Japan's Pharmaceutical Retail Model as a Blueprint for China: Strict Separation of Medical and Pharmacy Services, Parallel Development of Specialized Pharmacies and Drugstore Chains, and the Rise of Chain Operations

Given their similar demographic structures and developmental backgrounds, Japan’s path of economic development has long been a key focus of study and research in China. Its policy formulation, technological accumulation, and industrial development processes offer valuable insights for the Chinese economy.

Against the broader macroeconomic backdrop, the historical development of Japan’s pharmaceutical industry has become a key focus of study in China. Its universal health insurance system, which shares similarities with China’s, along with measures such as promoting pharmaceutical innovation, compressing profit margins in distribution channels, and encouraging diversified operations in pharmaceutical retail, has culminated in Japan’s current high-quality pharmaceutical industrial base and a well-developed supply of medical and pharmaceutical services.

Focusing on the pharmaceutical retail segment, China’s pharmaceutical retail industry appears to be following the development path of Japan’s pharmaceutical retail industry.

VCBeat (WeChat ID: vcbeat) has provided a brief overview of Japan’s pharmaceutical retail industry and, in light of the tiered and classified management system for retail pharmacies currently being proposed in China, has forecasted future development trends in China’s pharmaceutical retail sector. The key insights are as follows:

1. Japan has implemented the separation of prescribing and dispensing with remarkable thoroughness, with approximately 70% of prescriptions being filled outside of medical institutions. For China’s ongoing healthcare reforms aimed at separating prescribing from dispensing, this figure serves as a significant benchmark.

2. Japanese pharmaceutical retail institutions are divided into dispensing pharmacies and drugstores; the former are equivalent to pharmacies spun off from medical institutions, primarily selling prescription drugs and insurance-covered medications, while the latter sell over-the-counter drugs and general merchandise. Against the backdrop of the separation between prescribing and dispensing, China’s pharmaceutical retail sector may also witness such a divergence.

3. Chain expansion is the inevitable path for the development of dispensing pharmacies and drugstores. With the number of retail pharmacies in China approaching saturation, mergers and acquisitions will be the dominant trend in the industry in the near future.

Separation of Medical Services and Drug Sales Drives Rapid Growth in the Retail Market

Similar to China, Japan also implements a universal health insurance system. Individuals pay insurance premiums at varying rates based on age and income, generally amounting to approximately 10% of their income, with the cost shared equally between the insured individual and their employer.

After medical expenses are incurred, 70% will be reimbursed for individuals under the age of 70, 80% for those aged 70–74, and 90% for those aged 75 and above.

Higher reimbursement ratios have placed considerable pressure on the operation of health insurance funds. In response, the Japanese government has adopted diversified cost-containment measures to curb the growth rate of medical expenditures and alleviate the strain on health insurance funds, with “separation of prescribing and dispensing” serving as a key strategy.

Japan has implemented the separation of medical services and pharmaceutical dispensing since the 1980s, focusing on two main pillars: “medical care” and “pharmaceuticals.” In terms of medical care, registration and consultation fees have been increased to reduce the proportion of drug revenue in the income of medical institutions and physicians. Meanwhile, a prescription dispensing fee has been established to incentivize doctors to prescribe medications for fulfillment at external pharmacies.

In terms of pharmaceuticals, the government leverages national health insurance reimbursement as a key mechanism to intervene in ex-factory drug prices. Drug price negotiations are generally conducted every two years, with the new health insurance reimbursement price determined based on a market benchmark price plus a specific coefficient. Regarding distribution, although the Japanese government does not impose restrictions on drug distribution prices, healthcare institutions and retail pharmacies procure drugs from distributors at prices below the benchmark. Markups within the distribution channel are constrained by market forces, and distributors’ profits primarily derive from manufacturer rebates and refined management achieved through economies of scale.

Through the above two pathways, Japan successfully achieved “separation of prescribing and dispensing.”

