Unlocking Europe's $70 Billion Dental Market: Six Strategies for Successful Clinic Expansion

According to KPMG’s 2017 survey data, the European dental market was estimated at over $70 billion, characterized by a low level of chain consolidation.

Private equity firms have recognized the potential in the dental sector and have begun acquiring individual clinics and small chains to form larger branded networks. A report by Straumann estimated that by 2020, the market share of dental chains in Germany, Europe’s largest oral care market, would reach 75%.

The influx of capital has unlocked the industry’s exciting potential.

This is partly due to the steady growth in oral care demand across most European regions, where patients require better dental health and treatment education.

On the other hand, economies of scale can be achieved through shared services, such as shared dental practitioners and integrated laboratories and clinics. As long as local market differences and customs are respected, integrating the upstream and downstream industry chains and developing chain operations can bring significant operational and procurement efficiencies, a possibility that also attracts investors.

Despite the existence of investment opportunities and the increasing liberalization of the healthcare market, the dental market in Western Europe as a whole remainsHighly fragmented and decentralized, with industry consolidation in its early stages。

When establishing a pan-European business model, chain clinics should be wary of becoming an undifferentiated organization. A lack of genuine integration—"connected but not unified"—can cause these clinics to lose their individual character, which is crucial for attracting patients.

A strong local management team,The focus is on long-term profitability rather than quick gains.. Defining such goals and business models helps ensure that customer intimacy and care quality are maintained, while enabling the enterprise to effectively adapt to country-specific regulations and market requirements.

What are the characteristics of the dental clinic market in Europe? What are the prevailing chain models and key players? How is the landscape of mergers and acquisitions evolving? What conditions are essential for the success of dental chains? In response to these questions, VCBeat (WeChat ID: vcbeat) has compiled and analyzed the relevant insights.

Over the past decade, following the introduction of free-market mechanisms in certain sectors of European healthcare, some Western European governments have responded to the dual challenges of rising patient demand and fiscal budget constraints by stimulating higher levels of efficiency and quality.

Although this liberalization has driven an increase in mergers and acquisitions (M&A) across other healthcare sectors, such as hospitals, nursing centers, and private clinics, consolidation within the dental care industry remains relatively low. The following are key trends:

1. Patient:Better patient education, a higher prevalence of comorbidities, and an increasingly important consumer experience;

2. Dentist:A more diverse customer base, an increasing number of female dentists, general practitioners assuming greater workloads, a shortage of specialists in orthodontics and implantology, and a restoration-driven approach;

3. Technology:No longer single-discipline; integrated hardware, software, and services; digitalization transforming workflows; innovation enhancing efficiency and patient throughput.

4. Market:Health awareness penetration drives growth, emerging markets; brand + personalization are crucial in mature markets;

5. Economic Environment:Europe's economy remains sluggish, the US and emerging markets drive growth, and competition for talent is intense.

In most European countries, dental clinics are predominantly small, single-site practices, typically staffed by an average of one to three dentists.A highly fragmented structure indicates that an industry has reached maturity.

According to KPMG, the top 11 markets by size are Germany (€28 billion), France (€12 billion), Spain (€9 billion), Italy (€9 billion), the United Kingdom (€9 billion), Switzerland (€3 billion), the Netherlands (€3 billion), Belgium (€2 billion), Finland (€1 billion), Norway (€1 billion), and Denmark (€1 billion).

In addition to cost challenges related to business operations, small clinics are currently facing significant pressures. For instance, many dentists are approaching retirement age, and there is a shortage of newly qualified professional dentists to replace them. Meanwhile, a considerable number of young dentists (typically women) prefer part-time work and are therefore reluctant to own their own practices. According to Straumann data, the proportion of female dentists in the German market was projected to reach 45%–50% by 2020.

It is widely agreed among many European dentists that establishing an independent private practice is extremely challenging.This creates significant opportunities for private equity and strategic investors, who are beginning to acquire clinics and establish chain models to introduce economies of scale, improve efficiency, and better manage risks related to business continuity and perpetual operation at exit.

