Will Commercial Insurance + Pharmacy Retail Become a 'Dimensionality Reduction Strike' Transforming the Healthcare Industry?

“Dimensional reduction attack” has frequently appeared in recent business discussions. This concept, which originated in science fiction novels, originally referred to attacking with weapons whose technological level is far superior to that of the target.

In business discussions, it has been extended to mean participating in market competition in ways that competitors do not expect, such as Qihoo 360’s free security model versus a host of paid antivirus software, and the rise of food delivery services alongside the decline of convenient instant foods.

In the healthcare industry, a phenomenon of "dimensional reduction attack" may also occur, such as the integration of commercial insurance and pharmaceutical retail.

Why Commercial Insurance + Pharmaceutical Retail Constitutes a "Dimensional Strike" on the Healthcare Industry: First, this model is highly innovative, currently adopted by only a few companies, giving it significant forward-looking value. Second, it holds immense potential; both the commercial insurance and pharmaceutical retail markets are expanding rapidly, creating strong synergies. Once proven viable, this approach could disrupt traditional medical insurance and pharmaceutical retail sectors. Third, the model aligns with policy directions and market trends, offering a promising new pathway for the transforming healthcare industry.

So, what is the historical evolution of the “commercial insurance + pharmaceutical retail” model? Are there any relatively mature experiences to draw from? Which companies in China are operating in this space? To address these questions, VCBeat (WeChat ID: vcbeat) has reviewed the “commercial insurance + pharmaceutical retail” model and compiled several corporate case studies through interviews.

“How Dimensional Reduction Strikes” Appeared in the United States

The development trajectory of the U.S. healthcare industry has long served as a benchmark for China to study and emulate. The business model combining commercial health insurance with pharmaceutical retail, which leverages asymmetric competitive advantages, also draws inspiration from the United States. Among these, the most mature and comprehensive model is Pharmacy Benefit Management (PBM), representing one of the most refined operational forms within the integrated commercial insurance and pharmaceutical retail sector.

PBM is a product of the U.S. healthcare system. The U.S. health insurance system differs from the universal coverage models in China and some European countries, where insurance funds are centrally managed by the government. In the United States, the predominant model involves employers purchasing health coverage for their employees, with commercial insurance serving as the primary payer.

In this context, insurance institutions have devised various strategies to control medical costs in order to reduce expenditures. Examples include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Point of Service plans (POS), and Accountable Care Organizations (ACOs).

Its primary operational model involves transitioning from fee-for-service to managed care with end-to-end monitoring, strictly controlling healthcare expenditures through health management, disease prevention, and diagnosis-related group (DRG) payment models, thereby reducing medical costs for insurers and employers.

The PBM business model involves collaboration between relevant organizations and insurance providers, pharmaceutical companies, healthcare institutions, and retail pharmacies to intervene in the medication process. By reviewing and modifying prescriptions—such as substituting originator drugs with lower-priced generics—without compromising patient treatment outcomes, it ultimately aims to control healthcare expenditures.

The core services of PBMs include medication utilization management, intervention in drug access methods, differentiated reimbursement rates, and chronic disease management. Among these, chronic disease management refers to the long-term monitoring of medication use among patients with chronic conditions, aiming to improve medication adherence, reduce the risk of severe complications, and achieve cost containment.

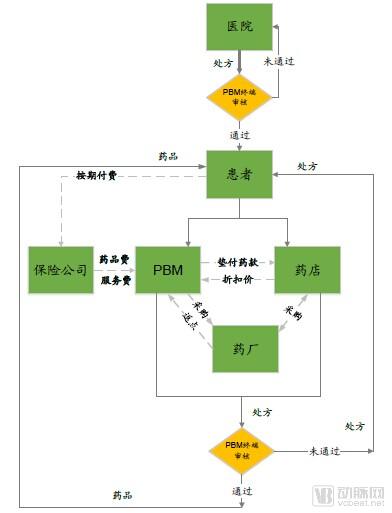

PBM Organizational Processes

Source: Tiantuo Consulting

The primary reason PBM companies have become the critical link connecting the upstream and downstream segments of the pharmaceutical industry chain is their ability to effectively balance the interests of all stakeholders. By leveraging third-party system operations, PBMs integrate pharmaceutical demanders, suppliers, and payers. This model enables them to acquire a large-scale base of corporate and individual members at the front end, which serves as bargaining leverage in negotiations with pharmaceutical manufacturers and retail pharmacies. Consequently, this ensures a stable supply of medications while also satisfying the needs of healthcare consumers.

