Capital Rush in China's Pharmacy Chain Sector: Billions Invested and Thousands of Stores Acquired Amid Industry Consolidation

Between 2012 and 2017, nearly 50,000 independent retail pharmacies “disappeared.”

Statistics from the China Food and Drug Administration show that in 2012, there were 271,000 independent retail pharmacies and 152,000 chain pharmacy outlets across China; by 2017, the number of independent retail pharmacies had sharply declined to 226,000, while chain pharmacy outlets had grown to 220,000.

The pharmaceutical retail sector is undergoing a shift characterized by the decline of independent pharmacies and the rise of chain stores, with mergers and acquisitions serving as the primary driver behind this trend.

According to incomplete statistics from VCBeat (WeChat ID: vcbeat), in recent years, professional investment institutions such as Tianyi Capital, GF Xinde, and Hillhouse Capital, along with industrial enterprises including GPC Baiyunshan, Tasly Group, and Buchang Pharmaceuticals, have been actively participating in investments and mergers and acquisitions within the pharmaceutical retail sector. Coupled with listed pharmaceutical retail companies intensifying their acquisition of small chain pharmacies, the “land grab” campaign in the pharmaceutical retail industry has been unfolding with great momentum.

Capital's Predatory Hunt for Pharmacies

In fact, capital participation in the M&A and consolidation of the pharmaceutical retail industry has a long history. As early as 2004, Nepstar signed a $40 million investment agreement with Goldman Sachs, a globally renowned investment bank, becoming the first domestic pharmaceutical retail enterprise to accept direct foreign investment.

Subsequently, domestic investment firms also began to participate in investments in retail pharmacies. Behind the major publicly listed retail pharmacy chains are now prominent professional investment firms.

In 2007, LBX Pharmacy received a RMB 423 million investment from Zexing Investment. By the time LBX Pharmacy listed on the Shanghai Stock Exchange in 2015, Zexing Investment held a 46.42% stake in LBX Pharmacy, making it the largest shareholder. Currently, Zexing Investment still holds a 32.58% stake in LBX Pharmacy, with a securities value of approximately RMB 6 billion.

In 2008, Capital Today injected RMB 200 million into Yifeng Pharmacy. Currently, Capital Today still holds approximately 21% of Yifeng Pharmacy’s shares. Based on Yifeng Pharmacy’s current market capitalization, the value of Capital Today’s stake has exceeded RMB 3 billion.

In 2010, Legend Capital, Hony Capital, and Bailihong Venture Capital acquired 6.62%, 4.95%, and 0.99% equity stakes in Yunnan Hongxiang Yixintang, respectively, through capital increases and equity transfers, with Legend Capital investing approximately RMB 100 million. To date, Legend Capital remains one of the top ten shareholders of Yixintang, holding a 1.01% stake. Based on a 5% reduction and the 52-week average share price, Legend Capital has gained at least RMB 600 million from this investment.

In 2015, Morgan Stanley injected RMB 410 million into Dashenlin Pharmaceutical Group, acquiring a 6% stake, at which time Dashenlin was valued at RMB 6.8 billion. By January 2018, Dashenlin’s valuation had reached RMB 20.5 billion, significantly boosting the value of Morgan Stanley’s holdings.

Beyond the aforementioned cases, professional investment institutions are also behind regional retail giants such as Yunnan Jianzhijia, Shandong Shuyu Pingmin, and Hebei Xinxing Pharmacy, all of which are awaiting their market listings. These investors are expected to reap substantial returns following their public debuts.

Why Is Capital So Keen on Investing in Pharmaceutical Retail? VCBeat Consulted Qiu Min, a Pharmaceutical Analyst at Huachuang Securities, Who Stated That Capital Has Always Been Optimistic About Pharmaceutical Retail and Has Seen a Small Surge Recently.

Capital favors pharmaceutical retail for three main reasons: first, it is a business model with low barriers to entry, making market access relatively easy; second, the domestic pharmaceutical retail industry has a low concentration ratio, and capital infusion can facilitate industry consolidation; third, favorable policies support the development of retail pharmacies, such as the relaxation of medical insurance accreditation reviews and opportunities for prescription outflow driven by the separation of prescribing and dispensing.