Older dentists are highly willing to sell their practices to chain groups, viewing this as an ideal solution that allows them to continue working toward the end of their careers while avoiding the administrative burdens of running an independent practice. The proportion of such older dentists is not insignificant; Straumann data indicate that dentists aged 55–64 account for one-quarter of the German market, and their successors are increasingly female.

Finland has witnessed the most significant consolidation in its dental clinic sector, with chain clinics accounting for 35% of the market share in terms of the number of dentists. In the Netherlands, following a phase dominated by small-scale, solo-practice clinics, there is a growing trend toward clinic affiliations, aimed at overcoming the limitations and vulnerabilities inherent in sole proprietorships.

In countries with larger market sizes,Only the United Kingdom and Spain have a significant proportion of chain stores., but it still accounts for only one-quarter of the total. Germany is the largest dental market in Western Europe, yet 99% of its clinics are small in scale.

The potential and debates surrounding the European dental market have long persisted. One perspective holds that the future lies in numerous small, differentiated clinics, while another argues that chain expansion inevitably compromises quality as scale increases. Due to the unique medical characteristics of dental practices, their revenue models and profitability cycles are fundamentally at odds with the nature of capital.

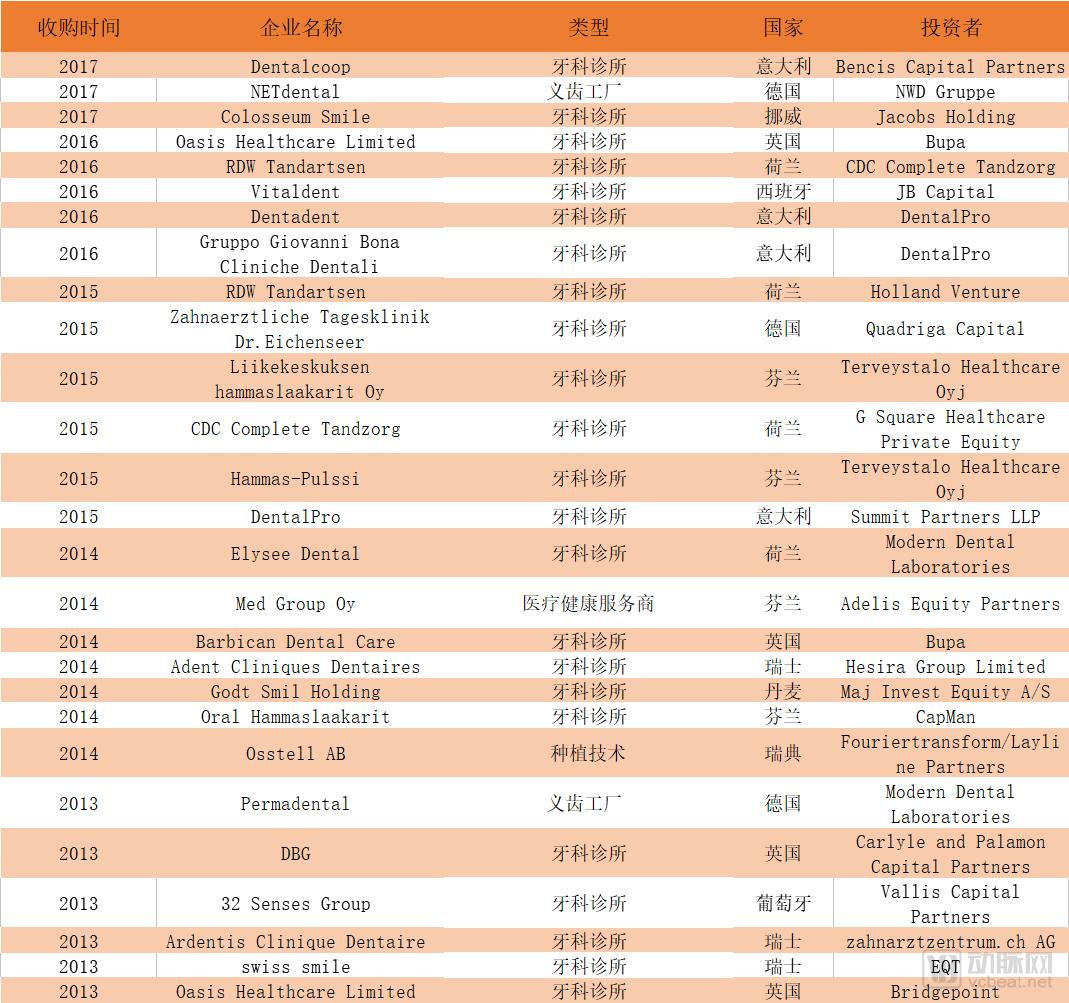

Nevertheless, clinic transactions in several countries have remained robust, with the majority driven by private equity investors. The Carlyle Group and Palamon Capital Partners jointly own mydentist, the UK’s largest dental chain. Established in 2011, mydentist currently operates 654 clinics and holds 598 National Health Service (NHS) dental contracts, treating more than 8 million patients annually.

Mydentist was formerly known as Integrated Dental Holdings (IDH), a leading provider of private dental services in the UK. With the growth of the UK economy, the private dental sector in the country has expanded rapidly.

Mydentist has benefited from favorable systemic trends, such as high stability in patient volume and pricing, the UK government’s long-standing commitment to enhancing dental services, favorable demographic growth trends, and rising consumer spending in the dental sector.

Additionally, Mydentist has become a leading supplier of dental and other medical consumer goods, materials, and services (including the installation and servicing of professional dental equipment), and has established specialized academies and experience programs dedicated to dentist training and enhancing patient experience.

In 2013, Bridgepoint acquired Oasis Healthcare, the UK’s second-largest chain, and sold it again in 2016 to Bupa, a private health insurance company. Bupa, which held shares in the Spanish dental chain Sanitas, initially entered the UK dental market in 2014 by acquiring Barbican Dental Care.