The most prominent PBM in the United States is ESI Group, fully known as Express Scripts. According to its 2016 annual report, it covered over 95% of retail pharmacies nationwide, with annual revenue reaching $100.2 billion and a net profit of $3.4 billion. It is also the third-largest pharmaceutical retail organization in the U.S., excluding CVS and Walgreens. It provides medication supplies, including new specialty drugs and investigational drugs, to its managed members through mail-order and online pharmacy services.

CVS, the largest pharmaceutical retailer in the United States, also maintains a substantial PBM business. Through its subsidiary CVS Caremark, it provides pharmacy benefit management services, with key components including health management programs and the processing of commercial medical insurance claims.

At the end of 2017, CVS acquired Aetna Inc. for $69 billion, a move widely seen as a signal of CVS’s increased commitment to the insurance business. Commentators stated that this would bring about new transformations in the health insurance and pharmaceutical retail industries, both in the United States and globally.

The Insurance-Plus-Pharmaceuticals Model Lands in China

The PBM business model crossed the ocean to China several years ago. At that time, Haihong Holdings partnered with ESI Group to launch pilot programs for medical insurance cost containment, making PBM the flagship business of Haihong Holdings.

Haihong Holdings’ approach is to operate as a third-party tool provider, entering into cooperative agreements with local healthcare security administrations to build an intelligent prescription-assisted review platform and deliver refined management services for medical insurance funds.

Subsequently, companies such as Jiashitang, Wonders Information, Winning Health, and Ping An Good Doctor also ventured into the PBM business, with their primary focus being collaboration with medical insurance fund pooling authorities.

However, the implementation of PBM services in China has not been smooth. According to Haihong Holdings’ annual report, its PBM business did not generate actual revenue for the company in 2009 and 2010. After 2012, annual revenue from this segment remained at approximately RMB 10 million, with limited growth over the years. In 2016, Haihong Holdings reported PBM business revenue of RMB 13.132 million against costs of RMB 42.422 million.

Haihong Holdings stated in its annual report that, due to varying degrees of business progress across different regions, a unified fee structure has not yet been established. Moving forward, the company will build on its existing business foundation to actively explore diverse pricing models, such as fee-for-service and proportional fees based on fund size, while maintaining active communication with relevant authorities.

PBM services have faced significant challenges in China due to multiple factors. First, there are differences between China and the United States in terms of healthcare payers, fragmented management of medical insurance funds, and divergent needs and models for cost containment. Second, the lack of foundational infrastructure—such as limited interoperability and mutual recognition of medical information across hospitals, conflicts of interest related to prescription rights, difficulties in standardizing drug formularies, and the widespread practice of subsidizing healthcare providers through drug sales—has constrained the development of PBM services.

However, the core of PBM extends beyond merely managing medical insurance funds; its collaboration with commercial health insurance is even more promising. For instance, PBM companies can provide commercial insurers with services such as product design, underwriting and claims processing, medical data services, and sales channel support through a third-party service model. Currently, some enterprises in China are already exploring this approach.

Below, we will introduce some of these enterprises and their business models.

Quanyi Health: PBM + Chronic Disease Management

Quanyi Health is a subsidiary of Quanyuantang. Quanyuantang is a well-known pharmaceutical e-commerce enterprise in China and a company listed on the National Equities Exchange and Quotations (NEEQ). It reported annual revenue of RMB 476 million in 2016 and revenue of RMB 261 million in the first half of 2017, ranking among the top tier of pharmaceutical e-commerce companies.

In September 2016, Quanyi Health launched the internet health insurance product “Tang Bao Bao,” marking the official implementation of Quan Yuantang’s PBM business.

Quanyi Health's current main business is:

1. Health Insurance Product Development: Primarily collaborate with insurance companies and reinsurers to develop health insurance products;

2. Health Management Services: Providing comprehensive, one-stop health management services to institutions such as insurance companies, insurance brokerage sales firms, and human resources companies;

3. Innovative Sales Platform: Establish a non-traditional, broader insurance promotion platform through proprietary or partner platforms (including Quanyuantang Pharmacy) and affiliated pharmaceutical companies.

