Low Barriers, High Valuations, Easy Exits: Mainland Healthcare Firms Eye Hong Kong IPO Surge

The Hong Kong Stock Exchange is undergoing its most significant listing rule reforms in 25 years, increasingly becoming the preferred destination for mainland China’s growth-oriented enterprises to access capital markets.

On February 23, the Hong Kong Stock Exchange released the Consultation Paper on the Listing Regime for Emerging and Innovative Companies (hereinafter referred to as the “Consultation Paper”). The Consultation Paper indicates that the Hong Kong Stock Exchange will permit the following companies to list in Hong Kong:

a) Biotechnology companies that fail to pass the financial eligibility test, including those without a record of revenue or profitability;

b) High-growth and innovative companies with dual-class share structures;

c) Eligible issuers seeking a secondary listing on the Stock Exchange.

Mainland Chinese enterprises, particularly internet companies and innovative pharmaceutical and biotechnology firms, are showing strong enthusiasm for listing in Hong Kong. Tech companies such as Xiaomi, Kuaishou, and Lufax, as well as healthcare companies including Ping An Good Doctor, WeDoctor, and Henlius Biotech, have recently been reported to be planning Hong Kong listings.

What is the Hong Kong Stock Exchange’s position in the global capital markets, and what achievements has it made in the past? What are the listing rules for mainland Chinese companies in Hong Kong, and what treatment will they receive? How have mainland Chinese companies, particularly those in the pharmaceutical sector, performed after listing on the HKEX, and which high-quality investment targets stand out? VCBeat (WeChat ID: vcbeat) aims to address these questions and unravel the underlying dynamics behind the wave of listings in Hong Kong.

HKEX: An International Capital Market at Your Doorstep

The Hong Kong Stock Exchange is a world-leading capital market. According to the market profile data released by the Hong Kong Stock Exchange in December 2017:

As of the end of 2017, there were 2,118 companies listed on the Main Board and GEM of the Hong Kong Stock Exchange; the total market capitalization was approximately HK$34 trillion, representing a 37% increase from the previous year.

In 2017, 164 companies were listed on the Hong Kong Stock Exchange, a 38% increase from 2016. The total amount raised through IPOs was HK$128.2 billion, a 34.4% decrease from the previous year.

The average daily transaction amount was RMB 88.2 billion, representing a 32% increase from RMB 66.9 billion in 2016.

For comparison, we can look at the data from the Shenzhen Stock Exchange:

As of the end of 2017, the number of listed companies on the Shenzhen Stock Exchange (SZSE) reached 2,089, an increase of 219 from the previous year; the total market capitalization stood at RMB 23.58 trillion, representing a 5.69% year-on-year increase.

In 2017, there were 222 initial public offerings (IPOs), representing a 79.03% increase from the previous year. The total capital raised through IPOs amounted to RMB 92.453 billion, a year-on-year increase of 93.07%.

The cumulative transaction volume reached RMB 61.69 trillion, a year-on-year decrease of 20.51%. (The average daily transaction volume was approximately RMB 169 billion.)

The above data indicate that the Hong Kong Stock Exchange (HKEX) and the Shenzhen Stock Exchange (SZSE) are roughly equivalent in terms of the number of listed companies, but the total market capitalization of Hong Kong stocks is higher than that of the Shenzhen market. In terms of trading volume, the activity level of Hong Kong stocks is lower than that of the Shenzhen market. Meanwhile, both markets have opened IPO channels; the number of companies going public in 2017 saw a significant increase in both places, but the amount of funds raised through IPOs on the HKEX declined, whereas the SZSE experienced a substantial rise.

Comparison of Data Between HKEX and SZSE (End of 2017)

Another major “highlight” of the Hong Kong Stock Exchange (HKEX) is, of course, the Chinese mainland market. As of December 2017, there were 640 mainland private enterprises listed in Hong Kong, accounting for 66.2% of the total market capitalization and 78.4% of the total trading value. It can be said that mainland companies have underpinned the “core foundation” of the HKEX.