The acquisition of Oasis has propelled Bupa into the leading ranks of dental care providers in the UK, with over 400 clinics and more than 2 million customers. This move may signal that other strategic investors from adjacent healthcare sectors are entering the dental market.

In the Netherlands, since 2011, the leading dental groups Samenwerkende Tandartsen, Tandartsen, and Tandvitaal have been held by private equity firms NPM Capital and Bencis Capital Partners, respectively.

European Dental M&A Activity (Source: KPMG)

Private equity firms are also actively participating in the Northern European dental market, showing interest in Colosseum Dental (since 2010), Oral, and Med Group. Similarly, in Southern Europe, Italy’s largest chain, DentalPro, has been controlled by Summit Partners since 2015, while the Spanish/Italian chain Vitaldent is partially owned by the Spanish private equity firm JB Capital.

Despite these developments, consolidation among most clinics in the region remains in its early stages, offering potentially exciting returns for investors who can successfully capture operational and integration efficiencies.

A notable trend is that industry consolidation has intensified competition for talent, putting some institutions at risk of closure.

Data shows that as of December 31, 2017, Mydentist held a total of 654 clinics, compared with 677 clinics as of December 31, 2016. In the Gwynedd region, nearly 4,500 patients lost their only National Health Service (NHS) dentist, as this was the sole private healthcare provider in the area.

Mydentist Clinical Director Steve Williams stated,The clinic’s inability to recruit new doctors over the past two years was the reason for his decision to close the Wales clinic.

In terms of growth rate, the dental market in Western Europe has remained relatively stable in recent years, with most forecasts projecting it to maintain current levels or grow by a few percentage points annually.Patient education remains key to supporting growth in emerging markets.

Why is projected growth anticipated? This is due to population growth, significant aging (which typically brings a series of more complex dental issues), patients’ increasing desire to retain their natural teeth, and rising demand for preventive care. As patients’ awareness of oral hygiene improves, the focus is shifting from “curative” to “preventive” approaches.

For instance, the cost of dental implant procedures at European clinics typically ranges from $2,000 to $2,800, with premium options such as Nobel Active reaching up to $5,000. These prices vary significantly depending on factors such as the implant brand, stability, and the clinician’s expertise. However, as people place increasing emphasis on oral care,The cost of treating oral diseases has instead decreased., for example, dental chains derive over 40% of their revenue from teeth cleaning, while dental implants account for only 5%.