Since its establishment in 2016, Quanyi Health has officially launched two chronic disease management insurance products, including:

Tangbaobao—Comprehensive Insurance Plan for Diabetes Complications: An innovative insurance product developed in collaboration with Asia Pacific Property & Casualty Insurance, it is China’s first PBM (Pharmacy Benefit Management) insurance product that integrates insurance coverage with medication expenditure (cost control). Individuals with diabetes are eligible for enrollment, benefiting from low premiums and comprehensive, convenient support services. Quanyi Health is currently developing the second generation of Tangbaobao.

Tangtongbao – Diabetes Complications Insurance (Blindness Coverage): Jointly developed by PICC (China’s largest insurer), Munich Re (one of the world’s largest reinsurers), diabetic retinopathy screening institutions, and leading pharmaceutical companies and pharmacies. The base coverage amount is RMB 5,000, which can be gradually increased with greater utilization of medications or diabetic retinopathy screening services, up to a maximum of RMB 150,000. This product enables screening institutions and pharmaceutical companies/pharmacies to upgrade their customer service systems from mere customer support to an integrated model of “service plus protection.” It is a win-win innovative insurance product that represents not only innovation in sales channels but also in business philosophy and operational strategies.

According to Su Peiyong, General Manager of Quanyi Health, in addition to the development of the aforementioned health insurance products, Quanyi Health has independently developed a one-stop health management platform that provides services including online consultations (with prescription issuance), pharmacist services, online ordering, appointment scheduling, green channels for medical care, and overseas medical consultation services.

Quanyi Health is currently providing such services to over 70,000 members and expects even faster growth in 2018. In addition, it is collaborating with insurance companies to integrate its one-stop services with insurance sales and promotion.

In terms of insurance promotion, in 2017, Quanyi Health established an in-depth partnership with the online platforms of Grade A tertiary hospitals to recommend targeted insurance products to their users. In the first quarter of 2018, Quanyi Health will provide partner pharmacy stores with a dedicated platform to promote personalized and scenario-based insurance products to in-store consumers. Through integrated online and offline activities, this initiative aims to bring insurance products closer to the front lines of consumer engagement.

Su Peiyong revealed that Quanyi Health will next offer a wider variety of chronic disease health insurance products, collaborating with specific pharmaceutical manufacturers to customize product designs; the company will also continue to deepen its efforts in health management and the promotion of insurance products.

JianYiBao: Medication Coverage & Worry-Free Medication

JianYiBao was founded in late 2016 by Zhang Shengming. Previously, he held marketing and sales roles at foreign pharmaceutical companies and also gained experience in the insurance industry, where he participated in and led the development and operation of numerous insurance products tailored for individuals with chronic diseases. To innovate and more effectively integrate insurance with pharmaceuticals, Zhang conceived the idea of starting a business, leading to the establishment of JianYiBao.

Zhang Shengming introduced that Jianyibao currently offers two main products: “Medication Coverage” and “Worry-Free Medication.”

"Medication coverage targets patient populations. Through a collaboration among Jianyibao, pharmaceutical companies, and insurance providers, insurance products tailored to specific drug indications have been developed. 'This model does not impose additional costs on patients; instead, it enhances medication adherence, reduces the risk of disease progression, and ultimately lowers overall healthcare expenditures. In the event of complications, partner insurers provide prompt compensation, thereby alleviating patients' financial burdens and preventing poverty caused or exacerbated by illness, which aligns with national policy directives,' stated Zhang Shengming."

"Worry-Free Medication" primarily targets pharmaceutical retail channels, including chain pharmacies, e-pharmacies, and O2O pharmaceutical enterprises. In the event of serious adverse reactions to medications sold through these channels, insurance companies provide corresponding compensation. The "Worry-Free Medication" program effectively alleviates doctor-patient conflicts and delivers timely and effective assistance to patients.

JianYiBao will participate in the design of insured subjects, coverage responsibilities, and actuarial premium rates for the aforementioned insurance types, collaborating with insurance companies to develop related insurance products. The insurance company also authorizes JianYiBao to assist in handling claim appeals for certain insurance types.

Currently, Jianyibao has established a deep partnership with Anxin Insurance and entered into a strategic cooperation with Fosun Group in areas such as insurance product development, policy services, medical data, and health management services. It serves over ten key clients, including pharmaceutical companies, online pharmaceutical e-commerce platforms, and retail pharmacies.

