2017 Global Healthcare Investment Report: 1,028 Deals Raise RMB 157.1 Billion, Technology Innovation Drives Capital Growth

According to statistics from the VCBeat database, global financing in the healthcare sector increased by 57% in 2017 compared to 2016, reaching RMB 157.1 billion and setting a new historical high.

Key Insights of the Report

Biotechnology and pharmaceuticals have driven the growth of global healthcare financing.

Capital markets are becoming more rational, as evidenced by greater diversification in investment and the concentration of capital in high-quality projects;

The average amount per single financing round has risen significantly, with the domestic average exceeding RMB 100 million;

Technology-driven healthcare is more attractive to investors than consumer-driven service sectors;

Domestic angel and seed funding rounds continue to decline, with a more severe shortage of early-stage investments in the consumer services sector;

Benefiting from national support for innovation in the pharmaceutical and medical device sectors, pharmaceutical, medical device, and biotechnology enterprises with independent innovation capabilities are likely to attract investment in the future;

A decline in investment deals within the primary healthcare sector, with early signs of industry consolidation emerging;

Hot investment sectors at home and abroad are largely similar; however, compared with overseas markets, the domestic market is less mature, making early-stage projects more likely to secure investment.

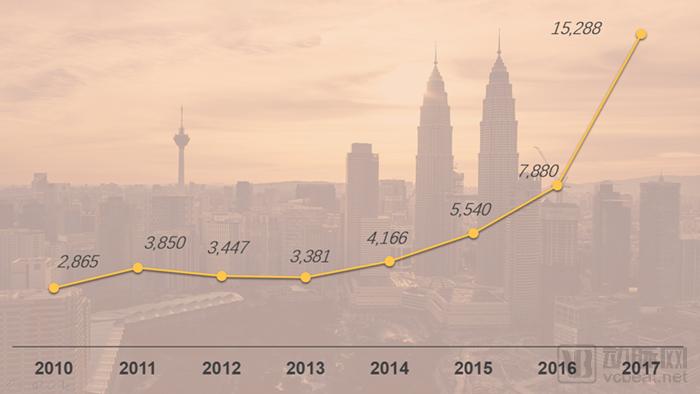

2010–2017: Changes in Global Healthcare Industry Financing Volume, Compiled by VCBeat

In 2014, the digital health sector gained momentum as internet technologies fostered new models of healthcare delivery, attracting significant capital inflows into the medical and health industry. In the three major sectors of biotechnology, healthcare informatics, and medical devices, enhanced innovation capabilities and growing application demands drove global investment growth in healthcare.

According to data from VCBeat, total global healthcare financing more than tripled between 2013 and 2015, with 41% of the increase coming from the three aforementioned sectors.

In 2016, as investment in healthcare informatics and medical devices slowed, the growth of overall industry financing gradually declined. However, in 2017, a surge in major financing rounds in biotechnology and pharmaceuticals drove a significant rebound in global healthcare industry funding. The total financing amount for 2017 increased by 57% year-on-year, reaching RMB 157.1 billion.

Compared with 1,191 financing deals in 2016, only 1,028 deals occurred in 2017, representing a 10% decline. Against the backdrop of rapid growth in overall investment volume, the decrease in the number of investment deals led to a substantial increase in the average size per deal.

2010–2017: Changes in Single-Round Financing Amounts in the Global Healthcare Industry, Compiled by VCBeat Research Institute

According to the VCBeat database, the average single financing amount in the global healthcare industry reached RMB 152.88 million in 2017, a 94% increase from RMB 78.8 million in 2016, indicating a clear trend of capital concentration.

The maturation of the industry, a decline in early-stage investments, and the surge in large-scale investments in the pharmaceutical and biotechnology sectors are the primary drivers behind the increase in the average size of individual financing rounds.

2017: Changes in Average Financing Amounts by Sub-sector in the Global Healthcare Industry, Compiled by VCBeat Research Institute

As the industry matured, over half of the sub-sectors saw financing volumes reach RMB 100 million in 2017. The pharmaceutical sector recorded the highest average financing amount, with an average single-round financing of RMB 330.92 billion, doubling year-on-year.