The pharmaceutical retail industry is a unique consumer sector characterized by low purchase frequency, high gross margins, and low market concentration. In terms of purchase frequency, retail pharmacies receive approximately 50 customers per day, which is lower than convenience stores and supermarkets. Regarding profit margins, the average profit margin in pharmaceutical retail stands at around 30%, with large chain pharmacies achieving margins as high as 40%. As for market concentration, the revenue concentration of directly operated stores among China’s top 100 pharmaceutical retailers is only about 20%, significantly lower than the levels observed in developed countries.

Notably, the density of retail pharmacies in China is already very high. Based on 2016 data, with a population of 1.375 billion and 446,000 pharmacies, the ratio was approximately 3,082 people per pharmacy, whereas the “saturation standard” in developed countries is 2,500 people per pharmacy. Given China’s high urbanization rate and concentrated population distribution, the number of pharmaceutical retail outlets has approached saturation. This implies that, barring significant demographic shifts, opening new stores will no longer be the primary avenue for entering the pharmaceutical retail industry.

In terms of market concentration, data from the Ministry of Commerce shows that in 2016, the top 100 pharmaceutical retail enterprises in China operated a total of 54,300 stores, accounting for 12.2% of the national store count; their sales revenue reached RMB 107 billion, representing 29.1% of the total retail market; and the combined market share of the top three retailers was only 6.7%. In contrast, the chain store penetration rate in the United States is approximately 75%, with the top three companies holding more than 80% of the total market share. There is still significant room for improvement in China’s chain store penetration rate and market concentration.

Therefore, recent industry policies have been dedicated to promoting an increase in the chain affiliation rate of pharmaceutical retail. For instance, the “Development Plan for the Pharmaceutical Distribution Industry (2016–2020)” stated that the pharmaceutical retail chain affiliation rate should exceed 50% by 2020. Meanwhile, the increasingly stringent regulatory and industrial environments have made independent pharmacies and small-scale chains more willing to join forces with industry giants, making franchising or being acquired a highly rational exit strategy. All these factors will contribute to enhancing industry concentration.

It is also essential to address the impact of policy on the retail sector, particularly the outflow of prescriptions driven by the separation of prescribing and dispensing. Global experience indicates that separating prescribing from dispensing is an inevitable trend. The United States has implemented a relatively thorough separation, with approximately 60–70% of medications sold through non-hospital channels (pharmacies, Pharmacy Benefit Managers [PBMs], and mail-order services). Japan has practiced this separation for over 40 years, with currently around 70% of prescription drugs dispensed through outpatient channels. The experiences of the United States and Japan provide valuable references for estimating the scale of prescription outflow in China.

VCBeat previously conducted a preliminary estimate, projecting that by 2018, the outflow of prescription drugs would generate an incremental market value of over RMB 130 billion to RMB 165 billion in the out-of-hospital sector. Adopting a more conservative approach and lowering the target figure, the scale of prescription outflow in 2018 would still amount to at least RMB 100 billion. Such promising prospects have naturally attracted significant capital investment targeting retail pharmacies.

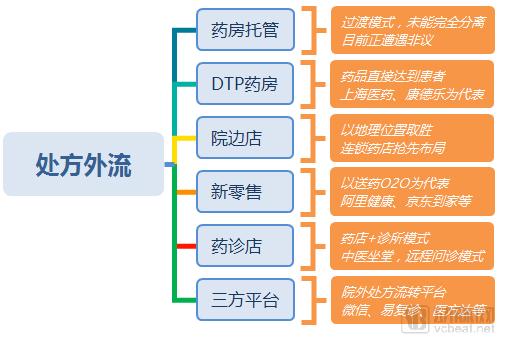

Another noteworthy trend is the rise of pharmacy trusteeship, DTP (Direct-to-Patient) pharmacies, new retail models, and integrated pharmacy-clinic formats within the pharmaceutical retail industry. This structural adjustment has also created opportunities for capital investment in the sector.

So, what will capital injection bring to the pharmaceutical retail industry? First, it will lead to a clear ownership structure and refined management; second, it will provide support in terms of M&A integration expertise and funding.

Retail enterprises that attract capital investment are typically regional leaders with an established business foundation, yet there remains significant room for optimization in their ownership structure and management models. This is akin to internet companies in their early stages, where the founding team lays the operational groundwork; once operations stabilize and follow a clear trajectory, professional managers with experience in large-scale corporate management are brought on board to safeguard sustainable growth. In this sense, capital serves as a crucial ally in helping retail enterprises scale up and strengthen their competitive edge.