Following the implementation of the Stock Connect program, southbound capital has flowed into the Hong Kong Stock Exchange in pursuit of investment opportunities, with average daily trading volumes reaching approximately HK$10 billion, accounting for about 10% of the exchange’s total daily turnover.

In addition to the securities market, the HKEX Group also operates two major markets: the Hong Kong Futures Exchange and the London Metal Exchange.

As China’s international financial center, Hong Kong possesses unique advantages and serves as a vital link between China and global investors. As one of the largest securities trading markets in the world, the Hong Kong Stock Exchange (HKEX) effectively acts as a springboard for the internationalization of Chinese enterprises. With a series of reforms such as the Shanghai-Hong Kong Stock Connect, the Shenzhen-Hong Kong Stock Connect, and the Bond Connect, the Hong Kong Exchanges and Clearing Limited has fostered closer ties with mainland and global investors, offering increasingly diverse participation channels. This is also a significant factor attracting mainland companies to list in Hong Kong.

Reform: The New Economy Transformation of the Hong Kong Stock Exchange

Mainland Chinese companies’ enthusiasm for listing in Hong Kong is partly attributable to the Hong Kong Stock Exchange’s relatively more lenient listing requirements compared with the A-share market.

Among these, the most critical factor is profitability.

Listing Requirements for the Main Board and SME Board of A-Shares:

1. The net profit for each of the last three fiscal years has been positive, with a cumulative total exceeding RMB 30 million; the net profit shall be calculated based on the lower of the figures before and after deducting non-recurring gains and losses;

2. The cumulative net cash flow from operating activities over the most recent three fiscal years exceeds RMB 50 million; or the cumulative operating revenue over the most recent three fiscal years exceeds RMB 300 million.

Even the ChiNext board requires: consecutive profitability for the past two years, with cumulative net profit of no less than RMB 10 million over the past two years; or profitability in the most recent year, with operating revenue of no less than RMB 50 million in that year. Net profit shall be calculated based on the lower of the figures before and after deducting non-recurring gains and losses.

Revenue and Profitability Have Become the Biggest Obstacle for Many Technology and Pharmaceutical/Biotech Companies Prior to Their IPOs. Even if a company operates at a very large scale and is experiencing continuous growth, it will still not be approved for listing if it fails to meet profitability requirements.

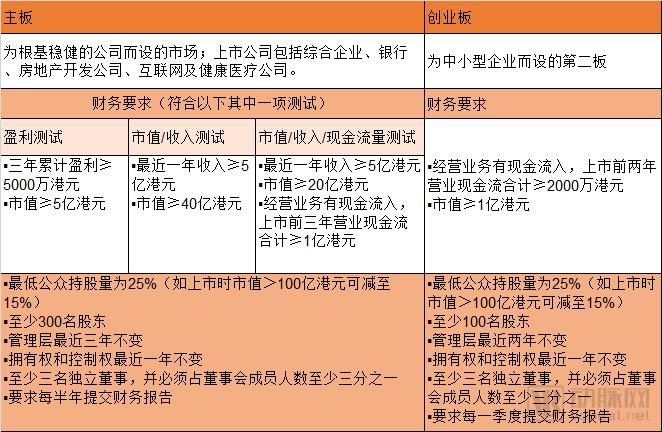

The Hong Kong Stock Exchange (HKEX) does not impose a mandatory profitability requirement on companies seeking listing; instead, they can meet financial eligibility criteria through various assessment methods. For instance, under the Profitability Test, a company is only required to have an aggregate profit of over HK$50 million in the three years preceding its listing and a market capitalization exceeding HK$500 million, which is relatively achievable for the vast majority of high-growth enterprises.

Listing Requirements of the Hong Kong Stock Exchange

Meanwhile, the Hong Kong Stock Exchange is preparing new listing rule reforms, proposing to include the following three types of companies in its listing framework:

1. Emerging and innovative industry issuers with weighted voting rights structures—companies with dual-class share structures;

2. Biotech issuers that are not yet profitable/have no revenue;

3. Overseas-listed companies applying for secondary listing in Hong Kong.

At a media luncheon in 2018, Charles Li, CEO of the Hong Kong Exchanges and Clearing Limited (HKEX), revealed that reforming the listing rules would be HKEX’s “top priority” for the year, aiming to “ensure that the fundraising market keeps pace with the times, enhance connectivity in the equity market, and boost the competitiveness of the derivatives market.”

