2017 in Review: The Year of IPOs and Indigenous Innovation in China's Gene Industry

2017,The Gene Industry Sees Renewed Turmoil.With two industry leaders going public in succession, the tumor detection sector is poised for rapid growth following regulatory approvals, while microbiomics is gradually maturing under policy guidance, leading to a diversified industry landscape. Meanwhile, with the launch of domestically developed, independently innovated sequencers by MGI Tech and Hanhai Genomics, the battle for domestic substitution in the upstream sequencing sector has officially begun.。

Over the course of a year of tracking and observation, VCBeat published a total of 154 articles related to the genomics industry. During this period, we covered more than 20 companies and conducted nine data reviews spanning multiple subsectors, including liquid biopsy, non-invasive prenatal testing (NIPT), and data analysis and interpretation.

This year, we observed trends in tumor detection and domestic substitution within the genetic industry; and analyzed which company is most likely to pursue an IPO next, following the public listings of two leading enterprises.

This year, we engaged in dialogues with more than 20 industry experts, leveraging their insightful perspectives to discern potential industry shifts from the subtlest details.

This time, VCBeat has reorganized its 2017 reports on the gene industry. As we stand at the juncture between the old and the new, let us review the past and look toward the future.

I. 23andMe’s Year of Celebration

In 2017, the FDA approved 23andMe’s direct-to-consumer genetic testing products for Parkinson’s disease and Alzheimer’s disease. This marked the first direct-to-consumer genetic test approved by the FDA. Such a generous green light seems to signal that the FDA is intentionally moving toward the formalization and regulation of consumer genetic testing.

Some view this as the voice of the public; others see it as a lifeline for 23andMe; still others believe the FDA’s move is premature.

Whether it is acting too hastily or making full preparations, different people have different views, but practice will be the sole criterion for testing truth.

Click for Details: Green Light Given! FDA’s First Approval of 23andMe’s Consumer Genetic Test—Hasty Move or Well-Prepared?

A few months later, 23andMe announced the completion of its $250 million Series E financing round. Earlier, foreign media had reported that Ancestry, a competitor of 23andMe, had secretly filed for an IPO in June, sparking speculation: Is this latest funding round by 23andMe a preparatory step toward going public?

After more than a month of observation and verification, VCBeat has learned that 23andMe’s latest financing will not be used for an initial public offering (IPO). Instead, the funds will be directed toward expanding its Therapeutics Team and investing in comprehensive upgrades to its capabilities in handling genetic sample data.

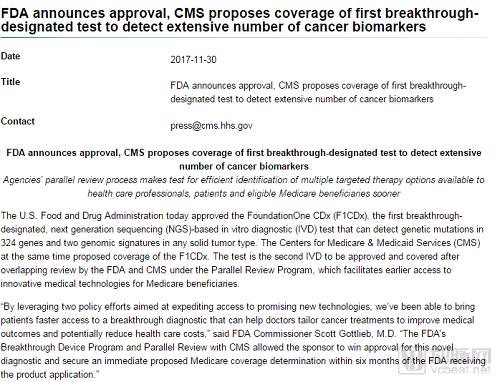

II. A Year of Sweeping FDA Reforms

In addition to genetic consumer products, the FDA has also undertaken sweeping reforms in the regulation of oncology testing.

On December 1, 2017 (Beijing Time), the FDA formally approved the marketing application for FoundationOne CDx (F1CDx). This is the first next-generation sequencing (NGS)-based in vitro diagnostic (IVD) multi-cancer companion diagnostic genetic testing platform approved by the FDA.

Concurrently with the FDA’s approval of the product, the Centers for Medicare & Medicaid Services (CMS) issued national coverage determinations for F1CDx and other similar NGS/IVD products, defining the scope of beneficiaries with advanced-stage cancer (i.e., recurrent, metastatic, or Stage IV cancer).

Compared with other FDA-approved diagnostic technologies or drugs, F1CDx offers unparalleled coverage. This product provides clinicians with a broader range of testing methods, thereby significantly aiding in the clinical diagnosis and treatment of cancer patients.

