Chinese Senior Living Real Estate Report: Enterprises Compete for Strategic High Ground as Platformization Emerges as Key Trend

The concept of senior living real estate originated in economically developed countries that were among the first to enter an aging society in the 1970s. It refers to the integration of elderly care themes into real estate development projects to meet the growing market demand for senior services.

Senior housing real estate must incorporate age-friendly design across all aspects, including architectural design, landscape planning, decoration standards, supporting facilities, and service protocols. Traditional senior housing development closely follows the patterns of high-end residential property development.

It can be said that senior living real estate is based on traditional real estate projects, yet surpasses them in terms of services and supporting facilities. This imposes high competency requirements on the entities responsible for project implementation and operations. Currently, the primary entities involved in the implementation and operation of large-scale senior living real estate projects in China are experienced large-scale real estate enterprises and well-capitalized large insurance companies.

With the intensifying aging of society and rising household consumption power, an explosion in demand for senior housing real estate is an inevitable outcome of historical development. By analyzing the industry’s macro environment, fundamentals, and benchmark companies, and drawing on international development experience, we aim to identify the current competitive landscape, the core competencies and capability requirements of market participants, and future growth opportunities for the industry.

Having reviewed over 500,000 words of relevant literature and employing methods such as field research, telephone surveys, and the synthesis of industry expert opinions, we have compiled this comprehensive analysis report on senior living real estate, exceeding 20,000 words in length. This report not only provides a holistic overview of the industry but also includes substantial strategic development recommendations and operational data analysis, offering a thorough interpretation ranging from the micro to the macro level.

At the macro level, we conducted a comprehensive analysis of industry-related policies and, through quantitative modeling of multiple macroeconomic indicators combined with international development experience, identified regional demand potential and projected development trends for the senior housing real estate sector over the next 30 years.

At the meso level, a comprehensive scan of the industry was conducted to provide an in-depth analysis of the industry landscape and competitive dynamics, thereby identifying the core competitive factors in this field. Meanwhile, the overseas elderly care industry was also subjected to an in-depth analysis;

At the micro level, we conducted a comprehensive analysis of benchmark enterprises, covering multiple dimensions such as corporate strategy, project details, product and service models, and operational data.

In addition, we have conducted an in-depth profiling of the user personas on the demand side of senior living real estate, leveraging authoritative research data.

This is an industry analysis report on senior living real estate with substantial strategic guidance value. This excerpt includes selected content from Chapters 1, 2, and 5 of the report; for full details, please refer to VCBeat’s “Research Report on China's Senior Living Industry》, the report totals 51 pages and contains over 50 charts and figures.

"Research Report on China's Elderly Care Industry" Table of Contents

I. Supply-Demand Imbalance Accelerates the Rapid Growth of Senior Housing Real Estate

II. Enterprises Seize the High Ground, with Platformization Becoming a Trend

2.1 Industry Development History: From Marketing Gimmicks to Strategic Industrial Layout

2.2 Business Model: Finding the Optimal Solution Between Corporate Demand and Profitability Risk

2.3 Refined Management and Platform Advantages: The Two Core Competitiveness Factors of Senior Housing Real Estate

2.4 List of Major Annual Events in China’s Senior Housing Real Estate Sector

3. Real Estate Developers and Insurance Companies Are the Main Forces in Senior Housing

3.1 Vanke’s “Suiyuan Series”: A Closed-Loop Elderly Care Service Model, Evolving from Senior Real Estate to the Broader Elderly Care Industry

3.2 Poly’s “Trinity” Elderly Care Industry Strategy

3.3 Beijing Hexihui Senior Apartment: Integration of Medical Care and Elderly Care, Leasing + Membership System

3.4 Taikang Insurance: “Insurance + Medical and Elderly Care” Enters the Senior Living Industry

IV. International Models

4.1 Japan: Driven by the Long-Term Care Insurance System, Comprehensive Development of High-, Mid-, and Low-End Facilities