The substantial cash reserves brought by capital have also provided ample ammunition for the consolidation of retail pharmacies. In the pharmaceutical retail sector, operating cash flow is not abundant, and external mergers and acquisitions require significant funding. Commercial borrowing or bank loans would impose considerable financial costs and repayment pressures on enterprises, whereas cash injected through equity investment by capital firms avoids these burdens.

Zhang Dingding, Marketing Director at Haoyaoshi, also believes that capital participation in the consolidation of pharmaceutical retail will objectively drive the integration of independent pharmacies and regional chains, facilitating unified regulatory oversight. The financial and management expertise brought by capital will help enhance the service capabilities of retail enterprises, leading to changes in their operational structures. These enterprises will offer diversified value-added services centered on pharmaceuticals, such as appointment scheduling and consultations, health management, and new retail models featuring online ordering with in-store pickup or delivery.

Which Capital Is Investing in Pharmaceutical Retail?

Which Capital Firms Are Investing in Pharmaceutical Retail? VCBeat Provides an Overview.

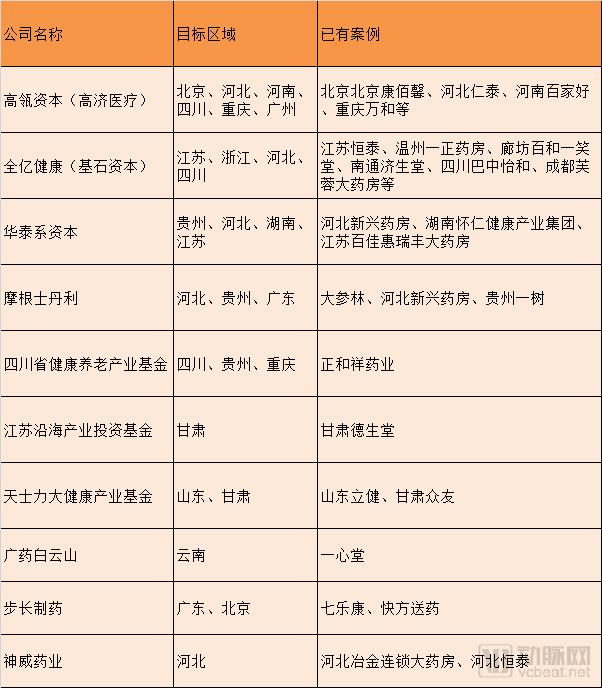

Hillhouse Capital (Gaoji Medical)

Hillhouse Capital Group, founded in 2005, is a firm dedicated to long-term structural value investing. After more than a decade of development, Hillhouse has become one of the largest investment funds in Asia by assets under management. The capital entrusted to Hillhouse primarily comes from global institutional investors, including endowments of top-tier universities worldwide, sovereign wealth funds, pension funds, and family offices. Hillhouse Capital’s successful investment portfolio includes internet companies such as Baidu, Tencent, and JD.com, as well as industrial enterprises like Gree Electric, ZTO Express, and Jiangxiaobai.

In August 2017, Gaoling Healthcare, a subsidiary of Hillhouse Capital focused on strategic investment and operations in the healthcare sector, entered into strategic partnerships with Chongqing Wanhe, Sichuan Dongsheng, Chengdu Huaxing Pharmacy, and Beijing Kangbaixin Pharmacy.

A review of business registration records by VCBeat also revealed that, in addition to the aforementioned chains, pharmaceutical retail companies in which Gaoji Medical has made external investments include Guangdong Bangjian, Hebei Rentai, and Henan Baijiahaoyisheng.

Quanyi Health (CITIC Capital)

Quanyi Health can be described as a “dark horse” in investment within the pharmaceutical retail sector, characterized by its frequent mergers and acquisitions and extensive regional coverage.

Since its establishment in 2016, it has successively acquired Jiangsu Hengtai, Wenzhou Yizheng Pharmacy, Langfang Baihe Yixiaotang, and Nantong Jishengtang. In 2017, Quanyi Health further acquired pharmaceutical chain enterprises such as Wenzhou Yetongren, Changzhou Zhongcheng Pharmacy, Sichuan Bazhong Yihe, and Chengdu Furong Grand Pharmacy.

The shareholders behind Quanyi Health are CDH Investments and Hony Capital, while its core management team hails from Neptune Star, Sinopharm Holding, and investment institutions.

