China's Private Chain Orthopedic Industry Report: Low Scalability, Regional Leaders Emerging

The growth of private medical institutions is one of the significant trends under the backdrop of China’s healthcare system reform. Consumer-oriented medical services, such as dentistry, ophthalmology, and medical aesthetics, have achieved scaled replication and expansion driven by social capital. However, specialized medical fields, including oncology and neurology, remain predominantly served by large public hospitals.

Orthopedics is a specialty situated between consumer healthcare and professional medical care, characterized byHigh proportion of service-based projects, extensive use of high-value consumables, and high gross profit marginscharacteristics. VCBeat Research Institute estimates that, against the backdrop of intensifying competition in consumer healthcare, orthopedics may become the next investment hotspot in China’s healthcare services industry.

Therefore, VCBeat·VBInsight completed this report by studying policies in relevant fields, conducting on-site visits to multiple hospitals, and interviewing operators of chain orthopedic medical institutions, orthopedic surgeons, and startups in related areas.China's First In-Depth Research Report on Chain Orthopedic Hospitals—“Report on China’s Private Chain Orthopedic Industry”, which features an in-depth analysis of the international benchmark orthopedic hospital, the Royal National Orthopaedic Hospital (UK), and includes a comprehensive map of the chain orthopedic industry, helping industry professionals gain a clear and efficient understanding of the sector.

By reading this report, the following questions can be addressed:

What Is the Current State of China’s Chain Orthopedic Industry?

What are the leading brands of chain orthopedic hospitals and chain orthopedic clinics in China?

What does the industrial chain landscape of orthopedic medical institutions look like?

What are the primary factors to consider when selecting locations for chain orthopedic clinics?

What is the recommended site selection based on the two guiding factors of aging degree and consumption power level?

What Are the Two Most Practical and Effective Ways for Orthopedic Chain Medical Institutions to Drive Patient Traffic?

How to Implement the Most Cost-Effective Marketing Strategies for Chain Medical Institutions?

Where Do the Positioning Differences Between Mid-to-High-End Chain Orthopedic Hospitals and Affordable Chain Orthopedic Hospitals Lie?

What Are the Core Competencies of Orthopedic Chain Medical Institutions?

Table of Contents:

I. Private Orthopedics: A Blue Ocean Market in China's Healthcare Service System

II. Core Competencies: Prioritizing Internal Operations and External Marketing Is the Key to Success for Chain Orthopedic Hospitals

III. Representative Enterprises: Bang'er Orthopedic Medical Group and the Royal National Orthopaedic Hospital

IV. Investment Recommendations: The Industry Landscape Is Far from Settled; Regional Leaders Can Serve as Reference Benchmarks

V. Risk Warning: Aligning Investment Scale with Actual Capabilities Is a Prerequisite for Sustainable Development

This article excerpts Part I and Part II of the report. To read the full text, please scan the QR code below to become a VCBeat member, gain access to the complete report, and learn more about the current state and development trends of China’s private chain orthopedic industry.

Scan the QR code to become a VCBeat member

I. Private Orthopedics: A Blue Ocean Market in China’s Healthcare Service System

(I) Three Major Factors Driving the Continuous Rise in the Incidence of Orthopedic Diseases

Orthopedics, also known as orthopedic surgery, is a medical specialty primarily focused on the prevention, treatment, and rehabilitation of conditions related to the musculoskeletal system. Common orthopedic conditions include frozen shoulder, cervical spondylosis, lumbar disc herniation, arthritis, and fractures. Major subspecialties within orthopedics encompass trauma orthopedics, joint surgery, spine surgery, sports medicine, and bone oncology.

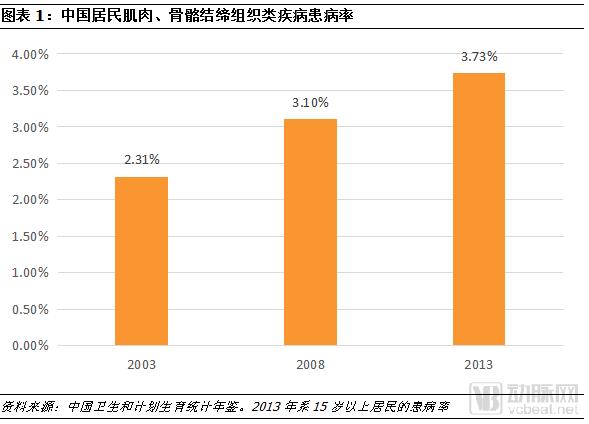

According to the National Health Services Survey, conducted every five years and recorded in the China Health and Family Planning Statistical Yearbook, the prevalence of musculoskeletal and connective tissue diseases among residents aged 15 and above in China reached 3.73% in 2013, up from 2.31% in 2003, showing a steady increase over this period. Conservatively estimated, there are at least 2 million new cases of orthopedic diseases annually in China. Furthermore, statistics from the Chinese Journal of Surgery indicate that there are as many as 20 million orthopedic trauma cases each year in China, with 79.35% requiring surgical treatment.