4.2 United States: Separation of Investment and Operations, Highly Market-Oriented

V. Elderly User Needs: Greater Acceptance of the Leasing Model

VI. Trend Analysis: Short-Term Growth Depends on Consumer Spending Power, Long-Term Growth on Demographic Structure

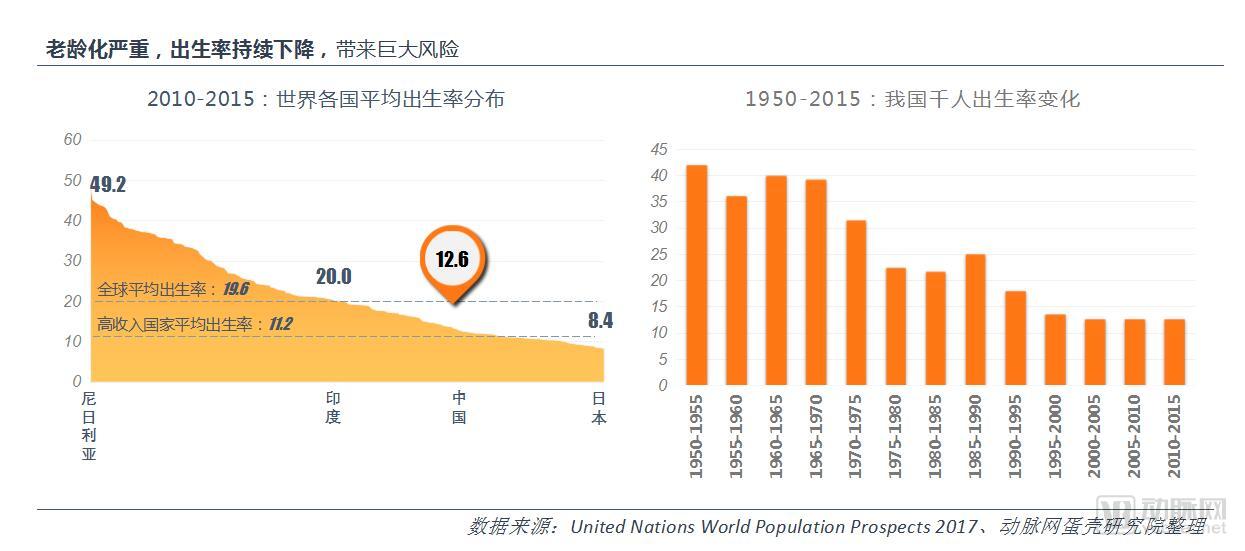

In 1983, the family planning policy was officially implemented in China. The national crude birth rate (per 1,000 population) declined from 24.9 in the late 1980s to 12.6 during 2010–2015. This figure is already lower than that of some developed countries, such as the United States, the United Kingdom, and Australia, and approaches the average level of developed nations.

From 1950 to 1970, China experienced its highest birth rates. Over the next two decades, as individuals born in the 1960s and 1970s gradually enter old age, the elderly population will increase substantially. The senior care industry, including senior housing real estate, will reap significant dividends from a surge in demand.

On the other hand, with improvements in living standards and healthcare service capabilities, the average life expectancy of Chinese residents has been increasing year by year. According to the latest data from the United Nations Population Division, the average life expectancy in China has risen from over 40 years in the 1950s to over 75 years currently. Furthermore, it is projected that the average life expectancy in China will surpass 80 years before 2050. The significant increase in the average lifespan of the existing population undoubtedly poses substantial challenges to China’s current elderly care service system.

The internationally accepted criterion for an aging society is that the proportion of residents aged 60 and above exceeds 10% of the total population.

According to international standards, China entered the ranks of an "aging society" as early as 2005. In the future, as population aging intensifies, both the number and proportion of elderly people in China will continue to rise. This trend is expected to persist until the second half of the 21st century, when the number and proportion of the elderly population in China will begin to decline.

Imbalance Between Supply and Demand in Elderly Care Institutions, with Prominent Contradictions