Cornerstone Capital is one of the earliest-established private equity firms in China, with healthcare investment cases including Conba, Zhongshan Bailing, and Dakang Medical. Hony Capital, a member of Legend Holdings, manages funds exceeding RMB 10 billion and has years of experience in industrial M&A and capital operations. Together, Cornerstone Capital and Hony Investment have provided Alljoy Health with billions of yuan in funding to support the nationwide acquisition of pharmaceutical retail chains.

“Capital + Management” is the core investment logic of Quanyi Health. By integrating regional leading chain enterprises to form urban oligopolies, optimizing operational structures, and introducing information technology and internet tools, it expands the business performance of its portfolio companies.

According to its official information, by the end of 2017, Quanyi Health Holdings had over 2,000 pharmacies, with sales exceeding RMB 6 billion in 2017 and projected to surpass RMB 8 billion in 2018.

Huatai-affiliated Capital

The parent company of the Huatai-affiliated capital entities is Huatai Securities, formerly known as Jiangsu Securities Company. Its subsidiary, Huatai Zijin Investment, serves as the primary platform for the Huatai group’s investments in the pharmaceutical sector.

In 2015, Huatai Zijin made a strategic investment in Guizhou Yishu Chain Pharmacy. In 2016, it successively signed strategic cooperation agreements with multiple pharmacy chains, including Hebei Xinxing Pharmacy, Hunan Huairen Health Industry Group, and Jiangsu Baijiahui Ruifeng Pharmacy.

Notably, the capital contributors to the Huatai-affiliated entities are not limited to Huatai alone. Through the establishment of a healthcare industry fund, it has attracted investments from Jinshiyuan Liquor, Suning Appliance, Wanchuan Medical, and others, with fundraising efforts ongoing.

All companies invested in by the Huatai Group are regional leaders with annual operating revenues of approximately RMB 1 billion. The capital injection from the Huatai Group will facilitate further expansion for these enterprises, with an exit strategy pursued through initial public offerings (IPOs).

Morgan Stanley

As previously mentioned, Morgan Stanley injected RMB 410 million into Dashenlin Pharmaceutical in 2015. In early 2016, Morgan Stanley jointly invested in Guizhou Yishu Pharmacy with Dashenlin; subsequently, in August of the same year, it made a strategic investment in Hebei Xinxing Pharmacy.

Notably, Hebei Xinxing Pharmacy and Guizhou Yishu are also portfolio companies invested by Huatai-affiliated capital, indicating that investors apply consistent selection criteria and pursue deliberate synergies when investing in pharmaceutical retail chains.

As a globally renowned financial services and investment institution, Morgan Stanley’s participation in the M&A consolidation of China’s pharmaceutical retail enterprises undoubtedly holds exemplary significance for the industry. Its deep involvement will also bring “international experience” to domestic investment firms engaging in M&A consolidation within the pharmaceutical retail sector.

Sichuan Provincial Health and Elderly Care Industry Fund

In late 2017, it was reported that Sichuan Health and Elderly Care Industry Equity Investment Fund Partnership (Limited Partnership) invested in Guizhou Zhenghexiang Pharmaceutical Group, with an investment scale of nearly RMB 1 billion.

The Sichuan Health and Elderly Care Industry Fund is a government-guided industrial fund initiated by Sichuan Juxin Development Equity Investment Fund Management Co., Ltd., the Finance Bureau of Chengdu High-Tech Zone, and Sichuan Equity Development Investment Fund Management Co., Ltd., making it a veritable “national team.”

Although neither party disclosed further investment details, business registration records indicate that Zhenghexiang Pharmaceutical completed a share pledge worth RMB 11.9511 million on December 6, 2017, with the Sichuan Health and Elderly Care Industry Fund as the pledgee. Given Zhenghexiang Pharmaceutical’s registered capital of RMB 39.837 million, this pledge represented approximately one-quarter of its equity.

Zhenghexiang Pharmaceutical was formed in 2015 through the consolidation of multiple retail pharmacies across Guizhou, Sichuan, Hunan, and other regions. With over 1,000 pharmacy outlets in Guizhou, Sichuan, Hunan, Chongqing, and surrounding areas, the company generates annual revenue of RMB 3 billion and ranks among China’s Top 50 Pharmacy Chains. Following the entry of state-backed funds, Zhenghexiang is poised to undertake further initiatives in regional pharmacy consolidation and branded operations.

Jiangsu Coastal Industrial Investment Fund

State-backed entities are entering the pharmaceutical retail sector, with the Sichuan Provincial Health and Elderly Care Industry Fund being just one example.

