Who Won the 2017 Mobile Health App Market: iOS or Android?

Today, the mHealth Economics program has been exploring digital health development for seven years. Since the release of the first report on the mobile health app market, a total of 6.7 million data points have been disclosed, revealing the market development of mobile health and digital health from 2010 to the present.

The Mobile Health Economics Project is the world’s largest digital health research initiative, with more than 15,000 participants since its inception.

About This Report

This report aims to reveal the current market landscape and future trends in digital health. It reflects the maturity of mobile health applications, market dynamics, and the direction of development.

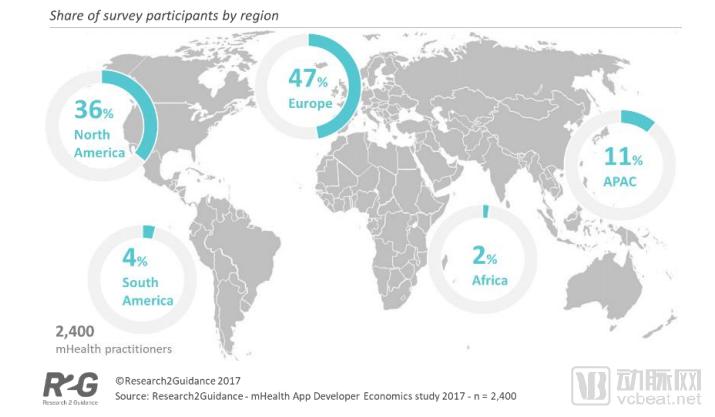

In 2017, more than 2,400 experts and decision-makers in mobile and digital health participated in market research and contributed to this report.

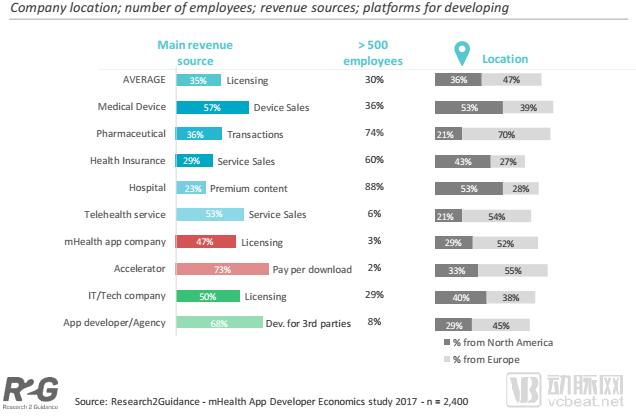

The report shows that the majority of digital health practitioners are from Europe (47%) and the United States (36%). 11% are from the Asia-Pacific region, while South America and Africa account for only a small proportion.

Participants included application owners and administrators, developers, project managers, physicians, and healthcare startups. Data were collected from 91 countries worldwide, with the 2,400 participants representing 3% of global medical app publishers.

Establishment of the Digital Health Submarket

Long before the advent of various digital health solutions, Apple had already launched the App Store in 2008. From this perspective, ten years is both a long and a short period. In the traditional healthcare industry, ten years merely spans a single product development cycle; whereas in the IT sector, a decade ago feels like prehistoric times.

The fast-paced IT industry and the slow-paced healthcare sector have long been in conflict, while digital health has brought disruptive changes to the market.

This report analyzes the current state of digital health. After a decade of market development, some early bubbles have burst, and industry leaders and followers have been clearly defined.