On February 23, the Hong Kong Stock Exchange (HKEX) released its Consultation Paper as scheduled, with reforms to its listing regime advancing steadily. The proposed amendments to the HKEX Listing Rules are expected to be finalized by mid-2018, paving a fast-track route to Hong Kong listings for the three aforementioned categories of companies.

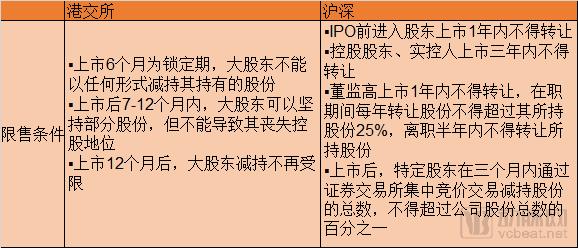

In addition to the relatively easier process of “going public,” exiting the Hong Kong Stock Exchange (HKEX) is also simpler. Its listing lock-up period is shorter than that of A-shares, and exit options are more diversified.

Comparison of Delisting Conditions: HKEX vs. Shanghai and Shenzhen Stock Exchanges

This means that investors can quickly realize growth returns from their portfolio companies, with shorter investment horizons and more controllable risk-return profiles. Driven by institutional investors, these new-era companies will soon embark on their IPO journeys in the Hong Kong stock market.

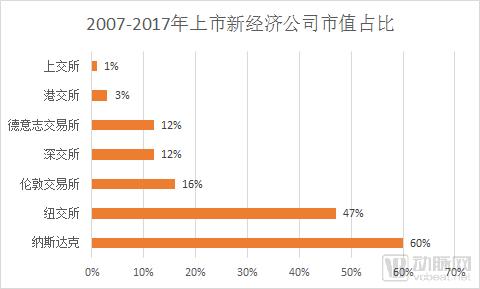

These changes at the Hong Kong Stock Exchange (HKEX) are referred to as “new economy transformation.” The HKEX defines the “new economy” as encompassing biotechnology, healthcare technology, internet software and services, computers and peripheral equipment, among other sectors.

Data shows that new-economy companies account for 3% of the total market capitalization of firms listed on the Hong Kong Stock Exchange (HKEX), compared with 60% and 47% on the NASDAQ and the New York Stock Exchange (NYSE), respectively. Even the Shenzhen Stock Exchange, in close proximity, sees a significantly higher proportion, with new-economy companies representing 12% of its total market cap.

Market Capitalization Data of New Economy Companies on Globally Renowned Exchanges

Source: HKEX Issues "Framework Consultation Paper – Proposed Establishment of the Innovation Board"

Moreover, Hong Kong’s market share remains minimal in some of the fastest-growing sectors globally: Pharmaceuticals, Biotechnology & Life Sciences (1%), Healthcare Equipment & Services (1%), and Software & Services (9%, which drops to just 1% after excluding Tencent).

This reflects the HKEX’s historical preference for blue-chip stocks and the conservative nature of its investors, which also left the exchange out of step with the new economy driven by the previous wave of internet-driven transformation.

A particularly intriguing case is that the Hong Kong Stock Exchange (HKEX) “missed” Alibaba in 2013—a technology company with a dual-class share structure—which was widely regarded as a regrettable oversight at the time. In the aftermath, HKEX began deliberating reforms to its listing rules, placing greater emphasis on high-growth technology and innovative enterprises.

Currently, Tencent, which went public in 2004, is the only well-known global new-economy company listed on the Hong Kong stock market. Apart from Tencent, other new-economy companies have relatively smaller market capitalizations.

