2017 Medical and Healthcare IPO Report: 50 Listings, RMB 25.8 Billion Raised – Annual Performance of Investment Institutions

In the realms of investment and entrepreneurship, investors and founders are inseparable companions on a shared journey. Once embarked, the scenery along the way becomes a temptation, while the sacred destination in one’s heart turns into a distant goal requiring steadfast perseverance. Investment and exit form a closed loop; the primary objective of capital investment is to realize returns through an exit, which is currently achieved mainly through corporate initial public offerings (IPOs).

In 2016, 28 biopharmaceutical companies went public via initial public offerings (IPOs), averaging two healthcare listings per month. High-profile companies such as China Resources Pharmaceutical, Buchang Pharmaceuticals, and Yiming Pharmaceutical attracted significant attention from all sectors. Following the somewhat frenzied activity of 2016, the capital market’s enthusiasm for pharmaceutical and healthcare enterprises continued, reaching a new peak. Starting in late 2016, the number of new stock issuances per week on the Shanghai and Shenzhen stock exchanges increased significantly, marking the normalization of IPOs. However, beginning in late May 2017, the pace of IPO issuance slowed considerably due to market downturns. In October, the establishment of a new Issuance Examination Committee ushered in a new era for China’s IPO review process, shifting various approval philosophies and imposing stricter requirements on corporate business quality.

In 2017, a total of 50 companies in the healthcare sector completed initial public offerings (IPOs), among which 29 had venture capital/private equity (VC/PE) backing, involving more than 100 VC/PE firms.

VCBeat · VCBeat Institute has compiled and analyzed the full-year 2017 IPO data of healthcare companies based on publicly available information. By tracing every inflow and outflow of capital, we aim to map out the journey of those who have successfully reached their destination, offering silent encouragement to waiting investors and hearty cheers to striving entrepreneurs.

Data sources: Corporate prospectuses, CSRC website, Choice

Sample Subjects: Healthcare enterprises registered in China

IPO dates are based on the listing date, while issuance review dates are based on the announcement dates published by the China Securities Regulatory Commission (CSRC).

Trading Venues: NASDAQ, Shanghai Stock Exchange, Shenzhen Stock Exchange, Hong Kong Stock Exchange, Korea Exchange

Statistical Period: 2017.01~2017.12

1.1Mass Entrepreneurship and Innovation Ignite the Fire of Equity Investment

China’s equity investment sector has developed for over two decades. With the advent of the “Mass Entrepreneurship and Innovation” boom, the equity investment market has advanced in tandem with the entrepreneurial wave, embarking on a path of rapid growth.

Data from the Asset Management Association of China (AMAC) shows that by the end of December 2017, the scale of private equity funds in China reached RMB 11.1 trillion, a year-on-year increase of approximately 41%. The number of fund managers stood at 22,400, the number of registered funds exceeded 66,400, and the total number of employees was 238,300. Notably, the scale of private equity and venture capital funds grew by RMB 2.4 trillion in 2017, becoming the primary driver of growth in the private equity market. The assets under management in this segment reached RMB 7.09 trillion, accounting for approximately 64% of the total private equity fund scale. Meanwhile, the scale of securities-focused private equity funds shrank by RMB 480.3 billion, standing at RMB 2.29 trillion.

The explosive growth of equity venture capital and private equity is primarily driven by national policies encouraging innovation, entrepreneurship, and the development of the new economy, which have created a favorable environment for equity investments. Meanwhile, the normalization of initial public offerings (IPOs) has opened up channels for direct corporate financing, providing investors with smooth exit opportunities and returns. In the healthcare sector, which we closely monitor, a similarly dynamic trend is evident, characterized by robust investment activity and a surge in IPOs.

In 2017, capital enthusiasm for investment in the healthcare sector remained high, with a total of 455 investment deals recorded in China, involving an amount exceeding RMB 47.3 billion. Compared with 2016, the investment stages in the healthcare sector in 2017 shifted noticeably toward later rounds. Taking early-stage investments, namely seed and angel rounds, as an example, there were 218 financing events in 2016, accounting for 31.6% of the total number of financing deals that year. In 2017, seed and angel rounds totaled 194 financing events, representing 18.9% of all financing rounds. Using internet healthcare as an example, since the rapid development of new business models began in 2014, the industry has become increasingly mature, and competitive moats have been established. Capital is now more focused on companies with clear profitability models at later stages, leaving limited opportunities for new entrants.

