StartUp Health Releases 2017 Digital Health Investment Report Highlighting $11.5B in Funding, Primarily Flowing to Mid-to-Late Stage Ventures

StartUp Health, a renowned U.S.-based digital health startup accelerator, recently released its 2017 Global Digital Health Investment and Financing Report, revealing that disclosed funding in the digital health sector reached $11.5 billion in 2017.

While summarizing the state of affairs in 2017, StartUp Health also forecasted healthcare development trends for 2018. VCBeat (WeChat ID: vcbeat) promptly compiled and organized the details.

10 Major Health Moonshot Initiatives

As the concept of StartUp Health’s Health Moonshots gains widespread acceptance, a new generation of entrepreneurs, investors, industry leaders, and governments will face more daunting challenges. Below are the ten major Health Moonshots:

1. Nursing Channel Expansion Plan

To provide high-quality nursing care for every individual, regardless of their location or socioeconomic status.

2. Zero-Cost Nursing Plan

Fundamentally reduce healthcare costs.

3. Disease Cure Plan

Curing Diseases with Data, Technology, and Customized Medications.

4. Termination of Cancer Programs

End the Erosion of Cancer on Patients.

5. Women's Health Program

Prioritizing Women's Health: Advocating for Preventive Care and Launching New Research.

6. Child Health Program

Ensure that every child has access to high-quality care, particularly in regions with scarce medical resources and medications.

7. Nutrition and Fitness Plan

Provide a healthy environment for people and support an active lifestyle.

8. Brain Health Program

Unlocking the Mysteries of the Brain to Enhance Physical and Mental Health.

9. Mental Health and Well-being Program

Pursuing holistic well-being of the mind, body, and spirit.

10. Life Extension Program

Extend human healthspan by 50 years.

2017 Year-End Summary

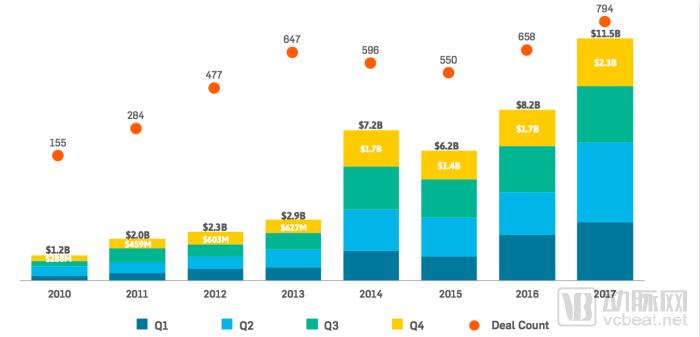

In 2017, digital health investment hit a new high.The total financing amount for 794 transactions reached $11.5 billion. Thus, digital health financing has entered a more mature phase. Early transaction activity fueled the entrepreneurial wave and the now-mature market, while later-stage opportunities have attracted new investment from around the globe.

In terms of financing and M&A activities in digital health, 2018 will be a year of breakthrough achievements, with previous efforts driving new progress.

1. A Historic Year

Global investment exceeded $11.5 billion, with 2017 marking the highest funding year to date, surpassing 2016 by nearly $3.5 billion.

2. Q4 with the Largest Financing Amount

The fourth quarter of 2017 was the highest-funded Q4 on record, with 227 deals totaling $2.3 billion. November and December 2017 were the months with the highest total financing to date, with December’s financing volume nearly double the average level of previous years.

3. Early-stage financing did not decline

The tech industry warned of an early downturn in the second half of 2017, but digital health investment has remained active. Although the median deal size for seed and Series A financing rounds has declined, the total number of transactions has continued to increase.