In recent years, economic downturns in Spain and Italy have, to some extent, heightened the demand for quality among both patients and dentists due to financial pressures. Nevertheless, the overall outlook for Europe appears promising, as dental care is widely regarded as essential in most countries.

For example, in the Netherlands, approximately 75% of citizens visit a dentist at least once a year, with similar trends observed in Nordic countries. In contrast, it is estimated that only 40% of Spaniards see a dentist annually. This figure suggests, to some extent, significant market expansion opportunities through oral health education, particularly given that dental care remains an affordable expense in both Spain and Italy.

Payment methods for dental care vary across Europe. In some countries, the cost of care is partially or fully covered by public health insurance schemes, while in others, patients must pay out-of-pocket for treatment in addition to any public or private insurance coverage. No significant changes in insurance policies are expected in the near future; therefore, market prices for dental services are projected to continue rising at a moderate pace.

The attractiveness of a specific market is also significantly influenced by the stability of its healthcare system. A robust social insurance framework and comprehensive legal regulations constrain improper practices by certain providers. Appropriately sized clinics within a geographic radius help prevent the competitive waste of social and individual resources, while collaboration among clinics with diverse specialties fosters shared benefits and optimal utilization of societal resources.

Private equity investors are more likely to be interested in establishing dental chains in countries with predictable future conditions. Italy is currently undergoing various reforms and innovations, but their impact—particularly regarding payment procedures and patient pricing—is difficult to assess due to the incomplete implementation of relevant laws. In recent years, the impact of Finland’s healthcare reforms on dentists has remained unclear.

Apart from these countries, there appear to be no major planned regulatory reforms likely to impact the dental market. Although price increases typically lead to a temporary decline in demand, this trend usually reverses quickly and is therefore not considered a significant deterrent to investment decisions.

The trend toward subscription-based pricing in private dental care, as already seen in Finland and the United Kingdom, may shift the balance of power from insurers/payers to dental clinics, thereby creating a more favorable environment for investors who can rely on more predictable revenue streams.

For payers, subscription or membership models represent a favorable approach, facilitating timely and preventive dental care and improving oral health outcomes.

Large chain stores can offer numerous benefits, such as centralizing back-office functions—including finance, IT, procurement, marketing, and comprehensive management—within shared service centers to reduce administrative costs and secure procurement discounts on disposable devices, instruments, and equipment, which account for a significant proportion of operating expenses.

Shared service centers are common in most current chain practices, allowing existing dentists to focus on providing patient care.Once a chain achieves scale, it also gains financial leverage., negotiate more favorable terms for property leasehold rights.

A broad local talent pool of dentists, specialists (such as hygienists), and support staff across multiple chains enables the company to allocate work across facilities during periods of high demand. This should enhance overall service capacity and minimize the likelihood of turning away patients.

As demand grows and larger dental clinics are established in high-traffic areas such as shopping malls, these clinics may extend their operating hours to evenings and even weekends, further increasing their numbers. Large chain brands with well-known reputations are also more likely to attract dentists and other staff, thereby overcoming technical shortages.

Currently, most smaller-scale clinics rely on third-party technical laboratories to produce crowns and implants. Chain practices can achieve vertical integration by establishing centralized dental laboratories that serve all their clinics. In developed countries, efficiency must be improved, as the current patient load per technician or dentist has already exceeded optimal levels.

Mydentist is the UK’s largest dental chain and the country’s leading comprehensive dental services provider, with its own in-house laboratory. By producing crowns, implants, and bridges internally at lower costs, the chain can boost profitability and even generate additional revenue by selling these products to other clinics outside its own network.

By establishing laboratories in low-wage regions such as mainland China, Taiwan, China, or Eastern Europe, dental chains can further increase their profit margins while ensuring that technical quality is not compromised.

Dental chains have also effectively leveraged advancements in technologies such as computer-aided design/computer-aided manufacturing (CAD/CAM) and 3D printing, which are less labor-intensive, shorten the supply chain for crowns and bridges, and reduce costs.Digitalization Will Further Transform the Value Chain and Workflows of Dentists and Laboratories. Simpler and more standardized treatment regimens are crucial for reducing consultation time, which means that efficiency will be improved.