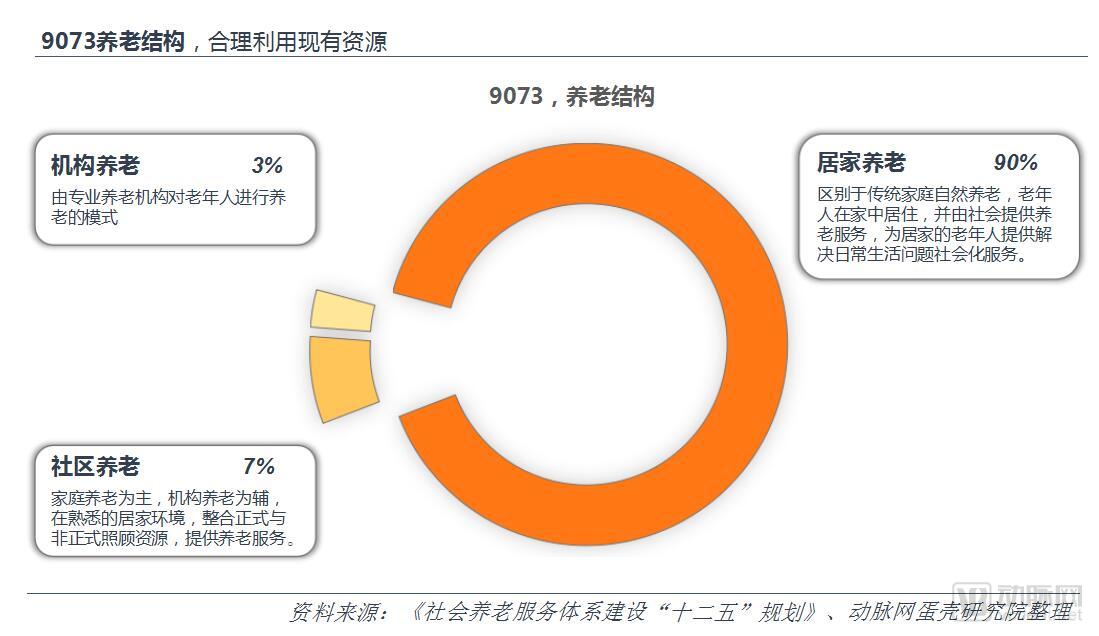

In light of residents’ lifestyle habits and national conditions, the Ministry of Civil Affairs proposed the “9073” elderly care model as early as 2011 in the issued “12th Five-Year Plan for the Construction of the Social Elderly Care Service System.” This model stipulates that 90% of older adults receive home-based care, 7% receive community-based care, and 3% receive institutional care.

90% Home-Based Elderly Care: Home-based elderly care refers to a model in which older adults reside in their own homes while receiving elder care services provided by society. This approach is distinct from institutional care and also differs from traditional family-based natural caregiving. Centered on the family, supported by the community, and driven by professional services, it delivers socialized services primarily aimed at addressing the daily living needs of older adults living at home.

7% Community-Based Elderly Care: Community-based elderly care is a model that prioritizes home-based care while supplementing it with institutional care. By integrating the advantages of both approaches, it enables older adults to access a comprehensive range of elderly care services without leaving their familiar home environments. This model combines formal and informal care resources to provide seniors with essential daily living assistance, emotional support, and healthcare services outside the home.

3% Institutional Care: Institutional care refers to a model in which professional elderly care institutions provide care services for the elderly.