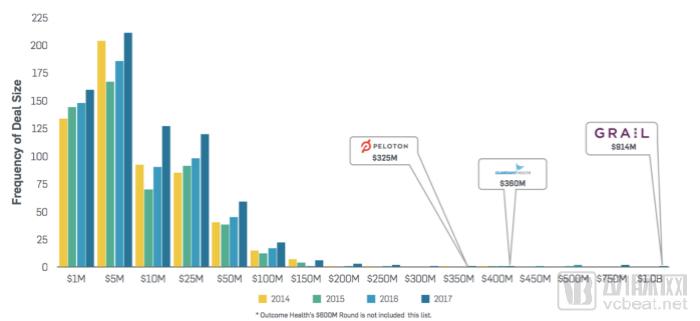

4. Growth Across Transactions of All Sizes

In 2017, sustained growth in financing drove transaction volumes across all scales to record highs, with deal sizes ranging from $1 million to $100 million. Capital was available at every stage for entrepreneurs with strong value propositions.

5. The Surging Series B Financing Round

Over the past four years, the median size of Series B transactions has steadily increased. In 2017, the total value of 94 deals reached $15 million, compared to 80 deals in 2016. As capital was concentrated in early-stage deals the previous year, the rise in later-stage investments indicates that investment in the digital health industry has matured.

6. Global Opportunities Are on the Rise

StartUp Health’s report has, for the first time, revealed the most internationally active regions for investment in 2017. The top five regions span multiple countries, indicating that entrepreneurs and investors are faced with global opportunities in the digital health sector.

Financing Overview: Year-over-Year Comparison

To date, 2017 was the most active year for digital health financing, with a record 794 transactions totaling over $11.5 billion in funding.

The fourth quarter of 2017 also saw record-breaking figures, with a total of 227 transactions exceeding $2 billion—the highest single-quarter total in history. With growing global market opportunities and increasing demand for innovation, high-quality entrepreneurs are flocking to the sector. As digital health remains in the early stages of its innovation cycle, we anticipate that substantial capital will continue to flow into this industry in 2018.

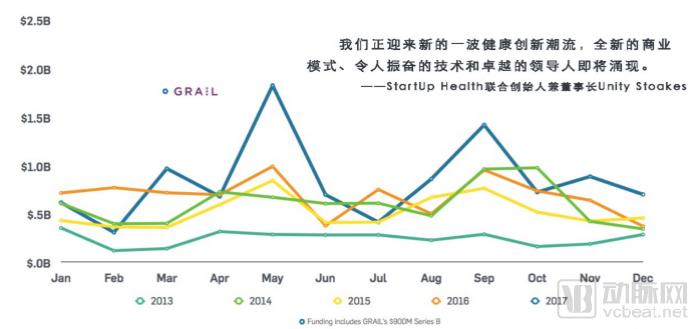

Financing Overview: Monthly Comparison

In May and September 2017, financing amounts reached $2 billion and $1.5 billion, respectively, including multiple deals exceeding $100 million. These large-scale transactions made 2017 a record-breaking year. As more companies mature, mega-deals are expected to continue in 2018.

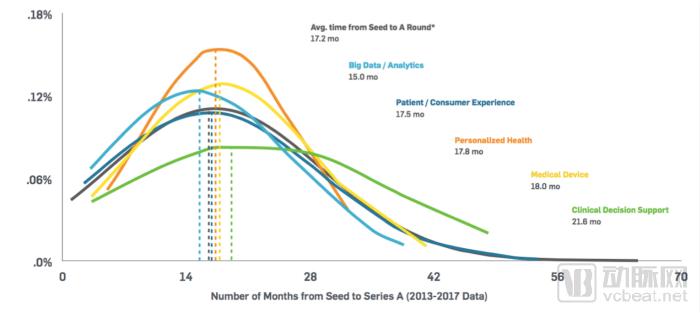

Funding Velocity: Five Booming Sectors

Big data/analytics companies closed their Series A financing rounds at the fastest pace, while clinical decision support (CDS) companies had the longest average interval between their seed and Series A financing rounds.

For clinical decision support companies, the interval between two rounds of financing has increased by more than 6.5 months since 2016. The impact of the FDA's recent regulations on clinical decision support remains to be seen.