Investment and exit form a closed loop, with investment booms often marking the beginning of return surges. In the following section, we will primarily analyze IPO data from the healthcare industry in 2017 to present an overview of leading enterprises and top investment institutions in the healthcare sector.

1.2 Surge in IPO Numbers, Decline in Average Funds Raised

VCBeat · Eggshell Research Institute has compiled a list of healthcare companies that went public in 2017, based on publicly available data. By analyzing capital inflows and outflows, we aim to map the journey of those who have successfully reached their IPO destination, offering silent encouragement to waiting investors and hearty cheers to entrepreneurs still striving for success.

2017List of Healthcare IPO Companies

Data Source: CSRC Website, Choice

In 2017, a total of 50 companies in the healthcare sector completed initial public offerings (IPOs), among which 29 had venture capital/private equity (VC/PE) backing, involving more than 114 VC/PE firms. The penetration rate of investment institutions reached 58%, on par with the 57% VC/PE penetration rate for Chinese enterprises this year. A total of RMB 25.789 billion was raised, with an average fundraising amount of RMB 641 million per transaction.

In 2017, the number of healthcare companies going public reached 50, a year-on-year increase of 78.57% compared to 28 in 2016. The total amount raised amounted to RMB 25.7 billion, remaining flat compared to the previous year. However, the average fundraising amount declined significantly: in 2017, the average fundraising per company was RMB 641 million, representing a 28.15% decrease from the 2016 average of RMB 920 million. This decline was primarily attributed to several large-scale financing events in 2016, notably China Resources Healthcare’s IPO, which raised RMB 11.5 billion. In contrast, most companies that went public in 2017 were small and medium-sized enterprises, leading to a lower average fundraising amount compared to 2016.

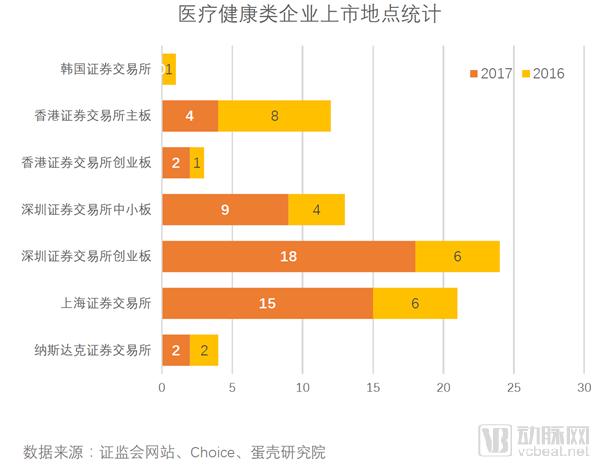

1.3 Increasing Proportion of Healthcare Companies Listed Domestically in China

2017 was a peak year for initial public offerings (IPOs) among healthcare companies, with the number of IPOs nearly doubling compared to 2016. However, the number of healthcare enterprises listing overseas decreased rather than increased. As domestic IPO reviews returned to normal, the advantages of higher valuations in China and closer proximity to the local market gradually became apparent.

On December 15, 2017, the Hong Kong Stock Exchange (HKEX) issued an announcement accepting listing applications from biotechnology companies that are not yet profitable or revenue-generating. This move is poised to attract a large number of high-potential companies in the R&D stage to list in Hong Kong, significantly stimulating the biotechnology sector and creating new opportunities for investment institutions and enterprises.

1.4 Shifting Focus: Healthcare Service Providers Take Center Stage

In recent years, medical innovation has been primarily driven by the dual forces of policy and technology. Policy-driven advancements stem from healthcare reform entering a critical phase, encouraging capital investment in private healthcare and reforms within public healthcare institutions. Technology-driven progress arises from the dividends of mobile internet development and the rapid advancement of biotechnologies, represented by biologics and genomic sequencing.

During this period, healthcare investment flourished: internet healthcare shone brightly, while sequencing, diagnostics, and biologics began to emerge and grow rapidly. A large number of new investment firms flooded into the healthcare sector, bringing a new dawn to this previously low-profile industry.