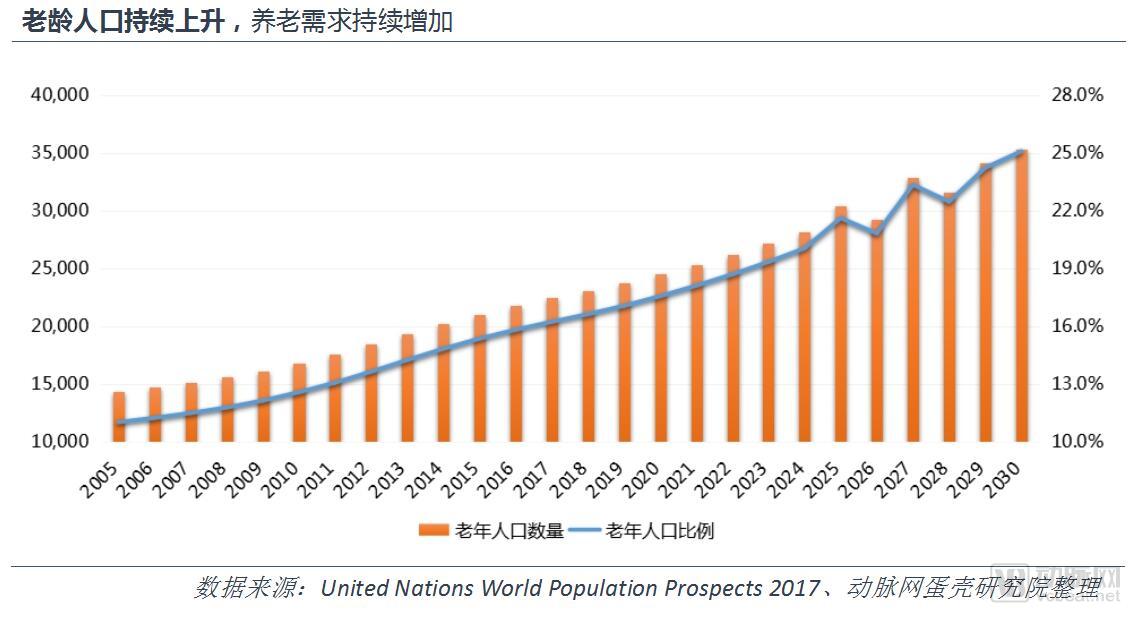

However, at present, there is still a certain gap between the service capacity of domestic elderly care institutions and the targets proposed by the “9073” elderly care plan. According to the 2017 Statistical Bulletin on Social Service Development, China currently has 31.6 elderly care beds per 1,000 people, which is lower than the 35–40 beds per 1,000 elderly population targeted in the 12th Five-Year Plan. This indicates that there is currently a shortfall of at least one million beds relative to the planning target.

The supply in the existing market struggles to meet current demand, while population aging and shifting consumption patterns have generated incremental demand. The increasingly prominent supply-demand imbalance has driven the reform and development of senior living real estate.

Getting Old Before Getting Rich: The State Promotes the Rapid Development of Senior Housing Real Estate

The degree of population aging is often highly correlated with a country’s level of economic development. During the process of economic growth, as income levels rise, residents’ birth rates gradually decline, leading the nation into an aging society. Most countries had already become developed nations through long-term, stable economic development before entering the aging phase. This means that although these countries have entered an aging society, their national productivity, legal systems, social security mechanisms, and elderly care-related service industries are already relatively well-developed, allowing the state to be better prepared to address the challenges posed by population aging.

In developed countries, the per capita GDP typically exceeded $5,000 to $10,000 when they entered an aging society. In contrast, China has entered an aging society prematurely, before achieving modernization and while its economy remains underdeveloped. Mu Guangzong, a professor at the Institute of Population Research of Peking University, stated that China’s aging trend is irreversible, yet its elderly care service system lags behind the demand for such services, a phenomenon described as “getting old before getting rich.”

“Getting old before getting rich” will undoubtedly have a significant impact on China’s economic development. As the issue of population aging intensifies, the government has placed increasing emphasis on the elderly care industry and has successively issued various policies. Since 2010, the density of policies related to senior housing real estate has gradually increased, with a particular surge between 2013 and 2016, primarily focusing on core issues in the elderly care sector such as finance and land use.

Industry Development: From Marketing Gimmicks to Strategic Industrial Layout

2000–2010: Elderly Care Real Estate as a Promotional Gimmick:

The concept of elderly care has begun to emerge, with real estate developers emphasizing “sales” rather than “services,” turning “elderly-care real estate” into a marketing gimmick within traditional property projects. Although some age-targeted services have been incorporated into property product design, the lack of subsequent operational management has resulted in poor-quality elderly care services and an immature business model.

2011–2015: Policy-Driven Development of Senior Housing Real Estate:

The senior living real estate model is gradually maturing, with developers offering increasingly diversified product formats. Various models have emerged, including integrated medical and elderly care (exemplified by Shui On Land’s Dongtan Ruici Garden, which hosts Ruijin Hospital within the community), migratory tourism-based elderly care (exemplified by Poly’s Sanya Haitang Bay project and Taiping Insurance Group’s Wutong Renjia), and academy-style elderly care (exemplified by Greentown’s Wuzhen Yayuan). However, senior care institutions still face challenges such as insufficient service capacity, a shortage of caregiving personnel, and the need for further improvement in facilities and equipment.

2016–Present: Endogenous Drivers of Industry Transformation, Enterprises Seizing Competitive High Ground:

The number of elderly care beds in China increased rapidly from 1.58 million in 2005 to 7.3 million by the end of 2016; investment in Public-Private Partnership (PPP) projects for elderly care surged from RMB 122.7 billion at the beginning of 2016 to nearly RMB 190 billion by August 2017. Due to the unique characteristics of senior housing real estate, the integrated medical and elderly care service model has become its core component. First-tier cities and developed regions have become key focal points for real estate developers’ strategic expansion.