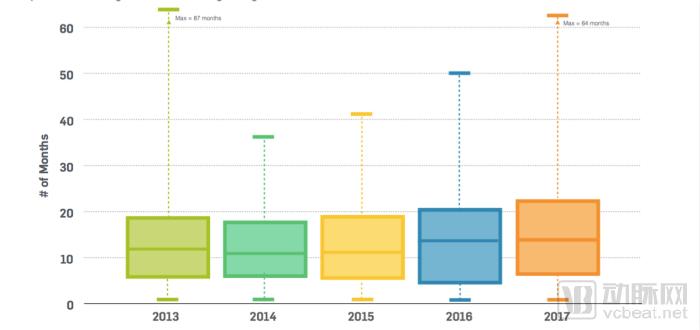

Funding Speed: Annual Comparison of Seed and Series A Rounds

In 2016 and 2017, the median time required to raise a Series A fund was 13 months. Entrepreneurs should carefully consider the time cost associated with capital raising, as well as the changes brought about by integrating financial plans. In 2017, companies took an average of three months to progress from seed-stage financing to Series A financing.

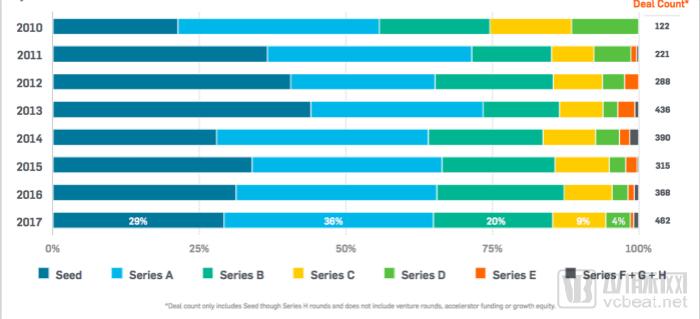

Financing Activities: Stage Comparison

Despite the third consecutive annual increase in Series A financing, early-stage transactions continued to account for 65% of total deal activity, while seed-stage deals represented their lowest share of total transaction volume since 2014.

The share of Series D deals in 2017 has doubled since last year, accounting for 4% of all transactions.

Median Deal Size and Transaction Volume: Comparison by Financing Stage

The median deal sizes for seed and Series A financing rounds saw a more significant decline, falling to levels comparable to the $1.7 million and $6.5 million recorded in 2015, respectively. Although the median deal size has decreased, the number of transactions is higher than ever before, indicating that the market has not yet experienced an “early-stage downturn.”

Median Transaction Size: Comparison by Financing Stage

Driven by the deal sizes of Series B and Series D financing rounds, the median transaction value has increased year over year. Since 2014, the overall median transaction value has grown by 22.7%, rising from $4.4 million to $5.4 million. As later-stage transactions are influenced by the volume of early-stage deals, the overall median transaction value for early-stage rounds has remained on track.

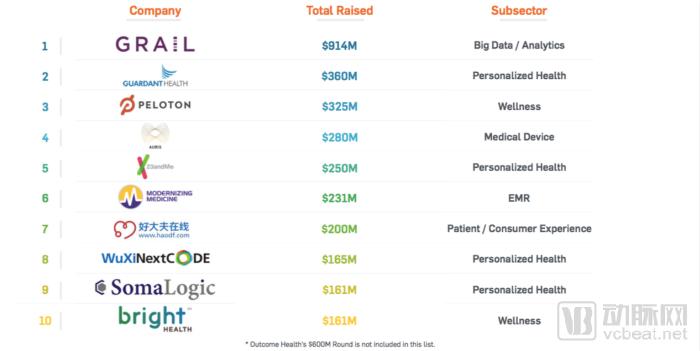

Top Large-Scale Transactions List

Despite more capital flowing into late-stage investment activities, the volume of transactions across all stages increased in 2017, highlighting that investor interest remained strong across every stage. Meanwhile, Peloton, Guardant Health, and Grail topped the list of companies that raised over $300 million in financing in 2017.

Top 10 Deals of 2017

In 2017, more than 26% of the total investment amount was allocated to the following ten companies. Four of the ten largest deals were in the personal health sector.

StartUp Health Portfolio Performance: Key Deal Activity in 2017

Overall, the StartUp Health portfolio raised nearly $200 million in 2017, covering stages from seed to Series C. The five largest investments in the StartUp Health portfolio in 2017 totaled $37.6 million, coming from various investors including Safeguard and Digitalis.