From 2007 to 2009, the hotspot in the capital market was outsourcing, exemplified by WuXi AppTec securing financing and going public. From 2009 to 2016, with the launch of the ChiNext board, capital flocked to traditional pharmaceutical manufacturers and medical device companies. Since the healthcare reform began in 2012, chain specialized medical services, private hospitals, and mobile health have emerged as market winners, as seen with Phoenix Medical. In 2014, precision medicine created a new hotspot, with companies like BGI Genomics and Berry Oncology completing capital integration. In 2015 and 2016, new drug R&D became the focus, exemplified by Innovent Biologics.

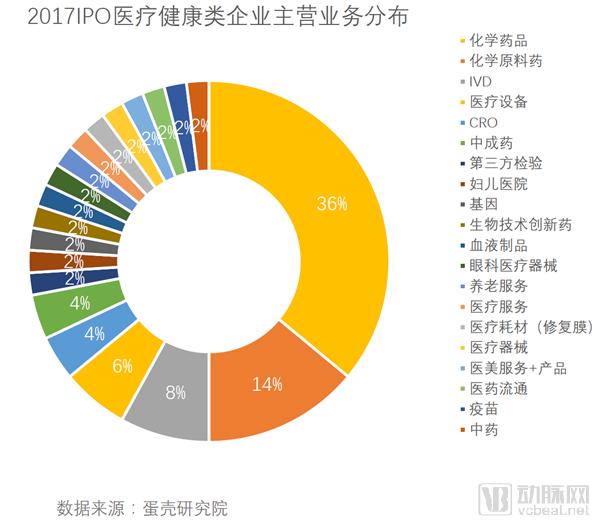

Investment hotspots from 2013 to 2015 became the main force behind IPOs in 2017, and healthcare service providers, which had rarely appeared in previous years, also made their way onto the 2017 IPO list of medical enterprises.

Medical Services: Honghe Renai Medical

On March 16, 2017, Honghe Renai Medical Group Co., Ltd., the core platform controlled by Hony Capital for hospital operations and management services, was listed on the Hong Kong Stock Exchange, with Liu Chuanzhi, Chairman of Legend Holdings, personally attending to support the listing and ring the opening bell.

According to the listing documents, Honghe Renai Medical Group is an operational management group led by a professional team with extensive hospital management experience. By operating and managing hospitals, it plans to integrate medical resources within the regions where its affiliated hospitals are located, restructure regional medical service centers, and provide continuous, systematic, convenient, and high-quality comprehensive medical services to residents in these areas. The group focuses on the diagnosis and treatment of common diseases, frequently occurring illnesses, and chronic conditions. In terms of 2015 revenue, Yangsi Hospital was the largest non-public hospital in Shanghai, while Fuhua Hospital extended the scope of medical services provided by Yangsi Hospital.

Gene: BGI Genomics

Founded in 1999, BGI is a cutting-edge technological institution dedicated to life sciences research. Through an integrated approach encompassing education, research, and application, its business spans molecular genetics research in areas such as human health, medicine, agriculture, animal husbandry, and the conservation of endangered species. As a core entity, BGI participated in the establishment of the China National GeneBank and has founded the Center for Reproductive Health and the Center for Clinical and Medical Health.

According to incomplete statistics, more than 40 venture capital (VC) and private equity (PE) firms have clustered their investments in BGI Genomics, with total investment exceeding RMB 7.2 billion. In 2017, Berry Genomics, which belongs to the first tier of gene sequencing companies alongside BGI Genomics, went public through a reverse merger, marking the maturation of emerging biotechnology companies represented by those focused on genomics.

1.5 Lack of Large-Scale Financing

Top 20 IPO Financing Amounts

In terms of funds raised, WuXi Biologics secured RMB 3.3 billion, far outpacing its peers, with the majority of healthcare companies raising less than RMB 1 billion. Although the average IPO proceeds for healthcare companies declined in 2017, it is encouraging to note that the warming trend in IPOs on the ChiNext board has enabled more young, innovative enterprises to enter the capital markets.

2.1 JD Capital Reaps Bountiful Harvest, Zhangjiang Venture Capital Records Exceptionally High Returns

In 2017, the healthcare sector entered a harvest season for investment. Several firms reaped substantial returns, most notably Zhangjiang Venture Capital, which recorded a 36-fold paper gain on its investment in Tellgen Corporation made a decade earlier. JD Capital, DT Capital Partners, CDH Investments, and other firms also saw multiple portfolio companies successfully complete initial public offerings (IPOs), generating significant returns.