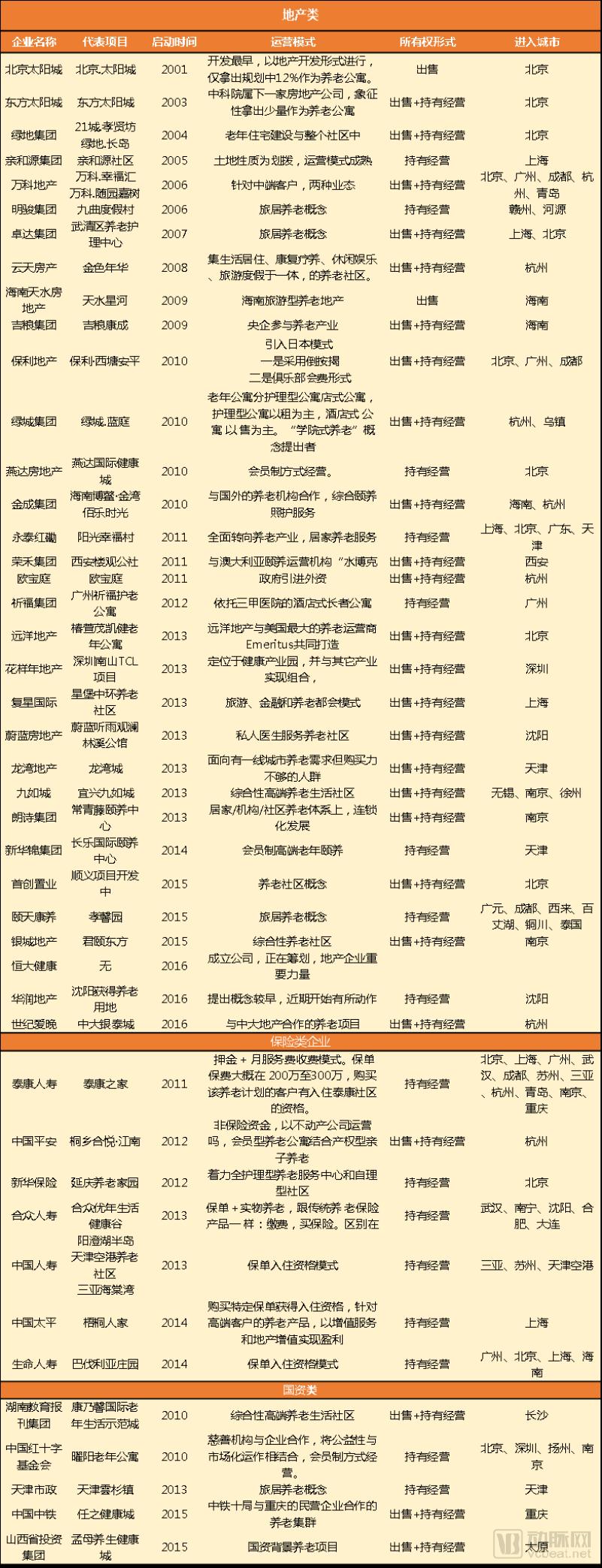

VCBeat has compiled a selection of key projects in the senior living real estate sector in recent years:

Business Model: Seeking the Optimal Solution Between Corporate Demand and Profitability Risk

From a demand perspective, elderly care scenarios can be categorized into four types: home-based care, community-based care, institutional care, and resort-style care. These four models collectively constitute China’s current elderly care service system. However, influenced by cultural values and income levels, family-based care remains the predominant model in China at present.

Based on different elderly care scenarios, the models of senior housing real estate can be categorized into five types: community-supported senior apartments, all-age communities, integrated senior living communities, medical-nursing combined communities, and wellness tourism communities.

In contrast to the singular and one-time nature of returns from traditional real estate projects, senior living real estate, which is service-centric, can generate stable and substantial profits through “services,” thereby enabling property developers to diversify their revenue streams. Overall, the profit models for senior living real estate can be categorized into three types: the sales model, the leasing or membership-based model, and the combined sales and leasing model.

The sales model is based on the concept of senior housing, involving the sale of property ownership rights while providing elderly care-related services and community support. Compared to traditional real estate projects, developers bear higher development costs due to the provision of services and supporting facilities.