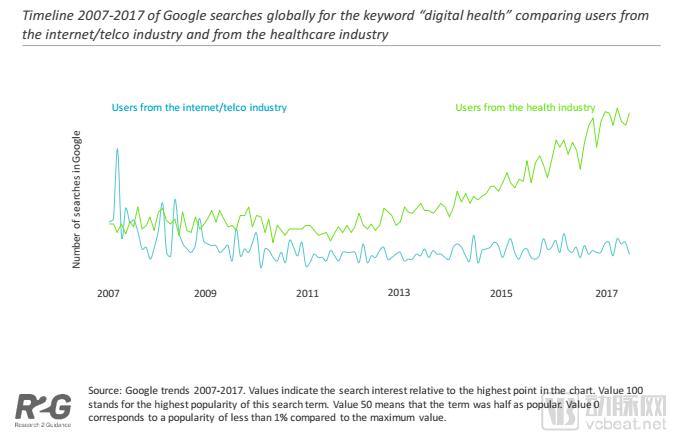

Data from the Google search engine reflects the search dynamics between internet and telecommunications companies (outsiders) and the healthcare industry (insiders). More than a decade ago, “digital health” was a popular search term. However, as the digital health market has expanded and matured, search volume for “digital health” among internet professionals has declined year by year, while interest within the healthcare sector has gradually intensified. Other topics, such as artificial intelligence, virtual reality, and the Internet of Things, have also become hot topics among these groups.

Although the hype surrounding mobile health has subsided, stakeholders in the healthcare industry are making relentless efforts to advance mobile health solutions. They continue to adopt new technologies, business models, and workflows, with some early digital health companies having grown into industry giants.

The 2017 Mobile Health Economy Report shows that some successful mobile health enterprises have established their market positions and set a direction for followers.

Digital Mobile Health Market Continues to Grow

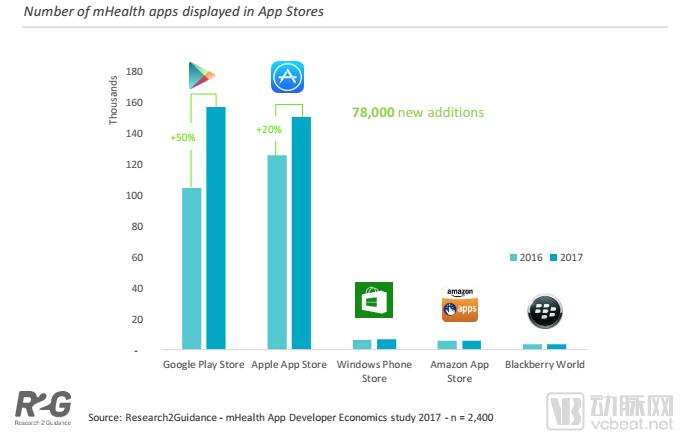

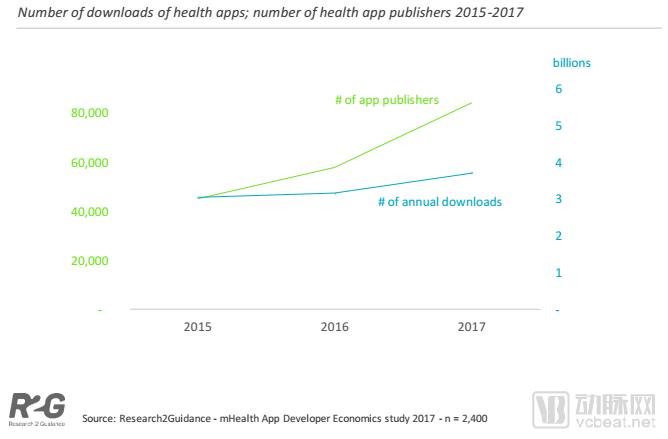

Over the past few years, the mobile health market has been growing steadily. In 2017, there were more than 325,000 healthcare apps in major global app stores, marking the highest record to date. From 2016 to 2017, mainstream global app stores added 78,000 new healthcare apps.

The growth of mobile health applications has been primarily driven by the increase in Android apps. The number of Android healthcare apps grew by 50% from 2016 to 2017, whereas iOS healthcare apps increased by only 20% over the same period. Currently, Android has surpassed iOS to become the leading platform for healthcare applications.

According to statistics, there are currently 325,000 healthcare and medical apps in the Google Play Store, surpassing the Apple App Store.