Smaller clinics may hesitate to make substantial capital investments in such equipment, which could place them at a disadvantage in attracting patients requiring high-tech dental procedures. Investment in new technologies will raise the barriers to establishing dental practices.

In the long run, technology investment may be a prerequisite for attracting and retaining patients, thus becoming another driver of mergers and acquisitions.

From the perspective of customer satisfaction, vertical integration and technological investment are also highly significant. A chain organization often operates numerous specialized clinics capable of providing various services, such as dental implants, orthodontics, and prosthodontics. This means that patients do not need to seek specific treatments elsewhere.

The emergence of dental chains has proven beneficial to the industry, creating advantages in medical quality, transparency, efficiency, and capital resources. This will deliver more professional, higher-quality services and care to patients—a view widely endorsed by many members of European dental associations.

Centralization can enhance efficiency, but any integration strategy should be aligned with local conditions and operational characteristics. Regulations and health insurance policies vary significantly across countries, making a “one-size-fits-all” pricing model impractical.

Dentistry is inherently a local business that attracts patients from the surrounding area, with a defined service radius. Therefore, it is advisable to build region-specific brands within the company’s overall portfolio. This approach not only reassures customers but also helps mitigate reputational risks for other brands within the group in the event of adverse publicity. For example, Hesira operates under two brands: Dental Clinics Nederland in the Netherlands and Adent Cliniques Dentaires in Switzerland.

When hiring dentists from other countries, chain practice management should ensure that, wherever possible, they are proficient in the local language and familiar with local work practices. It is advisable to minimize the use of short-term staff to maintain the continuity of care that patients value.

Dentists are the core resource of dental clinics. Unlike chain stores such as McDonald's, it is highly difficult to rapidly train and replicate dentists. Although the trend toward digitalization in dentistry is irreversible, aiding dentists' professional growth and improving efficiency through training, education, and surgical assistance, in the short term,Dentist turnover remains a significant challenge for clinic operations.。

A clinic operator pointed out, “You need to find employees who are willing to work for you for 10–20 years. Patients prefer to be treated by the same dentist, but this is a service that chain clinics struggle to provide.”

A dentist also highlighted this issue: “The primary challenge facing chain clinics is staff turnover. If patients encounter a new dentist at every visit, let alone one who speaks the local language, such a chain has no future.”

Finally, when establishing large-scale enterprises, dental chains must recognize the intimate nature of the relationships between patients and dentists—a sentiment strongly held by many experts. Clinics need to prioritize service, technology, and humanized management to retain patients and cultivate a patient-centric management mindset.

For most people, the experience of visiting a dentist is undifferentiated; therefore, when acquiring other chains or individual practices,It is necessary to select stores that prioritize personalized, high-quality care and gradually and carefully integrate each clinic., and integrate into chain brands, emphasizing long-term growth rather than short-term profitability; brand awareness cannot be achieved overnight.

With this mindset, investors should be able to fully capitalize on the window of opportunity presented by market consolidation. By enhancing treatment consistency and quality, reducing per-patient costs, and improving preventive oral care, the increased efficiency of chain practices can also benefit the broader healthcare ecosystem.

In summary, establishing a successful dental chain can be distilled into six key strategies:

1. Ensure that each clinic within a brand has its own local differentiated features;

2. Retain the original management team to address regulatory issues, such as payment policies;

3. Establish a flexible dental team capable of operating across multiple locations as needed, while maintaining maximum staff consistency and continuity to ensure continuity of patient care;

4. Invest in employee retention by providing training and promotion opportunities;

5. Achieve vertical integration by acquiring or establishing dental laboratories, and consider leveraging these capabilities where appropriate;

6. Consider investing in digital and 3D printing technologies, such as CAD/CAM, to improve supply chain efficiency.

Note: All monetary units in the text are in US dollars.

References:

https://www.beckersdental.com/

http://www.dentalproductsreport.com/

http://www.dentistry.co.uk/2017/11/07/mydentists-day-out/

How will dentistry look in 2020? Straumann

The dental chain opportunity,KPMG International Global Strategy Group

https://www.carlyle.com/media-room/news-release-archive/carlyle-group-partnership-palamon-capital-partners-acquire-dental