Furthermore, based on individualized test results, F1CDx assists clinicians in selecting the optimal treatment from 15 FDA-approved targeted therapy regimens for various solid tumors. It provides patients and healthcare professionals with comprehensive reports containing all relevant information, thereby avoiding the need for repeat biopsies.

In other words, this platform has transcended the “one drug, one test” model. This is perhaps the most significant implication of the F1CDx approval, marking a major step forward in bringing tumor genetic testing from the laboratory into clinical practice.

Click to view details: The First NGS-Based In Vitro Diagnostic (IVD) Multi-Cancer Companion Diagnostic Gene Testing Platform Approved by the FDA

That same month, the FDA issued two new draft guidelines on personalized medicine, outlining regulatory requirements for in vitro diagnostic devices in the development of molecular subtype–based targeted therapies and their clinical trials.

In the first draft guidance titled “Developing Targeted Therapies in Low-Frequency Molecular Subsets of a Disease,” the FDA explores how to stratify patients by molecular subtypes for enrollment in clinical trials of targeted therapies, particularly when one or more molecular subtypes are relatively rare.

The second draft guidance, titled “Investigational IVD Devices Used in Clinical Investigations of Therapeutic Products,” is designed to assist sponsors and Institutional Review Boards (IRBs) in conducting risk assessments for investigational in vitro diagnostic (IVD) devices used in clinical investigations of therapeutic products.

The new draft also addresses how to determine patient inclusion for clinical trials, summarize outcomes, assess and label benefits and risks, and further refine the target population for benefits, thereby clarifying and standardizing the clinical application of molecular diagnostics.

The final version will clarify the regulatory pathway for investigational in vitro diagnostic (IVD) devices used in clinical trials of therapeutic products, ensuring that trial results for novel targeted therapies are not compromised by the failure of specific biomarker diagnostic tests to meet regulatory standards. The draft aims to enhance the approval efficiency for personalized medicines and diagnostic systems, thereby accelerating their progress in the right direction.

III. A Year of Frenzied Financing in Tumor Detection

In January 2017, Illumina’s subsidiary specializing in early cancer screening launched its Series B financing round, with a target of $1 billion and a potential maximum of $1.8 billion.

This round of funding will be used to further develop and validate the company’s research on blood-based cancer detection, including the previously announced circulating cell-free DNA profiling study and other trials. The research requires large-scale clinical trials, with an expected enrollment of over 10,000 patients.

Moreover, Illumina also intends to accelerate the spin-off of Grail, with the proceeds from this transaction to be used for repurchasing the shares held by Illumina.

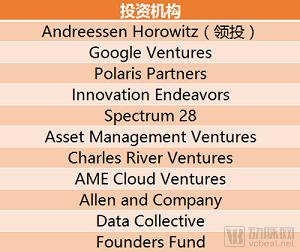

Two months later, the company successfully completed its financing as scheduled, with the first tranche of its Series B round raising up to $900 million, setting a new record for the highest funding in the liquid biopsy sector in 2017.

ARCH Ventures, the largest investor in the Series A round, continued its strong support by leading the Series B financing. In addition to venture capital firms such as McKesson Ventures, investors from the pharmaceutical and technology sectors also participated, including Johnson & Johnson, Amazon, Bristol-Myers Squibb, Celgene, Merck & Co., Varian Medical Systems, and China’s Tencent Holdings. Among them, Johnson & Johnson was the largest investor aside from ARCH Ventures.

Following the completion of its financing, Grail swiftly launched STRIVE, its second large-scale clinical trial after CCGA, to further advance its research on blood-based liquid biopsy technology for early cancer screening.

STRIVE is a large-scale prospective observational trial. The company plans to enroll 120,000 women and, by analyzing cell-free nucleic acids in their blood, develop and validate an early screening protocol for breast cancer.

The project will track these individuals for up to five years, and the data obtained will be used to train an artificial intelligence model. Furthermore, these data will support the future development and validation of Grail’s multi-cancer early detection screening.