Beyond accidental injuries such as trauma, the rising incidence of orthopedic disorders is also influenced by broader societal factors. We primarily analyze this trend from four perspectives: demographic structure, work-related stress, lifestyle habits, and sports-related injuries.

First, population aging is intensifying. According to United Nations criteria, a country or region is considered an aging society when the proportion of individuals aged 60 and above exceeds 10% of the total population, or when those aged 65 and above account for more than 7%. Currently, the share of China’s population aged 60 and over has surpassed 15.5%, while those aged 65 and over exceed 10.1%, with aging expected to deepen further before 2040. Human skeletal degeneration typically begins at age 35, progressing with advancing age and elevating the risk of orthopedic disorders. The expanding proportion of elderly individuals in the population will directly drive up the overall incidence of orthopedic diseases in China.

Secondly, with China’s rapid economic growth, the fast-paced social environment has led to ever-increasing work-related stress. According to a survey conducted by the professional services firm Regus among working professionals in 80 countries worldwide, office workers in China rank first in terms of work stress. Due to prolonged periods of high-intensity work, orthopedic conditions such as cervical spondylosis, lumbar disc herniation, and tendonitis account for a significant proportion of health issues among working professionals. Data from the Orthopedics Outpatient Clinic of Zhongda Hospital Affiliated to Southeast University show that approximately one-third of patients treated at the clinic in 2016 were diagnosed with cervical spondylosis, with desk-bound office workers constituting the majority, including even middle school and university students.

Once again, modern society has altered residents’ lifestyle habits. The advent of mobile internet and the widespread adoption of smartphones have turned many people into “phubbers,” while vibrant nightlife has made barbecue and cola standard fixtures on late-night snack tables. No matter how cautiously we try to avoid them, modern society can easily lead us to develop unhealthy habits, and many orthopedic conditions arise precisely from these seemingly trivial behaviors.

Finally, sports injuries are also a significant cause of orthopedic conditions, primarily affecting professional athletes as well as fitness and outdoor sports enthusiasts. With rising disposable income and changing lifestyle habits, residents are increasingly prioritizing physical exercise to maintain health. Particularly in economically developed regions such as Beijing, Shanghai, Guangzhou, Shenzhen, and coastal areas, patients with sports injuries account for nearly one-third of all orthopedic cases, with 30%–50% of them requiring subsequent surgical treatment.

(II) The market dominance of private orthopedic hospitals has become even more pronounced following the “New Healthcare Reform”

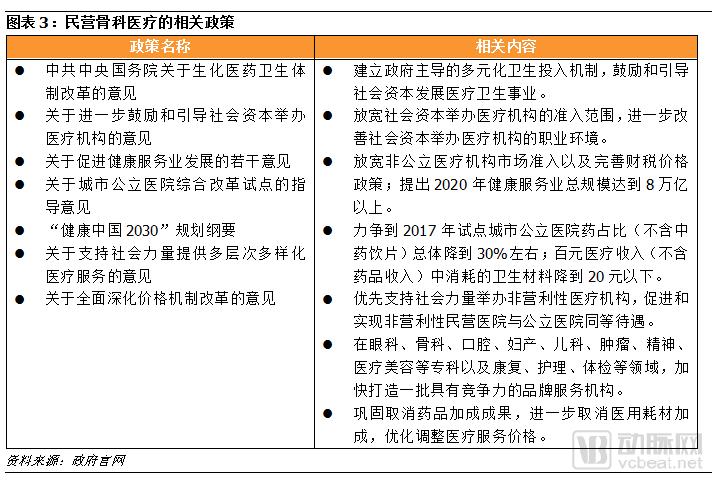

On March 17, 2009, the Central Committee of the Communist Party of China and the State Council released the Opinions on Deepening the Reform of the Medical and Health Care System to the public. The Opinions set forth the short-term goal of “effectively reducing residents’ financial burden for medical care and substantially alleviating the difficulties and high costs associated with accessing medical services,” as well as the long-term goal of “establishing and improving a basic medical and health care system that covers both urban and rural residents, providing the public with safe, effective, convenient, and affordable medical and health care services.” Encouraging the development of private healthcare has thus become an integral component of the “New Healthcare Reform.”