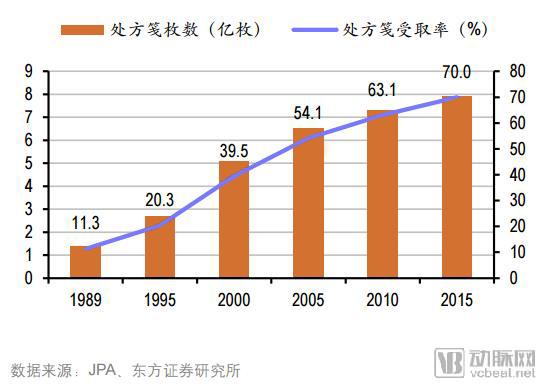

Data from the Japanese Pharmacists Association shows that the prescription acceptance rate, a key indicator of the separation of prescribing and dispensing, rose from 11.3% in 1989 to 70% in 2015. (Prescription acceptance refers to the process by which dispensing pharmacies accept prescriptions from medical institutions and complete the dispensing; it is a key indicator of the separation of prescribing and dispensing.)

Under these circumstances, Japan’s pharmaceutical retail market has steadily expanded. In the early 1990s, retail pharmacy sales accounted for only about 5% of the total pharmaceutical end-market; this share rose to approximately 40% by around 2000 and reached 54.3% by 2014. Correspondingly, the size of medical end-markets such as hospitals and clinics has continued to decline.

In addition, the Japanese government has further achieved cost-containment effects by guiding market uptake of generic drugs. In 2016, the Japanese government set a target for generics to account for 70% of the pharmaceutical retail market by 2017, with this figure slated to rise to 80% by 2020. This implies that profit margins in the pharmaceutical market are being further squeezed, thereby strengthening the impetus for the separation of prescribing and dispensing.

The background for implementing the separation of prescribing and dispensing in China is similar to that in Japan—driven by the need to control healthcare insurance costs. The pathways taken are also largely comparable, such as Beijing’s healthcare reform measures involving increased prices for medical services and transparent drug procurement, as well as group purchasing programs launched in Shanghai, Guangdong, and other regions. These initiatives lay the foundation for comprehensive separation of prescribing and dispensing. The only difference lies in the fact that China currently lacks pharmaceutical retail institutions equivalent to Japan’s dispensing pharmacies, resulting in limited capacity to handle outpatient prescriptions.

Dispensing Pharmacies and Drugstores Are Regarded as Equally Important

As previously mentioned, Japan’s pharmaceutical retail sector is divided into two types. Dispensing pharmacies are responsible for the sale of insurance-covered and prescription drugs, while drugstore chains primarily sell over-the-counter (OTC) medications, cosmetics, daily chemical products, and other general consumer goods.

In terms of scale, the two are comparable. According to data from Japan’s Ministry of Health, Labour and Welfare, the market size of dispensing pharmacies in Japan was approximately ¥7.2 trillion in 2015, while that of drugstores was around ¥6.1 trillion. (1 trillion = 1,000 billion)

Although the scale is similar, there are significant differences in market structure. The compounding pharmacy market has low concentration, whereas the drugstore/cosmetics store market exhibits high concentration.

According to data from the Ministry of Health, Labour and Welfare, there were 57,000 dispensing pharmacies in Japan in 2015. The top ten companies operated a combined total of more than 5,100 stores, accounting for less than 10% of the market. In terms of sales, the combined revenue of the top ten dispensing pharmacies reached ¥1 trillion, representing a market share of only around 14%.

Sales Performance of Japan's Top 10 Dispensing Pharmacies (2015)

Data Source: Mac-advisory, Orient Securities Research Institute

By comparison, the top ten drugstore chains operate a combined total of approximately 9,700 stores, accounting for around 60% of the 17,500 stores nationwide, with a market size of JPY 3.67 trillion, representing a 61% share.

Sales Performance of Japan's Top 10 Drugstore Chains (2015)

Data Source: Mac-advisory, Orient Securities Research Institute

The low market concentration in the dispensing pharmacy sector is attributed to the fact that, under the Japanese government’s drug price controls, profit margins for prescription drugs have been significantly compressed. This has led to sluggish growth in the market size of dispensing pharmacies, limiting the profit potential for large enterprises and hindering their mergers and acquisitions (M&A) activities. Additionally, dispensing pharmacies typically maintain contractual relationships with hospitals, forming interest alliances that serve as a barrier to entry for external competitors. However, as profit margins continue to shrink, some independent dispensing pharmacies are finding it increasingly difficult to sustain operations, gradually driving the industry toward consolidation. In 2016, more than 1,000 dispensing pharmacies were acquired, signaling an impending shift in the landscape of Japan’s dispensing pharmacy sector.