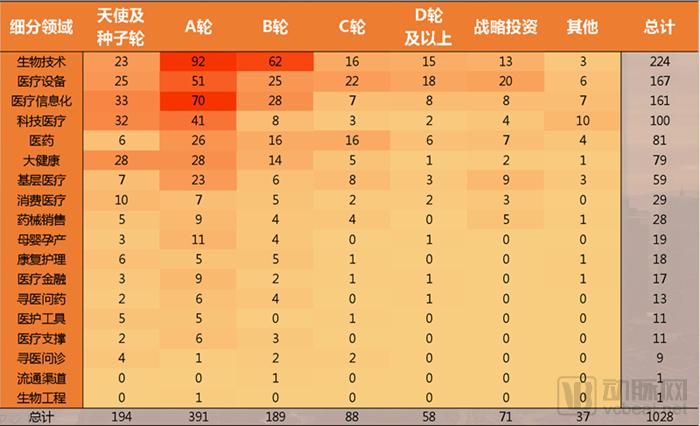

2017: Distribution of Financing Heat in Subsectors of the Global Healthcare Industry, Compiled by VCBeat Research Institute

In 2017, Series A financing rounds dominated the global landscape, with a total of 391 deals, accounting for over 38% of the total.

Financing events were primarily concentrated in four technology-driven sectors: biotechnology, medical devices, healthcare informatics, and digital health, which together accounted for 652 deals, or 63.4% of the total. In contrast, financing performance in the service innovation sector—driven by consumer demand and encompassing areas such as online medical consultation, rehabilitation and nursing care, and maternal and infant care—was less robust, as the industry landscape gradually became more defined.

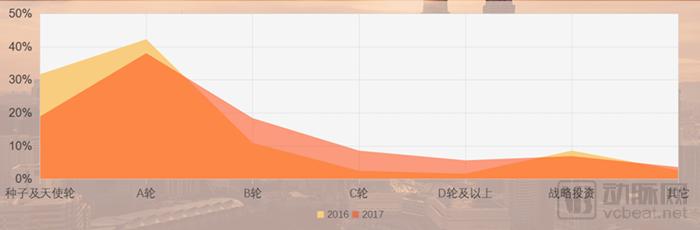

2016–2017: Migration of Financing Rounds, compiled by VCBeat Research Institute

Compared with 2016, global investment rounds in the healthcare sector shifted significantly toward later stages in 2017. Taking early-stage investments such as seed and angel rounds as an example, there were 218 financing events in 2016, accounting for 31.6% of the total number of financing events that year. In 2017, seed and angel rounds totaled 194 financing events, representing 18.9% of all financing rounds. Taking internet healthcare as an example, since the rapid development of new business models began in 2014, the industry has become increasingly mature, and competitive moats have been established. Capital is now more focused on companies with clear profitability models at later stages, leaving limited opportunities for new entrants.

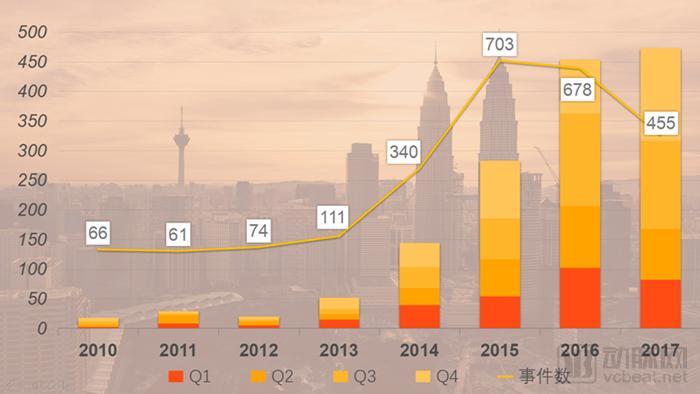

2010–2017: Changes in Financing Scale of China’s Healthcare Industry, Compiled by VCBeat

In 2017, there were a total of 455 investment deals in China, amounting to RMB 47.4 billion. Compared with previous years, the growth rate of financing scale in the healthcare sector significantly slowed down in 2017. The total amount increased by only RMB 1.7 billion compared to 2016.