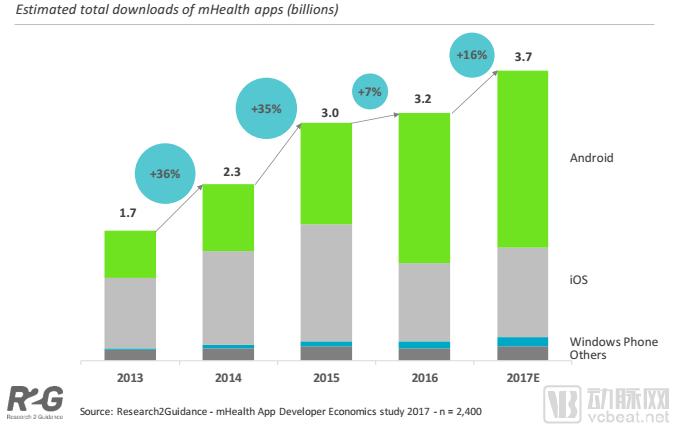

The aforementioned 325,000 medical and health apps achieved an estimated 3.7 billion downloads in 2017, representing a 16% increase from the previous year.

Android accounted for the largest share (estimated) of health and medical app downloads in 2017. Apart from Android and iOS, other app stores contributed insignificantly.

The healthcare industry is experiencing the same phenomenon as other sectors: the demand for mobile apps is accelerating.

In 2017, the estimated number of downloads for healthcare apps reached 3.7 billion, with Android app stores accounting for the largest share:

Compared with a few years ago, the growth rate of downloads has slowed down. Although app usage remains high, acquiring new users has become a challenging task, as the vast majority of users regularly use fewer than 20 apps.

On the supply side, the number of app developers continues to grow. By 2017, more than 84,000 app developers were creating apps for the healthcare market.

In 2017, the number of app developers increased by 45%. Consequently, they generally faced the dual challenges of rising supply and declining demand.

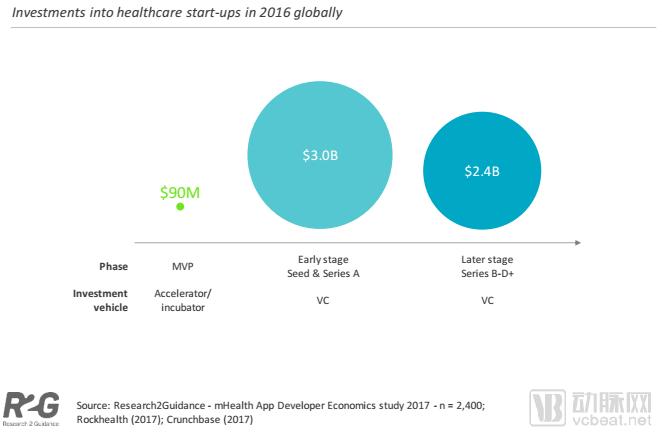

Another driver of growth in the digital health market is the expansion of startups fueled by early-stage investments from accelerators, incubators, and venture capital firms. Statistics show that by 2016, early-stage venture capital firms had invested approximately $5.4 billion in digital health startups worldwide.

In 2016, U.S. venture capital firms invested a total of $4.2 billion in digital health, slightly lower than the previous two years. In the first half of 2017 alone, investment surpassed the full-year total for 2016, making 2017 a record-breaking year for digital health.

The primary constraint facing the digital health market is the stringent and complex regulatory policy framework, which is widely regarded as one of the most significant factors contributing to the slow development of digital health solutions.

A survey by mHealth Economics found that 18% of digital health stakeholders were prevented by the healthcare sector from developing applications due to regulatory uncertainty. Digital and non-digital medical solutions that may pose risks to patient safety must be approved by regulatory authorities, such as China’s CFDA and the U.S. FDA.

However, there are signs that these agencies will undergo significant changes in their regulation of digital health in the future. In July 2017, the U.S. FDA announced a new approach to approving digital health solutions (known as the Digital Health Innovation Action Plan). Under this framework, each product from digital health companies would not need to go through traditional regulatory review and approval processes.

The FDA has launched a framework to regulate digital health solutions, which could serve as a blueprint for other countries to follow. Due to regulatory differences across nations, there are significant variations in target market selection for application developers subject to such regulations.