Grail announced several major developments in 2017, but the most exciting was its merger with Cirina.

Cirina was co-founded in 2014 by Dennis Lo, Rachel Hui-Chun Chiu, and Junjie Chen from The Chinese University of Hong Kong, along with lead investor Decheng Capital. Headquartered in Hong Kong, the company’s research teams are based in Hong Kong and South San Francisco, California.

Dennis Lo is an authority in the field of non-invasive molecular diagnostics and screening, and the first scientist globally to discover cell-free fetal DNA in the blood of pregnant women. The three founders have made significant contributions by utilizing plasma nucleic acids for the detection of cancer and other diseases. Specific products and services have not yet been disclosed.

Following the merger, Dennis Lo will be appointed as Scientific Co-Founder and will join Grail’s Scientific Advisory Board. Min Cui, Founding Partner and Managing Director of CDH Investments, will join Grail’s Board of Directors as an observer. Maneesh Jain, CEO of Cirina, will also join the Grail team.

Following the merger, Grail will continue to develop its global commercial product markets, including those in Europe, the United States, and Asia. As an operating subsidiary of Grail, Cirina will continue its research collaboration with The Chinese University of Hong Kong and further deepen this relationship.

Massive financing, large-scale trials, and strategic mergers made 2017 a whirlwind year for Cirina, but its competitors were far from idle.

#1 competitor Freenome announced its financing news on the same day as Grail.

Freenome is a liquid biopsy diagnostics platform that has been in operation for two years, leveraging cell-free DNA (cfDNA)-based liquid biopsy technology to conduct research on early cancer screening. In 2017, Freenome raised $65 million in Series A financing, led by Andreessen Horowitz (a16z), which had also led its $5.5 million seed round one year earlier. Other investors included Google Ventures and Founders Fund.

Contestant No. 2, Guardant Health, also secured a substantial amount of financing during this year. In May 2017, the company announced that it had raised up to $360 million in its Series E funding round and planned to sequence tumor DNA for more than one million cancer patients within five years.

Previously, Guardant Health had already conducted testing in 40,000 individuals. This round of financing will expand Project LUNAR, the early cancer detection initiative announced by Guardant Health in 2016.

In addition to these prominent overseas companies, domestic tumor liquid biopsy companies also performed remarkably well in 2017.

On November 2, 2017, Annoroad Gene Technology announced the completion of its latest round of financing, raising nearly RMB 700 million. The round was co-led by Shenzhen GTJA Investment Group and Ping An Venture Capital, with other investors including SoftBank China Capital and SAIF Partners China.

The funds raised by Annoroad in this financing round will be used to support the company’s global expansion, talent system development, R&D investment in technology, and industrial investments.

Geneseeq also completed a new round of financing amounting to hundreds of millions of RMB in July. Through this round, Geneseeq successfully introduced a number of well-known investment institutions in China’s healthcare industry, including Industrial Securities Innovation Capital (a wholly-owned private equity fund subsidiary of Industrial Securities), Boyuan Hongsheng, Huatai Ruihe Healthcare Industry Fund, and Cowin Capital.

Click for details: Geneseeq Completes New Round of Financing Worth Hundreds of Millions, Continuing to Lead in Tumor NGS and Liquid BiopsyWorld

Benchmark Medical also completed a $28 million Series B financing round in November. The round was co-led by Alliances Healthcare Venture Capital and Sijia CCB Fund, with other investors including the renowned U.S. venture capital firm Arch Venture Partners, WuXi AppTec, and KingMed Diagnostics. Yuan Yi Capital, an investor from the previous round, continued to participate.