The leasing model entails an excessively long payback period, imposing significant financial pressure on developers; however, it facilitates the establishment of brand influence and supports future brand-oriented development. Meanwhile, the high rental and service fees mean that such projects can only cater to seniors with strong purchasing power.

The “sale + lease” model represents a more balanced approach, entailing relatively lower financial pressure but demanding higher management capabilities from developers; determining the optimal ratio between leasing and sales is also critical.

Refined Management and Platform Advantages: The Two Core Competitiveness Factors of Senior Living Real Estate

Compared to traditional real estate projects, senior housing developments require adequate age-friendly facilities, high-quality elderly care services, and premium living environments. These essential facilities and offerings inevitably increase project development costs. Generally, investments in senior care facilities add at least RMB 1,000–3,000 per square meter to the cost of senior housing projects. For a medium-sized senior housing project with a gross floor area of 100,000 square meters, this translates into an additional investment of RMB 100–300 million.

Current senior living real estate projects primarily adopt two models—transfer of usage rights and sale of ownership—to achieve capital recovery. On one hand, the leasing model entails a long payback period, undoubtedly increasing the financial pressure on developers. On the other hand, while selling ownership can provide rapid capital inflow for real estate enterprises, it is difficult for senior living properties to command higher prices based solely on their elderly-care features, given the current consumption mindset of the older population.

Rising development costs, coupled with slow capital recovery and weak pricing power, have squeezed profit margins for real estate developers and exacerbated the risk of funding shortages. Therefore, compared to traditional real estate projects, senior living real estate operates on a razor-thin margin between profit and loss; any misstep could result in significant capital shortfalls, necessitating more refined management.

This means that during the initial development phase, real estate enterprises need to rigorously calculate the return on investment (ROI), achieve accurate pricing, and secure profit margins. On the other hand, they must also implement strict management of operational metrics during the post-development service phase, establish precise efficiency indicators, find a value equilibrium, and thereby achieve controllable risks and maximized profits.

Currently, most enterprises involved in senior living real estate emphasize platform development and industrial integration. This is primarily because the core of senior living real estate lies in delivering diversified value-added services through the integration of medical care and elderly care. “Medical services” constitute the primary value proposition of senior living real estate, while “elderly care services” serve as the main vehicle for enhancing quality of life. The delivery of these two types of services requires support from a range of essential elements. Compared with traditional real estate projects, senior living real estate represents a complex integrating multiple service formats; therefore, competition in this sector is essentially competition among platforms. Strong comprehensive platform competitiveness is key for senior living real estate companies to establish their moats.

Meanwhile, this also means that small real estate developers unable to integrate high-quality service resources will effectively be unable to establish a foothold in the senior living real estate industry. In the future, competition in senior living real estate will inevitably revolve around platforms, resource integration capabilities, overall corporate strength, integrated product-and-service offerings, and high entry barriers.

List of Major Annual Events in China’s Senior Living Real Estate Sector

The key participants in the senior living real estate sector can be categorized into three groups: first, well-established and experienced property developers such as Vanke, Poly Development, Fosun International, and Greenland Group; second, insurance institutions with substantial capital reserves, including China Life Insurance, Taikang Life Insurance, and Sino Life Insurance; and third, social capital firms seeking industrial expansion or profitable investment opportunities, such as Sequoia Capital China, Yunfeng Capital, and Harmony Capital.

Entering 2017, various players have been increasing their investments in the senior living real estate sector:

【Zhongnan Construction】In March 2017, it signed the “Government and Social Capital Cooperation (PPP) Project Contract for the Rencheng District Geriatric Care Center of Jining City Integrated Traditional Chinese and Western Medicine Hospital” with Jining City, with a total investment scale of RMB 666 million.

【Zhonghong Shares】In April 2017, it won the bids for two plots of A61 institutional elderly care facility land in Xiagezhuang Town, Pinggu District, Beijing, at RMB 496 million and RMB 660 million, respectively.

【Tongrentang】In May 2017, Beijing Tongrentang (Group) Co., Ltd. announced the establishment of the Tongrentang Elderly Care Industry Fund, with a capital size of RMB 1 billion, and simultaneously launched the Tongrentang Beijing Health and Elderly Care Project, marking the official implementation of Tongrentang’s national strategy for health and elderly care as a century-old brand.

