terrain and infrastructure limitations. Zipline utilizes the world’s only drone delivery system to dispatch emergency medications to patients, regardless of their location.

Diversity Leadership Award

Canaan Partners believes that diverse teams bring fresh thinking, spirited debate, and exceptional performance. The company upholds these values by hiring a workforce that spans industries, generations, and coasts, and demonstrates its commitment to diversity through its investment portfolio. Forty percent of Canaan’s investment team are women, while 47% are immigrants or first-generation Americans.

Annual Non-Profit Organization

According to U.S. News & World Report, Boston Children’s Hospital is the top-ranked pediatric hospital in the nation, dedicated to improving pediatric care for all children.

To fulfill this mission, the Innovation and Digital Health Accelerator (IDHA) at Boston Children’s Hospital supports leaders in clinical care and research as they pursue breakthrough pediatric technologies, with a commitment to delivering these innovations to patients and clinicians worldwide. During its first two years of rapid growth as a startup, IDHA launched four ventures backed by more than $13 million in venture funding.

The Most Prolific Venture Capital Funds

KPCB is committed to bringing world-changing ideas to market. To date, the firm has supported hundreds of entrepreneurs and stands as one of the top venture capital funds in the United States, with successful investments in companies such as Google, Amazon, and Uber. This year, KPCB participated in six digital health deals, including those involving Peloton, Nuna Health, and Kinsa.

The Most Prolific Venture Capital Firms

GE Ventures leverages its global network to invest in new ideas that help deliver better outcomes for customers and society at large. As the most active digital health venture capital firm in 2017, GE Ventures participated in several funding rounds, including investments in Arterys, Evidation Health, and Syapse.

Top-Performing IPO Companies

Tabula Rasa HealthCare provides technology and services to at-risk healthcare organizations, optimizing medication regimens to reduce hospitalization rates, lower costs, and mitigate risks. As of the release of the TOP list, Tabula Rasa’s stock had surged by 140%, marking the largest growth among publicly traded digital health companies in 2017.

Disruptive Founder of the Year

Todd Park

Todd Park co-founded Devoted Health with his brother Ed Park, a company dedicated to helping seniors navigate the healthcare system.

The company delivers a streamlined patient experience through personalized guidance and world-class technology, while partnering with top-tier healthcare providers to enhance patients’ overall health outcomes. Led by a team of renowned data scientists and technology executives, the company plans to launch a Medicare Advantage plan in 2019.

Journalist of the Year

Dan Diamond

Dan Diamond is a contributor to Politico, and his reporting on spending by the U.S. Department of Health and Human Services became one of the most significant news stories of 2017.

Dan is the author of the daily newsletter “Politico Pulse” and the host of the Pulse Check channel, where he engages in weekly conversations with some of the most interesting and influential figures in the healthcare industry.

Best Digital Health Communicator

Lisa Suennen

Lisa Suennen

Lisa Suennen is the author of the Venture Valkyrie blog and co-host of the biweekly Tech Tonics podcast. She is a prominent figure in the digital health sector and has interviewed numerous leaders in healthcare and technology.

She is also a Senior Managing Director at GE Venture’s healthcare investment group, a member of the Haas School of Business at the University of California, Berkeley, and the founder of C-Sweetener.

C-Sweetener is a nonprofit organization dedicated to matching senior female leaders in the healthcare sector with suitable mentors, thereby empowering them to achieve greater success in their careers. As an entrepreneur, investor, and board member, Lisa has nearly 30 years of experience in the healthcare industry.

Best Policy Advocate

Andy Slavitt

Andy Slavitt

Andy Slavitt has consistently championed initiatives to advance healthcare technology and innovation, paving the way for future industry breakthroughs and thereby helping consumers and healthcare providers access the health information they need.

As a former executive at the U.S. Centers for Medicare & Medicaid Services (CMS), Andy helped design and advance healthcare initiatives impacting millions of Americans, including the Electronic Health Record (EHR) Incentive Program.

Most-Loved CEO by Employees

Anne Wojcicki

Anne Wojcicki

Anne Wojcicki is the co-founder of 23andMe, a genetic technology company dedicated to becoming a data services enterprise focused on the mining, analysis, and interpretation of genetic information. The company integrates into the translation phase from scientific research to commercial products, leveraging its services to collect data while simultaneously using that data to enhance its services.

Anne Wojcicki has achieved a 100% approval rating on Glassdoor, setting the standard for how to lead a rapidly growing healthcare company. Employees say they are deeply impressed by this female leader, who provides clear organizational structure and invests in her staff, thereby fostering personal growth and teamwork. She is a powerful leader who inspires all employees.

Angel Investor of the Year

Paul Buchheit

Paul Buchheit

Paul Buchheit is an American computer programmer and entrepreneur, as well as the creator and lead developer of Gmail. His 2017 angel investment portfolio included DocTalk, Lively, and The Mednet.

Paul is also an early angel investor in drchrono, Picnic Health, and Circle Medical. As a partner at Y Combinator, Paul provides various forms of support to entrepreneurs and actively promotes diversity in the technology industry.

# The Most Tech-Friendly Healthcare Service Provider

Dr. Farzad Mostashari

Dr. Farzad Mostashari

Dr. Farzad Mostashari has spent his career at the forefront of healthcare policy and health information technology, with the goal of empowering physicians to deliver high-quality care. He is the founder and CEO of Aledade and formerly served as the National Coordinator for Health Information Technology.

Aledade transforms physicians to a value-based healthcare model and operates under value-based payment structures, thereby enabling physicians to remain independent, deliver better patient care, and reduce overall costs.

Note: All stock price fluctuations and related data mentioned in the text are current as of the publication date of the article and report. VCBeat strives to ensure the accuracy, completeness, and rigor of the translation.