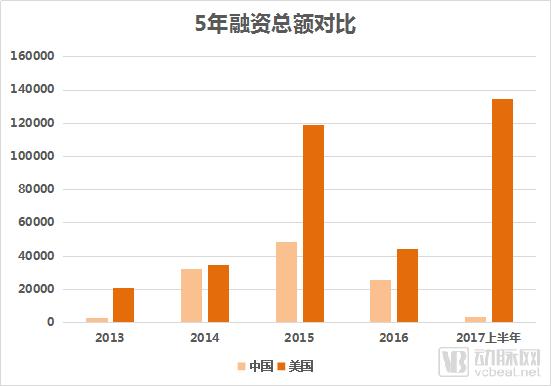

In addition, companies such as Feishuo Biology and Youxun Medicine have also successfully completed their financing rounds. In 2017, the domestic tumor NGS liquid biopsy sector attracted over RMB 2 billion in funding.

What lies behind this trend? Why did capital pour heavily and frequently into this niche sector in 2017, almost in unison? Here, we offer a brief analysis.

Behind the frenzy of financing lies a new industrial ecosystem driven by technological and industry maturity, as well as new opportunities created by regulatory approvals.

As we can see, China’s entire biotechnology industry, driven by both technological advancements and policy support, is rapidly catching up with Europe and the United States.

V. The Tenth Anniversary of the Emergence of NIPT Technology

So, what has happened in the NIPT industry, which matured prior to cancer detection?

On January 4, Washington time, five leading genetic testing companies—Counsyl, Illumina, Progenity, Natera, and Laboratory Corporation of America’s specialty lab, Integrated Genetics—jointly announced the establishment of the Coalition for Advanced Prenatal Screening (CAPS).

It was revealed that CAPS will work together to better achieve non-invasive prenatal screening through cell-free DNA (cfDNA)-based non-invasive prenatal testing (NIPT), raise public awareness of the value of cfDNA-based NIPT, and provide services of the highest standards and quality. Meanwhile, CAPS will also be committed to promoting relevant legislative development and insurance coverage to enhance patients’ personalized care experience.

Dr. Arnold W. Cohen, Honorary Chairman of Einstein Healthcare, serves as the Chairman of the Clinical Advisory Board within the Alliance. Under his leadership, the Alliance is establishing a Clinical Advisory Board to provide the public with an independent medical perspective.

In China, although no similar alliance has been established, NIPT has achieved successful commercialization in the market after ten years of development and has played a significant role in the prevention and control of birth defects.

This technology is disruptive, meeting the bidirectional needs of clinical practice. Furthermore, during the one-year pilot period for its removal, governments at various levels and enterprises provided varying degrees of subsidies and price concessions for testing.

As the coverage area expands, public acceptance of NIPT is also increasing. Improved regulatory frameworks and reduced costs have enabled the technology to reach primary-care hospitals.

To enable more people to benefit from non-invasive prenatal testing (NIPT), incorporating it into medical insurance coverage would be the most effective measure. As early as 2011, local governments began to successively establish pricing standards for NIPT.

Currently, the price bureaus of five provinces—Guangdong, Sichuan, Jiangsu, Hubei, Fujian, and Zhejiang—have established pricing standards for non-invasive prenatal testing (NIPT). However, only Shenzhen City and Qianxinan Prefecture in Guizhou Province have included NIPT in their maternity insurance coverage.

Nevertheless, local governments have long since shouldered the cost of birth defect prevention and control.Beyond NIPT, various regions have introduced subsidy policies for prenatal screening and diagnostic procedures such as serological screening, amniocentesis, and ultrasound examinations, with some even offering these services free of charge nationwide.

Therefore, we can anticipate that the inclusion of NIPT in medical insurance coverage may not be far off.

Click for details: A Decade in the Making—What Is the Current Clinical Status of NIPT?

VI. The First Year of NGS Commercialization in China

In 2017, the most exciting development in China’s NGS sector was the initial public offerings of two leading companies.

After two prospectus filings and one suspension of review, BGI Genomics finally listed on the A-share market in July 2017.

“Or listed in 2016,” “Earliest listing in March”—rumors about BGI Genomics’ IPO have never ceased. Now, with the bell-ringing ceremony on the A-share market, BGI Genomics (300676) has officially been listed and issued, bringing all speculation to a close.