Based on publicly available data, VCBeat has compiled the timing of each investment round made by institutional investors in companies that successfully completed their IPOs during the first half of the year, resulting in this “VCBeat Report on IPO Performance of Healthcare Investors in H1 2017.”

IPO Performance of Healthcare Investment Firms in H1 2017

Data Source: CSRC Website, Choice

JD Capital: The “Wolf” of the Investment World

Since its inception, JD Capital has consistently played the role of a “disruptive innovator” in the industry. In 2017, it secured five initial public offerings (IPOs) for healthcare companies. This “wolf” of the investment world swiftly capitalized on the opening of the ChiNext board to establish its position, introducing assembly-line processes into private equity (PE) investment and rapidly transforming into a diversified financial group holding multiple licenses. To date, JD Capital manages nearly RMB 30 billion in funds, has invested in approximately 300 companies, and has achieved over 50 listed company exits.

Shenzhen Capital Group: Preparing for Global Expansion

As the “leader” of domestic venture capital, Shenzhen Capital Group has consistently delivered outstanding IPO results. In 2017, Haichen Pharmaceutical, BGI Genomics, Zhenghai Biotechnology, and Intco Medical—companies in the healthcare sector—successfully completed their initial public offerings.

As one of the earliest-established and best-performing domestic venture capital firms in China, Shenzhen Capital Group (SCGC) has primarily operated within the domestic market over the past decade, covering fund raising, investment, and exit activities. On June 30, SCGC officially unveiled its RMB 4 billion China-US Fund and signed cooperation agreements with Microsoft (China), KPCB, and other partners, marking the comprehensive launch of SCGC’s internationalization strategy. Ni Zewang, Chairman of SCGC, stated that the firm aims to increase the proportion of foreign currency investments to over 20% by the end of the 13th Five-Year Plan period.

Detong Capital: Healthcare Investment Enters Harvest Season

In 2017, DT Capital Partners’ healthcare sector achieved significant success, with three portfolio companies going public: Kanghui Pharmaceutical, Tiansheng Pharmaceutical, and Hite Bio. Previously, its healthcare investments in companies such as Buchang Pharmaceuticals and Porton Pharma Solutions had already successfully listed, yielding substantial returns. Additionally, DT Capital Partners has invested in other healthcare enterprises, including Xinglong Xili, Kaisheng Technology, Puai Medical Equipment, and Wuxi Luoyi.

Dettong Capital focuses primarily on three investment sectors in the healthcare industry: innovative drugs and high-barrier generic drugs, medical devices and in vitro diagnostics (IVD), and healthcare services. The firm currently manages funds equivalent to RMB 10 billion, with dozens of its portfolio companies having successfully exited through initial public offerings (IPOs) or mergers and acquisitions (M&A).

CDH Venture Partners: A Bumper Harvest in the Healthcare Sector

In January this year, New Century Healthcare, in which it had invested, officially listed on the Hong Kong Stock Exchange, followed by Poly Pharma’s listing on the ChiNext board. On May 16, Zhenghai Biotech officially listed on the ChiNext board of the Shenzhen Stock Exchange.

To date, CDH Investments has facilitated the public listings of nine portfolio companies in the healthcare sector. Previously, companies such as Luye Pharma Group, Kanghong Pharmaceutical, Aier Eye Hospital Group (note: context suggests Kangning Hospital, but standard translation for listed entities should be verified; here we stick to literal "Kangning Hospital" or its known English name if applicable, however, Kangning is often associated with mental health services. Let's use the specific names provided), Harmony Medical, New Century Healthcare, and Poly Pharm have all gone public. CDH Investments’ strategy in the healthcare industry is primarily divided into four segments, with investments in over 30 companies to date. Specifically, it has invested in nine companies in the healthcare services sector, including Ciming Health Checkup, New Century Children’s Hospital, and Kangning Hospital; nine enterprises in the pharmaceutical sector, including Kanghong Pharmaceutical, Luye Pharma Group, and Zhangjiang Bio; twelve companies in the medical devices sector, including Weigao Group and Zhenghai Biotechnology; and, adopting a more cautious approach in the healthcare TMT sector, it has currently invested in only three companies.