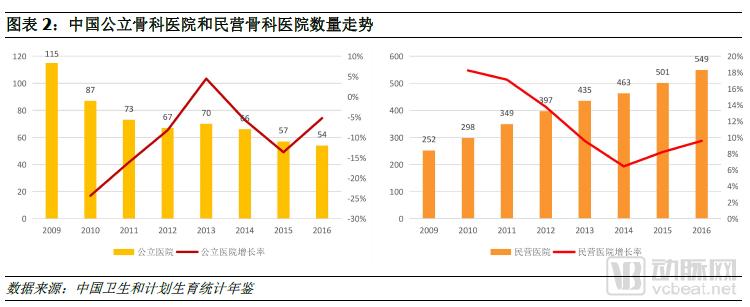

In fact, a high degree of market-oriented operation had already been achieved before the official release of supportive policies, and this trend became even more pronounced after 2009. By the end of 2016, the total number of private orthopedic hospitals reached 549, while the number of public orthopedic hospitals stood at only 54. Private orthopedic hospitals accounted for 90% of the total number of orthopedic hospitals in China.

Data compiled from third-party enterprise information platforms indicate that there are currently 851 and 1,014 orthopedic clinics in normal operation in China, as well as 683 and 1,312 rehabilitation clinics. Given that a significant proportion of rehabilitation clinics specialize in orthopedic rehabilitation, and that some orthopedic clinics may not include terms such as “orthopedics” or “rehabilitation” in their business registration names—leading to undercounting—we estimate that the total number of orthopedic clinics in China is at least 2,000. The majority of these are independent practices, with a low level of chain affiliation.

While providing policy support to privately-run medical institutions, the government has also issued important documents to control the costs of pharmaceuticals and medical consumables. The “Guiding Opinions on Pilot Comprehensive Reform of Urban Public Hospitals,” issued by the State Council in 2015, explicitly required that the proportion of pharmaceuticals and medical consumables in total medical expenses be reduced to below 30% and 20%, respectively. In contrast, in previous orthopedic care, the combined share of pharmaceuticals and consumables accounted for 60%–70% of the total medical expenditure. In 2017, all public hospitals in China completely abolished drug markups, and the subsequent elimination of markups on medical consumables in public hospitals was placed on the agenda. On November 10, 2017, the National Development and Reform Commission released the “Opinions on Comprehensively Deepening the Reform of the Price Mechanism,” which clearly stated: consolidate the achievements of abolishing drug markups and further eliminate markups on medical consumables.

Orthopedics is a specialty with a high concentration of high-value medical consumables. Driven by policy changes, the income of orthopedic surgeons in public hospitals is expected to be significantly impacted. Consequently, compensation packages will become a major driver for private orthopedic institutions to attract orthopedic surgeons from public hospitals.

(3) The level of chain operations among domestic orthopedic hospitals and orthopedic clinics remains low.

From the perspectives of treatment standardization and therapeutic risk, orthopedics lies between consumer-oriented specialties such as dentistry and ophthalmology, and serious-condition specialties such as oncology and neurology. Given that nationwide giants have already emerged in dentistry and ophthalmology, orthopedics is well-suited for chain-based operations. Furthermore, orthopedics involves numerous out-of-pocket services, such as those for tendinopathy and osteoporosis, and high-value surgical consumables are also paid for by patients, resulting in a high average revenue per user. Currently, the level of chain consolidation among orthopedic medical institutions in China is relatively low; the development of chain models will help establish brand advantages and cost efficiencies.