Click for Details: BGI Genomics Goes Public Today—A Review of Its 18-Year Journey

Also going public this year is Berry Genomics. Perhaps when Zhou Daixing jotted down the mathematical model on a plane, he did not realize that this seemingly simple model would usher him into a magnificent new world, and that his efforts, together with those of his global peers, would spark a profound revolution in prenatal screening technology.

In just eight years, this young company has spawned and shaped an entire industry, growing from a three-person team into a publicly listed corporation valued at tens of billions.。

With the IPOs of two leading companies, we must ask: In the vast NGS market, who will be the next lucky winner?

By reviewing the primary and secondary markets, we compared the basic information of several leading companies and analyzed their likelihood of going public in the coming years.

VII. The Year the $100 Genome Arrives

For the global market as a whole, the most exciting news for sequencing professionals in 2017 was undoubtedly the further decline in sequencing costs.

At the J.P. Morgan Healthcare Conference on January 9, global genetic testing giant Illumina announced the launch of its NovaSeq series sequencers. With unparalleled throughput, streamlined operation, low cost, and flexibility, the system reduces the cost of gene sequencing to $800.

The NovaSeq series also achieves a breakthrough in sequencing speed. While the HiSeq X requires 72 hours for whole-genome sequencing, the NovaSeq series reduces this time to 40 hours.

Although the $100 genome has not yet been truly realized, Illumina states that this goal will be achieved in the coming years. The launch of the NovaSeq system at least marks the advent of the era of hundred-dollar-level gene sequencing.

VIII. The Year of the Rise of Domestic Innovations

NovaSeq may be Illumina’s ultimate weapon in the sequencer market, as well as another sharp sword for its global expansion in the sequencing industry.

Similarly, the domestic upstream NGS market has also seen substantial gains. In October 2017, MGI Tech, a subsidiary of BGI Genomics, launched two high-throughput sequencers: the MGISEQ-2000 and the MGISEQ-200.

MGISEQ-2000 is built upon the BGISEQ-500 dual-chip independent operating platform, with two additional chip specifications introduced to provide users with more diverse options. A single run can generate up to 600 Gb of output data. Under full load in PE100 read length mode, it completes sequencing in less than 48 hours, achieving an annual throughput equivalent to more than 1,000 human whole-genome datasets.

The MGISEQ-200 retains the convenience and flexibility of the BGISEQ-50. Operating at full capacity in PE100 read length mode, it generates 60 G of output data in less than 48 hours, enabling rapid testing of an average of 24 tumor samples per day.

Jiang Hui, Vice President of MGI Tech, stated at the launch event, “The MGISEQ-2000 and MGISEQ-200 represent another perfect integration of intelligence and technology.”

In addition, Hanhai Gene launched its own third-generation sequencer in 2017, which received CFDA approval for clinical-grade sequencing.

This is also currently the only third-generation gene sequencer for clinical applications worldwide.According to the company, its technology has reached a world-leading level. Once the product is mass-produced and commercialized, the cost of whole-genome sequencing will plummet from the current $1,000 for second-generation sequencing to $100, while the sequencing turnaround time will be significantly reduced—from one week for second-generation sequencing to just one day.

Annuoda, in collaboration with Illumina, officially launched the NextSeq 550AR, a new desktop high-throughput gene sequencer registered and certified by the China Food and Drug Administration (CFDA). Concurrently, it released a CFDA-certified kit for detecting fetal chromosomal aneuploidies (T21, T18, and T13) based on the NextSeq 550AR sequencing platform, utilizing reversible terminator sequencing technology.

The launch of the NextSeq 550AR signifies that Annoroad has completed its layout across the entire industry chain, with business operations spanning upstream instrument and reagent manufacturing, midstream sequencing centers and cloud storage platforms, as well as downstream medical and scientific research testing services.

We can see that after years of cultivation, the leading companies have begun to layout in the upstream field. With the emergence of companies mastering core technologies, Chinese NGS companies are moving towards self-sufficiency.