The “new economy” transformation of the Hong Kong Stock Exchange is essentially a pursuit of the next wave of economic opportunities—where the next cohort of large-scale companies may emerge from the technology and pharmaceutical/biotechnology sectors.

Performance: A Value Depression Gaining Increasing Attention

The Hong Kong Stock Exchange is dominated by institutional investors, who place greater emphasis on the “fundamentals” of listed companies, resulting in undervaluation of high-growth firms.

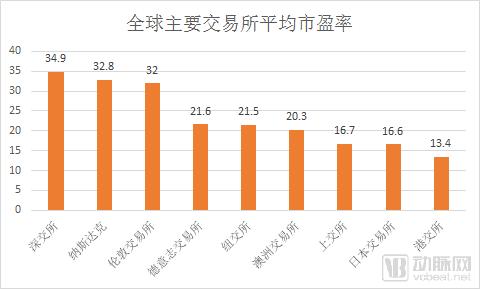

According to the HKEX’s consultation paper, the Hong Kong Stock Exchange has the lowest market valuation among major global exchanges when measured by price-to-earnings (P/E) ratio, at just 13.4x, compared with an industry average P/E ratio of 24.6x.

High-growth industries are undervalued on the Hong Kong Stock Exchange, which may lead to market stagnation and waning investor interest, further depressing valuations and thereby undermining Hong Kong’s appeal to potential new issuers.

After the Hong Kong Stock Exchange administered a “shot in the arm” to the new economy, relevant companies and investors are integrating into this value depression, rediscovering the HKEX’s investment and financing value.

The Hang Seng Index reached an all-time high of 33,484.08 points during intraday trading on January 29, 2018, which, to some extent, corroborates the rise of Hong Kong stocks.

In fact, the Hang Seng Index has been on a continuous upward trajectory since February 2016. By the end of 2017, the Hang Seng Index closed at 29,919.15 points, representing a 36% increase from the end of 2016. In January 2018, it closed at 33,154.12 points, marking an approximate 10.8% rise from the end of 2017, significantly outperforming other major global market indices.

Hong Kong stocks are ushering in a new “golden age” of sustained growth. With mainland Chinese insurance capital, mutual funds, and various asset management funds flowing south to seek opportunities, coupled with international investors’ pursuit of China-concept stocks, the Hong Kong stock market will continue to prosper.