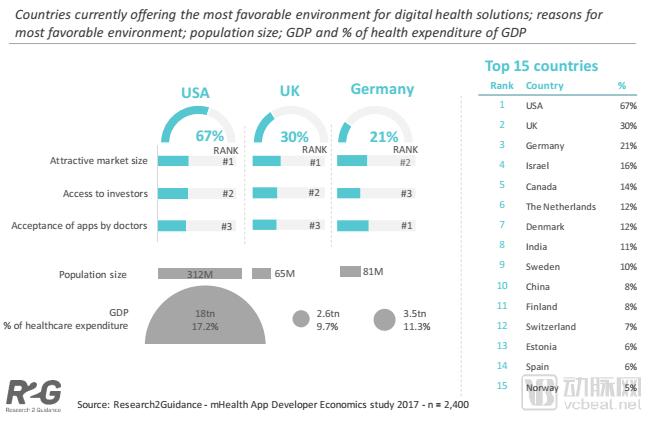

Currently, the countries with the most favorable market conditions for digital health solutions are the United States, the United Kingdom, and Germany. The United States (67%) is far ahead, while other leading countries include Israel (16%), Canada (14%), and the Netherlands and Denmark (both at 12%).

The two top-ranked countries (the United States and the United Kingdom) are attractive due to their “large market size,” followed by “ease of access to investment” and “physician adoption of apps.”

Although app developers tend to choose their own countries as the primary market, the United States undoubtedly has the best digital healthcare environment.

A comparison of GDP, population size, and healthcare expenditure share between the United States and the other top-three ranked countries (the United Kingdom and Germany) reveals the reasons for its attractiveness: the United States has the largest population (312 million), the highest GDP, and the highest proportion of gross domestic product allocated to healthcare.

The factors driving a country’s attractiveness vary significantly. However, entrepreneurs tend to favor markets that align with their company’s stage of development.

For example, startups seeking external investment tend to favor markets and countries where securing funding is easier.

Meanwhile, relatively mature companies in the expansion phase are more focused on countries that can offer “potential business partners” and where “physicians are more receptive to apps.”

Characteristics of Digital Health App Publishers and the Impact of Digital Intruders on the Healthcare Industry

In 2017, the types of mobile health app developers continued to diversify. The rise of mobile apps has enabled more digital health companies to assume the role of disruptors, and they have begun to emerge as a significant force in the healthcare industry.

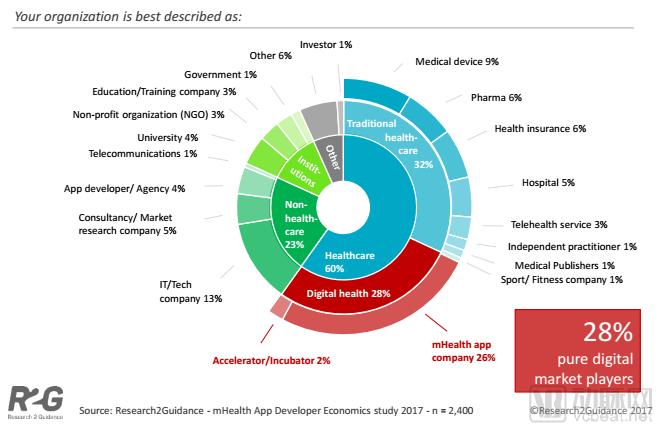

These digital disruptors (mHealth companies) constitute the largest group in the global digital health market, accounting for 26% of the market share. The traditional healthcare market is being penetrated by a new generation of digital disruptors, and “digital” business models are on the rise.

28% of the digital health market is occupied by pure-play digital market leaders, mobile health companies, accelerators, and incubators.

The non-digital segment of the healthcare market, comprising traditional healthcare service providers, remains dominated by industry giants. The largest groups among traditional healthcare companies are, in order, medical device manufacturers, pharmaceutical companies, health insurance providers, hospitals, and telemedicine service providers. Traditional healthcare companies have begun to view mobile health solutions as an extension of their core businesses.

Compared with other digital health markets, the profile of digital disruptors (mobile health app companies) is less clear. They are often European rather than North American. In terms of company size, they are well below the average.

It is hardly surprising that mobile health companies generate the most revenue through product licensing.