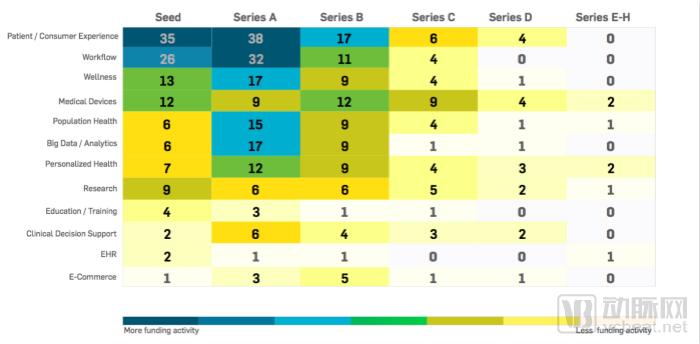

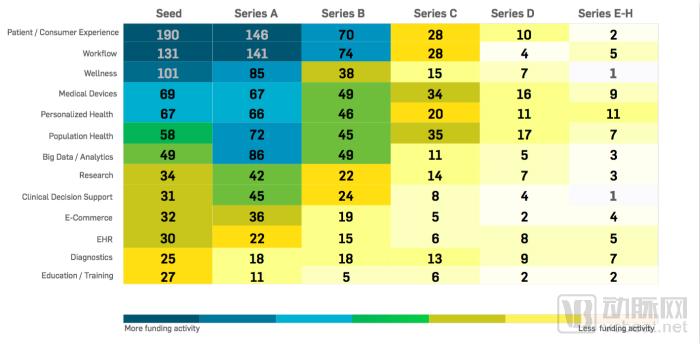

Top 10 Most Active Fields in 2017

Contrary to what the average deal size might suggest, the median deal size hovers between $4 million and $6 million. Among these,"The biggest surprise comes from the workflow and research field.", with median transaction sizes of USD 3 million and USD 10 million, respectively.

2017 Market Maturity Map

Compared with the end of 2016, financing activities in the early stages of the workflow sector saw a significant increase, with the number of Seed and Series A transactions both doubling. The number of Seed financing rounds grew from 12 in 2016 to 25 in 2017, while Series A financing rounds increased from 15 in 2016 to 30 in 2017.

Market Maturity Map: Transaction Activity Since 2010

Since StartUp Health began tracking digital health financing activities in 2010, this is the first time that 12 sub-sectors, excluding education and training, have seen double-digit volumes of Series B financing transactions. More than half of the sub-sectors also experienced double-digit volumes of Series C financing transactions, further indicating that the digital health financing market in 2018 is maturing.

The Most Active U.S. Regions in 2017

With the exception of San Francisco and San Diego, nearly every other major U.S. hub saw its deal volume in the second half of 2017 double compared to the first half. The significant surge in the latter half was driven by Chicago (where transactions nearly tripled), as well as New York and Boston (both registering approximately 30% growth).

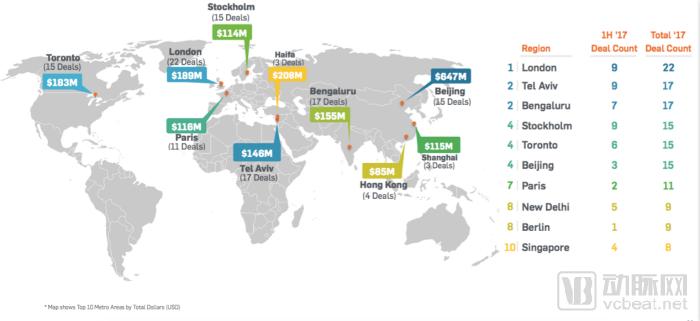

2017 International Hotspots

Beijing leads in total investment amount, but ranks in the middle in terms of transaction volume. The number of transactions increased significantly in the second half of 2017, with Tencent being one of the most active investors among all global companies.

Most Active Investors in 2017

Despite a decline in transaction volume, Khosla Ventures and GE Ventures once again ranked among the year’s three most active investors. Deal activity at familiar venture capital firms such as Sequoia Capital, NEA, Norwest, and Safeguard increased significantly.