[Nanjing Xinbai] In June 2017, it planned to acquire a stake in Nanjing Hekang Smart Elderly Care Industry Co., Ltd. through equity transfer and capital injection, with a total transaction price of RMB 122 million for a 51% equity interest, further accelerating its expansion in the home-based elderly care services sector.

【Greenland Group】and 【Fosun Star Castle】signed a cooperation agreement in June 2017 to establish an elderly care project in Foshan Zhangcha Future City; in July of the same year, Greenland Hong Kong reached a cooperation agreement with the Australian aged care services group ProvectusCare.

【China Resources Group】In August 2017, it acquired the first elderly care land plot in Liangqing District, Nanning, for a total price of RMB 1.046 billion; in the same month, it officially signed a cooperation agreement with the Tiexi District Government of Shenyang to build a demonstration zone for elderly care and health industries in Shenyang.

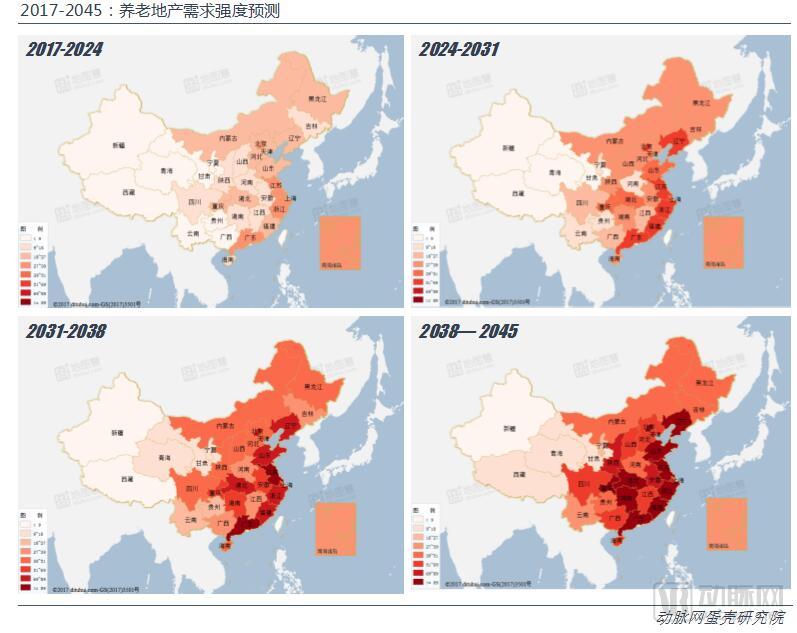

Given China’s vast territory, the demand for senior living real estate exhibits regional asynchrony due to disparities in local economic development levels and demographic structures. Furthermore, as time progresses and the economy develops, the landscape of these regional demand differentials will inevitably shift, leading to decreased demand in some areas and increased demand in others.

To determine the intensity of demand for senior housing real estate across different regions at various time points, we developed a demand model using multiple economic, social, and consumer behavior indicators, including income, urbanization rate, regional GDP and its growth rate, per capita savings, the absolute number of elderly individuals, and total population. Furthermore, we validated and refined the model based on relevant data from the historical development of Japan’s senior housing real estate sector.

The final model architecture was established and used to project the overall demand index for China’s senior living real estate industry from 2017 to 2045. A higher index indicates a greater total demand for elderly care services in that region. It is important to note that this model uses provinces, municipalities directly under the central government, and autonomous regions as the smallest analytical units; therefore, there are certain limitations when analyzing provinces with vast territories or complex demographic and economic structures. Taking Sichuan Province as an example, there are significant disparities in economic development across different areas within the province. In reality, Chengdu exhibits a strong overall demand for senior living real estate, and many industry players have prioritized Chengdu as a key city for their recent projects. However, due to uneven regional economic development, the analytical score for Sichuan Province as a whole remains relatively low.

The above is part of the content of this report. To download the full version, please scan the QR code below.

Scan the QR code below to become an official VCBeat member and receive the PDF version."2017 Research Report on the Senior Housing Industry". Moreover, over the coming year, you will enjoy unrestricted access to comprehensive industry trend reports, stay abreast of the latest global investment and financing developments, leverage a comprehensive database of healthcare enterprises, and gain access to extensive resource-matching opportunities.