The decline in financing capacity within the big health sector is a significant factor contributing to the slowdown in the growth of the industry’s overall financing scale. In 2016, the big health sector, with health management and exercise management as its primary sub-segments, saw financing exceed RMB 6 billion, representing a year-on-year increase of over 100% from RMB 2.8 billion in 2015. However, in 2017, total financing in this sector amounted to only RMB 1.8 billion.

After experiencing frenetic growth from 2013 to 2016, the industry now has a sufficient number of participants, and product models in the existing market are largely homogeneous. Consequently, new entrants and projects lacking competitiveness will struggle to attract investors. In the future, absent innovation in service models, the cooling of investment enthusiasm will further intensify as the industry landscape becomes increasingly clear.

On the other hand, compared to 678 financing events in 2016, the number of financing events in China’s healthcare industry dropped by one-third in 2017, totaling only 455. Similarly, the maturation of the service innovation sector was also a major reason for the overall decline in the number of financing events in the industry.

2010-2017: Changes in the Average Financing Amount in China's Healthcare Industry, Compiled by VCBeat

In terms of the average amount per transaction, the average domestic financing amount is currently below the global average. Differences in industry maturity have resulted in lower financing capabilities for projects within China compared to those overseas.

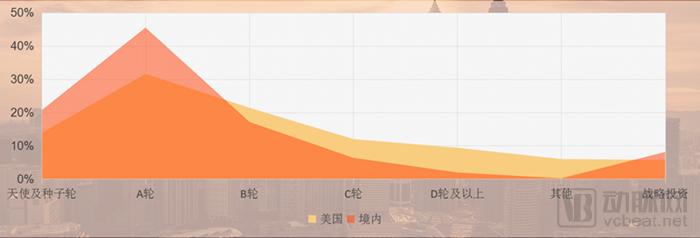

2017: Distribution of Financing Rounds in the China-U.S. Healthcare Industry, Compiled by VCBeat

Differences in industry maturity can be reflected in the distribution of investment rounds.

Compared with the United States, China’s healthcare sector accounts for 66% of investment deals at Series A and earlier stages, whereas the corresponding share in the U.S. is only 45%. This suggests that, relative to the U.S. entrepreneurial environment, new entrants in China’s healthcare industry can more readily secure investment opportunities by leveraging their unique competitive advantages.

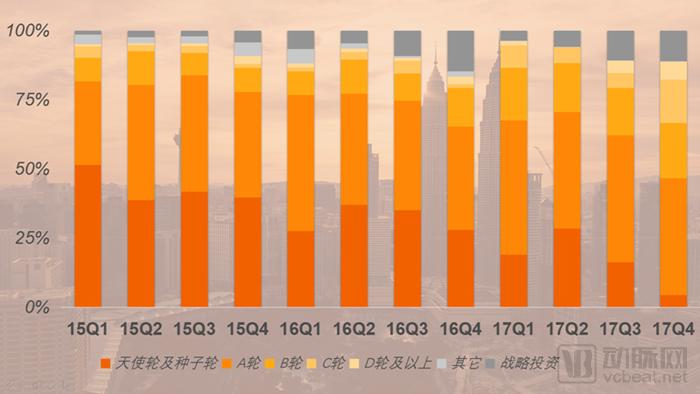

2015-2017: Distribution of Financing Rounds in China’s Healthcare Industry, Compiled by VCBeat

Despite the significant gap in industry maturity compared to developed countries, innovative projects in China’s healthcare sector continue to mature.

Through an analysis of financing rounds, we found that the proportion of seed and angel rounds in the healthcare sector in 2017 had decreased by more than twofold compared to 2015. In 2017, such rounds accounted for less than 17% of all financing events.

At the same time, this also means that after two and a half years of development, many sectors within the healthcare industry have seen the emergence of relatively mature companies, while the fundraising capacity of early-stage projects is declining.