Aoyin Capital: Moving Toward Precision Medicine

In 2017, Aoyin Capital saw two of its healthcare portfolio companies go public: Kangtai Biological Products and Menovo Pharmaceutical. Since its establishment in 2009, Aoyin Capital has adhered to an investment philosophy centered on technology-driven growth, supplemented by innovation in business models and creative strategies. Prior to 2011, the firm’s investment focus was broadly within the “big healthcare” sector, spanning both biological vaccines and chemical-based pharmaceuticals. Today, Aoyin Capital concentrates more specifically on niche segments of the healthcare industry, such as in vitro diagnostics (IVD) and precision medicine.

Panlin Capital: 2 IPOs, with a Key Focus on Healthcare

Having strategically positioned itself in China’s healthcare and medical industry for many years, Panlin Capital entered a period of substantial returns in 2017, successfully seeing two of its portfolio companies, Kangtai Biological Products and Hybribio, go public. Since its establishment in 2010, Panlin Capital has focused its investment activities on three key sectors: healthcare, energy conservation and environmental protection, and new consumer models. With a particularly strong emphasis on healthcare, the firm has invested in more than ten projects to date, including Kangtai Biological Products, Hybribio, Deyi Dongfang, Sinocare, YZY Biopharma, Zhikang Boyao, Saian Biology, Ribo Life Science, and Beijing Children’s Hospital (Kyoto).

2.2 New Regulations on Share Reduction Issued, Increasing Exit Difficulties

In 2017, investment institutions reaped substantial profits. Taking a company public is the dream of many investors, but the journey is far from easy. Even firms that invest at the pre-IPO stage must endure a waiting period of two to three years, while others have accompanied their portfolio companies for decades, navigating a path fraught with hardships and helplessness. Now, as these institutions enter their harvest season, they are joyfully reaping the fruits of success.

Looking back on the first half of the year, alongside the joy of a bountiful harvest, there were also moments of concern. On May 27, the China Securities Regulatory Commission (CSRC) issued the “Several Provisions on Share Reduction by Shareholders, Directors, Supervisors, and Senior Executives of Listed Companies.” Dubbed the “strictest new regulations on share reduction in history,” this announcement initially sparked significant controversy. Under the new rules, the pace of institutional exits has slowed, and exit cycles have lengthened slightly; however, the positive effects are gradually becoming apparent. An increasing number of VC/PE firms are returning to value investing, while the once-hot Pre-IPO projects are gradually “cooling down.”

With the announcement late on December 27, 2017, that five out of eight IPO applications reviewed by the Issuance Review Committee were approved while three were rejected, the A-share IPO review work for 2017 came to a close. In 2017, the Issuance Review Committee reviewed IPO applications from 488 companies in total; 380 were approved, 86 were rejected, and 22 had their decisions deferred, resulting in an annual IPO approval rate of only 77.87%. By contrast, in 2016, the committee reviewed 266 companies, rejecting only 18, with an approval rate as high as 90.6%. Among the applicants, 62 were from the healthcare sector: 40 were approved, 7 were rejected, and 15 had their reviews suspended.

Since 2017, the acceleration of IPO reviews has become evident. Healthcare companies constitute a significant portion of IPO applicants; however, their approval rate stands at only 74%, lower than the overall average of 83%. This lower approval rate indicates that healthcare firms face stricter regulatory scrutiny during their initial public offerings, and the China Securities Regulatory Commission (CSRC) has historically maintained a cautious stance toward the healthcare sector.

3.1 Commercial Bribery and Authenticity of Performance Are the Primary Concerns of the Issuance Review Committee

Given the complexity of the pharmaceutical industry across production, distribution, and commercial operations—which requires specialized qualifications—regulatory scrutiny focuses on compliance in manufacturing and sales practices, as well as issues such as commercial bribery and dealer-related matters. Consequently, obtaining approval is more challenging than in other industries.

We have compiled the reasons why 10 companies in the healthcare sector failed to pass regulatory review in 2017, as follows:

Statistics on Reasons for Corporate Rejections

Six key areas of concern include the authenticity of financial performance, business or sales models, sustainable profitability, commercial bribery, fundraising investment projects, and inaccurate information disclosure.