In August 2017, Jiangsu Coastal Industry Investment Fund and Nanjing Bangsheng Investment Company jointly invested in Gansu Deshengtang. The Jiangsu Coastal Industry Investment Fund was initiated by Ping An Innovation Capital, Bangsheng Investment, Jiangsu Coastal Development Group, and Jiangsu High-Tech Venture Capital Group, among others, and is an industry investment fund with government capital participation.

Gansu Deshengtang was established in September 1999. After nearly two decades of continuous development, it has become a modern, group-based chain enterprise specializing in pharmaceutical and healthcare services. Its business covers multiple fields, including pharmaceutical retail, pharmaceutical wholesale, medical services, internet B2C, B2B, O2O, and telemedicine.

Currently, Deshengtang operates over 500 chain stores across more than 30 cities in nearly 20 provinces and municipalities throughout China, with annual sales exceeding RMB 1 billion. Bolstered by capital investment, Deshengtang has embarked on a nationwide expansion and a diversified business strategy, having entered markets such as Beijing and launched e-commerce operations.

Tasly Grand Health Industry Fund

As another pharmaceutical retail giant in Northwest China, Gansu Zhongyou Health has also received capital support. In September 2016, Zhongyou Health secured a RMB 500 million investment from the Tasly Great Health Industry Fund.

The Tasly Great Health Industry Fund is a health industry fund with a total size of RMB 5 billion, jointly established by Taikang Life Insurance as the lead investor, and Zhongyuan Bank and Tasly as co-investors.

Tasly Capital’s industrial fund has extensive experience, having launched five RMB-denominated funds and three USD-denominated funds, with total capital raised exceeding RMB 10 billion. Guided by the investment philosophy of “industry + capital,” it aims to build an ecosystem for the big health industry. To date, it has invested in over 50 projects, spanning multiple sectors including pharmaceuticals and biotechnology, pharmaceutical retail, and healthcare services.

Zhongyou Health was established in 1996. In 2015, leveraging an innovative M&A-driven growth model, Zhongyou Health rapidly acquired and integrated more than 30 chain pharmacy enterprises across Shaanxi, Gansu, Ningxia, Qinghai, and Xinjiang within just one year. It quickly grew into an industry-leading company with annual operating revenue of RMB 2.56 billion and over 800 stores, with total operating revenue projected to reach RMB 3.5 billion in 2016.

Zhongyou Health stated that, with the support of the Tasly Grand Health Industry Fund, it will expand its nationwide presence more extensively by selecting one to three high-quality small and medium-sized pharmacy chains in target provinces and binding them to its public listing through equity swaps.

Overview of Capital Participation in M&A and Integration in Pharmaceutical Retail

By capital type, pharmaceutical industrial companies such as GPC Baiyunshan, Buchang Pharma, and Shineway Pharmaceutical; industrial investors including Matrix Partners China, GGV Capital, Zhongwei Fund, Hejun Capital, and Huakang Fund; and listed pharmaceutical retail chains like Yixintang, Yifeng Pharmacy, and Laobaixing Pharmacy have all rushed to stake out territory in the pharmaceutical retail sector.

In December 2017, Baiyunshan subscribed to approximately RMB 800 million worth of newly issued shares in Yixintang. Buchang Pharmaceutical invested in the pharmaceutical e-commerce enterprise Qilekang in 2015 and, in April 2017, invested in the pharmaceutical O2O company Kuai Fang Songyao. Meanwhile, Shenwei Pharmaceutical has been expanding its presence in Hebei Province since 2015, successively acquiring and investing in multiple local pharmaceutical chain enterprises, covering nearly 700 stores with annual sales exceeding RMB 1.4 billion.

Industrial capital has heavily invested in pharmaceutical e-commerce enterprises; for instance, IDG Capital, SoftBank China, and Shengtai Investment have invested in Shanghai Pharma Cloud Health, while Tus-Holdings Venture Capital, Jiangsu Gaoke, and Changjiang Guohong have invested in Qilekang.

Listed pharmaceutical retail companies have been aggressively expanding their market share. Taking Yixintang, known as the “M&A Maniac,” as an example, it operated more than 2,400 stores before its IPO in April 2014. After going public, the company pursued multiple mergers and acquisitions, bringing its store count to over 5,000 by the third quarter of 2017—more than doubling its previous number. While maintaining a focus on Southwest China, Yixintang has extended its reach across the country.