Zhang Shengming shared with VCBeat data on a medication coverage product co-developed by Jianyibao and a globally renowned pharmaceutical company: The project was officially launched in July 2017. As of December 31, 2017, more than 10,000 patients across China had participated in the coverage program, obtaining over 50,000 insurance policies.

JianYiBao is currently undergoing its first round of financing. Its development plan for 2018 is as follows: to implement a coordinated online and offline strategy, deepen the cultivation of its two core products—Medication Coverage and Worry-Free Medication—develop more insurance products for chronic diseases, explore further cooperation with distribution channels, and accelerate market expansion.

What Lies Ahead for Commercial Insurance and Pharmaceutical Retail?

In addition to the two cases mentioned above, companies such as Nanjing Guoyao and Yaolian have also made attempts in the integration of insurance and pharmaceutical retail.

In July 2017, Nanjing Sinopharm partnered with Ping An Health Insurance to develop and launch “Kongtang Bao,” an insurance product covering diabetic complications, designed to help patients with diabetes mitigate the risks of complications and financial burdens. Kongtang Bao is an integrated online-offline chronic disease management and insurance solution that leverages Nanjing Sinopharm’s chain pharmacies to provide diabetes management services to insured patients. The coverage includes reimbursement for certain glucose-lowering medications, medical devices, and consumables not listed in the national medical insurance catalog, covers multiple types of complications, and offers sum assured ranging from RMB 50,000 to RMB 100,000.

Yaolian is a value-added service platform for chain pharmacies under Shanghai Juyin Information Technology, providing services such as expired drug replacement and chronic disease management. Its initiative in integrating insurance with pharmaceutical retail involves partnering with insurance companies to incorporate health insurance products into pharmacy offerings as value-added services, thereby assisting pharmacies in customer acquisition and operations.

From the above cases, we can observe several notable characteristics of the domestic commercial insurance plus pharmaceutical retail business model:

1. This model is primarily targeted at patients with chronic diseases, such as diabetes and hypertension;

2. Insurance products are jointly developed by insurance companies, third-party service providers, retail pharmacies, and other entities;

3. Product launches are still in their early stages, with patient outreach primarily achieved through medication purchase incentives and value-added services.

In light of these characteristics, Su Peiyong, General Manager of Quanyi Health, stated that the PBM (Pharmacy Benefit Management) model is still in its infancy in China, representing an immature market that requires extensive education for both partners and end users. Zhang Shengming, founder of Jianyibao, also believes that the insurance industry has previously left a poor “impression” on consumers; to achieve full consumer acceptance, continuous user education is essential. Key efforts should focus on simplifying policy terms, highlighting claims settlement models, streamlining the claims process, and introducing internet-based tools.

From the perspective of the integration of health insurance and pharmaceutical retail, the future is highly promising, as both sectors are experiencing rapid market growth and align with the direction of healthcare reform.

From the perspective of the health insurance market, data from the China Insurance Regulatory Commission (CIRC) shows that the compound annual growth rate (CAGR) of the health insurance market size was 42% from 2011 to 2016. In 2017, the original insurance premium income from health insurance business reached RMB 410.554 billion by November, representing a year-on-year increase of 6.87%. The health insurance market size is projected to reach RMB 1 trillion by 2020.

In terms of insurance coverage for individuals with pre-existing conditions, since 2015, applicants have been permitted to obtain coverage despite existing health issues, provided they make full disclosures. Correspondingly, health insurance companies began launching health insurance products tailored to specific patient populations during this period. For instance, ZhongAn Insurance launched "Tang Xiaobei 1.0" in November 2015, and subsequently introduced "Tang Xiaobei 2.0," "Kangkang Hypertension Insurance," and "Omron Hypertension Insurance," among others.

From the perspective of the pharmaceutical retail market, the market size has maintained an average annual growth rate of over 10% in the past five years. In 2016, the market size reached RMB 337.7 billion, and it is projected to exceed RMB 370 billion in 2017. The compound annual growth rate (CAGR) of B2C pharmaceutical e-commerce has surpassed 100% in the past five years, with the transaction volume expected to exceed RMB 50 billion in 2017.

The “Health Insurance + Pharmaceutical Retail” model will leverage these two massive markets. If developed properly, it could expand beyond patients with chronic diseases to cover a broader healthy population, establishing a comprehensive healthcare service system that integrates health insurance, health management, disease prevention, and medical services, thereby providing more valuable healthcare security for the nation.