The high market concentration in the drugstore sector is closely related to the nature of its product offerings. These stores primarily carry over-the-counter (OTC) medicines, cosmetics, and daily sundries, which are akin to fast-moving consumer goods (FMCG) and require sustained marketing efforts to engage customers. Chain operations ensure the consistency and continuity of these marketing activities, enabling larger enterprises to more easily establish brand recognition.

Policy has also significantly influenced the development of two business models: dispensing pharmacies and drugstores. The most recent major adjustment was the enactment of the Revised Pharmaceutical Affairs Law in 2009. This policy streamlined the existing regulatory framework for drug sales, categorizing pharmaceuticals into prescription drugs, over-the-counter (OTC) preparations, and general-use medicines. For general-use medicines, the requirement for licensed pharmacists was relaxed, allowing registered sales personnel to conduct sales. This change substantially enhanced the flexibility of pharmaceutical retail and directly promoted its growth.

Driven by policy and market forces, dispensing pharmacies and drugstores have adopted divergent development models. Dispensing pharmacies have become more focused on building capabilities in prescription drugs and pharmaceutical care services, gradually expanding into light medical services with enhanced specialization.

Drugstore chains are pivoting toward broader health-and-wellness products and fast-moving consumer goods (FMCG). For example, Matsumoto Kiyoshi, the top-ranked drugstore chain, launched a new store concept called Beauty U in Tokyo, moving away from the traditional mixed-retail model that combines pharmaceuticals, cosmetics, and food, and making a comprehensive push into the cosmetics sector. Matsumoto Kiyoshi’s entry into the cosmetics market has prompted fresh reflections within Japan’s drugstore industry: leveraging established brand equity to expand into the consumer goods sector, thereby further advancing diversified business models.

China’s Pharmaceutical Retail Sector to Follow Japan’s Path

From the perspective of the current state of China’s pharmaceutical retail industry, there are many similarities with the Japanese market. First, influenced by policy reforms, the separation of prescribing and dispensing is gradually being implemented, requiring retail pharmacies to accommodate prescription outflows. Pressure from medical insurance cost containment remains, resulting in low growth rates for the overall pharmaceutical terminal market and further compression of profit margins. Second, market saturation is extremely high, necessitating internal resource integration and diversified operations to identify new profit growth points. Potential expansion paths include dermocosmetics and supermarket-style operations.

According to the statistical bulletin issued by the China Food and Drug Administration, as of the end of November 2016, there were 220,700 retail chain pharmacy outlets and 226,300 independent retail pharmacies, totaling 447,000 stores, with each store serving approximately 3,100 people. The standard for pharmacy saturation in developed countries is one store per 2,500 people, while in Japan it is approximately one store per 1,700 people. Given China’s high urbanization rate and concentrated population distribution, the number of pharmaceutical retail outlets in China has approached saturation. In fact, even a slightly rational observer would concur with this assessment after a brief market survey: in regional central cities, there is nearly one pharmacy every 200 meters.