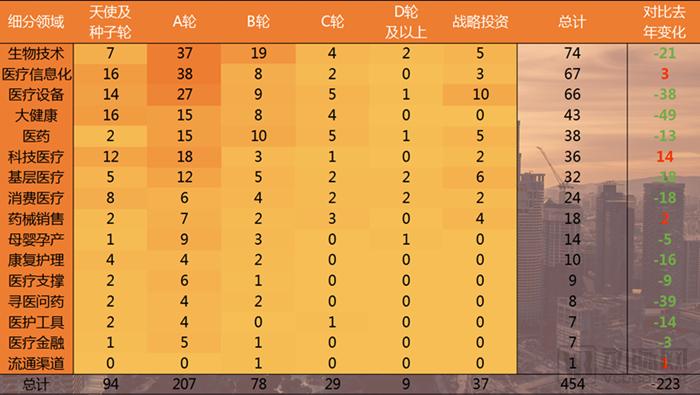

2017: Financing Capacity in Subsectors of China’s Health Industry, Compiled by VCBeat Research Institute

In terms of the distribution of investment enthusiasm across niche sectors, the financing advantages established by technological innovation have become evident. Niche sectors with certain technical barriers, such as biotechnology, medical informatics, and pharmaceuticals, are experiencing significantly higher investment interest compared to other areas; meanwhile, investment enthusiasm in sectors driven by service model innovation, such as maternal and infant care and online medical consultation services, is declining.

Taking online medical consultation as an example, there were 47 financing events in 2016, but only 8 investment deals in 2017.

In the field of service innovation, industry maturity is higher compared to the technology sector. Meanwhile, product homogenization among enterprises is quite severe, with strong replicability. Companies can achieve rapid growth through capital injection; once industry giants emerge, the homogeneous competitive environment makes it difficult for smaller players to survive.

As the competitive landscape of the service innovation sector becomes increasingly clear, early-stage projects lacking first-mover advantage are no longer able to attract investor attention. If existing service paradigms cannot be broken through, investment enthusiasm in the field of service innovation is likely to continue cooling as the industry structure solidifies.

2017: Distribution of Financing Heat in Sub-sectors of China's Healthcare Industry, Compiled by VCBeat

Among the 16 subsectors that secured financing, four witnessed a slight increase in the number of financing deals. However, the rapid maturation of the industry led to a decline in financing activity across the other subsectors, with the most significant drops observed in medical devices, general health and wellness, and online healthcare consultation services.

In terms of investment rounds, Series A transactions were the most frequent, with a total of 207 deals, accounting for 46% of all events, representing a slight increase compared to 2016.

2017: Active Investment Institutions in China’s Healthcare Industry, Compiled by VCBeat Research Institute

In terms of investment institutions, those with more than ten domestic investment deals in 2017 were Matrix Partners China, Qiming Venture Partners, Sequoia Capital China, and Legend Capital. Other relatively active investment firms included SoftBank China, Grand Healthcare Investment (Honghui Capital), GTJA Investment, Tsinghua Holdings Silver Investment, Lilly Asia Ventures, and Huagai Capital.

2017: Distribution of Large-Scale Financing in China's Healthcare Industry, Compiled by VCBeat

United Imaging Healthcare Raises RMB 3.333 Billion in Series A Financing, Ushering in a New Era for Innovation in the Medical Device Sector

United Imaging Healthcare is a provider of high-end medical equipment and healthcare informatics solutions. Headquartered in Jiading, Shanghai, its business encompasses the research, development, and manufacturing of premium medical products for the entire process of imaging diagnosis and treatment, as well as the provision of innovative healthcare informatics solutions.

In an open letter to all employees, Xue Min, Chairman of United Imaging Healthcare, stated that following the financing round, the company would continue to increase its investment in innovation and provide cost-effective products and healthcare informatics solutions.

Currently, United Imaging Healthcare has cumulatively filed over 1,700 patent applications, including more than 1,500 domestic invention patent applications and over 200 international invention patent applications.

In 2016, the company won China’s first Gold Award for Patents in the high-end medical equipment industry with its innovative MRI technology, “Image Reconstruction Method for Echo Planar Imaging Sequences.” In May 2017, United Imaging Healthcare officially unveiled the world’s first total-body scanning PET-CT system, the uExplorer, which enables 4D real-time dynamic whole-body imaging.