Other healthcare institutions adopt different commercialization models. For instance, application developers generate revenue through third-party development services, while medical device companies profit from equipment sales. Neither health insurance companies nor hospitals monetize their apps, as their development objectives differ. For example, their apps may be used to promote health insurance policies or support clinicians.

Digital Disruptors (mHealth App Companies) Vary Widely in Experience and Profitability. Compared with other digital health stakeholders, mHealth companies constitute a highly diverse group.

Among them, 14% of mobile health companies are highly experienced, having launched their first applications in 2010 or earlier, while 38% are newcomers with only one to two years of experience. Among mobile health app developers, 10% generate annual revenues exceeding $1 million, whereas 22% report annual revenues of less than $100,000.

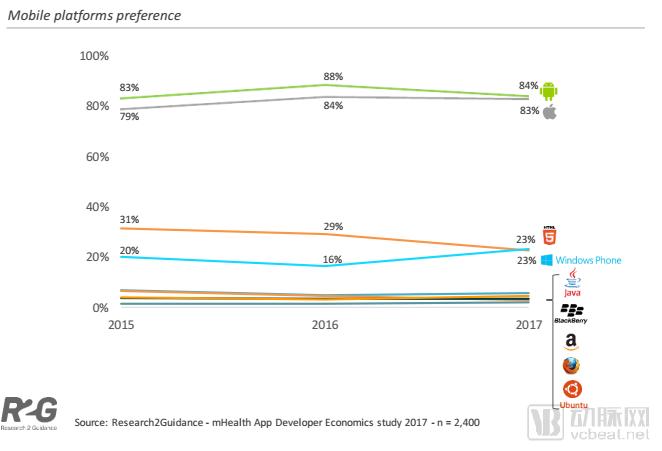

The term “platform war” is hardly unfamiliar. In recent years, there has been intense debate over which platform is best suited for app development. As it stands, two clear winners have emerged: iOS and Android (at least in terms of their appeal to mobile health application developers).

These two operating systems, which have been leading the field for years, will further converge in 2017.

Although Android’s popularity has remained at the same level compared to 2016, Apple’s iOS has begun to lose some of its appeal.

Among the other platforms, HTML5 mobile is losing its appeal to medical app developers, while Windows Phone has seen a slight increase. Java ME holds a 6% market share, and all other platforms play only a marginal role.

82% of mobile health developers are developing for at least two platforms, consistent with last year’s survey findings.

"Digital Invaders" (mHealth companies) are also increasingly adopting iOS, which is least attractive to telemedicine service providers.

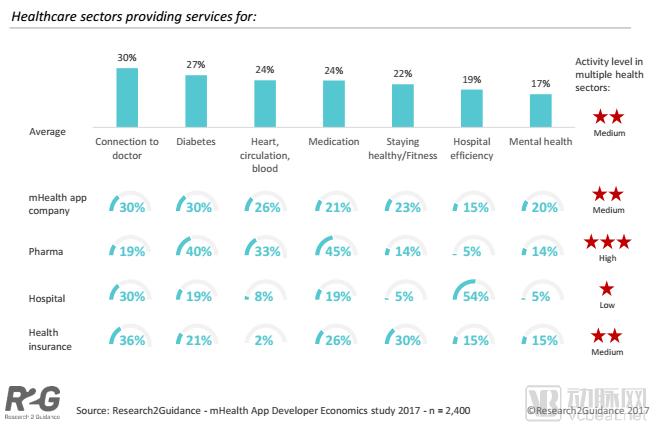

Health apps encompass a wide range of application scenarios. The most popular scenario, offered by 30% of market participants, is “connecting with doctors,” followed by “diabetes,” “heart and circulation,” and “medication.”

In a comparison among pharmaceutical companies, hospitals, health insurers, and mobile health companies, different organizations are using their applications as expected, though there have been some surprises.

Pharmaceutical companies are focusing on providing products and services for “drugs,” “diabetes,” and “heart and circulation,” while hospitals are developing apps to enhance “hospital efficiency.”

Mobile health companies focus on areas such as “weight management” or “mental health.” Health insurers are more active than average in the area of “health and fitness.”

Telemedicine companies focus on “hospital efficiency” and “medication therapy.”