Several Hypotheses on Capital Taking Control of Pharmaceutical Retail

Hypothesis 1: Can Regional Integration Achieve Success Through a Single Consolidation?

Capital participation in mergers, acquisitions, and consolidation within the pharmaceutical retail sector will undoubtedly drive up industry concentration in the short term. However, consolidation is merely the first step. For dealmakers, ensuring the thorough integration of acquired resources involves addressing a wide range of challenges—including clashes in corporate culture between different enterprises, power transitions between new leadership and incumbent executives, clarification of management structures, alignment of responsibilities, authority, and interests, and adjustments to business strategies. These issues require time to resolve, and a prolonged period of digestion is expected to follow this wave of consolidation.

Hypothesis 2: How Will the National Market Landscape Change?

Currently, there are more than ten pharmaceutical retail enterprises with extensive national coverage in China, such as Yixintang, Laobaixing, Yifeng, and Dashenlin, whose pharmacy networks span the entire country. Additionally, each region has its own local leaders, including Shandong Lijian, Hebei Emerging Pharmacy, Henan Zhang Zhongjing, Hubei Tianji, and Sichuan Derentang. As the pace of mergers and acquisitions in the pharmaceutical retail industry accelerates, independent pharmacies and small-to-medium-sized chains will inevitably be absorbed to varying degrees in the future.

The future landscape of China’s pharmaceutical retail sector will be characterized by a few nationwide enterprises alongside regional leaders, with mutual checks and balances between the national giants and regional frontrunners.

Hypothesis 3: How long after integration can the product be launched on the market?

2017 was regarded as the year that reignited the “IPO wave” for pharmaceutical retail companies. Following the surge in IPO applications by pharmaceutical retailers in 2014, Dashenlin, Shuyu Pingmin, and Jianzhijia made another push for public listings in 2017. Among them, Dashenlin successfully passed the regulatory review and has since become the pharmaceutical retailer with the highest market capitalization.

Although many integrated pharmaceutical retail enterprises have already met the listing standards of the China Securities Regulatory Commission (key financial indicators: positive net profits for the last three fiscal years with a cumulative total exceeding RMB 30 million, operating cash flow exceeding RMB 50 million, or cumulative revenue exceeding RMB 300 million), the failed attempts of some pharmaceutical retail companies to go public have offered valuable lessons for later entrants.

The China Securities Regulatory Commission (CSRC) primarily focuses on issues such as payment collection, related-party transactions, taxation, store registration procedures, financial compliance, medical insurance, and profitability levels when reviewing pharmaceutical retail companies for approval.

Capital participation in the M&A and consolidation of pharmaceutical retail is undoubtedly driven by the objective of exiting through an initial public offering (IPO). If the aforementioned issues cannot be resolved, IPO plans will be significantly impacted. This aligns with the first hypothesis: mere simple mergers will fail to achieve standardized and large-scale operations. It is anticipated that after extensive capital involvement in the M&A and consolidation of pharmaceutical retail, two to three years will be required to address these issues, and this wave of “IPO listings” will continue until around 2020.

In summary, from a capital perspective, pharmaceutical retail represents a high-quality sector with relatively low entry barriers and significant return potential. Given its favorable long-term growth trajectory, investors can proactively position themselves in relevant targets to capitalize on the dividends of industry upgrading. For retail enterprises, introducing strategic investors can expand M&A capital, optimize operational structures, and pilot new business models, thereby laying the groundwork for diversified development and asset securitization.

References

Key Focus Areas of CSRC Review for Chain Pharmacy IPOs_Sohu Finance_Sohu.com

http://www.sohu.com/a/193110486_618578

Opportunities in Prescription Outflow: Market Size to Reach RMB 160 Billion in 2018, Benefiting Retail Pharmacies with DTP Model Gaining Favor

http://vcbeat.top/NDQ2MWM3Yjg2OWJmYjJlZjE5ZTEyZWViOTgyMmZiMjg=

Oriental Securities - In-Depth Report on the Pharmaceutical and Biotechnology Industry: Prescription Outflow Drives Growth in Pharmacy Sales, While Regulatory Upgrades and Asset Securitization Spur Consolidation of Existing Assets

Guosen Securities - Special Research on Chain Retail Pharmacies (Part I): Riding the Spring Breeze of Healthcare Reform, Welcoming the Outflow of Prescriptions

Huachuang Medicine Japan Pharmaceutical and Biotech Industry Observation (Issue 6): Pharmaceutical Distribution, Carrying the Future