Recently, the United Imaging 96-ring light-guided PET-CT was installed at Fujita Health University Hospital in Nagoya, Aichi Prefecture, Japan, becoming the first high-end medical device from China to enter the Japanese market.

Adhering to the independent development of core technologies, prioritizing innovation, and providing competitive self-developed products are the fundamental reasons for United Imaging’s rapid growth and recognition by the capital market. Meanwhile, this largest financing round in the history of the medical equipment sector also heralds the rise of domestically produced innovative devices.

Against the backdrop of the trend toward independent innovation in China’s healthcare sector, medical device companies with core technologies can establish a virtuous cycle driven by innovation, supported by favorable policies, fueled by capital, and reinforced by product enhancement. This dynamic not only accelerates corporate growth but also boosts the competitiveness of domestically produced devices and promotes vertical deepening of the industry.

Haodf.com Secures $200 Million in Funding: Tencent’s Multi-Sector Strategy

Haodf Online was established in 2006, initially focusing on providing medical consultation information. After years of development, Haodf Online has fully transformed into an internet hospital.

In April 2016, Haodf.com and the Yinchuan Municipal Government announced the joint establishment of the Yinchuan Smart Internet Hospital. Eight months later, the internet hospital officially commenced operations. On March 19, 2017, Haodf.com publicly announced that the Yinchuan Internet Hospital had been formally integrated into the medical insurance system.

As of March 2017, Haodf.com had indexed 490,000 physicians from 7,500 accredited hospitals across China, among whom 145,000 had completed real-name registration. Its post-consultation services have evolved into a large-scale online disease management system, overseeing more than 10 million patients.

This round of $200 million in investment was provided by Tencent’s Industrial Win-Win Fund. Previously, Tencent had already made substantial investments in similar doctor- or doctor-patient platforms such as WeDoctor, Dingxiangyuan, Zhuojian, and Medlinker. Its decision to further increase its stake in Haodaifu Online, despite the competitive relationship, may stem from Tencent’s belief that the market space is sufficiently large, and that the advantages derived from business differentiation among these companies outweigh the risks of competition arising from homogenization.

Meanwhile, as a unicorn in its niche sector, Haodafu itself possesses ample resources of doctors and patients. This is precisely what attracts Tencent.

Allwin Health’s Chain Pharmacy Integration Strategy: Securing Two Major Rounds of Funding in Succession

On October 30, Quanyi Health Pharmacy Chain Co., Ltd., a leading retail pharmacy operations and management platform in China, announced that it had secured billions of yuan in Series B financing, led by Hony Capital. Following this round of financing, Hony Capital has become the second-largest shareholder of Quanyi Health. Previously, Quanyi Health also received billions of yuan in investment from CDH Investments.

Quanyi Health achieved growth from zero to 2,000 partner pharmacies and RMB 6 billion in annual revenue within just one year. Through large-scale mergers and acquisitions, Quanyi Health rapidly established a competitive advantage characterized by regional integration and nationwide coverage, which has entailed substantial capital requirements. This underscores the imperative for Quanyi Health to secure significant financing.

China’s pharmaceutical retail market is fragmented, with a low level of concentration. After securing substantial funding, All-in Health has acquired and integrated leading regional pharmacy chains while enhancing profit margins through refined management. The company aims to build a pharmacy chain enterprise with regional pricing power and advantages in centralized procurement and management, thereby expanding its footprint across China and ultimately establishing a nationwide chain characterized by sound corporate governance, excellent managerial capabilities, and deep regional penetration.

The “war-sustaining-war” acquisition and expansion strategy has created substantial capital requirements for Quanyi Health. Meanwhile, the phased operational successes and the strategic viability of its business logic have encouraged investment institutions to inject significant capital, thereby strengthening its competitive advantage.