“Connecting with Doctors” and “Diabetes” are the most popular mobile health application scenarios.

On average, each type of institution or company is involved in 3–4 subsectors. Some entities are more active; for instance, pharmaceutical companies are the most active across multiple subsectors, whereas hospitals, due to their high degree of specialization, are the least active in multiple subsectors.

Survey results reported in 2016 indicated that health insurance companies were expected to offer a wide range of application scenarios, from “chronic disease management,” “teleconsultation,” and “health education” to “electronic health records”; however, the 2017 results did not bear this out.

Digital and Mobile Health Continue to Attract New Entrants

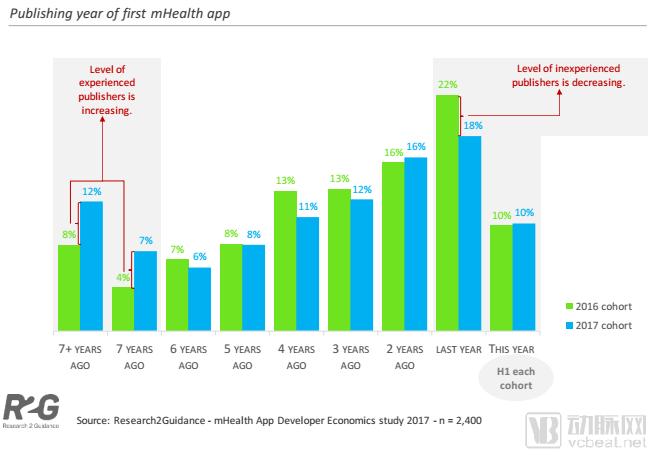

Creating a successful and sustainable digital health business depends on multiple factors. One key factor is the amount of time developers invest in their apps. Given that the digital health market is still relatively young, varying levels of experience contribute to differences among companies.

Most medical app developers are highly inexperienced. Of these, 28% launched their first app in 2017 or 2016. Only 19% of mobile health developers have more than seven years of experience.

This reflects that the mobile healthcare market remains highly attractive.

Compared with 2016, the number of newly listed digital health app developers (with less than two years of experience) decreased by 5%.

On the other hand, the number of experienced developers (with more than 7 years of practice) increased by 7%. Therefore, the industry's level of experience has been continuously improving over the years.

APP development experience also varies by geographic location. App developers from the United States have the most experience in medical apps, with 42% of such apps globally originating from the U.S. (compared to a global average of 36%).

Moreover, U.S. app developers boast more diverse business models and greater technological sophistication. The Asia-Pacific region has the largest number of developers (17% of inexperienced developers are from the Asia-Pacific region, compared to an average of 11%).

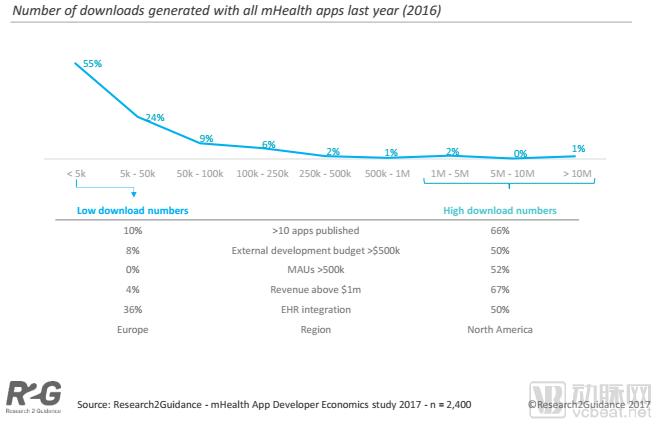

As many developers are novices, most apps do not exhibit significant annual download volumes. The majority of these apps garner only a few thousand downloads per year (55% have fewer than 5,000 downloads).

Nevertheless, 3% of developers still achieve annual downloads exceeding one million.

Compared with 2016, there was little change in the download categories of healthcare apps in 2017.

The downward trend in download volumes is consistent with the widening gap between supply and demand for mobile health apps. Although the overall quality of app developers has improved, annual download growth has not materialized, precisely due to the continuous increase in the number of health-related apps.