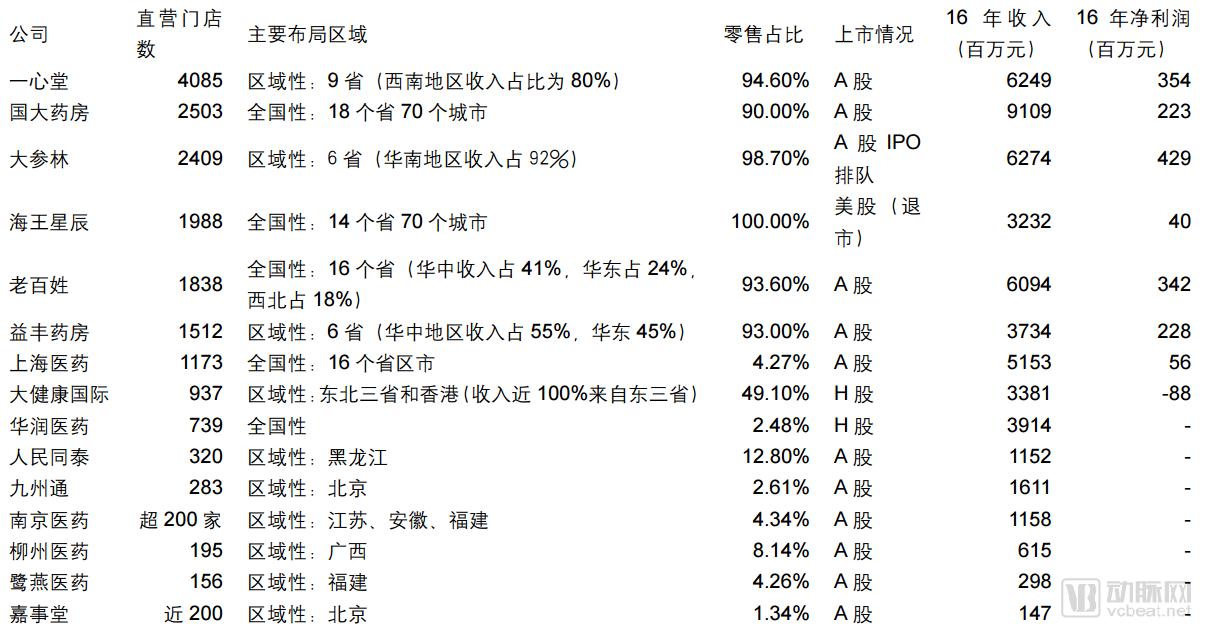

However, similar to the market structure of Japan’s dispensing pharmacies, the concentration of China’s pharmaceutical retail market remains low. According to data from the Ministry of Commerce, in 2016, the top 100 pharmaceutical retail enterprises by sales operated a total of 54,300 stores, accounting for 12.2% of all stores nationwide; their sales revenue reached RMB 107 billion, representing 29.1% of the total retail market size; and the combined market share of the top three retailers was merely 6.7%.

Overview of Data on Major Domestic Pharmaceutical Retail Enterprises

Data source: Orient Securities

Therefore, recent industry policies have been dedicated to promoting an increase in the chain affiliation rate of pharmaceutical retail. For instance, the "Development Plan for the Pharmaceutical Distribution Industry (2016–2020)" stated that the pharmaceutical retail chain affiliation rate should exceed 50% by 2020. Meanwhile, the increasingly stringent regulatory and industrial environments have made independent pharmacies and small-scale chains more willing to align with industry giants, with franchising or mergers and acquisitions becoming highly cost-effective exit strategies. All these factors will contribute to greater industry consolidation.

Under the broader policy framework, there is a relatively “invisible” policy that is easily overlooked by the market: the classified and graded management of retail pharmacies. This concept first appeared in 2012, when the Department of Market Order under the Ministry of Commerce issued the Code of Practice for Retail Pharmacy Operations and Services, proposing the implementation of classified and graded management for pharmacies. Retail pharmacies are to be rated based on criteria such as business area, pharmaceutical care capabilities, drug supply capacity, and staffing levels. A clear similarity can be observed between this approach and Japan’s Pharmaceutical Affairs Act amendments. Subsequently, regions including Beijing, Hubei, and Shandong successively promulgated trial measures, but these were not rolled out nationwide.

The “2017 Healthcare Reform Task List” proposed piloting a classified and tiered management system for retail pharmacies, encouraging the development of chain pharmacies, and exploring the interconnectivity and real-time sharing of prescription information from medical institutions, health insurance settlement data, and pharmaceutical retail consumption records. This indicates that regulators intend to emphasize the linkage between the classified and tiered management of retail pharmacies and the outflow of prescriptions and integration with health insurance systems, which will have a profound impact on the future development of the pharmaceutical retail industry.

Will China’s pharmaceutical retail industry also evolve toward the Japanese model in the future? Specifically, a strict separation between medical care and drug dispensing, with parallel development of professional pharmacies and drugstore-cosmetic retailers, and chain operations becoming the mainstream. Currently, this appears to be a highly probable scenario.

References

Oriental Securities - In-Depth Report on the Pharmaceutical and Biotechnology Industry: Prescription Outflow Drives Growth in Pharmacy Sales, While Regulatory Upgrades and Asset Securitization Spur Consolidation of Existing Assets

Huachuang Pharma Japan Pharmaceutical and Biotech Industry Observation (Issue 6): Pharmaceutical Distribution, Carrying the Future