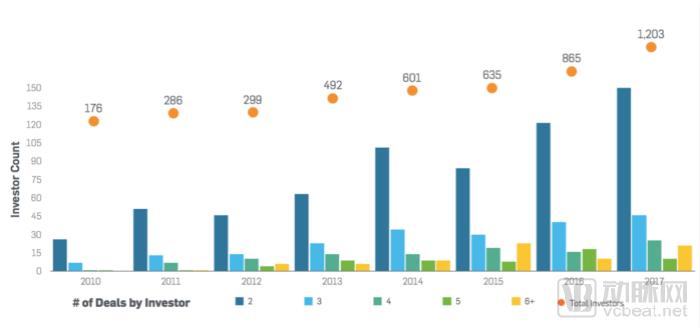

Number of Investors: Year-over-Year Comparison

A total of 21 companies invested in more than six deals throughout the year, doubling the figure from 2016 and reaching a level comparable to that of 2015. The total number of investors increased by 37% in 2017, with new entrants into the digital health sector also achieving remarkable results.

Top Investors in 2017: Sector Comparison

In 2017, top investors participated in an average of five different subsectors. While some investors, such as Khosla Ventures and NEA, made six to seven investments within the same sector, firms like Accel Partners concentrated their interests in three or four sectors.

2018 Trend Forecast

Here are some predictions on development trends for 2018 from medical entrepreneurs, observers, and investors:

Natalie Hodges, Co-founder and Chief Marketing Officer of PreventScripts: “I hope that the pressure from the Medicare Access and CHIP Reauthorization Act (MACRA) will compel healthcare providers to adopt a proactive mindset toward patient-centered care. I expect that the competitive pressure on healthcare providers to expand their API capabilities will foster the development of large-scale patient interventions by digital health companies. 2018 is the year of scalable interventions.”Preventive interventions are the most effective way to reduce costs.。”

Unity Stoakes, Co-founder and Chair of StartUp Health: “Wearables, location tags, apps, and digital diagnostics will begin to leverage the stream of health data provided by connected consumers to create robust health platforms that go beyond popular apps and trackers. Vertical and point solutions have paved the way for more powerful horizontal innovations, which will deliver reliable results through compelling business models. If you plan to compete in 2018, you will need to pay a higher entry fee.”

Lais Suennen, General Manager of GE Ventures: “People are finally recognizing that the majority of funds flowing through healthcare are service-driven. Technology is great, butIn healthcare, technology needs to be integrated by providing clinical and administrative services.。”

Venrock Capital Partners Bob Kocher and Bryan Roberts: “Although we believe that robots will not replace doctors anytime soon, weWe look forward to AI and machine learning moving beyond R&D projects to deliver tangible improvements in cancer diagnosis, pathology, and image recognition."We believe that the training datasets and technological capabilities have reached a stage where they can enable the creation of new products and facilitate ambitious expansion."

Mark Liber, a member of the StartUp Health Moonshot Institute: “U.S. policy is beginning to catch up with digital health innovation. With the FDA’s latest regulations on software as a medical device (clinical decision support) and reimbursement for remote monitoring, we are seeing that regulators have recognized the potential of certain technologies and intend to incentivize healthcare providers to adopt them to improve patient care. The first step was completed in 2017; in 2018, these areas will not only continue to see more innovations, but digital health technologies will also gain broader clinical adoption.”

David Sarabia, Founder of inRecovery: “It is gratifying to see how two major technologies are transforming the healthcare industry. Artificial intelligence and blockchain technology are laying the foundation for the future of healthcare.”I predict that by the end of 2018, we will witness the large-scale launch and application of blockchain technology in healthcare.”

Jo Schneier, CEO and Co-Founder of Cognotion: “We need to bring more humanity into this industry, which will have a profound impact on quality of life and standards of care, while also reducing hospital stays.”

Andrei Zimiles, CEO and Co-Founder of Doctor.com: “There are still some data silos in the healthcare industry, and we hope these silos will disappear in the future. The joint efforts of patients and healthcare providers can bring us a more modern experience.”