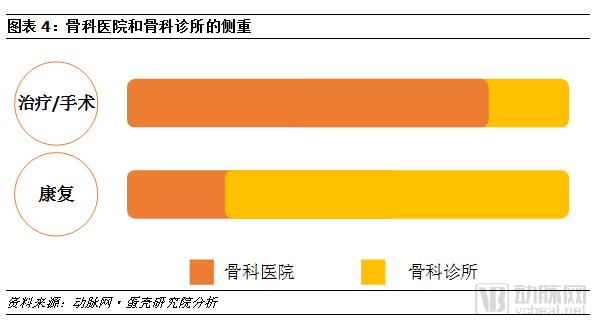

Orthopedic hospitals focus on surgical procedures, whereas orthopedic clinics prioritize rehabilitative therapy for patients. In terms of professional complexity, medical activities in orthopedic hospitals are more intricate and carry relatively higher risks compared to those in orthopedic clinics. Consequently, orthopedic clinic chains can adopt a franchise model with looser management; however, this approach presents significant management bottlenecks, and its ability to establish a strong brand image remains questionable. In contrast, chain orthopedic hospitals exercise greater caution in their strategic layout, predominantly adopting an asset-heavy, direct-operation model that facilitates management but makes achieving scale relatively difficult.

Currently, chain orthopedic hospitals and clinics in China have not attracted significant attention from capital markets. Among them, only Ai Bafang was listed on the Qianhai Equity Exchange Center in October 2016, while Bang'er Medical secured RMB 90 million in Series A financing in October 2014 and RMB 200 million in Series B financing in January 2017. Investors included Jinpu Industrial Investment Fund, Zhejiang Private Enterprise United Investment Co., Ltd., and Fidelity Investments. Given that the chain orthopedic sector (particularly chain orthopedic hospitals) operates under an asset-heavy model, the national presence of various chain brands remains fragmented, preventing them from leveraging the advantages of economies of scale.

II. Core Competencies: Emphasizing Internal Operations and External Marketing Is the Key to Success for Chain Orthopedic Hospitals

(1) Medical institutions are the central link in delivering medical value to patients.

In the orthopedics sector, the value chain can be segmented into upstream segments dominated by physicians, medical devices, and pharmaceuticals. What distinguishes orthopedics from other specialties is its relatively low proportion of pharmaceutical expenditures, with a primary focus on medical devices and high-value consumables.

Furthermore, for orthopedic hospitals, site selection prior to establishment and obtaining approval from regulatory authorities are indispensable; therefore, we classify real estate developers and government agencies as upstream players in the industry. The midstream segment consists of hospitals and clinics, typically categorized into public and private institutions. Finally, the downstream segment is patient-centric, encompassing both pre-treatment patient acquisition through various media channels and post-treatment rehabilitation support facilitated by internet-based tools.

(2) The degree of population aging and the level of consumer spending power are important reference factors for the site selection of medical institutions

The degree of regional aging (particularly the absolute number of elderly individuals) and the level of consumer purchasing power play a pivotal role in site selection for chain orthopedic hospitals. The former determines market capacity, while the latter dictates whether the positioning of medical institutions aligns with the overall environment of the target region. For instance, Shandong Province ranks among the top ten nationwide in both its elderly population and per capita GDP, suggesting that the province generally provides a fertile ground for developing mid-to-high-end private chain orthopedic services.

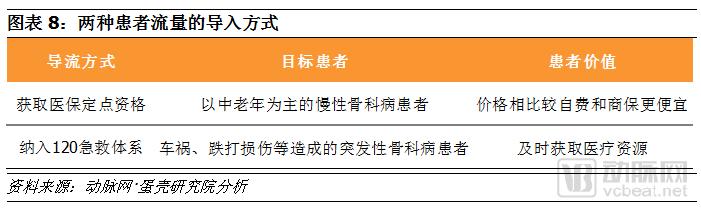

(3) Supporting medical insurance reimbursement and inclusion in the 120 emergency medical services system are the two primary methods for driving patient traffic.

Orthopedic conditions can be categorized by etiology into acute orthopedic injuries (such as those resulting from car accidents and traumatic injuries) and chronic orthopedic disorders (such as lumbar disc herniation). For acute cases, the emergency medical services (EMS) system typically adheres to the "nearest facility" principle while respecting the patient’s preference when transporting them to a hospital. Through collaboration with regional EMS systems, hospitals can secure a portion of their patient intake. In contrast, chronic orthopedic conditions predominantly affect middle-aged and elderly populations, for whom insurance coverage is a critical factor in selecting hospitals or clinics. Unless targeting self-pay patients or high-end clients with commercial insurance, most chain orthopedic providers rely on participation in national health insurance schemes to ensure steady patient flow.

Currently, private orthopedic clinics see roughly equal proportions of patients with acute and chronic orthopedic conditions, both of which are of equal importance.