The disparity between developers with high download volumes and those with low download volumes stems from multiple factors. Generally, top-performing developers maintain their own app portfolios, thereby contributing to higher download counts.

On a technical level, developers with higher download volumes are investing more technology into their products and services. Furthermore, their external development budgets tend to be above average.

Currently, these technologies and investments are yielding returns. Mobile health app developers with high download volumes are attracting more users and generating higher revenues. Two-thirds of app developers with substantial download numbers have achieved revenues exceeding $100.

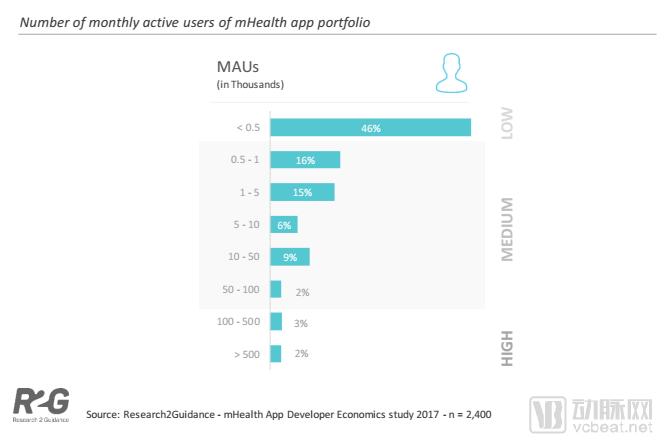

Low download volumes have also resulted in low monthly active user (MAU) counts for apps. Since most mobile health app developers recorded fewer than 5,000 downloads annually (in 2016), their MAU figures were likewise predominantly low.

Among developers of mobile health apps, 46% classified themselves in the lowest tier, with fewer than 500 monthly active users (MAU). Only a small fraction reported more than 50,000 MAU.

Outlook: Conditions and Technologies Shaping the Future of the Digital Health Market

The Mobile Health Economy Report provides market forecasts for the digital health industry. Leveraging seven years of data, it offers insights into the patterns and evolutionary trends within the digital health market.

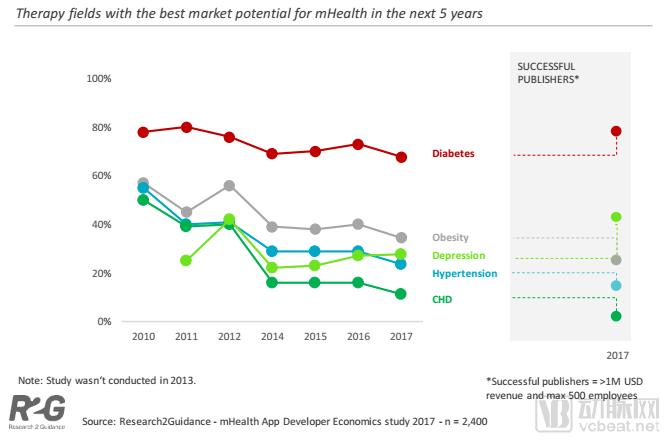

In the near future, diabetes will remain the most promising segment in the digital health solutions market.

Following diabetes, “obesity” and “depression” rank next. Although the prevalence of all chronic diseases has declined over the past six years, depression emerged as a prominent focus in 2017. Currently, depression ranks third among subsegments, demonstrating strong market potential.

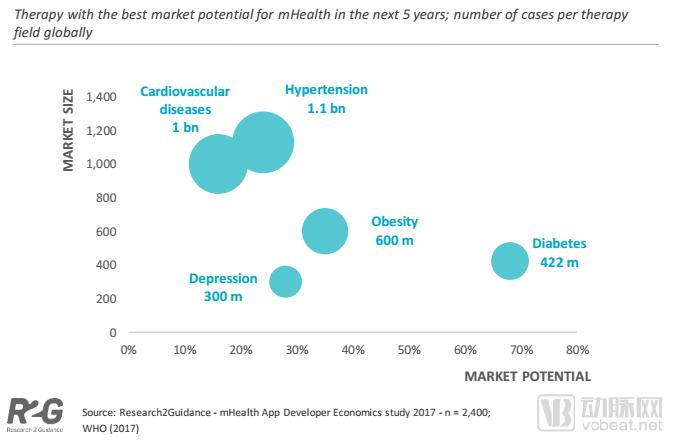

Diabetes and obesity hold the greatest market potential, yet they do not currently represent the largest markets.