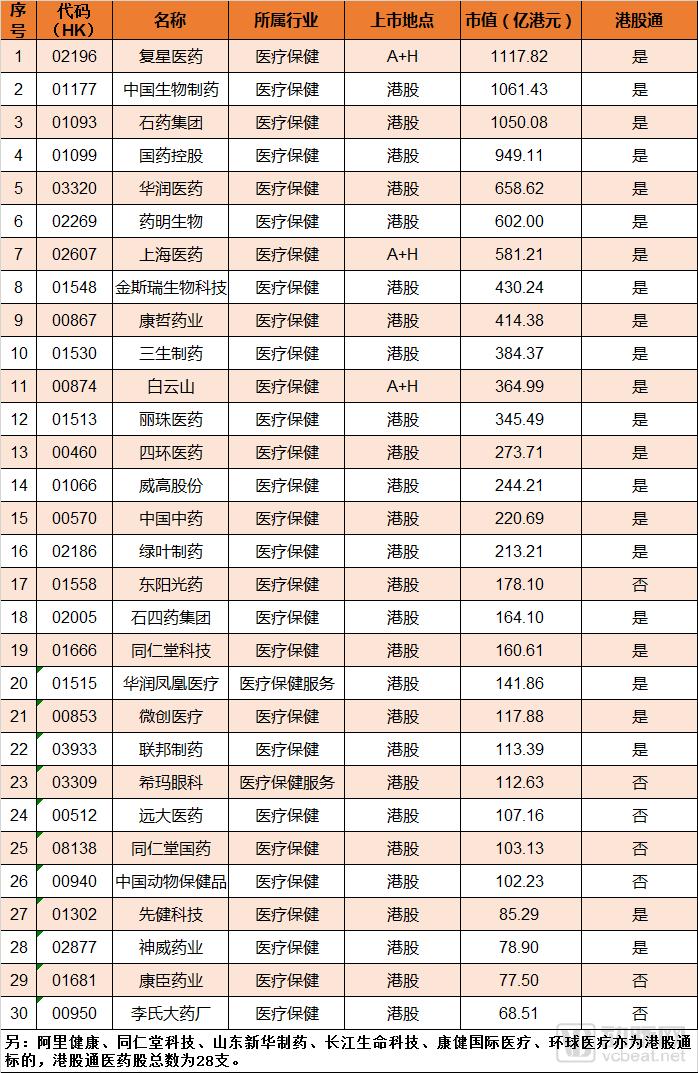

Scan of Hong Kong-Listed Pharmaceutical Companies

Recently, the news that Ping An Good Doctor has submitted an application for listing in Hong Kong continues to gain traction, drawing attention from professionals in the healthcare industry.

Since its establishment in November 2014, Ping An Good Doctor submitted its prospectus and reached the IPO stage in just over three years. This rocket-like growth speed has created a miracle in the internet healthcare industry. It is expected that Ping An Good Doctor will list on the Hong Kong Stock Exchange as early as the second quarter of 2018, becoming the first mainland Chinese internet healthcare company to enter the secondary market.

Behind the miracle, more healthcare companies are reportedly preparing for Hong Kong IPOs, including WeDoctor, Henlius, and Hua Medicine.

We can examine the composition and market performance of healthcare companies listed on the Hong Kong Stock Exchange:

According to Choice statistics, there are a total of 117 companies under the Healthcare and Services category on the Hong Kong Stock Exchange, of which 28 are included in the Stock Connect program. There are five A+H pharmaceutical stocks, namely: Shanghai Pharma, Fosun Pharma, Baiyunshan, Livzon Pharmaceutical Group, and Xinhua Pharmaceutical.

We selected the top 30 healthcare companies listed on the Hong Kong Stock Exchange by market capitalization. The combined market cap of these 30 companies totals HK$1.05 trillion, accounting for over 99% of the total market capitalization of pharmaceutical stocks on the Hong Kong Stock Exchange, thereby essentially representing the full landscape of the sector.

The Hang Seng Industry Classification is less granular than the A-share classification, with most Hong Kong-listed pharmaceutical stocks categorized under Healthcare. According to the Shenwan Industry Classification, the composition of Hong Kong-listed pharmaceutical companies is relatively comprehensive, featuring representative enterprises in traditional Chinese medicine, chemical drugs, biotechnology, medical devices, pharmaceutical distribution, and healthcare services.

We have compiled statistics,The average P/E ratio of profitable companies in the Hong Kong-listed healthcare sector is 115x.,The average P/E ratio of profitable companies in the A-share pharmaceutical and biotechnology sector is 80x.,This indicates that healthcare companies enjoy higher valuations in the Hong Kong stock market—even when the overall valuation level of the Hong Kong market is lower than that of the A-share market.(Based on the TTM P/E ratio at the midday trading session on February 7)

Over the past year, WuXi Biologics and C-MER Eye Care, both well-known players in the industry, have listed in Hong Kong and attracted significant market attention. WuXi Biologics currently has a market capitalization of approximately HK$58 billion, with a trailing twelve-month (TTM) price-to-earnings (P/E) ratio of around 350x. C-MER Eye Care has a market capitalization of roughly HK$11.1 billion, with a TTM P/E ratio of 214x. By comparison, Joinn Laboratories, a newly listed contract research organization (CRO) on China’s A-share market, has a market capitalization of approximately RMB 3.814 billion, with a TTM P/E ratio of only 51x. Aier Eye Hospital has a market capitalization of about RMB 51.5 billion, with a TTM P/E ratio of 71.35x.