Pharmaceutical Innovation Attracts Capital from the Industry

In October this year, the State Council and the General Office of the Central Committee of the Communist Party of China jointly issued the “Opinions on Deepening the Reform of the Review and Approval System to Encourage Innovation in Drugs and Medical Devices.” This policy standardizes and streamlines processes related to the management of clinical trials and market approval for pharmaceuticals, demonstrating the state’s support for innovation in the medical and pharmaceutical sectors.

It can be said that the innovation trends in the medical device sector have become an important direction for the development of the pharmaceutical industry in recent years.

Pharmaceutical and technology R&D companies that rely on innovative medicines and biotechnology as their core will naturally gain favor in the capital market. In 2017, four companies from the pharmaceutical and biotechnology sectors made it to the top 10 list of financing amounts. All four of these companies are innovative pharmaceutical or biotechnology firms.

Taking Rongchang Pharmaceutical, which made the list, as an example: Founded in 1993, Rongchang Pharmaceutical has, after more than 20 years of development, become a modern pharmaceutical enterprise integrating research and development (R&D), production, and sales, with operations spanning four major sectors: modern traditional Chinese medicine, biopharmaceuticals, contract development and manufacturing organization (CDMO) services for biological drugs, and incubation of biopharmaceutical enterprises and projects.

R&D on Endostar, a national Class I novel anti-tumor biologic (“vascular endothelial cell growth inhibitor”), commenced in 1998, and the new drug certificate was obtained in 2005. In 2008, RemeGen Co., Ltd. (Yantai) was established to develop innovative biologics targeting major human diseases such as cancer and autoimmune disorders.

RemeGen has developed RC48, a novel antibody-drug conjugate (ADC) targeting multiple cancers, including gastric cancer and breast cancer. It is the first ADC new drug in China to receive approval from the China Food and Drug Administration (CFDA) to enter clinical trials.

“Tai’ai” (RC18), a novel drug developed by RemeGen for autoimmune diseases such as systemic lupus erythematosus and rheumatoid arthritis, features independent intellectual property rights, with its molecular structure protected by global patents.

According to statistics, RemeGen currently has more than ten Class 1 novel antibody-based biologics in its research and development pipeline, three of which are in the clinical trial stage.

Driven by innovation trends, the pharmaceutical and biotechnology sectors are bound to attract the attention of capital markets. Their substantial R&D investment requirements also mean that these fields will become regular fixtures in the top 10 rankings for financing.

2010–2017: Changes in Financing Scale of the Overseas Healthcare Industry, Compiled by VCBeat

In 2017, there were 573 outbound investment deals, totaling RMB 109.8 billion.

Compared with 2016, the number of financing events in 2017 increased by 12%, while the total financing amount surged by 110%. The significant enhancement in fundraising capabilities across the five major sectors—biotechnology, pharmaceuticals, medical devices, healthcare informatics, and digital health—was the primary driver behind the rise in cross-border investment and financing scale in 2017.

Meanwhile, in 2014, the decline in investment projects within the broader health and healthcare informatics sectors led to a slowdown in the growth of overseas financing deals. Taking the healthcare informatics sector as an example, although the number of financing deals decreased, the total financing volume continued to grow steadily. This indicates that the overseas healthcare informatics industry is maturing; high-quality, mature projects still demonstrate strong capital-attracting capabilities, whereas early-stage projects are finding it increasingly difficult to enter this field.

2017: Financing Capacity by Sub-sector in the Overseas Healthcare Industry, Compiled by VCBeat Research Institute

In terms of fundraising momentum, biotechnology is the most sought-after sector, with both the number of financing deals and the total capital raised far exceeding those in other fields. Overseas investment activity is more inclined toward technology-driven niche segments.

2017: Major Overseas Health Industry Investment Projects, Compiled by VCBeat Eggshell Research Institute

Roivant in the pharmaceutical sector secured $1.1 billion in angel financing, marking the largest overseas funding round in 2017.

Biotechnology and pharmaceuticals demonstrate the strongest capital attraction, accounting for three spots in the Top 10.

The overall investment and financing levels of the top-ranked overseas healthcare companies are higher than those of their domestic counterparts, while the distribution of key sectors among the top rankings is largely similar to that of China’s financing leaderboard.