Market potential is negatively correlated with actual market size. The conditions with the highest market potential are diabetes, obesity, and depression; however, their global case counts are lower than those of hypertension and cardiovascular diseases.

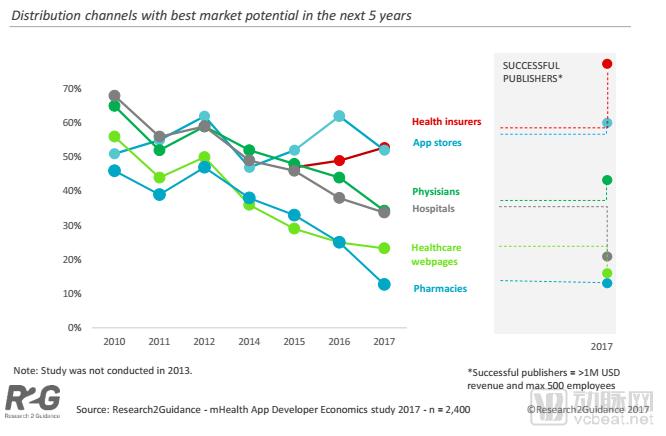

How Should Mobile Apps Find Users in the Future? For Years, the Answer to This Question Seems to Have Changed Significantly.

In 2017, health insurance companies were regarded as the most important distribution channel for the future. The popularity of health insurance companies as a distribution channel has been growing steadily, even surpassing “app stores” as the preferred distribution channel.

In the past few years, nearly all app distribution channels once deemed effective have disappointed developers. Consequently, mobile health distributors have suffered significant devaluation—with one exception: health insurance.

In 2010, “hospitals” and “doctors” were considered the most promising distribution channels for the future; however, within seven years, “medical websites” and “pharmacies” have taken center stage.

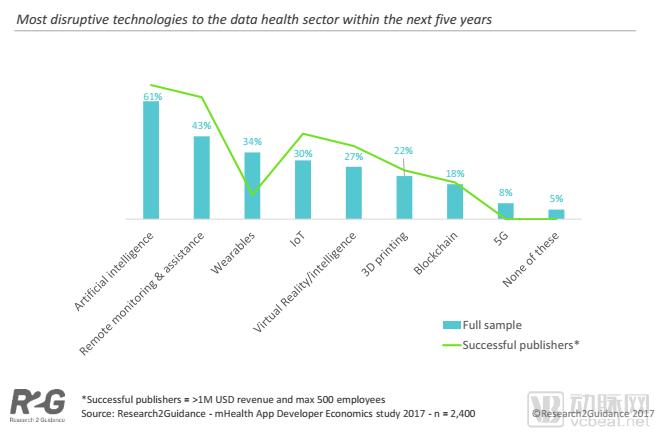

With the introduction of new digital technologies, new markets will emerge, and the entire industry will be reshaped. Which new technologies will reshape the future digital health market?

Artificial intelligence, blockchain, the Internet of Things, 3D printing, and other technologies that gained prominence in 2017 have impacted nearly every industry, with the healthcare sector being no exception.

The technologies with the greatest disruptive potential over the next five years are artificial intelligence and remote monitoring. Wearable devices, the Internet of Things (IoT), virtual reality, 3D printing, and blockchain rank second, while 5G has the least disruptive impact.

Top mobile health developers are more optimistic about new technologies, particularly remote monitoring, the Internet of Things (IoT), and virtual reality. However, they are not optimistic about wearable devices.

Although the digital health market is still in its early stages, some digital health stakeholders have already solidified their positions by developing products and services with robust business models. These established and successful stakeholders can serve as proven models, paving the way for a new generation of digital entrants.

Report Source: R2G-mHealth-Developer-Economics-2017-Status-And-Trends