In August 2017, MGI Tech reached collaborations with Agilent Technologies and LC-Bio in succession. This marked the first collaboration among upstream manufacturers of instruments and reagent consumables for the next-generation sequencing (NGS) industry in China.

Throughout the NGS industry chain, the upstream sequencer market is unquestionably its core. BGI Genomics is the leader in the field of high-throughput sequencing, while MGI Tech has taken over the research, development, and manufacturing of its sequencing instruments. The recent collaboration in the upstream market for instruments, reagents, and consumables signifies the initial formation of an independently innovative ecosystem within the industry. The integration of equipment with supporting reagents has paved the way for independent innovation in China’s NGS sector. As Hang Xingyi, Founder and CEO of AccuGen, stated, this marks the launch of a “Belt and Road” initiative for Made-in-China NGS products.

Seven or eight years ago, Chinese-made smartphones seemed synonymous with knockoffs, and the vast majority of consumers held foreign brands such as Apple and Samsung in high esteem. However, with the rise of domestic brands like Huawei, Xiaomi, OPPO, and Vivo, Chinese smartphone brands have gradually gained a voice in both the domestic and international markets.

Similar to the smartphone market, after more than a decade of development in China, Chinese brands in the NGS industry are also gearing up for a wave of independent innovation.

Click to view details: Competing on Technology or Service? How Can Chinese High-Throughput Sequencing Companies Fire the First Shot in Their Turnaround Battle?

9. The Year the Earth BioGenome Project Was Launched

In 2017, following the Human Genome Project, the field of life sciences was set to witness another major milestone: BGI Group and the Smithsonian’s Genomics of Biodiversity Program jointly launched the Earth BioGenome Project (EBP), a grander initiative than the Human Genome Project, which was poised for imminent launch.

Under this initiative, scientists worldwide will sequence not only animals and plants but all eukaryotic organisms on Earth.

Click for details: After the Human Genome Project, BGI launched an even more ambitious project

Outlook | 2018

2017 has passed; what opportunities will the genetic testing industry have in 2018?

We have already witnessed the success of the NIPT industry. There is no doubt that with the CFDA’s approval of oncology testing kits, clinical diagnostics will once again surge with new vitality.

In recent years, tumor medication testing has primarily focused on targeted therapies. However, with the submission of Innovent Biologics’ PD-1 drug marketing application and the advancement of clinical trials by companies such as Baice Shenzhou and Junshi Biosciences, companion diagnostics for immune checkpoint inhibitors are poised for significant development.

The rise of NGS technology has not only driven the development of human genetic testing, but also promoted the detection of microorganisms closely associated with the human body.

Prior to the application of next-generation sequencing (NGS) technology in microbial sequencing, microbiome research was confined to the level of single organisms and qualitative analysis, with the understanding of microbial detection limited primarily to infectious diseases. NGS has enabled multi-pathogen detection and quantitative analysis, revealing correlations between many diseases previously thought to be unrelated to the human commensal microbiota—such as diabetes and depression—and these microbial communities.

“Which other diseases are associated with microbes, and what are the mechanisms by which microbes influence human health? With the application of next-generation sequencing to microbial sequencing, these questions have been revisited and reexamined.”

The completion of the Human Genome Project has provided humanity with a preliminary understanding of its genetic map. Nevertheless, it remains true that phenotypic traits are determined by both genetic factors and external environmental influences. To achieve a deeper understanding of genetic mechanisms, it is essential to investigate not only intrinsic factors but also extrinsic ones.

“The 13th Five-Year Plan for Special Projects in Biotechnology Innovation” listed the development of microbiomics as a frontier key technology requiring breakthroughs. Guided by policy trends, research related to microbial genomics is bound to usher in significant space for development.

Above is VCBeat’s review and outlook on the gene industry. We uncover the underlying logic from discrete data, and we build our understanding of the industry through exchanges with entrepreneurs and investors.

Over the past year, thank you for your support and attention to VCBeat.What stories will 2018 bring? As observers and chroniclers of the healthcare industry, we share your anticipation!