In its “2018 Investment Strategy Report on the Hong Kong Stock Market’s Healthcare Sector,” Guosen Securities pointed out that the appeal of healthcare stocks listed in Hong Kong lies in:

1) Compared with A-shares, high-quality companies of the same type in the Hong Kong stock market have lower valuations—creating a valuation depression;

2) The Hong Kong market features unique, scarce investment targets not available in the A-share market;

3) A portion of small- and mid-cap companies are significantly undervalued due to long-term neglect, with their investment value urgently requiring discovery and revaluation;

4) The Hong Kong Stock Exchange’s new listing policies will attract more innovative biotechnology companies from both domestic and international markets to list in Hong Kong. The pilot program for full circulation of H-shares commenced in the first quarter of 2018. If the scope of this program is expanded in the future, a number of Hong Kong-listed companies with total market capitalizations exceeding RMB 5 billion are expected to become eligible for the Stock Connect scheme and gradually achieve full share circulation. This will significantly incentivize company management and attract investment from domestic institutional investors.

High-quality targets in the healthcare sector of the Hong Kong Stock Exchange include:

Leading Large-Cap Innovative Drug Companies

Its long-term investment value is prominent, with the potential to continuously enjoy a valuation premium. This includes large-cap industry leaders such as 3SBio, CSPC Pharmaceutical Group, Fosun Pharma, and Sino Biopharmaceutical, which are characterized by substantial R&D investment, a rich pipeline of drugs under development, and clear visibility into future performance growth.

Rare High-Growth Biotech Investment Target

GenScript Biotech (1548.HK), the leading company in gene synthesis and cellular immunotherapy (CAR-T technology); WuXi Biologics (2269.HK), the leading company in biopharmaceutical contract research organization (CRO) services.

Value Depression, Niche Market Leaders with Certain Growth Potential

Significantly Undervalued Leader in TCM Formula Granules: China Traditional Chinese Medicine Holdings (0570.HK);

Turning Point in Performance, Entering R&D Harvest Period: Lee's Pharmaceutical (00950.HK);

High Growth in Insulin, Antibiotic Business Reaches Inflection Point: The United Laboratories (03933.HK);

Leading Large-Volume Parenteral Manufacturer Shijiazhuang No.4 Pharmaceutical Group (2005.HK): Benefiting from Deep Industry Consolidation with Rapid Performance Rebound;

Leading Anti-Influenza Chemical Drug Company with High-Growth Core Products and Promising Pipeline: Sunshine Guojian Pharmaceutical (1558.HK);

A Leading Cardiovascular Device Company with Technological Leadership and High-Potential Products in the Pipeline: LifeTech Scientific (1302.HK);

Steady Growth, Valuation Depression: Baiyunshan (00874.HK), Konsun Pharmaceutical (1681.HK), Tongrentang Technologies (1666.HK).

Leading pharmaceutical commercial companies with sufficient adjustments

In the long term, policy support will continue to drive consolidation in the pharmaceutical distribution sector, with industry leaders benefiting from this integration. In the short term, however, leading companies—including Shanghai Pharmaceuticals—have seen their growth rates slow due to the impact of the “Two-Invoice System” on wholesale and allocation operations. The adverse effects are expected to diminish after mid-2018, paving the way for accelerated growth. Investors should focus on well-adjusted, nationally oriented distribution leaders with attractive valuations, such as China Resources Pharmaceutical (3320.HK), Shanghai Pharmaceuticals (2607.HK), and Sinopharm Group (1099.HK).

Overall, as one of the world’s largest financial and securities markets, the Hong Kong Stock Exchange (HKEX) serves as a vital channel for Chinese companies to raise capital internationally and pursue global expansion. Historically, the HKEX has favored blue-chip stocks, with investors tending toward conservative strategies. However, this landscape is being reshaped by the rise of the new economy. The phenomenon of Hong Kong-listed stocks being undervalued is changing, potentially ushering in a “golden age” of sustained growth for the Hong Kong stock market.

For healthcare companies, the Hong Kong stock market offers the advantages of low entry barriers, high valuations, and easy exit. Following the Hong Kong Stock Exchange’s “new economy” reforms, more high-quality healthcare and biotechnology companies are expected to list on the exchange. A wave of mainland Chinese healthcare enterprises listing in Hong Kong may emerge in 2018.