Issues regarding the authenticity of performance and inaccurate information disclosure are absolute red lines. Other issues, such as sales models, internal controls, and product quality, are often concomitant with these two primary concerns. Commercial bribery and GMP certification issues related to fundraising investment projects represent persistent pain points in the pharmaceutical industry. Sustained profitability is a broad category encompassing all aspects of corporate operations. Issues concerning historical evolution have their own specificities and often constitute fatal flaws. Related-party transactions, horizontal competition, asset integrity, and significant changes in directors, supervisors, and senior management are relatively easier to resolve, or indeed should not occur at all; having an application rejected solely on these grounds is hardly justified. Unless there is a major fatal flaw, a company’s rejection is typically the result of multiple adverse factors cumulating to preclude approval, with only a few companies being rejected due to a single factor.

1. Can internal controls effectively prevent commercial bribery?

The pharmaceutical industry features a large number of distributors in the drug distribution chain, complex regulations, and a high propensity for non-compliant practices; therefore, the Issuance Examination Committee places significant emphasis on internal control issues. During its voting meetings, the Committee specifically questioned whether internal controls effectively prevented commercial bribery in the cases of three pharmaceutical companies rejected in 2017 to date: Shenghe Pharmaceutical, Shenghuaxi, and Puhua Pharmaceutical. The primary reason for the rejection of Jiangxi 3L Medical Products Group was deficiencies in the issuer’s internal controls during the reporting period, which failed to effectively prevent sales personnel from forging customer seals and submitting fraudulent invoices for expense reimbursements.

2. Compliance of Business Qualifications.

Pharmaceutical manufacturing requires operational qualifications and production technology patents. If pharmaceutical companies fail to obtain the relevant qualifications in a timely manner, their future business continuity will be affected; therefore, the Issuance Examination Committee places significant emphasis on qualification issues. In 2011, Chengda Pharmaceutical’s IPO application was rejected primarily because it had not yet obtained approval numbers for its active pharmaceutical ingredients (APIs) or Good Manufacturing Practice (GMP) certificates, resulting in operational uncertainties. In 2016, Xidian Pharmaceutical’s IPO application was rejected mainly due to patent-related issues concerning its key product, risperidone orally disintegrating tablets (Ketong).

3. Financial compliance and the appropriateness of accounting practices.

The healthcare industry is characterized by a high proportion of intangible and fixed assets, necessitating particular attention to related accounting treatments. This year, the primary reason for the rejection of Baihe Medical’s application was its non-compliance with accounting standards in the accounting of long-term prepaid expenses. One of the main reasons for the rejection of Puhua Pharmaceutical this year was the presence of various irregularities in financial management and accounting during the reporting period, including sales personnel directly collecting payments from customers, customers making repayments under their personal names, and offsetting sales expenses with payment receipts.

4.2 Establishment of the New Issuance Review Committee: IPO Scrutiny Enters a “Stricter” Normal

On September 30, 2017, the China Securities Regulatory Commission (CSRC) issued an announcement on the appointment of members to the 17th Issuance Review Committee, formally appointing 63 committee members. Unlike previous iterations, this committee did not distinguish between a Main Board Issuance Review Committee and a ChiNext Issuance Review Committee, and thus became commonly known as the “Grand Issuance Review Committee.” Of the 63 members, 42 were full-time and 21 were part-time, falling short of the statutory quota of 66. The establishment of the new Issuance Review Committee in October marked a new era for China’s IPO review process, bringing about significant shifts in underlying concepts.

At the inception of this committee’s term, the “LeEco case” exposed corruption involving two former members. Under the combined influence of intense anti-corruption pressure, lessons drawn from the LeEco case, and the fact that the majority of this Issuance Examination Committee were drawn from regulatory agencies, “comprehensive and stringent review” became the new normal, leading to a surge in rejection rates.

By examining the changes in rejection rates for companies with varying net profits in 2017, we observe a sharp increase in the rejection rates for enterprises with net profits exceeding RMB 100 million and RMB 200 million after the new Issuance Examination Committee assumed office. The long-held philosophy in IPO reviews that “performance is king” and “strong financial performance can overshadow all other deficiencies” has begun to shift. In addition to scrutinizing the authenticity and sustainability of profitability, the Issuance Examination Committee now also places emphasis on the effectiveness of internal controls and the compliance of information disclosure.

The above is a partial excerpt from this report. To download the full version, please scan the QR code below.

Scan the QR code below to become an official VCBeat member and receive the PDF version of the "2017 Annual Report on IPOs of Healthcare Companies." Additionally, over the coming year, you will enjoy unlimited access to comprehensive industry trend reports, timely updates on the latest global investment and financing news, a comprehensive database of healthcare companies, and extensive resources for networking and collaboration.