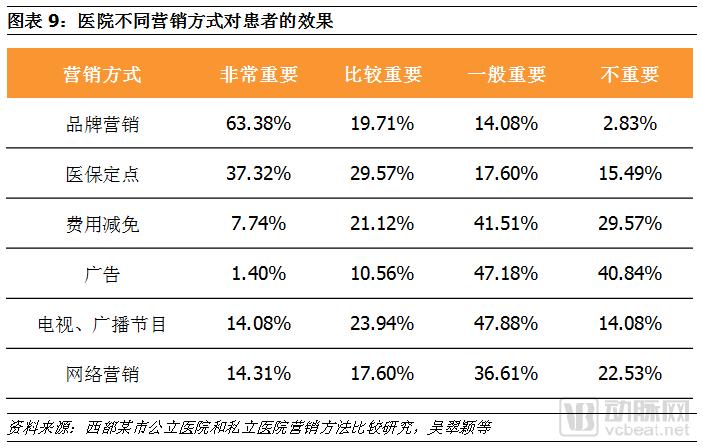

(4) A strong reputation is the most cost-effective marketing strategy.

There is no fundamental difference between orthopedic chain medical institutions and general practice or other specialized hospitals in terms of external marketing and promotion, which includes online advertising, outdoor advertising, free services, free clinic activities, and promotional publications. Word-of-mouth stands out as the most cost-effective marketing method, as it incurs virtually no additional costs; moreover, recommendations based on personal acquaintances among patients yield significantly higher effectiveness than other approaches.

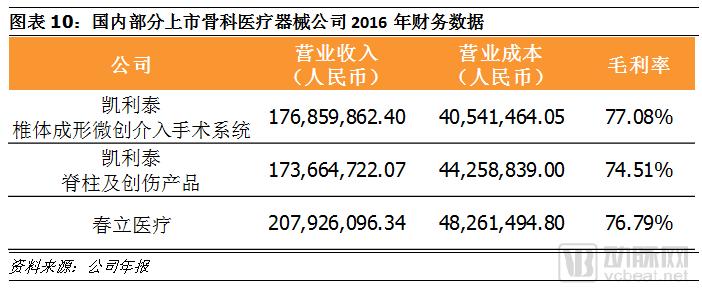

(5) High-value consumables are a key factor driving up profit margins in orthopedics

Orthopedics is one of the specialties with the highest profit margins, partly due to the stringent qualifications required for orthopedic surgeons, and partly because orthopedic consumables, known for their high cost, belong to a technology-intensive industry with strong bargaining power.

In June 2017, Wuhan No. 4 Hospital, renowned for its orthopedics department, disclosed that the average hospitalization cost per patient in its orthopedics department reached RMB 20,000 that month, with the average cost in the joint and trauma surgery subdivision amounting to RMB 32,000—significantly higher than that of other departments.

We compiled statistics on the orthopedic business segments of several publicly listed medical device companies based on their audited annual financial reports. These companies generally report gross profit margins between 70% and 80%, with unit prices often reaching tens of thousands of yuan. Private hospitals have room for negotiation with suppliers regarding the pricing of consumables.

Content of the remaining three sections:

III. Representative Enterprises: Bang'er Orthopedic Medical Group and the Royal National Orthopaedic Hospital

IV. Investment Recommendations: The Industry Landscape Is Far from Settled; Regional Leaders Can Serve as Reference Benchmarks

V. Risk Warning: Aligning investment scale with actual capabilities is a fundamental prerequisite for sustainable development

Please refer to the full report.

Special Acknowledgments:

The authors extend their sincere gratitude to Sun Xiaoyi, founder of Yishu, a platform for orthopedic medical science popularization, and Wei Yongjun, Associate Chief Physician at Changshou Shengwei Orthopedic Hospital, for their substantial support during the preparation of this report.

Scan the QR code below to becomeVCBeat Official Member, you can obtainFull Version of the "China Private Chain Orthopedics Industry Report". UnderstoodAn Overview of the Current Industrial Landscape and Development Trends in Depression Care: A “Sober Reflection” on Future Innovative Developments in the Chain Orthopedics Sector.Furthermore, in the coming year, you will have unrestricted access to the completeIndustry Trend Report, stay abreast of the latest global investment and financing information, with comprehensive access toHealthcare Enterprise Database, and alsoMassive Resource Matchmaking。

Scan the QR code to become a VCBeat member